Quick Navigation

Report Overview

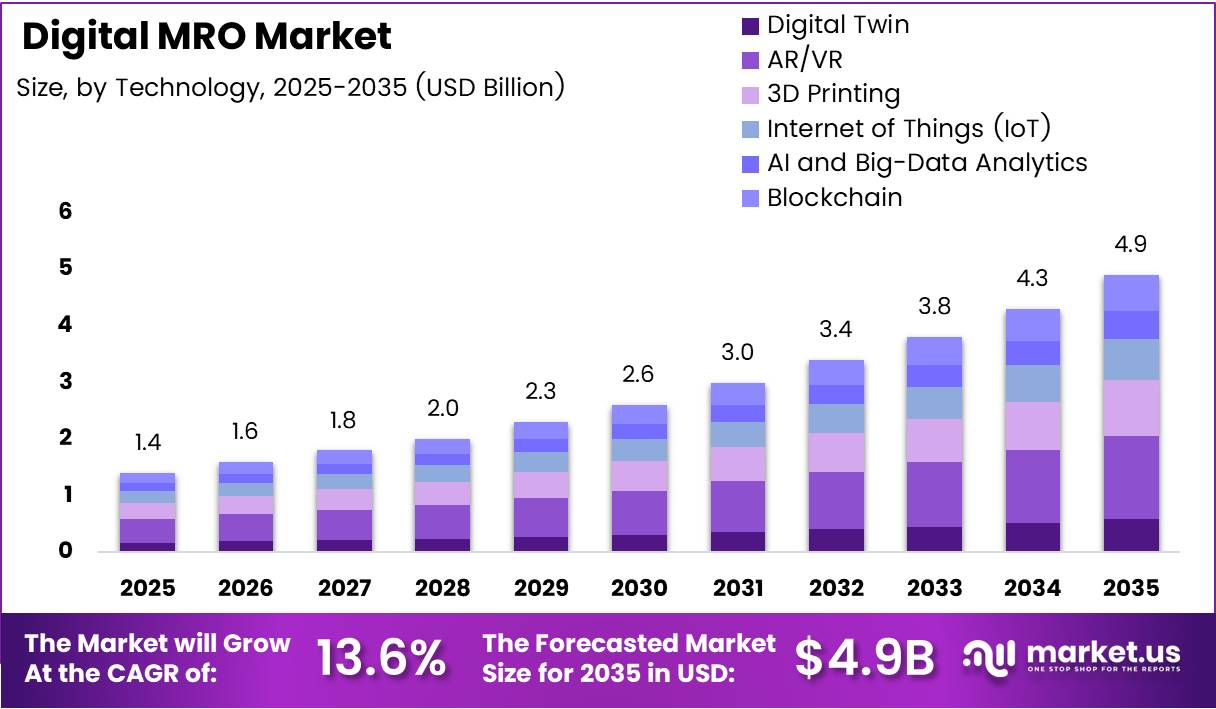

Global Digital MRO Market size is expected to be worth around USD 4.9 Billion by 2035 from USD 1.4 Billion in 2025, growing at a CAGR of 13.6% during the forecast period 2026 to 2035.

The digital MRO market covers technology-enabled maintenance, repair, and overhaul solutions for commercial and military aviation. These platforms replace paper-based workflows with connected systems — integrating sensors, analytics, and real-time data to manage aircraft health across entire fleets. The shift is structural, not cyclical, as operators face mounting pressure to cut ground time and reduce unplanned failures.

Aviation maintenance has historically been reactive — technicians inspect, identify faults, and repair. Digital MRO inverts this model by enabling condition-based and predictive strategies. Aircraft generate continuous streams of health data, and the platforms in this market convert that data into actionable maintenance schedules. This directly reduces the most expensive event in commercial aviation: an unscheduled aircraft-on-ground incident.

Fleet expansion across Asia Pacific and the Middle East creates sustained demand for scalable maintenance infrastructure. Airlines in these regions increasingly lack the legacy systems that Western carriers must replace, making them natural adopters of cloud-based and mobile MRO platforms from the outset. This greenfield dynamic gives digital-native vendors a structural entry advantage in high-growth aviation markets.

The regulatory environment reinforces digital adoption. Aviation authorities in North America and Europe now require traceable, auditable maintenance records — a standard that paper-based systems cannot reliably meet. Digital MRO platforms address this compliance requirement directly, making them operationally necessary rather than discretionary investments for certified carriers and MRO providers.

Technology convergence is accelerating capability. Digital twins, AI-driven diagnostics, AR-assisted repair, and IoT sensor networks are no longer standalone tools — vendors now bundle them into unified MRO ecosystems. This integration raises switching costs for airline customers and creates durable competitive moats for platforms that achieve fleet-wide deployment early.

According to oxmaint.com, airlines implementing digital twin technology for maintenance documented maintenance cost reductions averaging 28–35% across their fleets in 2025. A reduction of this scale does not represent incremental efficiency — it signals a fundamental repricing of maintenance economics that operators without digital platforms cannot match competitively.

According to oxmaint.com, 92% of companies implementing digital twin maintenance achieve ROI above 10%, with typical payback periods of 12 to 36 months. This near-universal return profile removes the financial risk argument against adoption and positions digital MRO investment as a measurable, time-bound capital decision rather than a speculative technology bet.

Key Takeaways

- The Global Digital MRO Market was valued at USD 1.4 Billion in 2025 and is forecast to reach USD 4.9 Billion by 2035, at a CAGR of 13.6%.

- By Technology, Augmented Reality/Virtual Reality (AR/VR) leads with a 26.8% market share in 2025.

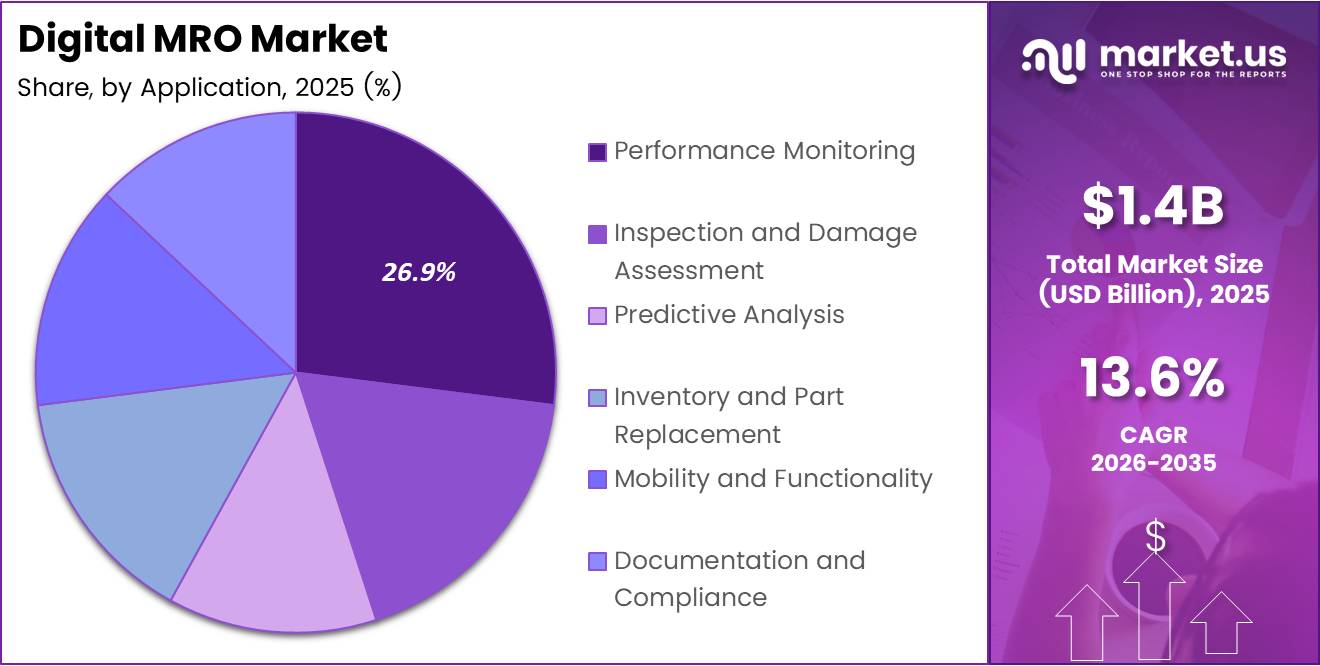

- By Application, Performance Monitoring holds the dominant position with a 26.9% share.

- By End User, Airlines represent the largest segment with a 43.1% share of the market.

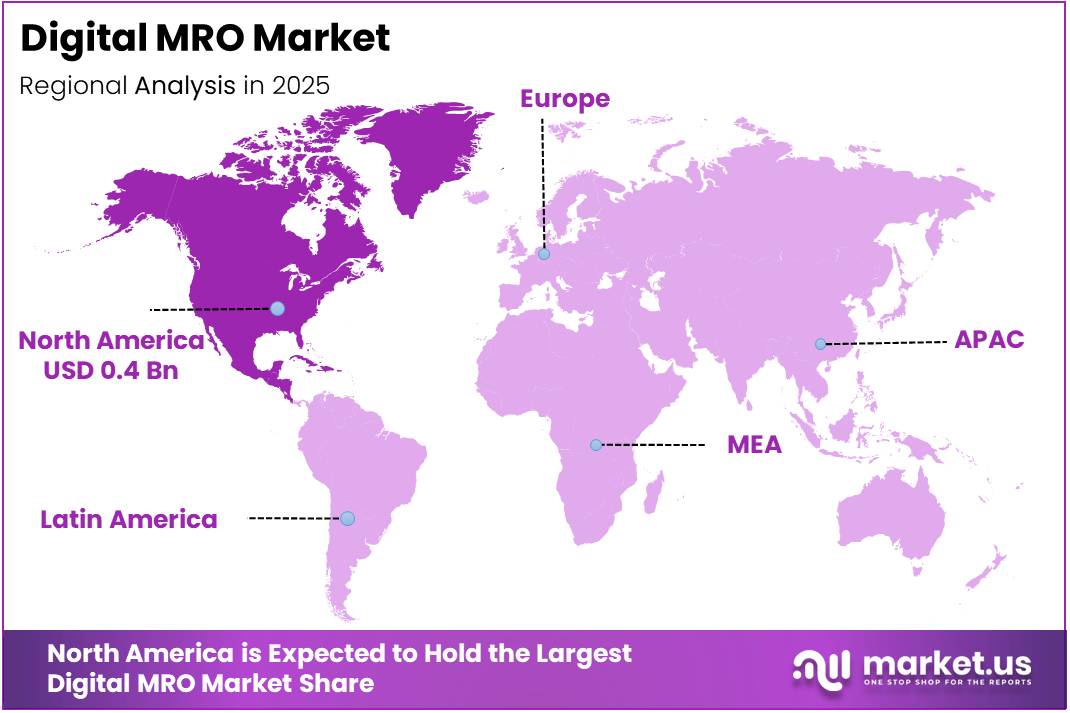

- North America dominates the regional landscape with a 34.80% share, valued at USD 0.4 Billion in 2025.

Technology Analysis

Augmented Reality/Virtual Reality (AR/VR) dominates with 26.8% due to direct technician productivity gains on the floor.

In 2025, Augmented Reality/Virtual Reality (AR/VR) held a dominant market position in the By Technology segment of the Digital MRO Market, with a 26.8% share. AR/VR overlays real-time repair instructions, wiring diagrams, and inspection checklists directly onto a technician’s field of view — cutting lookup time and reducing human error. This hands-free workflow improvement explains why airlines prioritize AR/VR deployment ahead of other digital tools.

Digital Twin technology creates a continuously updated virtual replica of each aircraft’s physical components, enabling maintenance teams to simulate failure scenarios before they occur in service. According to eajournals.org, digital twin-based scheduling has reduced annual maintenance costs by an average of USD 3.6 million per wide-body aircraft while increasing operational availability by 7.3%. These figures reframe digital twin investment as a revenue-protection tool, not just a cost-saving measure.

3D Printing addresses one of the costliest bottlenecks in aircraft maintenance: parts availability. When a certified replacement part is unavailable, an aircraft sits on the ground. Additive manufacturing allows MRO providers to produce low-volume, certified components on demand — reducing AOG duration and cutting inventory carrying costs simultaneously.

Internet of Things (IoT) forms the data collection layer for the entire digital MRO ecosystem. IoT sensors embedded in engines, landing gear, and avionics generate continuous health signals that feed predictive algorithms and digital twin models. Without this sensor infrastructure, AI analytics and digital twins operate on historical data rather than live aircraft condition — significantly reducing their accuracy.

Artificial Intelligence (AI) and Big-Data Analytics convert the raw sensor data collected by IoT networks into maintenance decisions. AI models identify anomaly patterns across thousands of flight cycles that no human analyst could process manually. The strategic implication is clear: airlines with larger fleets generate more training data, giving them a compounding accuracy advantage over smaller operators using the same platforms.

Blockchain solves the trust and traceability problem in aviation parts management. Aviation regulators require verifiable chain-of-custody records for every installed component. Blockchain creates an immutable, audit-ready ledger of part history — reducing fraud risk and accelerating regulatory approvals. For MRO providers operating across multiple jurisdictions, this auditability reduces compliance overhead materially.

Application Analysis

Performance Monitoring dominates with 26.9% due to continuous fleet-wide health visibility requirements.

In 2025, Performance Monitoring held a dominant market position in the By Application segment of the Digital MRO Market, with a 26.9% share. Airlines operate under strict airworthiness requirements that mandate continuous tracking of engine performance, fuel efficiency, and structural loads. Digital performance monitoring platforms replace manual log reviews with automated alert systems — allowing maintenance controllers to act on anomalies hours or days before they ground an aircraft.

Inspection and Damage Assessment applications use high-resolution imaging, AI-powered defect recognition, and AR overlays to conduct faster, more consistent aircraft inspections. Traditional visual inspections depend heavily on individual technician experience and are prone to variability. Digital inspection tools standardize the process across technician skill levels — reducing both missed defects and unnecessary maintenance actions triggered by false positives.

Predictive Analysis applications sit at the highest-value end of the digital MRO stack. By combining historical maintenance records with real-time sensor data, predictive platforms generate component-level remaining useful life estimates. Airlines using these tools can optimize maintenance intervals beyond the conservative fixed-interval schedules mandated by legacy programs — unlocking additional flight hours from assets already in service.

Inventory and Part Replacement platforms connect maintenance forecasts directly to parts ordering and logistics systems. When a predictive model flags a likely component failure within a defined window, the inventory system triggers replenishment automatically. This closed-loop approach eliminates the inventory bloat from over-ordering and the revenue loss from AOG events caused by part shortages.

Mobility and Functionality applications bring digital MRO workflows to the hangar floor through tablets and wearable devices. Technicians access job cards, schematics, and sign-off forms without returning to a workstation — compressing task completion time. For high-throughput line maintenance operations where turnaround time is measured in minutes, mobile MRO tools translate directly into aircraft utilization improvements.

Documentation and Compliance applications address the regulatory burden that consumes a disproportionate share of MRO labor hours. Aviation maintenance requires detailed, signed records for every task performed. Digital documentation platforms automate form generation, enforce completion checklists, and submit records directly to regulatory databases — eliminating transcription errors that can trigger costly re-inspection requirements.

End-User Analysis

Airlines dominate with 43.1% due to fleet scale creating the highest ROI from centralized digital platforms.

In 2025, Airlines held a dominant market position in the By End-User segment of the Digital MRO Market, with a 43.1% share. Airline operators manage maintenance across hundreds or thousands of aircraft — a scale at which manual systems become operationally unmanageable. Digital MRO platforms give airline maintenance control centers real-time visibility into fleet-wide health, enabling centralized decision-making that reduces both labor costs and unscheduled downtime simultaneously.

Independent MROs compete on turnaround speed and cost efficiency — two metrics that digital tools directly improve. As airlines raise performance expectations and put MRO contracts out to competitive tender more frequently, independent providers that cannot demonstrate digital capabilities face growing commercial pressure. Digital platform adoption is therefore a prerequisite for contract retention in this segment, not a differentiation strategy.

OEMs (Original Equipment Manufacturers) use digital MRO capabilities to extend their revenue relationship with customers beyond the initial sale. By offering connected maintenance services, OEMs convert one-time hardware revenue into long-term service contracts. This transition toward outcome-based service models — where the OEM guarantees availability rather than selling parts — fundamentally changes how maintenance economics are structured between manufacturer and operator.

Military and Defence Operators represent a distinct demand profile within the digital MRO market. Military fleets operate under classified data environments and require customized platform deployments that meet sovereign data requirements. However, the operational pressure to maximize aircraft availability in mission-critical scenarios makes these customers willing to invest heavily in digital maintenance capabilities — particularly predictive tools that reduce unplanned groundings.

Key Market Segments

By Technology

- Digital Twin

- Augmented Reality/Virtual Reality (AR/VR)

- 3D Printing

- Internet of Things (IoT)

- Artificial Intelligence (AI) and Big-Data Analytics

- Blockchain

By Application

- Performance Monitoring

- Inspection and Damage Assessment

- Predictive Analysis

- Inventory and Part Replacement

- Mobility and Functionality

- Documentation and Compliance

By End User

- Airlines

- Independent MROs

- OEMs

- Military and Defence Operators

Drivers

Predictive Maintenance and AI Integration Compress Maintenance Costs Across Commercial Fleets

Airlines face a clear commercial imperative: every unscheduled maintenance event costs more than a planned one — in parts, labor, and lost revenue from grounded aircraft. Predictive maintenance technologies address this directly by shifting repair timing from reactive to scheduled. The financial case is no longer theoretical, and aviation operators across all fleet sizes now treat digital maintenance adoption as a capital priority.

According to Panasonic, predictive maintenance programs deliver a 15% reduction in downtime, a 20% improvement in labor productivity, and an 18–25% reduction in maintenance costs. These are not marginal gains — they represent a structural repricing of MRO operations that makes digital platforms economically necessary for airlines competing on cost. Carriers without these tools face a widening cost disadvantage against digitally enabled competitors.

Real-time aircraft health monitoring extends this advantage further. AI systems continuously analyze engine sensor data, hydraulic readings, and structural loads to identify anomalies before they develop into failures. This capability directly reduces the fleet’s exposure to AOG incidents — the most expensive single event in commercial aviation. As fleet sizes expand globally, the ROI from AI-driven monitoring scales proportionally, reinforcing adoption across all operator segments.

Restraints

High Implementation Costs and Data Security Risks Slow Digital MRO Adoption Among Smaller Operators

Digital MRO platforms require substantial upfront investment — covering software licensing, hardware integration, sensor installation, and staff retraining. For smaller independent MRO providers and regional carriers, these capital requirements create a significant barrier. Vendors that fail to develop modular, pay-per-use pricing structures will find their addressable market constrained to large fleet operators who can absorb implementation costs more easily.

Data security concerns compound the financial barrier. Cloud-based aviation maintenance systems aggregate sensitive operational data — including fleet health metrics, component failure rates, and maintenance schedules. A breach does not just create regulatory exposure; it could expose competitive fleet data to rivals or compromise the airworthiness record integrity that regulators require. According to oxmaint.com, engine OEMs using digital twin monitoring report up to 48% more time on wing between major maintenance events — illustrating precisely what operators risk losing if security concerns prevent adoption.

The integration challenge with legacy systems adds a third layer of friction. Most airlines and MRO shops operate maintenance management systems built over decades, with heterogeneous data formats and proprietary architectures. Connecting new digital platforms to these environments requires expensive custom middleware and prolonged deployment timelines. Until vendors simplify integration pathways, adoption will remain slower than the market’s underlying economic logic would otherwise support.

Growth Factors

Digital Twin and Blockchain Expansion Opens Measurable New Revenue Streams for MRO Providers

Digital twin applications in aircraft maintenance have moved from pilot programs to fleet-wide deployment among leading carriers. The financial evidence now supports aggressive expansion: according to eajournals.org, aircraft digital twin deployments have reduced AOG incidents by 62.4% and decreased unscheduled component replacements by 35.8%. These outcomes create a clear commercial argument for MRO providers to position digital twin services as a premium, outcome-guaranteed offering rather than a software subscription.

Blockchain adoption for aviation parts traceability addresses a structural gap in the global MRO supply chain. Counterfeit and undocumented parts represent a compliance and safety risk that aviation authorities treat with zero tolerance. Blockchain platforms create verifiable, tamper-proof part histories — enabling faster regulatory approvals, reducing inspection duplication, and opening access to second-life component markets where traceability documentation determines residual value.

Augmented reality in technician training creates a third growth vector that directly expands the market’s serviceable base. AR platforms reduce new technician qualification time by allowing trainees to practice complex repair procedures in a virtual aircraft environment before working on live assets. For airlines and MRO providers facing a global technician shortage, faster qualification cycles translate directly into higher capacity — and create sustained licensing revenue for AR platform vendors.

Emerging Trends

IoT Sensor Networks and Paperless Documentation Redefine the Operating Model for Aircraft Maintenance

IoT sensor integration in aircraft maintenance systems has passed the deployment threshold where connectivity becomes a baseline expectation rather than a competitive differentiator. Airlines now install sensor packages during aircraft delivery — embedding IoT infrastructure into new fleet additions from day one. According to oxmaint.com, digital twin adoption driven by IoT data streams has produced downtime reductions of approximately 35%, equating to roughly 7.5 fewer hours of downtime per 1,000 flight hours — a figure that reframes sensor investment as a revenue protection mechanism.

Big data analytics for maintenance forecasting has shifted decision authority from individual technician judgment to algorithm-driven scheduling. Maintenance planners now work with probabilistic failure forecasts generated from fleet-wide historical data and live sensor feeds. Airlines using digital twin maintenance planning achieved an 18.7% reduction in total maintenance hours and extended component useful life by an average of 23.7%, according to eajournals.org. This compounds into significant asset value over a full aircraft service life.

The transition toward paperless maintenance documentation removes the last major analog bottleneck in the MRO workflow. Digital documentation platforms enforce task completion in sequence, auto-generate regulatory submissions, and create searchable maintenance histories accessible across global maintenance bases. For airlines operating mixed fleets across multiple regulatory jurisdictions, paperless systems reduce compliance overhead while simultaneously building the structured data sets that improve predictive model accuracy over time.

Regional Analysis

North America Dominates the Digital MRO Market with a Market Share of 34.80%, Valued at USD 0.4 Billion

North America holds 34.80% of the global Digital MRO Market, valued at USD 0.4 Billion in 2025. The region’s position reflects a combination of the world’s largest commercial aviation infrastructure, early FAA mandates for digital maintenance record-keeping, and a dense concentration of both major carriers and independent MRO providers. These structural advantages give North American operators both the scale and the regulatory incentive to lead digital platform deployment globally.

Europe Digital MRO Market Trends

Europe follows as the second most established market, supported by EASA’s rigorous airworthiness documentation standards and the presence of globally scaled MRO operations. European carriers and independent providers have embedded digital compliance tools into their maintenance workflows — driven less by choice and more by regulatory necessity. This compliance-first adoption pattern creates a mature, renewal-focused market where platform upgrades rather than new deployments drive revenue.

Asia Pacific Digital MRO Market Trends

Asia Pacific presents the market’s highest expansion potential. Fleet growth across China, India, and Southeast Asia is adding hundreds of new aircraft annually to a region that lacks the legacy maintenance infrastructure of Western markets. Airlines in this region build digital MRO capabilities into their operations from initial fleet deployment — creating high-volume, long-term platform adoption cycles that differ structurally from the replacement-driven markets in North America and Europe.

Middle East and Africa Digital MRO Market Trends

The Middle East concentrates digital MRO investment within a small number of state-backed carriers operating large, modern widebody fleets. These operators have both the capital and the fleet complexity to justify full-stack digital maintenance deployments. Africa remains at an earlier adoption stage, though investments in regional aviation infrastructure and growing low-cost carrier activity are beginning to create demand for scalable, cloud-based maintenance platforms suited to smaller fleet operators.

Latin America Digital MRO Market Trends

Latin America’s digital MRO adoption is constrained by fleet concentration among a small number of large carriers and a fragmented independent MRO sector operating on thin margins. However, post-pandemic fleet renewal across Brazil and Mexico has introduced newer aircraft types with native digital maintenance architectures — creating a natural entry point for digital platform vendors targeting OEM-linked service contracts on recently delivered aircraft.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

The Boeing Company leverages its dual position as an aircraft manufacturer and service provider to embed digital MRO capabilities directly into its fleet support contracts. Boeing’s access to aircraft design data gives its digital maintenance platforms a structural accuracy advantage — its predictive models operate from first-principles engineering knowledge rather than inferred sensor patterns alone. This positions Boeing’s service division to capture long-term maintenance contracts on its own installed base.

Lufthansa Technik AG has built one of the most commercially scaled digital MRO ecosystems in the industry, with its Digital Tech Ops platform — comprising AVIATAR, flydocs, and AMOS — now serving customers operating around 11,000 aircraft worldwide. In March 2026, Lufthansa Technik reported 2025 revenue of €8.049 billion, up 12% year-on-year, signaling that its integrated digital and physical MRO model is generating measurable commercial returns at fleet scale.

SITA N.V. approaches the digital MRO market from an aviation IT infrastructure position — providing connectivity, data exchange, and operational technology platforms across airports, airlines, and ground handlers. SITA’s network reach across global aviation stakeholders gives it a distribution advantage for MRO data integration products, particularly in markets where cross-operator data sharing creates value that single-vendor platforms cannot replicate.

Airbus SE pursues a strategy parallel to Boeing — using its engineering data access to build proprietary digital services that lock in Airbus fleet operators. Airbus’s Skywise platform aggregates operational and maintenance data across thousands of aircraft, enabling fleet-level benchmarking that individual airline analytics programs cannot match. This data network effect strengthens with every additional aircraft connected — creating a compounding competitive advantage against third-party MRO platform providers.

Key Players

- The Boeing Company

- Lufthansa Technik AG

- SITA N.V.

- Airbus SE

- GE Aerospace (General Electric Company)

- Honeywell International Inc.

- Rolls-Royce plc

- Collins Aerospace (RTX Corporation)

- Singapore Technologies Engineering Ltd.

- AAR CORP.

- Swiss AviationSoftware Ltd.

- Hexagon AB

Recent Developments

- March 2026 — Lufthansa Technik announced new infrastructure investments to expand its global MRO network, including a new engine repair facility with an integrated test stand in Calgary and expanded component repair capacity at its Tulsa site, reinforcing its position as a full-service physical and digital MRO provider.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.4 Billion |

| Forecast Revenue (2035) | USD 4.9 Billion |

| CAGR (2026-2035) | 13.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Digital Twin, Augmented Reality/Virtual Reality (AR/VR), 3D Printing, Internet of Things (IoT), Artificial Intelligence (AI) and Big-Data Analytics, Blockchain), By Application (Performance Monitoring, Inspection and Damage Assessment, Predictive Analysis, Inventory and Part Replacement, Mobility and Functionality, Documentation and Compliance), By End User (Airlines, Independent MROs, OEMs, Military and Defence Operators) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | The Boeing Company, Lufthansa Technik AG, SITA N.V., Airbus SE, GE Aerospace (General Electric Company), Honeywell International Inc., Rolls-Royce plc, Collins Aerospace (RTX Corporation), Singapore Technologies Engineering Ltd., AAR CORP., Swiss AviationSoftware Ltd., Hexagon AB |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |