Quick Navigation

- Report Overview

- Key Takeaways

- Component Analysis

- Type Analysis

- Maximum Take-off Weight Analysis

- Propulsion Analysis

- Operation Analysis

- Range Analysis

- Application Analysis

- Product Analysis

- End Use Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

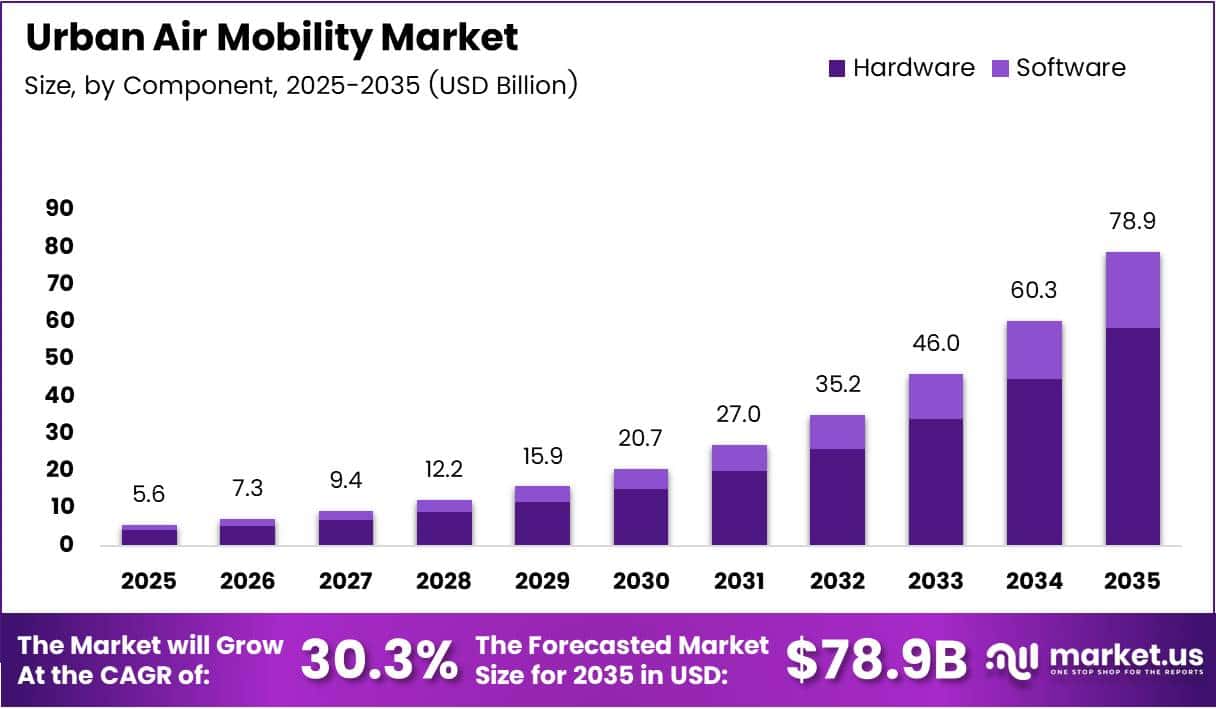

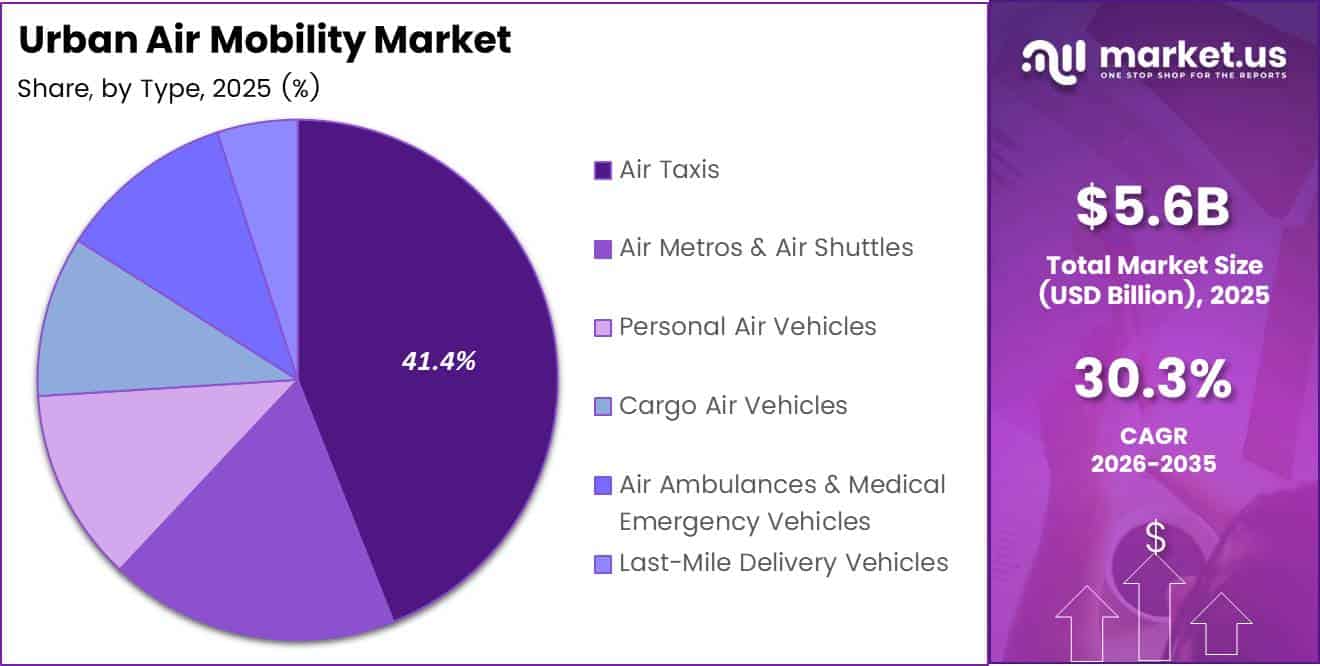

Global Urban Air Mobility Market size is expected to be worth around USD 78.9 Billion by 2035 from USD 5.6 Billion in 2025, growing at a CAGR of 30.3% during the forecast period 2026 to 2035.

Urban air mobility refers to a system of passenger and cargo transport using electric vertical takeoff and landing aircraft operating within and around cities. These vehicles use electric propulsion and advanced avionics to move people and goods through low-altitude urban airspace. The market covers air taxis, cargo drones, air ambulances, and last-mile delivery vehicles.

Severe road congestion in global cities creates measurable cost and time losses that ground transport cannot resolve. Aerial corridors above city rooftops bypass this infrastructure bottleneck entirely. This structural gap between urban mobility demand and existing road capacity forms the core commercial logic for eVTOL deployment at scale.

Governments across multiple regions now treat urban air mobility as part of their smart city infrastructure agenda, not just an aviation novelty. Public-private partnerships, airspace planning frameworks, and dedicated funding programs signal regulatory intent to enable commercial operations. This policy shift moves UAM from experimental to essential urban infrastructure.

Investment activity in this market reflects strong institutional conviction. In April 2025, Joby Aviation raised USD 500 million in a funding round, bringing total investment above USD 1.2 billion. This level of capital concentration in a single operator signals that institutional investors are placing high-conviction bets on near-term commercial viability, not long-term speculation.

According to Urban Air Mobility News, at least 40 U.S. cities or regions had active AAM/UAM initiatives as of early 2026, including pilots, planning programs, and public-private partnerships exploring eVTOL services and vertiport deployment. This breadth of municipal engagement shows that demand for urban aerial transport is not concentrated in one or two metros — it spans diverse geographies, urban sizes, and use cases.

According to BloombergNEF, a Manhattan-to-JFK eVTOL route would take approximately 7 minutes, compared to 50–75 minutes by car in typical traffic — implying up to a 90% reduction in travel time for that corridor. That time compression reframes eVTOL not as a premium novelty but as a structurally superior commute product, which is the condition needed to generate repeatable consumer demand at commercial scale.

The hardware segment, particularly propulsion and avionics, drives most development expenditure in this market. Electric propulsion dominates with a 72.2% share of the propulsion segment, reflecting widespread industry alignment on battery-electric architecture as the viable near-term technology path. As battery energy density improves, range and payload constraints will ease — directly expanding the commercial addressable market for each vehicle category.

Key Takeaways

- The Global Urban Air Mobility Market was valued at USD 5.6 Billion in 2025 and is forecast to reach USD 78.9 Billion by 2035.

- The market advances at a CAGR of 30.3% during the forecast period 2026 to 2035.

- By Component, Hardware leads with a 73.7% share in 2025.

- By Type, Air Taxis hold the dominant position with a 41.4% share.

- By Maximum Take-off Weight, the 100–300 Kg segment commands 45.9% share.

- By Propulsion, Electric accounts for 72.2% of the segment in 2025.

- By Operation, Remotely Piloted leads with a 51.6% share.

- By Range, Intracity (Below 100 km) dominates with 71.8% share.

- By Application, Passenger Transport leads with 66.3% share.

- By Product, Rotary Blade holds the top position with 55.5% share.

- By End Use, Commercial Ridesharing Operators lead with 44.8% share.

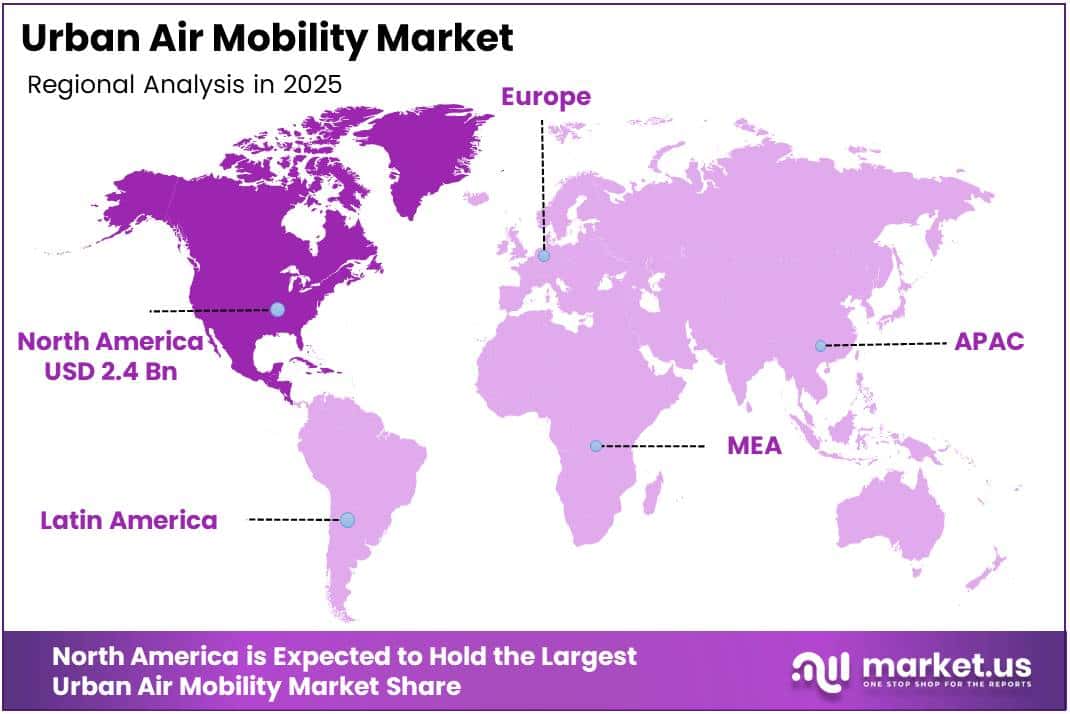

- North America dominates the global UAM market with a 43.80% share, valued at USD 2.4 Billion in 2025.

Component Analysis

Hardware dominates with 73.7% due to complex physical vehicle architecture requirements.

In 2025, Hardware held a dominant market position in the By Component segment of the Urban Air Mobility Market, with a 73.7% share. Physical vehicle systems — aerostructures, avionics, flight control, and propulsion — represent the majority of per-unit manufacturing cost and R&D expenditure. This concentration means that hardware suppliers sit at the highest-value node of the UAM supply chain.

Aerostructure forms the structural backbone of every eVTOL platform. Lightweight composite materials drive aerostructure design decisions, as every kilogram saved directly extends flight range and payload capacity. Suppliers with advanced composites capability hold a durable cost advantage over conventional airframe manufacturers attempting to enter this market.

Avionics determines the operational safety envelope of each aircraft. Certification requirements from the FAA and EASA demand redundant sensor architectures and fail-safe communication systems. Avionics complexity explains a significant portion of the time and capital required for type certification, making it a key bottleneck in fleet deployment timelines.

Flight Control System differentiates eVTOL platforms on handling quality and pilot workload. Advanced fly-by-wire control reduces pilot training burden and enables future autonomous operation modes. Operators that secure aircraft with proven, certified flight control systems gain a route-launching advantage over competitors still in test phases.

Propulsion System represents the core technology differentiator in current eVTOL competition. Electric motors, motor controllers, and thermal management systems define efficiency, noise output, and maintenance intervals. According to Engineering.com, Joby’s aircraft produces less than 65 dBA at 100 m during takeoff — roughly the level of normal conversation — demonstrating that advanced electric propulsion directly solves the urban noise acceptance barrier.

Software carries the highest margin within the UAM component ecosystem. Flight management software, digital twin platforms, and air traffic integration tools scale across fleets without proportional cost increases. As hardware becomes commoditized through manufacturing scale, software will capture a growing share of lifetime vehicle revenue.

Type Analysis

Air Taxis dominate with 41.4% due to high-value point-to-point urban commute demand.

In 2025, Air Taxis held a dominant market position in the By Type segment of the Urban Air Mobility Market, with a 41.4% share. The time-savings proposition of air taxi routes in congested cities creates a premium price point that justifies the vehicle and infrastructure investment. This commercial logic — premium fares on high-frequency urban corridors — makes air taxis the first UAM segment to attract operator capital at scale.

Air Metros and Air Shuttles serve as the scheduled, high-capacity complement to on-demand air taxis. Fixed-route operations between dense urban nodes reduce dispatch complexity and enable higher asset utilization. This segment suits operators seeking predictable load factors and infrastructure investment amortization over defined corridors.

Personal Air Vehicles represent the longest development horizon within the UAM type classification. Consumer ownership of aerial vehicles requires certification pathways, pilot licensing reform, and residential infrastructure that do not yet exist at scale. However, this segment carries outsized long-term market volume if regulatory barriers compress over the next decade.

Cargo Air Vehicles offer operators a regulatory-lighter entry path compared to passenger services, since removing human occupants simplifies safety certification requirements. E-commerce and express logistics companies face mounting last-mile cost pressure in dense urban zones, making aerial cargo a commercially motivated segment rather than a speculative one.

Air Ambulances and Medical Emergency Vehicles address a time-critical use case where aerial speed directly reduces mortality risk. Urban hospitals in traffic-locked cities increasingly face response-time failures with ground ambulances alone. This segment will likely see early regulatory approval given its clear public benefit profile.

Last-Mile Delivery Vehicles benefit directly from the same congestion economics driving passenger air mobility. Delivery density in urban cores makes aerial last-mile economically viable when ground-level parcel volumes exceed road network throughput. This segment connects the UAM investment thesis to the already-established e-commerce logistics market.

Maximum Take-off Weight Analysis

100–300 Kg segment dominates with 45.9% due to optimal balance of payload and regulatory manageability.

In 2025, the 100–300 Kg segment held a dominant market position in the By Maximum Take-off Weight segment of the Urban Air Mobility Market, with a 45.9% share. Vehicles in this weight class carry meaningful commercial payloads while remaining below thresholds that trigger the most complex airworthiness certification requirements. This regulatory positioning accelerates time-to-market relative to heavier aircraft categories.

The below 100 Kg weight class covers lightweight cargo drones and single-occupant experimental platforms. This class benefits from the most permissive regulatory frameworks globally, allowing faster testing cycles. However, limited payload capacity constrains its commercial application to small parcel delivery and infrastructure inspection rather than passenger transport.

The above 300 Kg weight class captures multi-passenger air taxis and heavy cargo aircraft requiring full transport-category certification. These vehicles offer the highest revenue-per-flight potential but face the longest certification timelines. Operators targeting this class must plan for extended pre-revenue development periods before achieving commercial service authorization.

Propulsion Analysis

Electric dominates with 72.2% due to zero-emission urban operation and lower noise output.

In 2025, Electric propulsion held a dominant market position in the By Propulsion segment of the Urban Air Mobility Market, with a 72.2% share. Battery-electric architecture eliminates combustion emissions in city airspace and produces significantly lower acoustic signatures than conventional rotorcraft. These two characteristics — clean operation and noise compatibility — are prerequisites for urban regulatory approval, making electric the de facto standard for near-term commercial UAM.

Gasoline propulsion retains relevance in legacy cargo drone applications and transitional UAM platforms where battery energy density still limits range. However, combustion-based vehicles face compounding headwinds from urban emission restrictions and community noise ordinances. This segment will shrink as battery technology advances and regulatory frameworks tighten around urban airspace emissions.

Hybrid propulsion bridges the range limitation of pure-electric systems with reduced emissions compared to gasoline-only aircraft. Hybrid systems appeal to intercity routes exceeding current battery range thresholds. As battery energy density improves, the commercial rationale for hybrid propulsion narrows — but it provides a viable medium-term solution for operators requiring range beyond 150 miles per charge.

Operation Analysis

Remotely Piloted dominates with 51.6% due to near-term certification readiness over full autonomy.

In 2025, Remotely Piloted operation held a dominant market position in the By Operation segment of the Urban Air Mobility Market, with a 51.6% share. Regulatory frameworks across the FAA, EASA, and CAAC require human-in-the-loop oversight for initial commercial UAM operations. Remote piloting satisfies this requirement while reducing onboard weight and enabling vehicle miniaturization — a commercially and regulatorily pragmatic position for early operators.

Fully Autonomous operation represents the long-term operating model that will determine UAM unit economics at scale. Removing pilots eliminates a significant per-flight labor cost and enables 24/7 operations without crew rest limitations. However, autonomous certification requires demonstration of fail-safe decision-making across thousands of edge cases, placing this segment on a longer regulatory timeline than remotely piloted systems.

Hybrid operation combines automated flight phases with remote pilot oversight at critical moments such as takeoff, landing, and emergency response. This approach lets operators capture partial automation cost savings without requiring full autonomous certification. Hybrid operation is emerging as the practical transitional standard as the industry moves from remote piloting toward full autonomy.

Range Analysis

Intracity (Below 100 km) dominates with 71.8% due to dense urban route economics and short-haul demand.

In 2025, Intracity (Below 100 km) held a dominant market position in the By Range segment of the Urban Air Mobility Market, with a 71.8% share. Urban congestion problems are concentrated within city boundaries, making sub-100 km routes the highest-value commercial opportunity for early UAM operators. Battery range constraints of current eVTOL platforms align naturally with intracity distances, removing the need for interim charging stops on core commercial routes.

Intercity (Above 100 km) operations require vehicle range capabilities that current battery technology only partially supports. Advanced battery integration and hybrid propulsion systems are extending the addressable intercity corridor map. As energy density improves, intercity routes between adjacent urban centers will become commercially viable — representing the next expansion wave for UAM operators after intracity markets mature.

Application Analysis

Passenger Transport dominates with 66.3% due to premium fare potential on congested urban corridors.

In 2025, Passenger Transport held a dominant market position in the By Application segment of the Urban Air Mobility Market, with a 66.3% share. Human mobility commands higher per-trip revenue than cargo in urban markets, justifying the higher vehicle certification cost and operational complexity. Operators focusing on passenger routes capture the most capital-efficient revenue model given current vehicle economics and infrastructure investment.

Freighter applications serve urban and peri-urban cargo networks where road congestion inflates last-mile delivery costs. E-commerce volume growth in dense cities creates structural demand for aerial freight alternatives. Freighter UAM benefits from a more permissive regulatory entry path than passenger services, allowing operators to generate early commercial revenue while passenger certification processes continue.

Product Analysis

Rotary Blade dominates with 55.5% due to vertical lift capability and urban operational flexibility.

In 2025, Rotary Blade held a dominant market position in the By Product segment of the Urban Air Mobility Market, with a 55.5% share. Multirotor and tiltrotor architectures provide true vertical takeoff and landing capability, eliminating the need for runways and enabling rooftop or compact vertiport operations within dense urban environments. This infrastructure flexibility makes rotary blade designs the most deployable product format for early-stage urban networks.

Fixed Wing eVTOL designs carry the highest aerodynamic efficiency in forward flight, enabling longer ranges and lower energy consumption per passenger-mile on intercity corridors. However, fixed-wing platforms require longer takeoff and landing footprints that conflict with dense urban infrastructure constraints. Their commercial advantage will emerge more fully on suburban and intercity routes rather than city-center operations.

Hybrid product designs combine vertical lift rotors with fixed-wing surfaces to optimize both urban operability and forward-flight efficiency. This configuration targets operators requiring flexible deployment across both intracity and intercity routes. Hybrid airframes carry higher design complexity and manufacturing cost, but their route versatility positions them as the preferred platform for network-scale UAM operators.

End Use Analysis

Commercial Ridesharing Operators dominate with 44.8% due to established urban mobility demand aggregation.

In 2025, Commercial Ridesharing Operators held a dominant market position in the By End Use segment of the Urban Air Mobility Market, with a 44.8% share. Existing ridesharing platforms bring proven demand aggregation infrastructure, customer bases, and dynamic pricing models directly applicable to air taxi operations. In March 2024, Volocopter and Stellantis announced a strategic partnership to co-develop urban air-mobility solutions — a clear signal that automotive and mobility operators view UAM as an extension of existing urban transport networks.

E-Commerce operators represent the fastest-growing end-use category by volume potential, driven by last-mile delivery cost pressure in congested urban cores. Aerial cargo delivery bypasses road-level congestion entirely, reducing delivery times and enabling service-level guarantees that ground transport cannot match in peak hours. This use case connects UAM investment directly to measurable logistics cost reduction.

Private Operators serve high-net-worth individuals and corporate clients requiring point-to-point aerial transport on flexible schedules. This segment commands premium pricing and tolerates higher per-trip costs, making it an early revenue-generating category before mass-market air taxi pricing becomes feasible. Private operations also provide operators with early real-world flight data to support broader certification programs.

Medical Emergency Organizations represent a high-impact, mission-critical end-use case where aerial response speed directly affects patient outcomes. Urban hospitals and emergency services in traffic-congested cities face consistent ground ambulance delays that aerial vehicles can structurally resolve. This segment is likely to receive preferential regulatory treatment given its public health mandate.

Others includes government agencies, defense contractors, and infrastructure inspection operators adopting UAM platforms for surveillance, border monitoring, and utility inspection. These applications diversify UAM revenue streams beyond commercial mobility and create public-sector procurement channels that reduce dependence on consumer market timing.

Key Market Segments

By Component

- Hardware

- Aerostructure

- Avionics

- Flight Control System

- Propulsion System

- Others

- Software

By Type

- Air Taxis

- Air Metros & Air Shuttles

- Personal Air Vehicles

- Cargo Air Vehicles

- Air Ambulances & Medical Emergency Vehicles

- Last-Mile Delivery Vehicles

By Maximum Take-off Weight

- <100 Kg

- 100 – 300 Kg

- >300 Kg

By Propulsion

- Gasoline

- Electric

- Hybrid

By Operation

- Remotely Piloted

- Fully Autonomous

- Hybrid

By Range

- Intracity (Below 100 km)

- Intercity (Above 100 km)

By Application

- Passenger Transport

- Freighter

By Product

- Rotary Blade

- Fixed Wing

- Hybrid

By End Use

- Commercial Ridesharing Operators

- E-Commerce

- Private Operators

- Medical Emergency Organizations

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Drivers

Urban Traffic Gridlock and Aerospace Investment Create Dual-Engine Demand for eVTOL Platforms

Road congestion in major cities costs economies billions annually in lost productivity and fuel waste. Ground transport networks in megacities cannot be expanded fast enough to absorb population growth. This structural deficit creates a concrete commercial case for aerial urban transport that bypasses surface infrastructure entirely — not as a premium product, but as a functional necessity.

Private investment in eVTOL development accelerated sharply through 2024 and 2025, with aerospace companies and ride-sharing platforms forming operational partnerships to develop commercial UAM services. In March 2024, Volocopter and Stellantis announced a co-development partnership combining eVTOL aircraft expertise with automotive urban mobility infrastructure. This partnership model compresses the time from prototype to commercial service by pooling regulatory experience, manufacturing scale, and distribution networks.

According to Joby Aviation, the company completed more than 850 eVTOL test flights in 2025 — approximately 2.6 times its 2024 rate — flying over 9,000 miles in that year alone. This acceleration in testing pace signals that leading operators are transitioning from proof-of-concept to certification-track development, which compresses the timeline to commercial deployment and forces competitor programs to match pace or fall behind on regulatory milestones.

Restraints

Certification Complexity and Vertiport Infrastructure Costs Create Compounding Barriers to Commercial Launch

FAA and EASA type certification for eVTOL aircraft requires demonstration of safety across thousands of flight conditions, system failure modes, and emergency scenarios. This process typically requires years of structured test flight programs before commercial authorization. For most operators, certification cost and timeline represent the single largest barrier between prototype capability and revenue-generating operations.

Urban vertiport construction requires securing real estate, obtaining aviation-specific building permits, and integrating with existing urban traffic management systems. According to Secure Energy, analysis of emerging UAM networks projects hundreds of vertiports needed globally by the late 2020s, with early operations relying heavily on modified airports and heliports rather than new builds. The capital intensity of greenfield vertiport development means that infrastructure deployment will lag vehicle certification — creating an operational bottleneck even after aircraft receive regulatory approval.

Urban air traffic management systems capable of coordinating dozens of low-altitude eVTOL flights simultaneously do not yet exist at commercial scale. Aviation authorities must develop new airspace frameworks, communication protocols, and conflict-resolution systems before dense urban UAM networks can operate safely. These regulatory and infrastructure gaps mean that even fully certified aircraft may face constrained initial route availability, limiting early operator revenue potential.

Growth Factors

Autonomous Air Taxi Development, Emergency Medical Use, and Advanced Battery Integration Define the Next Revenue Expansion Phase

On-demand autonomous passenger air taxis represent the highest-volume commercial opportunity in UAM once certification frameworks mature. Removing onboard pilots eliminates the largest recurring labor cost in air taxi operations, enabling fare structures competitive with premium ground transport. Operators that achieve autonomous certification ahead of competitors will capture network effects that make displacement increasingly difficult once route density builds.

Emergency medical services represent a high-certainty growth pathway because the value proposition is non-discretionary — faster aerial response times directly reduce mortality in cardiac, stroke, and trauma cases. UAM vehicles deployed for air ambulance operations generate utilization data, operational protocols, and public trust that directly accelerate certification timelines for broader commercial passenger services. According to AAM International, Eve Air Mobility’s full-scale prototype reached 50 successful test flights by April 2026, providing critical data to support its ANAC certification campaign and validating multi-application vehicle designs including ambulance configurations.

Advanced battery technology is expanding the commercially viable flight envelope for eVTOL platforms. Higher energy density reduces charging intervals, extends range beyond current 150-mile limits, and improves payload-to-weight ratios. Each incremental battery improvement unlocks new route categories — particularly intercity corridors — that were previously outside the economic range of electric propulsion, directly expanding the total addressable market for UAM operators.

Emerging Trends

Digital Air Traffic Management and eVTOL Prototyping Acceleration Define the Near-Term Competitive Frontier

Aviation authorities and technology companies are jointly developing digital air traffic management systems specifically designed for low-altitude urban airspace. These platforms use real-time data exchange between vehicles, ground infrastructure, and control centers to coordinate multiple simultaneous eVTOL flights safely. Early movers that integrate with these digital frameworks gain a structural advantage in route expansion speed once commercial authorization begins.

Aerospace startups are compressing prototype-to-certification timelines through rapid testing iteration cycles, enabled by digital twin simulation and modular vehicle architectures. According to Joby Aviation, the S4 eVTOL achieves a top speed of approximately 200 mph with a range up to 150 miles per charge and approach noise of approximately 45 dB at 500 m altitude. These performance specifications demonstrate that eVTOL platforms have crossed the threshold from experimental to commercially deployable — the metric that moves investors from pilot funding to fleet-scale commitment.

Public air taxi demonstrations in major cities are shifting consumer perception from novelty to expectation. Pilot programs in urban centers generate media coverage, regulatory familiarity, and early adopter feedback that directly inform vehicle and service design. Operators investing in visible public demonstrations now are building brand recognition and route acceptance ahead of commercial launch — an asymmetric advantage that cannot be replicated through private testing programs alone.

Regional Analysis

North America Dominates the Urban Air Mobility Market with a Market Share of 43.80%, Valued at USD 2.4 Billion

North America commands 43.80% of the global UAM market, valued at USD 2.4 Billion in 2025. The FAA’s structured type certification pathway, combined with the concentration of leading eVTOL developers and institutional investors in the United States, creates an ecosystem that accelerates development timelines. Additionally, at least 40 U.S. cities have active UAM planning programs, confirming broad geographic demand across the continent rather than concentration in a single metro market.

Europe Urban Air Mobility Market Trends

Europe builds its UAM competitive position on EASA’s progressive regulatory framework and the continent’s dense intercity corridor network, which suits both intracity and short-range intercity eVTOL deployment. Germany, France, and the UK anchor aviation manufacturing and investment activity. European aerospace incumbents and well-funded startups are advancing commercial certification programs that position the region as the second-largest UAM market globally.

Asia Pacific Urban Air Mobility Market Trends

Asia Pacific combines the world’s most congested megacities with aggressive government-backed smart city investment programs — a combination that creates strong structural demand for aerial mobility solutions. China, Japan, and South Korea lead regional eVTOL development activity, with China’s domestic manufacturers targeting both passenger and cargo applications. The region’s urban density makes the time-saving value of air mobility more pronounced than in lower-density Western markets.

Middle East and Africa Urban Air Mobility Market Trends

The Middle East leads UAM ambitions in this region through sovereign wealth fund investment and smart city megaprojects, particularly in the UAE and Saudi Arabia. Dubai’s aviation authority has conducted public eVTOL demonstrations and integrated UAM into its long-term transport planning. These government-directed initiatives remove demand uncertainty and create funded procurement pipelines that commercial operators can target with confidence.

Latin America Urban Air Mobility Market Trends

Latin America’s UAM development concentrates in São Paulo and Mexico City, where traffic congestion severity creates an acute commercial rationale for aerial transport. Brazil’s ANAC has engaged with eVTOL manufacturers on certification frameworks, reflecting regulatory intent to support commercial operations. Infrastructure investment constraints slow near-term deployment, but the severity of urban congestion in the region’s primary cities maintains long-term market relevance.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Airbus enters the UAM market from a position of unmatched aerospace manufacturing scale and established regulatory relationships with EASA and global aviation authorities. Its CityAirbus NextGen program leverages existing supply chain infrastructure and type certification expertise developed across decades of commercial aircraft programs. This institutional depth compresses development risk in ways that pure-play eVTOL startups cannot replicate, positioning Airbus as the most credible incumbent threat to startup-led market share.

Lilium GmbH differentiates through its jet-powered eVTOL architecture, which uses electric ducted fans instead of open rotors to achieve quieter, higher-speed forward flight. This design targets intercity corridor operations where speed and noise compatibility matter more than hover efficiency — a market segment that most tiltrotor competitors are less optimized for. However, the complexity of its proprietary propulsion system creates higher certification and manufacturing cost than multirotor alternatives.

Guangzhou EHang Intelligent Technology Co. Ltd holds a strategic first-mover advantage as the operator of the world’s first commercially certified autonomous aerial vehicle — the EH216-S — approved by China’s CAAC. This certification milestone allows EHang to generate commercial revenue while Western competitors remain in pre-certification development phases. Its domestic market access in China, combined with export partnerships across Asia and the Middle East, provides geographic diversification unavailable to U.S.-focused competitors.

Eve Holding, Inc. benefits from its origin as an Embraer spin-off, inheriting manufacturing relationships, FAA/ANAC regulatory familiarity, and a global MRO network that reduces post-certification operational risk. By April 2026, Eve’s full-scale prototype had reached 50 successful test flights, providing certification-relevant data to ANAC. This Embraer lineage gives Eve a structural advantage in commercialization speed that pure startups without aerospace heritage cannot match.

Key Players

- Airbus

- Lilium GmbH

- Guangzhou EHang Intelligent Technology Co. Ltd

- Eve Holding, Inc.

- Vertical Aerospace

- Textron Inc.

- Joby Aero, Inc.

- Embraer Group

- Hyundai Motor Company

- Archer Aviation Inc.

- The AIRO Group, Inc.

- Wingcopter GmbH

- BETA Technologies, Inc.

- Volocopter GmbH

- Uber Technologies, Inc.

- Safran Group

Recent Developments

- 2025 (Year-End) — Joby Aviation’s year-end update confirmed more than 850 test flights and over 9,000 miles flown in 2025 alone, surpassing 50,000 cumulative fleet miles and underscoring continued momentum toward commercial UAM certification and service deployment.

- April 2026 — Eve Air Mobility’s full-scale prototype reached 50 successful test flights, accumulating over 2 hours of total flight time since its first flight on 19 December 2025, providing key data to support its ANAC certification campaign.

- December 2024 — Chinese startup Huayu Xianxiang Aviation conducted the first flight of its Honghu Mark 1 eVTOL, a five-seat aircraft with 2,500 kg MTOW, 280 km/h cruise speed, 450 kg payload, and 60-minute endurance, targeting passenger, cargo, and air-ambulance applications.

- January 2024 — Bell Textron announced the successful first flight of its Nexus air-taxi eVTOL, marking a significant 2024 milestone in demonstrating a functional air-taxi platform and advancing Bell’s position in the commercial urban air mobility market.

- End of 2025 — Joby Aviation completed over 4,900 flight test points toward FAA type certification, covering performance verification, flight envelope expansion, and system safety objectives — one of the most advanced certification portfolios in the global eVTOL industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.6 Billion |

| Forecast Revenue (2035) | USD 78.9 Billion |

| CAGR (2026-2035) | 30.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware: Aerostructure, Avionics, Flight Control System, Propulsion System, Others; Software), By Type (Air Taxis, Air Metros & Air Shuttles, Personal Air Vehicles, Cargo Air Vehicles, Air Ambulances & Medical Emergency Vehicles, Last-Mile Delivery Vehicles), By Maximum Take-off Weight (<100 Kg, 100–300 Kg, >300 Kg), By Propulsion (Gasoline, Electric, Hybrid), By Operation (Remotely Piloted, Fully Autonomous, Hybrid), By Range (Intracity Below 100 km, Intercity Above 100 km), By Application (Passenger Transport, Freighter), By Product (Rotary Blade, Fixed Wing, Hybrid), By End Use (Commercial Ridesharing Operators, E-Commerce, Private Operators, Medical Emergency Organizations, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Airbus, Lilium GmbH, Guangzhou EHang Intelligent Technology Co. Ltd, Eve Holding Inc., Vertical Aerospace, Textron Inc., Joby Aero Inc., Embraer Group, Hyundai Motor Company, Archer Aviation Inc., The AIRO Group Inc., Wingcopter GmbH, BETA Technologies Inc., Volocopter GmbH, Uber Technologies Inc., Safran Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |