Quick Navigation

Report Overview

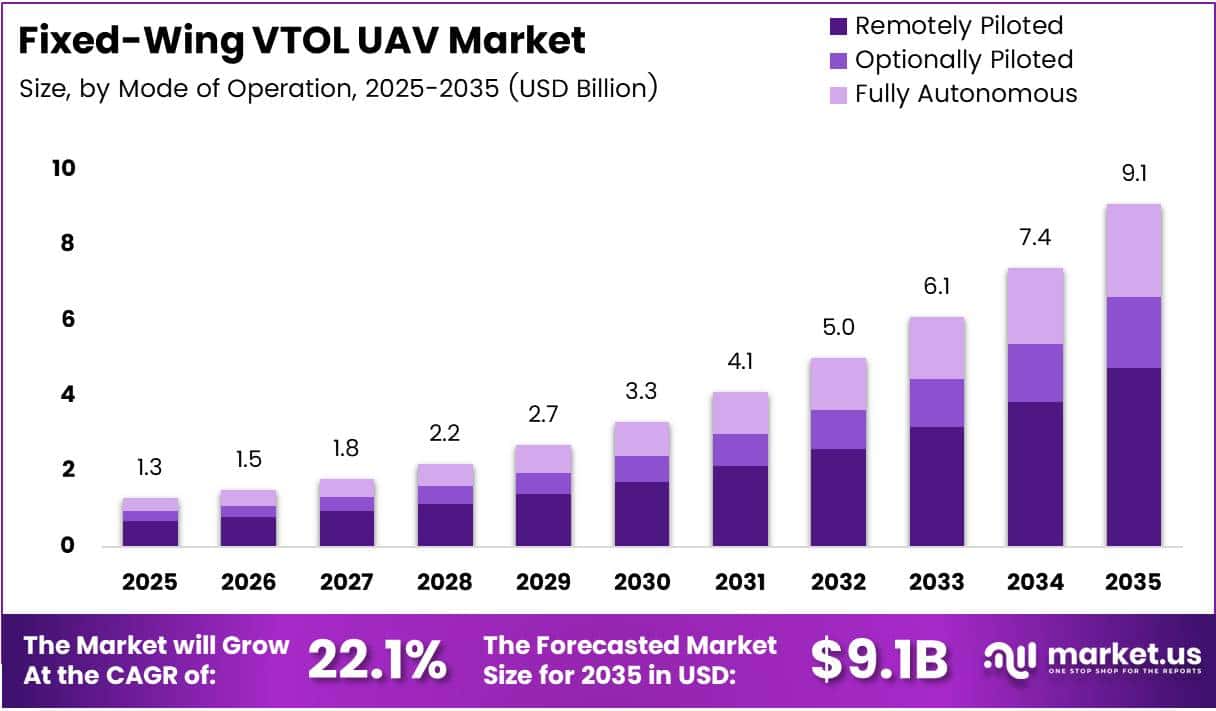

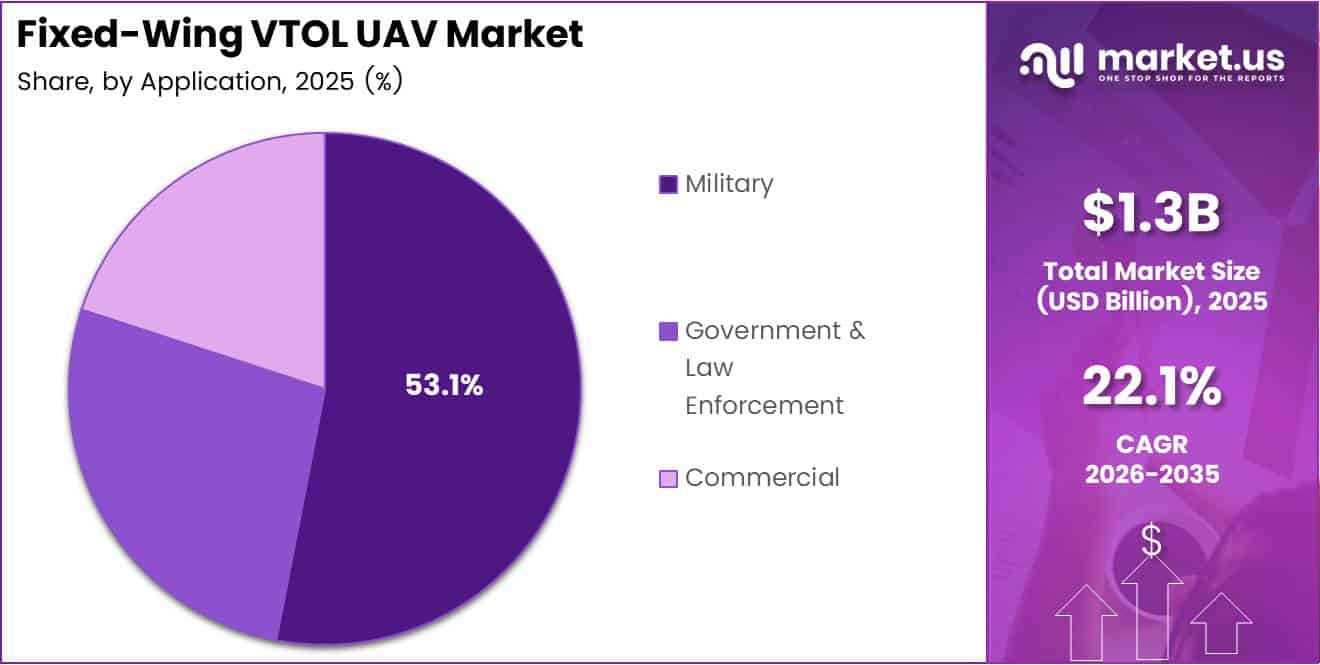

Global Fixed-Wing VTOL UAV Market size is expected to be worth around USD 9.1 Billion by 2035 from USD 1.3 Billion in 2025, growing at a CAGR of 22.1% during the forecast period 2026 to 2035.

Fixed-wing VTOL UAVs combine vertical takeoff and landing capability with the aerodynamic efficiency of fixed-wing flight. This hybrid design solves a long-standing tradeoff in drone engineering — the ability to operate from unprepared terrain while sustaining long-endurance cruise. Defense agencies, commercial operators, and government entities now deploy these platforms across reconnaissance, logistics, and environmental monitoring missions.

Military buyers drive the largest share of current procurement. Defense programs demand UAV platforms capable of multi-hour endurance, high-altitude operation, and payload flexibility — requirements that multirotor systems cannot meet at scale. Fixed-wing VTOL drones fulfill these criteria without the infrastructure dependency of conventional runway-based aircraft, making them strategically attractive for forward-deployed operations.

Commercial adoption adds a parallel growth layer. Agricultural mapping, offshore inspection, and infrastructure monitoring all require wide-area coverage that multirotors cannot deliver cost-effectively. Fixed-wing VTOL systems address this gap by combining hover capability for precision deployment with fixed-wing cruise efficiency for large-area data collection missions.

Regulatory frameworks are beginning to align with operational realities. In June 2025, U.S. Executive Orders directed the FAA to publish a BVLOS Part 108 NPRM by July 6, 2025 and finalize rules by January 31, 2026 — shifting beyond visual line of sight operations from case-by-case waivers to a standardized framework. This transition directly removes one of the most persistent commercial barriers for long-range fixed-wing VTOL operators.

Similarly, Transport Canada’s 2025 rule changes permit routine BVLOS operations for drones up to 150 kg in uncontrolled airspace below 122 m without a Special Flight Operations Certificate. These regulatory shifts signal that North American markets are moving toward operational normalization, which will accelerate commercial procurement cycles in mapping, delivery, and surveillance verticals.

According to Advexure, Wingtra’s WingtraRAY fixed-wing VTOL can map up to 1,300 acres in a single ~1-hour flight, collecting data roughly 10× faster than multicopters and ~30× faster than terrestrial methods. This performance gap signals that fixed-wing VTOL systems do not just replace alternative drones — they replace entire ground survey workflows, compressing project timelines and reducing labor costs at the same time.

According to UAV Model, fixed-wing drones used for long-range surveys cruise at 40–60 mph, allowing coverage of hundreds of acres in under one hour. For commercial buyers evaluating return on investment, this throughput advantage translates directly into lower cost-per-acre data collection — a compelling financial argument that accelerates enterprise adoption across agriculture, utilities, and civil infrastructure sectors.

Key Takeaways

- The global Fixed-Wing VTOL UAV Market was valued at USD 1.3 Billion in 2025 and is forecast to reach USD 9.1 Billion by 2035.

- The market advances at a CAGR of 22.1% during the forecast period 2026 to 2035.

- By Mode of Operation, Remotely Piloted leads the market with a 51.7% share in 2025.

- By Propulsion Type, Electric propulsion holds the dominant position with a 54.9% share.

- By Range, Beyond Line of Sight accounts for 48.5% of the market in 2025.

- By Application, Military holds the largest share at 53.1% in 2025.

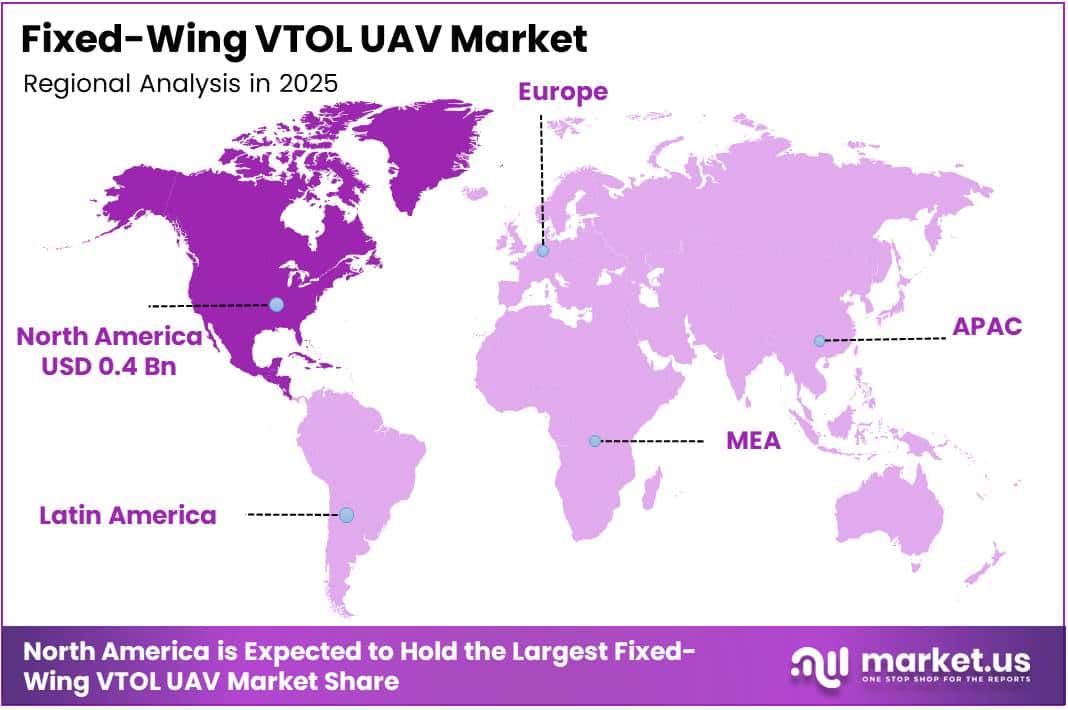

- North America leads all regions with a 37.80% share, valued at USD 0.4 Billion in 2025.

Mode of Operation Analysis

Remotely Piloted dominates with 51.7% due to defense procurement requirements and operator control mandates.

In 2025, Remotely Piloted held a dominant market position in the By Mode of Operation segment of the Fixed-Wing VTOL UAV Market, with a 51.7% share. Military and government buyers require human-in-the-loop command authority for sensitive operations — a structural procurement condition that keeps remotely piloted systems ahead of autonomous alternatives despite advances in onboard AI.

Optionally Piloted systems serve as the transitional architecture for operators moving toward autonomy without fully relinquishing manual control. This configuration appeals to defense agencies testing autonomous protocols in live environments, where mission risk tolerance remains limited. The flexibility to switch between modes reduces procurement hesitancy among buyers cautious about full automation.

Fully Autonomous platforms carry the highest long-term commercial relevance, particularly for repetitive inspection and logistics routes where human supervision adds cost without adding value. However, current regulatory frameworks in most jurisdictions still require remote command authority — meaning autonomous systems face structural market limits until BVLOS rules mature further across key geographies.

Propulsion Type Analysis

Electric dominates with 54.9% due to operational cost advantages and zero-emission compliance requirements.

In 2025, Electric held a dominant market position in the By Propulsion Type segment of the Fixed-Wing VTOL UAV Market, with a 54.9% share. Electric propulsion reduces per-mission fuel costs and maintenance complexity, making it the preferred choice for commercial operators running high-frequency survey and inspection missions where total cost of ownership drives procurement decisions.

Gasoline-powered platforms retain relevance in high-endurance military and long-range commercial applications where battery energy density cannot meet mission duration requirements. These systems trade operational simplicity for extended range, making them the default choice for missions exceeding the practical endurance ceiling of current electric configurations.

Hybrid propulsion represents the most technically ambitious segment. It combines electric vertical lift efficiency with combustion-powered cruise endurance — a configuration designed specifically for missions that demand both VTOL flexibility and multi-hour range. As composite airframe materials reduce overall system weight, hybrid platforms will become progressively more competitive on cost and endurance simultaneously.

Range Analysis

Beyond Line of Sight dominates with 48.5% due to military and long-range commercial mission requirements.

In 2025, Beyond Line of Sight held a dominant market position in the By Range segment of the Fixed-Wing VTOL UAV Market, with a 48.5% share. Defense operations, border surveillance, and offshore inspection missions fundamentally require BVLOS capability — operators cannot restrict these missions to visual range without losing most of their operational value. In February 2024, Wingtra expanded its WingtraOne GEN II platform with a high-precision LiDAR payload delivering 3 cm vertical accuracy from 60 m height, reinforcing the premium placed on sensor performance in long-range survey applications.

Extended Visual Line of Sight platforms occupy the mid-range commercial segment, serving users who need coverage beyond direct visual range but operate under jurisdictions where full BVLOS certification remains unavailable. Infrastructure inspection, corridor mapping, and utility line monitoring are core use cases, and this segment will compress as BVLOS regulatory frameworks expand into more markets.

Visual Line of Sight configurations address shorter-range commercial and training applications. These platforms serve operators in densely regulated airspace or early-stage commercial programs where operators prioritize regulatory simplicity over range. As operators scale their programs, most migrate to EVLOS or BVLOS configurations — making VLOS a gateway rather than a destination segment.

Application Analysis

Military dominates with 53.1% due to defense budget allocation and operational endurance requirements.

In 2025, Military held a dominant market position in the By Application segment of the Fixed-Wing VTOL UAV Market, with a 53.1% share. Defense agencies allocate the largest UAV procurement budgets and impose the most demanding performance specifications — endurance, payload, altitude, and survivability — that fixed-wing VTOL systems are uniquely positioned to satisfy. This structural demand concentration gives defense-oriented manufacturers a durable revenue base.

Government and Law Enforcement applications extend fixed-wing VTOL utility into border security, disaster response, coastal surveillance, and wildfire monitoring. These buyers share military-grade endurance requirements but operate under civilian procurement frameworks with different cost sensitivities. Government programs increasingly fund platforms capable of dual-use across both enforcement and humanitarian response missions.

Commercial applications span agriculture, energy infrastructure, environmental monitoring, and logistics. Commercial buyers evaluate platforms primarily on cost-per-mission efficiency rather than tactical performance. As BxUAV platforms demonstrate control and communication ranges up to 100 km with RTK positioning accuracy of 1 cm + 1 ppm, commercial operators gain access to survey-grade data collection at a fraction of traditional aerial survey costs — a value proposition that widens the addressable commercial buyer pool.

Key Market Segments

By Mode of Operation

- Remotely Piloted

- Optionally Piloted

- Fully Autonomous

By Propulsion Type

- Electric

- Gasoline

- Hybrid

By Range

- Beyond Line of Sight

- Extended Visual Line of Sight

- Visual Line of Sight

By Application

- Military

- Government & Law Enforcement

- Commercial

Drivers

Defense Demand for Long-Endurance Surveillance and Autonomous Border Security Drives Fixed-Wing VTOL UAV Procurement

Defense agencies worldwide require UAV platforms capable of sustained multi-hour flight, high-altitude operation, and reliable payload delivery — performance thresholds that conventional multirotors cannot meet. Fixed-wing VTOL systems satisfy these requirements by combining vertical takeoff flexibility with the aerodynamic efficiency needed for long-range surveillance and reconnaissance missions. This operational advantage translates directly into defense procurement priority.

Border and coastal security programs amplify this demand further. Governments invest in autonomous drone platforms specifically for perimeter monitoring missions where continuous coverage over large geographic areas is operationally non-negotiable. According to academia.edu, conceptual studies of hybrid-electric fixed-wing UAVs show a 59.21% increase in maximum speed and a 37% reduction in energy consumption compared with non-hybrid configurations — performance gains that directly lower per-mission operational cost for defense buyers running high-frequency patrols.

In June 2025, U.S. Executive Orders directed the FAA to publish a BVLOS Part 108 NPRM by July 6, 2025 and finalize rules by January 31, 2026. This regulatory action converts long-range VTOL operations from exception-based waivers into a standardized framework — removing a critical deployment barrier and giving defense contractors a clearer certification pathway for next-generation platform development. For vendors, this signals a procurement acceleration window before market consolidation narrows competitive entry.

Restraints

High Development Costs and Airspace Regulatory Complexity Constrain Fixed-Wing VTOL UAV Market Expansion

Hybrid vertical takeoff and fixed-wing systems require precision engineering across two fundamentally different aerodynamic regimes — vertical lift and horizontal cruise. This dual-mode design challenge drives up both development expenditure and per-unit production cost, creating a pricing barrier that limits procurement among cost-sensitive commercial operators and smaller government agencies operating under constrained budgets.

Maintenance complexity adds a second cost layer. According to Acceleron, a MALE VTOL fixed-wing UAV design requires a VTOL phase peak power of approximately 233 kW, satisfied using eight 30 kW electric motors to balance vertical lift with cruise endurance. Sustaining this level of powertrain complexity across operational lifecycles demands specialized technical personnel and component availability that many operators outside major defense programs cannot consistently support.

Airspace management presents a structural commercial barrier independent of platform cost. Commercial drone deployment requires regulatory clearance across jurisdictions with fragmented approval frameworks — a compliance burden that discourages smaller commercial operators from scaling fixed-wing VTOL programs. Transport Canada’s 2025 rule changes allowing BVLOS below 122 m without a Special Flight Operations Certificate represent progress, but most markets outside North America still impose restrictive airspace access conditions that slow commercial deployment timelines.

Growth Factors

Medical Delivery Expansion, AI Navigation Integration, and Offshore Inspection Demand Open New Revenue Verticals for Fixed-Wing VTOL Operators

Drone-based medical supply delivery in remote and disaster-affected regions creates a structurally distinct demand pool for fixed-wing VTOL systems. These missions require payload security, multi-hour range, and reliable landing in unprepared terrain — all capabilities where fixed-wing VTOL platforms outperform both multirotors and conventional logistics. Government health agencies and humanitarian organizations represent buyers with budget commitments tied to mission criticality rather than cost minimization.

In June 2024, JOUAV unveiled its JOS-C800 next-generation VTOL drone-in-a-box system at the 8th Drone World Congress, combining an automated hangar with the CW-15V VTOL fixed-wing drone to enable fully automated industrial operations with reduced manpower requirements. This product architecture signals a shift from individual platform sales toward integrated infrastructure contracts — a higher-value commercial model that expands revenue per customer significantly.

According to Hinaray, the VF40P hybrid fuel fixed-wing VTOL drone achieves up to 12 hours endurance at a 130 km/h cruise speed, carrying a 2 kg payload at 5,000 m operating altitude. For offshore inspection and maritime surveillance buyers, this endurance profile eliminates the need for support vessels during patrol missions — reducing total mission cost and expanding the commercial case for fixed-wing VTOL systems in energy and maritime sectors.

Emerging Trends

Satellite Communication Integration, Swarm Drone Technology, and Solar-Powered Platforms Redefine Long-Range Fixed-Wing VTOL Mission Architecture

Satellite communication integration in long-range UAV platforms removes the range ceiling imposed by line-of-sight radio links. Defense and commercial operators gain persistent connectivity over oceans, remote terrain, and contested airspace — mission environments where ground-based control infrastructure does not exist. This capability shift transforms fixed-wing VTOL drones from regional assets into globally deployable platforms with strategic operational reach.

Swarm drone technology adds a coordination layer to surveillance and reconnaissance missions. Multiple fixed-wing VTOL units operating collaboratively cover larger areas, provide redundant data streams, and reduce single-point failure risk — operational advantages that individual platforms cannot replicate. Defense agencies investing in swarm coordination software create a parallel procurement demand for compatible fixed-wing VTOL hardware optimized for networked mission profiles.

According to Hinaray, the H70P military-grade fixed-wing VTOL drone sustains up to 10 hours of flight endurance with a 50 kg payload at altitudes up to 6,000 m, reaching maximum speeds of 180 km/h. In January 2024, DronePilot Ground School updated its VTOL platform guide to highlight new long-range VTOL systems entering the market with multi-hour endurance and BVLOS profiles. Together, these data points confirm that solar-powered and high-endurance platforms are moving from experimental concepts into commercially deployable configurations — giving early adopters a performance advantage before these capabilities become standard.

Regional Analysis

North America Dominates the Fixed-Wing VTOL UAV Market with a Market Share of 37.80%, Valued at USD 0.4 Billion

North America holds 37.80% of the global Fixed-Wing VTOL UAV Market, valued at USD 0.4 Billion in 2025. The region leads through a combination of the world’s largest defense procurement budgets, mature drone regulatory infrastructure, and an active commercial UAV sector. The FAA’s 2025 BVLOS framework development further accelerates this lead by providing vendors a clear pathway for commercial long-range platform certification.

Europe Fixed-Wing VTOL UAV Market Trends

Europe builds its fixed-wing VTOL position through defense modernization programs and commercial applications in precision agriculture and infrastructure inspection. NATO member states increasing UAV investment under defense spending commitments, combined with the EU’s advancing drone regulatory framework, create structured procurement pathways for both military and civilian operators across the region.

Asia Pacific Fixed-Wing VTOL UAV Market Trends

Asia Pacific advances through government-driven agricultural modernization and defense capability investment across multiple major economies. India’s 2025 GeM tender specifying fixed-wing VTOL UAVs with operational altitude of 9,000 ft AMSL and payload capacity of 3–3.5 kg reflects active government procurement intent. China’s domestic UAV manufacturing base and Japan’s precision agriculture programs add commercial volume to defense-led regional demand.

Middle East and Africa Fixed-Wing VTOL UAV Market Trends

Middle East and Africa adopt fixed-wing VTOL systems primarily through border security and energy infrastructure inspection programs. Gulf Cooperation Council states invest in long-range surveillance platforms for both territorial monitoring and oil field inspection — missions where multi-hour endurance and large-area coverage justify premium platform investment. African governments deploy these systems selectively for disaster response and humanitarian logistics.

Latin America Fixed-Wing VTOL UAV Market Trends

Latin America develops its fixed-wing VTOL market through agricultural mapping, environmental monitoring, and government security programs. Brazil and Mexico represent the primary demand centers, driven by large agricultural land areas requiring cost-efficient aerial survey solutions and by government investment in border and coastal surveillance infrastructure. Commercial adoption scales progressively as regional regulatory frameworks align with BVLOS operational requirements.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Turkish Aerospace Industries Inc positions itself at the intersection of government-backed R&D and export-oriented defense manufacturing. Its fixed-wing VTOL programs benefit from direct Turkish Ministry of Defence procurement commitments and a growing export pipeline into allied and partner nations. This dual revenue structure — domestic procurement plus exports — reduces dependency on any single program cycle and supports sustained platform development investment.

Boeing Company leverages its systems integration expertise and existing defense customer relationships to compete in the high-end military fixed-wing VTOL segment. Boeing’s strategic advantage lies not in unit volume but in platform integration — embedding VTOL UAVs within broader defense network architectures where switching costs are high and long-term service contracts extend revenue well beyond initial hardware sales.

Textron Inc competes through its established presence across both military and commercial UAV segments, with platform portfolios spanning multiple endurance and payload classes. Textron’s multi-platform strategy allows it to serve different buyer tiers simultaneously — from defense agencies requiring high-endurance reconnaissance assets to commercial operators seeking cost-efficient mapping platforms — reducing revenue concentration risk across program cycles.

Saab Group applies its defense electronics and systems engineering capabilities to fixed-wing VTOL development, focusing on intelligence, surveillance, and reconnaissance applications where sensor integration and data processing matter as much as flight performance. Saab’s positioning in European NATO markets gives it structural access to defense modernization budgets, particularly as European governments accelerate UAV investment under updated NATO spending commitments.

Key Players

- Turkish Aerospace Industries Inc

- Boeing Company

- Textron Inc

- Saab Group

- AeroVironment Inc

- Schiebel Elektronische Gerate GmbH

- Israel Aerospace Industries Ltd

- Lockheed Martin Corporation

- SZ DJI Technology Co., Ltd.

- Northrop Grumman Corporation

Recent Developments

- February 2024 — Wingtra announced a new LiDAR payload option for its WingtraOne GEN II fixed-wing VTOL platform, integrating a high-precision LiDAR sensor designed to deliver vertical accuracy of approximately 3 cm from a 60 m flight height, expanding the platform’s capabilities for advanced infrastructure and terrain mapping use cases.

- June 2024 — JOUAV unveiled its JOS-C800 next-generation VTOL drone-in-a-box system at the 8th Drone World Congress, combining an automated hangar with the CW-15V VTOL fixed-wing drone to enable fully automated industrial drone operations, reducing manpower requirements for continuous monitoring and inspection programs.

- January 2024 — DronePilot Ground School updated its VTOL drones guide to highlight new long-range VTOL platforms entering the commercial market, including fixed-wing VTOL systems offering multi-hour endurance and beyond-visual-line-of-sight mission profiles for mapping and inspection applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.3 Billion |

| Forecast Revenue (2035) | USD 9.1 Billion |

| CAGR (2026-2035) | 22.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Mode of Operation (Remotely Piloted, Optionally Piloted, Fully Autonomous), By Propulsion Type (Electric, Gasoline, Hybrid), By Range (Beyond Line of Sight, Extended Visual Line of Sight, Visual Line of Sight), By Application (Military, Government & Law Enforcement, Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Turkish Aerospace Industries Inc, Boeing Company, Textron Inc, Saab Group, AeroVironment Inc, Schiebel Elektronische Gerate GmbH, Israel Aerospace Industries Ltd, Lockheed Martin Corporation, SZ DJI Technology Co., Ltd., Northrop Grumman Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |