Quick Navigation

Report Overview

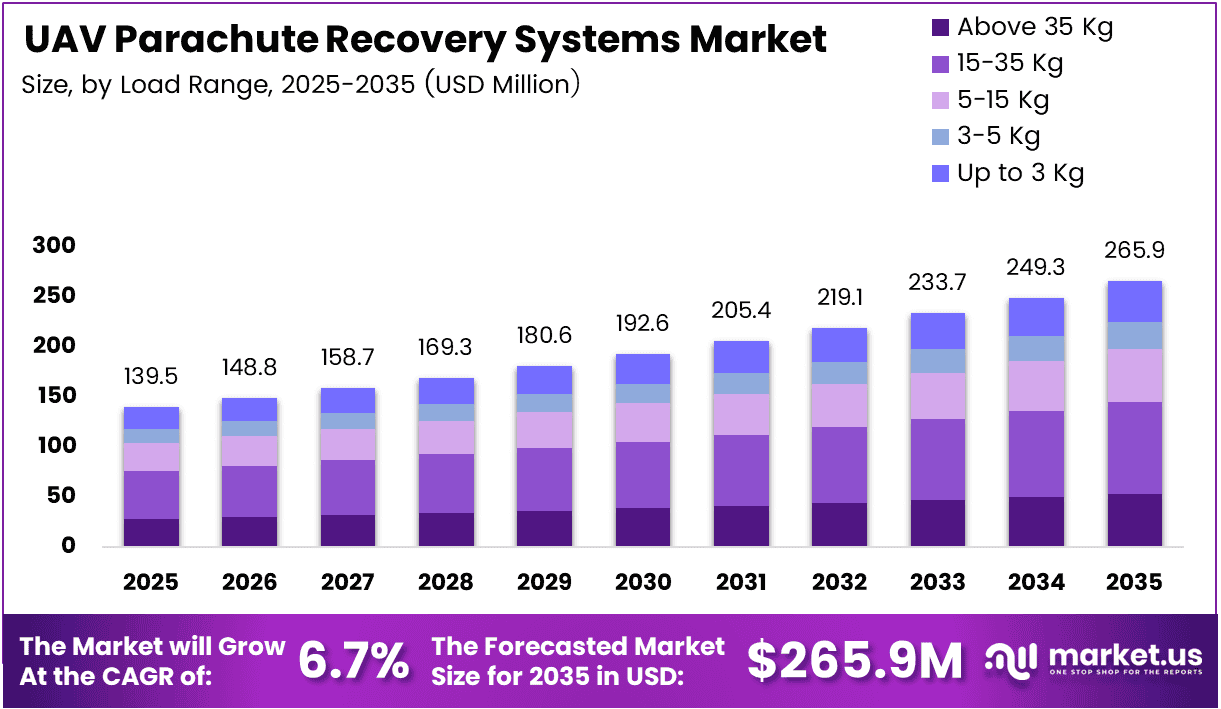

Global UAV Parachute Recovery Systems Market size is expected to be worth around USD 139.5 Million by 2035 from USD 65.9 Million in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

UAV parachute recovery systems are emergency safety mechanisms designed to slow or arrest the descent of an unmanned aerial vehicle during a malfunction or controlled termination event. These systems deploy autonomously or via command, preventing uncontrolled crashes that risk ground personnel, property, and regulatory compliance. Their relevance scales directly with drone adoption across civil and defense sectors.

The core value proposition of these recovery systems extends beyond crash prevention. Regulators in the US, EU, and Asia are tightening over-populated-area flight approvals for commercial drones, and parachute certification has become a gatekeeping requirement. Operators who integrate certified recovery systems gain access to higher-value urban delivery and inspection corridors unavailable to unequipped fleets.

Military operators drive a disproportionate share of system demand because drone loss in contested environments carries mission-critical consequences beyond hardware cost. Border surveillance, ISR, and logistical drone programs require recovery mechanisms that meet both operational reliability standards and weight constraints. This dual-use pressure shapes product design across the market’s leading providers.

Commercial drone logistics operators face a parallel compliance imperative. Delivery networks operating over populated areas in Europe and North America cannot obtain regulatory approvals without certified parachute recovery systems. This creates a structural demand floor that grows in direct proportion to drone delivery network expansion, rather than depending on discretionary technology adoption.

In April 2025, Butler Parachute Systems introduced the AeroSafe Tactical, a ruggedized recovery system targeting Group 3 unmanned aircraft — a segment with limited specialized options. This product launch signals that providers are moving upstream toward heavier, mission-critical platforms where pricing power and switching costs are substantially higher than in the consumer drone tier.

According to Unmanned Systems Technology, ParaZero’s DropAir system completed 50 consecutive successful deliveries in its July 2025 trials. This milestone matters because delivery drone operators require demonstrated reliability thresholds before regulatory bodies approve commercial route authorizations — making consistent field performance data a commercial differentiator, not just a technical benchmark.

According to AVSS, the parachute recovery system for the DJI Matrice 4 Series delivers an average descent rate of 3.82 mps and an impact energy of 10.1 J. These figures indicate the system keeps ground impact forces well within safe thresholds, which directly supports operator compliance with EASA and FAA regulations governing flights over people — a prerequisite for commercial urban operations.

Key Takeaways

- The UAV Parachute Recovery Systems Market was valued at USD 65.9 Million in 2025 and is forecast to reach USD 139.5 Million by 2035.

- The market advances at a CAGR of 6.7% between 2026 and 2035.

- By Load Range, the 15–35 Kg segment holds a 32.7% share, representing the dominant weight class.

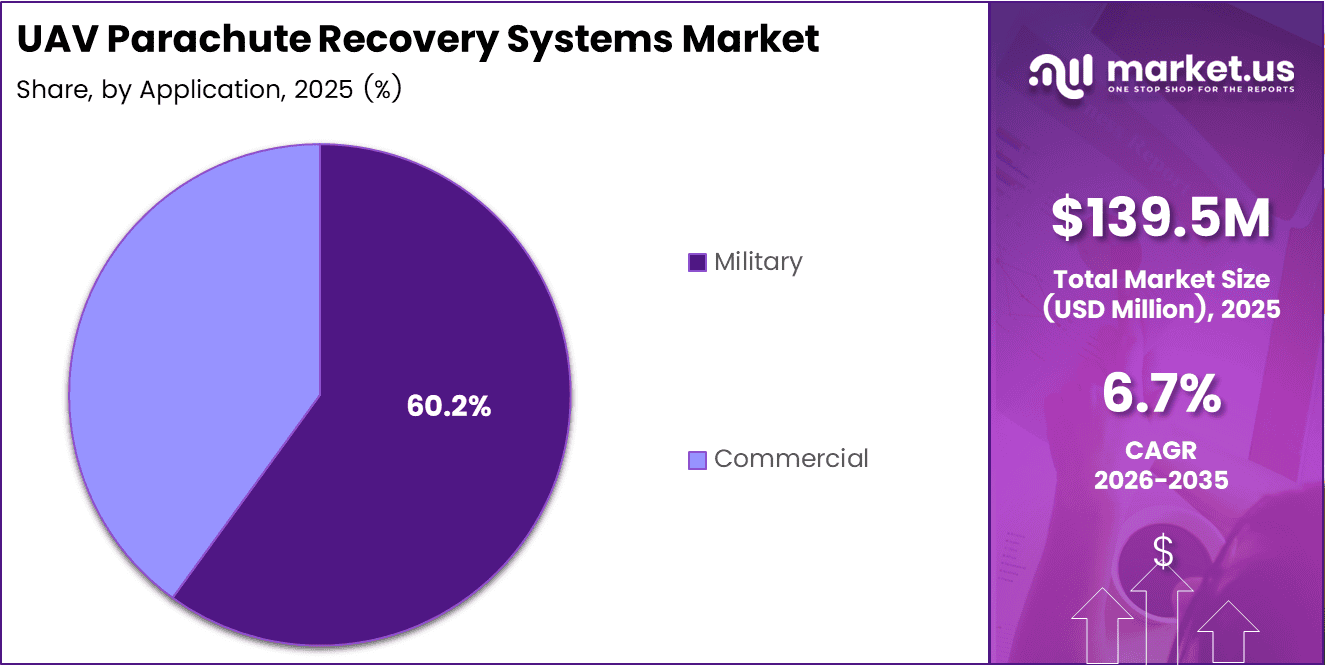

- By Application, Military accounts for 60.2% of market share, making it the leading end-use segment.

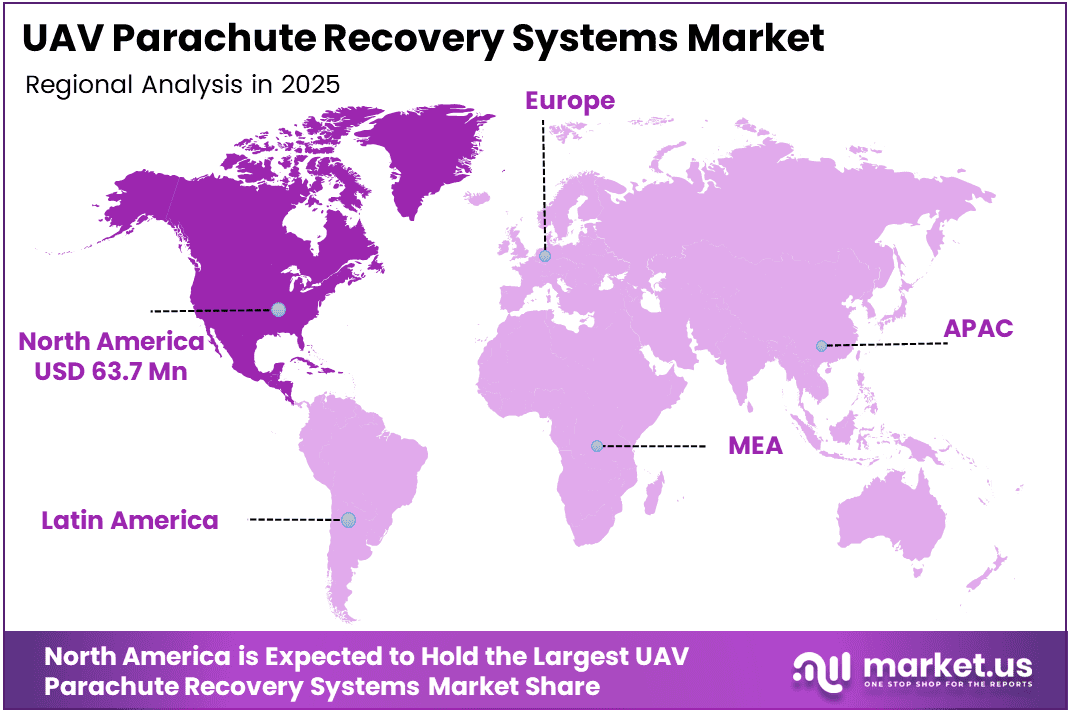

- North America dominates the regional landscape with 45.7% share, valued at USD 63.7 Million.

Load Range Analysis

15–35 Kg dominates with 32.7% due to defense and commercial mid-weight drone prevalence.

In 2025, the 15–35 Kg load range held a dominant market position in the By Load Range segment of the UAV Parachute Recovery Systems Market, with a 32.7% share. This weight class covers the majority of tactical military UAVs and commercial delivery platforms currently deployed at scale. Vendors targeting this tier face the most competitive pressure, but also benefit from the largest addressable base of active operators seeking certified recovery solutions.

Above 35 Kg platforms represent the high-value end of the recovery systems market. These heavy UAVs — including Group 3 and Group 4 military systems and large cargo drones — carry payloads where loss costs extend well beyond hardware replacement. Consequently, buyers in this tier prioritize reliability and certification credentials over unit price, creating stronger margin profiles for specialized system providers. In April 2025, Butler Parachute Systems targeted this segment directly with the AeroSafe Tactical launch for Group 3 UAS.

5–15 Kg drones occupy the intersection of commercial inspection, agricultural monitoring, and light logistics applications. Recovery system adoption in this range accelerates as operators seek regulatory compliance for over-populated-area flights. Vendors offering plug-and-play, model-specific solutions gain faster channel adoption in this tier because installation simplicity directly reduces operator downtime and certification lead times.

3–5 Kg drones sit at the cost-sensitivity threshold where operators weigh recovery system pricing against the replacement cost of the drone itself. Recovery system adoption here is largely compliance-driven rather than risk-preference-driven. Providers that engineer cost-efficient, lightweight systems for this class can capture volume that heavier-platform specialists overlook, particularly in the European regulatory market where over-populated-area rules apply regardless of drone size.

Up to 3 Kg drones represent the consumer and prosumer segment, where recovery systems remain largely optional outside specific regulatory zones. However, as urban air mobility rules tighten globally, even sub-3 kg platforms operated commercially face growing certification requirements. This creates a latent demand layer that has not yet converted to recurring revenue but will reshape the small-drone recovery segment within the forecast period.

Application Analysis

Military dominates with 60.2% due to mission-critical drone loss consequences in defense operations.

In 2025, Military held a dominant market position in the By Application segment of the UAV Parachute Recovery Systems Market, with a 60.2% share. Defense operators prioritize recovery systems because drone loss in active deployments carries intelligence exposure risk beyond hardware cost — a dynamic that civilian operators do not face. This asymmetry in loss consequences sustains higher per-unit spending and longer procurement cycles in military procurement channels. In October 2025, ParaZero received a purchase order from Airobotics specifically to support defense drone operations, reinforcing military sector demand. In May 2025, ParaZero secured a significant European order for its SafeAir M4 system, signaling cross-sector momentum building in tandem.

Commercial applications form the growth frontier of the recovery systems market as delivery, inspection, and logistics drone networks scale under tightening regulatory frameworks. Unlike military buyers who procure based on mission requirements, commercial operators adopt recovery systems primarily to satisfy aviation authority mandates for over-populated-area operations. This compliance-driven adoption model creates a direct link between regulatory stringency and commercial segment revenue growth — meaning stricter rules accelerate sales cycles rather than slowing them.

Key Market Segments

By Load Range

- Above 35 Kg

- 15–35 Kg

- 5–15 Kg

- 3–5 Kg

- Up to 3 Kg

By Application

- Military

- Commercial

Drivers

Safety Regulations and Defense Deployment Mandates Create Structural Demand for UAV Recovery Systems

Aviation authorities in the US and EU now require certified parachute recovery systems for drone operations over populated areas. This mandate transforms recovery systems from optional add-ons into non-negotiable procurement line items. Operators without certified systems face route restrictions that make commercial delivery and inspection businesses economically unviable — effectively linking revenue generation to recovery system adoption.

Defense and border surveillance programs have embedded UAV parachute recovery requirements directly into procurement specifications. Military operators conducting ISR, logistics, and border monitoring missions treat drone loss as a security risk, not just an asset replacement cost. According to AVSS, the DJI Matrice 4 Series recovery system deploys in under 0.5 seconds, meeting the response-time threshold that defense-grade applications require. This performance benchmark shapes buyer expectations across both military and civilian procurement.

The expansion of drone logistics and urban air mobility ecosystems adds a third demand layer. Delivery network operators scaling across European and North American cities require parachute certification as a precondition for regulatory approval on every new route. In March 2025, Fruity Chutes partnered with High Energy Sports to deliver scalable recovery solutions for UAV manufacturers — a signal that supply chains are organizing to meet multi-platform demand at volume.

Restraints

Payload and Cost Constraints Limit Recovery System Adoption Across Small UAV Platforms

Parachute recovery systems add weight to the host drone, directly reducing available payload capacity. For small commercial UAVs in the sub-5 kg class, this trade-off can render the platform operationally ineffective for its primary task — particularly in precision delivery and agricultural spraying applications where every gram of payload determines mission feasibility. Manufacturers face a physics constraint that engineering refinements only partially resolve.

Cost pressure compounds the payload problem for small UAV operators. In the 3–5 kg and sub-3 kg segments, recovery system pricing can represent a significant fraction of the drone’s purchase value. Operators in price-sensitive commercial markets — particularly in developing economies — delay adoption until regulatory enforcement tightens, creating a persistent gap between compliance requirements and actual deployment rates that slows overall market conversion.

The combined weight and cost barrier creates a two-speed market: heavy-platform military and enterprise operators adopt recovery systems willingly, while small-platform commercial operators resist until forced by enforcement. This structural divide limits the addressable market for standard recovery solutions and pushes vendors to invest in lightweight engineering — an R&D overhead that compresses margins for providers serving the high-volume small-drone segment.

Growth Factors

E-Commerce Drone Logistics and Government Safety Mandates Unlock New Recovery System Revenue Streams

E-commerce operators are scaling autonomous delivery drone programs that require certified parachute recovery systems to fly over residential and urban zones. Each new delivery corridor approval generates a direct hardware procurement requirement — creating a durable revenue stream for recovery system vendors that scales with logistics network expansion. This dependency makes recovery systems a recurring infrastructure cost rather than a one-time equipment purchase.

Governments in the US, EU, and Asia are codifying drone safety regulations that explicitly reference emergency recovery requirements for certain airspace categories. According to AVSS, the DJI Mavic 3 Enterprise recovery system achieves a minimum deployment altitude of 33.9 m, confirming that low-altitude urban operations — precisely where regulatory requirements concentrate — are technically viable. This performance data accelerates regulatory approval timelines for operators, translating directly into faster revenue generation for recovery system providers.

Infrastructure inspection and industrial monitoring represent an underserved growth channel. Utilities, oil and gas operators, and construction firms deploy UAVs over high-consequence environments — pipelines, power lines, and industrial facilities — where uncontrolled drone descent poses serious safety and liability risks. In January 2025, ParaZero launched its SafeAir Enterprise API, enabling real-time fleet-level monitoring of parachute events. This capability addresses a critical gap for multi-drone enterprise operators managing compliance across large asset portfolios.

Emerging Trends

Smart Autonomous Deployment and GPS-Integrated Recovery Systems Redefine Safety Benchmarks for Commercial and Defense Drones

Recovery system developers are embedding automatic deployment sensors that trigger without pilot input during a detected malfunction. This autonomy removes human reaction time from the safety equation — a critical improvement in beyond-visual-line-of-sight operations where the pilot cannot visually confirm a failure. Autonomous deployment capability is becoming a baseline expectation in advanced regulatory frameworks rather than a premium feature.

GPS and flight control integration enables recovery systems to log deployment location, altitude, and descent trajectory in real time. This data capability serves a dual purpose: it supports post-incident regulatory reporting and provides operators with performance analytics for fleet safety management. According to AVSS, the DJI Mavic 3 Enterprise system records an average descent rate of 3.93 mps and impact energy of 8.11 J — precisely the performance parameters regulators reference when evaluating over-people flight approvals.

As of August 2025, a Spanish SME developed an AI-guided parachute system with a lightweight design under 25 kg, tested at prototype level with flight campaigns planned across altitudes of 120 m, 800 m, and drone-deployed scenarios. AI guidance systems represent the next performance frontier — enabling parachutes to steer toward designated landing zones rather than descending passively. Early movers who commercialize this capability before regulatory bodies formalize guidance-system requirements gain a structural lead over passive-system providers.

Regional Analysis

North America Dominates the UAV Parachute Recovery Systems Market with a Market Share of 45.7%, Valued at USD 63.7 Million

North America leads all regions with a 45.7% share valued at USD 63.7 Million, anchored by the United States’ large defense drone programs and a mature FAA regulatory framework that mandates recovery systems for over-populated-area commercial operations. The region’s established drone procurement infrastructure and early regulatory adoption create conditions that other regions are now beginning to replicate.

Europe UAV Parachute Recovery Systems Market Trends

Europe represents the most dynamic regulatory environment outside North America. EASA’s drone regulations — particularly the SORA framework — require demonstrable risk mitigation for operations over populated areas, and certified parachute recovery systems form a primary compliance pathway. The May 2025 European order secured by ParaZero for its SafeAir M4 system confirms that commercial procurement is accelerating as European delivery operators scale urban operations.

Asia Pacific UAV Parachute Recovery Systems Market Trends

Asia Pacific holds substantial long-term potential, driven by China’s dominant commercial drone manufacturing base and India’s expanding drone policy framework. China deploys large commercial and agricultural drone fleets where recovery system integration remains inconsistent but is tightening under national safety standards. India’s Production Linked Incentive scheme for drones creates downstream demand for certified safety systems as local manufacturing scales.

Middle East and Africa UAV Parachute Recovery Systems Market Trends

The Middle East drives regional demand primarily through defense procurement, where Gulf state militaries operate surveillance and logistics UAV programs at scale. Border monitoring operations in North Africa and the Gulf Cooperation Council zone require recovery systems suited to harsh operating environments. Recovery system vendors with military certification credentials gain prioritized access to government procurement channels in this region.

Latin America UAV Parachute Recovery Systems Market Trends

Latin America presents an early-stage market where commercial drone adoption in agriculture and infrastructure inspection is advancing ahead of recovery system regulation. Brazil and Mexico lead regional drone deployment, but regulatory mandates for recovery system integration remain less developed than in North America or Europe. As national aviation authorities align with ICAO standards, mandatory recovery system requirements will create a compliance-driven procurement wave across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Butler Parachute Systems positions itself at the high-performance end of the recovery systems spectrum, targeting military and Group 3 UAS applications where ruggedization and reliability certifications matter more than unit price. Its April 2025 launch of the AeroSafe Tactical demonstrates a deliberate move toward heavier, mission-critical platforms — a segment with fewer direct competitors and significantly higher per-unit value than the commercial small-drone tier.

ParaZero Ltd. executes a multi-platform commercial strategy that spans product launches, regulatory compliance support, and fleet management software. The company introduced the SafeAir M4, secured a major European distribution order, completed a supply delivery reliability trial, won a defense purchase order from Airobotics, and appointed a new CEO — all within a nine-month window in 2025. This activity velocity signals a company accelerating its market penetration across both commercial and defense channels simultaneously.

Drone Rescue Systems GmbH focuses on the European commercial drone market, where EASA regulatory compliance requirements create the strongest near-term demand pull for certified recovery systems. The company’s positioning in the European regulatory environment gives it proximity to the continent’s most active enforcement-driven procurement cycle. Operators seeking SORA-compliant recovery solutions in Europe encounter Drone Rescue Systems as an established regional specialist rather than an international incumbent.

Fruity Chutes addresses the scalability challenge facing UAV manufacturers who need recovery systems across multiple platform sizes and weight classes. Its March 2025 partnership with High Energy Sports enables the company to offer high-performance solutions at manufacturing volume — a critical capability as drone OEMs seek to integrate recovery systems at the production stage rather than as aftermarket add-ons. This supply chain positioning creates stickier customer relationships than direct operator sales.

Key Players

- Butler Parachute Systems

- ParaZero Ltd.

- Drone Rescue Systems GmbH

- Fruity Chutes

- Mars Parachutes

- Skycat

- Galaxy GRS

- Appareo Systems

- Raven Industries

- DJI

Recent Developments

- January 2025 — Aerial Vehicle Safety Solutions launched the PRS-M4S Parachute Recovery System for the DJI Matrice 4 Series, enabling compliance with flight-over-people regulations. The plug-and-play system achieves deployment in under 0.5 seconds with an average impact energy of 10.1 J.

- April 2025 — ParaZero Technologies introduced the SafeAir M4, an autonomous parachute recovery system for the DJI Matrice 4 series featuring aircraft-grade technology and airbag-based deployment. The system targets operators requiring regulatory approval for urban commercial operations.

- October 2025 — ParaZero received a purchase order from Airobotics for drone safety systems to support defense operations, expanding its presence in the military procurement channel alongside its commercial portfolio.

- June 2025 — EKOFASTBA launched the EKOPARACHUTE ULTRA, certified under new standards for pilotless electric vertical takeoff and landing aircraft. The certification positions the product for emerging eVTOL operators facing mandatory recovery system requirements.

- July 2025 — ParaZero appointed a new CEO to lead advancements in UAS and counter-UAS safety technologies, signaling a strategic expansion beyond standard recovery systems into the broader drone safety platform market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 65.9 Million |

| Forecast Revenue (2035) | USD 139.5 Million |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Load Range (Above 35 Kg, 15–35 Kg, 5–15 Kg, 3–5 Kg, Up to 3 Kg), By Application (Military, Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Butler Parachute Systems, ParaZero Ltd., Drone Rescue Systems GmbH, Fruity Chutes, Mars Parachutes, Skycat, Galaxy GRS, Appareo Systems, Raven Industries, DJI |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |