Quick Navigation

Report Overview

North America simulator windows and simulator skylight market size is expected to be worth around USD 9.2 Billion by 2035 from USD 4.5 Billion in 2025, growing at a CAGR of 7.4% during the forecast period 2026 to 2035.

The North America simulator windows and simulator skylight market covers high-fidelity optical systems installed in full-flight simulators, flight training devices, and driving simulators. These components deliver the wide-angle, distortion-free visual fields that regulatory agencies and training operators require. Without qualified visual systems, simulators cannot achieve the certification levels that allow credit for real-world flight hours.

Flight simulation commands the dominant share of this market, reflecting the scale of commercial and military pilot training activity across North America. Aviation training centers operate under strict federal certification standards that directly specify the visual performance parameters their simulator hardware must meet. This regulatory pressure converts visual system upgrades from a discretionary investment into a compliance obligation.

Military flight training programs add a structurally separate demand layer alongside commercial aviation. Defense agencies continuously refresh simulator fleets to match new aircraft platforms, and military procurement cycles tend to be less price-sensitive than commercial ones. This dual demand base gives the market greater revenue stability than single-sector simulation markets typically achieve.

Government mandates drive hardware specifications with unusual precision in this sector. According to the FAA via Simutech Australia, FAA Part 60 mandates a minimum continuous field of view of 176° horizontal and 36° vertical for Level C and Level D full flight simulators. This single specification forces procurement of wide-aperture optical assemblies, eliminating cost-cutting workarounds at the hardware level and concentrating demand with a small group of qualified suppliers.

High-performance visual systems now define competitive differentiation among training operators. According to Wikipedia, modern Level D collimated cross-cockpit display visual systems deliver up to 200° horizontal and 40° vertical field of view using curved-mirror collimation. Operators who exceed minimum thresholds can market their simulators as premium training assets, justifying higher session fees and longer-term contracts with airline clients.

The shift toward next-generation rendering engines and augmented reality integration signals that the market is moving beyond hardware optics toward software-defined visual performance. This transition expands addressable revenue beyond the physical window assembly toward integrated system contracts. Vendors who combine certified optical structures with proprietary rendering platforms position themselves to capture recurring software and upgrade revenue on top of initial hardware sales.

North America’s combination of the world’s largest commercial aviation training infrastructure, active military simulation procurement, and a well-developed aerospace supply chain creates structural advantages that other regions will take years to replicate. The 7.4% CAGR reflects a market where compliance-driven replacement cycles and technology-led upgrades reinforce each other, reducing the volatility that typically characterizes capital equipment markets of this size.

Key Takeaways

- The North America simulator windows and simulator skylight market was valued at USD 4.5 Billion in 2025.

- The market is forecast to reach USD 9.2 Billion by 2035, growing at a CAGR of 7.4% from 2026 to 2035.

- By Application, Flight Simulation leads with a 67.9% share in 2025.

- By End User, Aviation holds the largest share at 61.5% in 2025.

- North America dominates the global simulator visual systems landscape, supported by FAA Part 60 certification requirements and large-scale pilot training infrastructure.

- Key players operating in this market include CAE, Inc., L3Harris Technologies, Rockwell Collins Inc., Thales Group, Frasca International, and Ansys, among others.

Application Analysis

Flight Simulation dominates with 67.9% due to FAA certification mandating high-fidelity visual systems.

In 2025, Flight Simulation held a dominant market position in the By Application segment of the North America simulator windows and simulator skylight market, with a 67.9% share. FAA Part 60 certification requirements force training operators to procure wide-angle, optically qualified window assemblies for Level C and Level D devices. This compliance-driven purchase cycle sustains predictable, recurring hardware demand regardless of airline market conditions.

Driving Simulation serves as a secondary but structurally distinct demand channel within the simulator visual systems market. Automotive OEMs, defense vehicle programs, and road safety research institutions deploy driving simulators with curved skylight and wraparound window assemblies for realistic environment rendering. However, this segment lacks the federally mandated specification floors that anchor flight simulation procurement, which limits average selling prices and volume predictability compared to aviation applications.

Others covers maritime, rail, and industrial operator training simulators that use adapted visual window systems. These applications draw on flight simulation optical technology but deploy it in lower-volume, application-specific configurations. The segment contributes incremental revenue for suppliers with flexible manufacturing capabilities, though it does not offer the scale or margin structure of aviation-driven demand.

End User Analysis

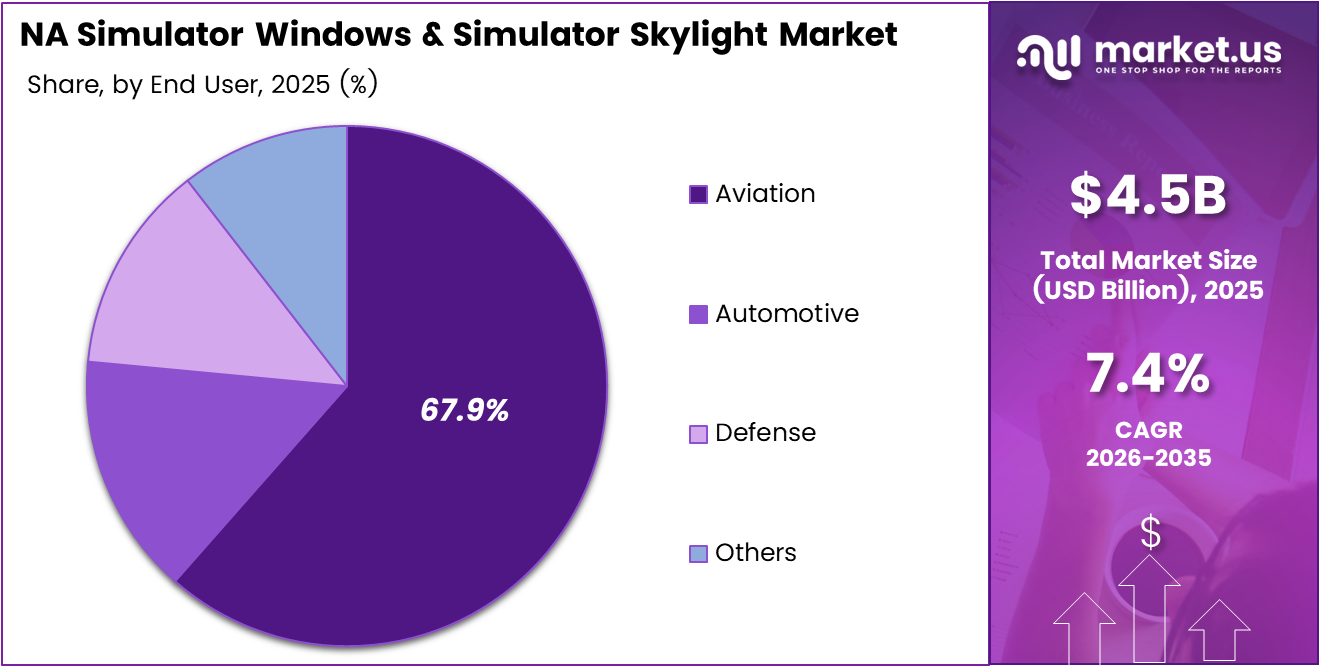

Aviation dominates with 61.5% due to federally mandated simulator certification requirements.

In 2025, Aviation held a dominant market position in the By End User segment of the North America simulator windows and simulator skylight market, with a 61.5% share. Commercial airlines, regional carriers, and independent flight training organizations all operate under FAA Part 60 or Transport Canada standards that require certified visual field performance. This regulatory foundation makes simulator window replacement and upgrading a recurring budget line rather than a discretionary capital decision.

Automotive end users procure simulator visual systems primarily for advanced driver assistance system validation and vehicle dynamics research. These buyers prioritize curved, wide-aperture skylight structures that replicate real-world peripheral visibility. Demand from this segment correlates with R&D investment cycles in autonomous and semi-autonomous vehicle programs, making it a faster-growing but less predictable revenue contributor than aviation.

Defense end users encompass military aviation, armored vehicle simulation, and special operations training programs. Defense procurement brings higher-specification requirements and greater budget capacity per unit than commercial aviation, but procurement timelines are longer and subject to program-level budget decisions. Nevertheless, defense contracts provide volume backstop revenue when commercial aviation training investment slows.

Others includes maritime academies, rail operator training programs, and space mission simulation facilities. These buyers represent niche but high-value opportunities, particularly where simulation fidelity requirements approach aviation-grade standards. Suppliers that already serve aviation certification requirements can address this segment with minimal product adaptation, making it a natural expansion path for established visual systems vendors.

Key Market Segments

By Application

- Flight Simulation

- Driving Simulation

- Others

By End User

- Aviation

- Automotive

- Defense

- Others

Drivers

FAA Regulatory Mandates and Commercial Fleet Expansion Force High-Specification Visual System Procurement

North American pilot training centers face direct procurement pressure from FAA Part 60 certification standards. According to Simutech Australia, FAA Part 60 requires full flight simulators to demonstrate a minimum of ten distinct occulting levels to simulate conditions such as fog and rain. This single requirement forces operators to procure visual systems that go well beyond basic optical performance, raising the floor on hardware investment across the sector.

Commercial aviation fleet expansion multiplies the number of pilots requiring simulator training hours before line operations. Airlines expanding their North American routes must certify new pilots against the fleet types they will fly, driving proportional growth in Level C and Level D simulator utilization. In November 2025, AXIS Flight Simulation qualified the first U.S.-based Level D Bombardier Challenger 350 full flight simulator for VistaJet America, equipped with an RSi XT6 visual system delivering a 200° × 45° field of view — illustrating how new aircraft type entries translate directly into demand for certified simulator visual hardware.

Military flight training programs add a further procurement layer that operates independently of commercial aviation cycles. Defense agencies require simulator visual systems that replicate specific threat environments and operational conditions, pushing technical specifications beyond commercial minimums. This dual-stream demand structure — commercial compliance-driven and defense mission-driven — means the market absorbs volume without the synchronization risk that single-sector dependency creates.

Restraints

High Certification Costs and a Narrow Supplier Base Constrain Market Scalability

Aviation-grade simulator windows and skylights carry manufacturing and certification costs that most industrial optical suppliers cannot absorb. Components must pass rigorous structural, optical distortion, and thermal performance tests before qualifying under FAA Part 60 and equivalent standards. These certification barriers limit the number of viable suppliers, which reduces competitive pressure on pricing and extends procurement lead times for training operators.

The specialized optical and composite materials required for high-fidelity simulator windows come from a limited number of qualified sources. Supply chain concentration at the materials level creates cost and availability risk that cascades through the finished product. When material lead times lengthen, simulator manufacturers face project delays, which in turn slow revenue recognition and create scheduling problems for training operators who have contracted pilot throughput commitments.

Together, these cost and supply constraints act as a structural ceiling on market participation. New entrants face a multi-year certification runway and substantial upfront tooling investment before generating any revenue. Established suppliers benefit from this barrier, but the same dynamic limits the supply response when demand accelerates — creating periodic capacity shortfalls that push hardware prices upward and extend delivery timelines across the market.

Growth Factors

AR and MR Integration and Next-Generation Training Infrastructure Expand the Addressable Market for Simulator Visual Systems

The integration of augmented reality and mixed reality visual systems into flight simulators transforms the simulator window from a passive optical component into an active display interface. This shift expands the revenue opportunity per simulator installation, as AR/MR-capable assemblies carry higher average selling prices and require tighter integration with rendering platforms. Vendors who develop certified AR/MR-compatible window systems position themselves to capture a growing share of premium simulator upgrade contracts.

According to Simutech Australia, lower-qualification FAA Part 60 flight training device levels A and B require a minimum continuous FOV of 45° horizontal and 30° vertical per pilot. The large installed base of lower-level FTDs represents a significant upgrade pipeline as operators seek Level C and Level D certification status. In February 2026, CAE announced at the Singapore Airshow that Embraer-CAE Training Services purchased its first CAE 3000 series full-flight simulator for Eve Air Mobility eVTOL pilot training, integrating the next-generation CAEProdigy Visual System powered by Unreal Engine — signaling that new aircraft categories are creating entirely new simulator qualification requirements.

Regional and business aviation training facilities represent an underpenetrated segment where investment is accelerating. Business jet operators and regional carriers increasingly require dedicated simulator access rather than relying on shared airline training centers, driving new simulator builds that each carry a full visual system requirement. Lightweight, high-durability transparent materials are enabling more cost-effective construction of these facilities, lowering the capital threshold for new training center development and broadening the buyer base for simulator window systems.

Emerging Trends

Ultra-High Resolution Rendering and Curved Skylight Structures Redefine Visual Fidelity Standards for Simulator Certification

Simulator manufacturers are shifting toward ultra-high resolution projection systems that demand physically larger and optically flatter window assemblies to preserve image quality across wide fields of view. This hardware requirement elevates specifications for both the transparent structure and its mounting system. Operators who invest in these systems differentiate their training centers on measurable fidelity metrics, which translates into pricing power when competing for airline and defense training contracts.

Curved skylight structures enabling 360° pilot visibility are moving from experimental installations into production simulator designs. These assemblies replace segmented flat panels with continuous curved opticals, eliminating distortion at panel joints and providing more realistic peripheral environment rendering. In November 2025, Frasca International launched VITAL FVS 100, a next-generation visual system powered by Unreal Engine featuring one-meter resolution terrain imagery and volumetric cloud modeling with VR/MR support — demonstrating how software-defined rendering is raising the performance bar that physical window assemblies must match.

Collaboration between simulator manufacturers and aerospace OEMs is accelerating type-specific visual system development. When an OEM introduces a new aircraft, simulator developers now work earlier in the product cycle to build cockpit visual environments that match production aircraft geometry precisely. Modular and reconfigurable simulator cockpit designs further reinforce this trend, as operators seek hardware that can be updated to new type variants without full replacement — creating recurring revenue opportunities for visual system suppliers across the aircraft’s service life.

Key Company Insights

CAE, Inc. holds a structurally advantaged position by combining simulator manufacturing, visual system development, and pilot training operations under one organization. This vertical integration allows CAE to align hardware certification cycles with its own training center procurement needs, compressing the sales cycle and reducing third-party dependency. CAE’s CAEProdigy Visual System, deployed in its 3000 series simulators for eVTOL training, signals a deliberate push into next-generation aircraft categories ahead of competitors.

L3Harris Technologies approaches the simulator visual systems market through its defense electronics heritage, giving it certified access to military simulation procurement channels that commercial-only suppliers cannot easily enter. Defense training programs require visual systems that replicate classified threat environments under strict operational security conditions. L3Harris’s ability to operate within those constraints positions it as a preferred supplier for high-specification military simulator visual hardware where security clearance and defense contracting experience matter as much as optical performance.

Rockwell Collins Inc. (now part of Collins Aerospace) leverages its deep integration within commercial aircraft avionics and cockpit systems to extend credibility into simulator visual system supply. Airline operators who already standardize on Collins avionics show a demonstrated preference for suppliers they trust across multiple aircraft systems, reducing procurement friction. This cross-system relationship gives Collins a non-optical competitive advantage that pure visual system vendors cannot replicate through product specification alone.

Thales Group brings a dual commercial and defense customer base to the simulator visual systems market, with established relationships across European and North American defense agencies. Thales’s simulation division benefits from platform integration work on military aircraft programs, which creates natural downstream demand for training simulators matching those platforms. Its investment in next-generation rendering and image generation technology positions it to address the ultra-high resolution visual system upgrades that Level D operators now prioritize.

Key Players

- CAE, Inc.

- L3Harris Technologies

- Rockwell Collins Inc.

- Thales Group

- Frasca International

- Ansys

- LIXIL

- VELUX

- YKKAP

- Sankyo Alumi

- CoeLux

- Okalux

Recent Developments

- February 2026 — FlightSafety International launched the industry’s first Advanced Circling and Visual Approach Course, combining eLearning, facilitated ground sessions, and hands-on simulator training. The course covers mountainous terrain, low-visibility, and tight-maneuvering scenarios, directly expanding the use case for high-fidelity simulator visual systems in advanced procedural training.

- February 2026 — CAE announced at the Singapore Airshow that Embraer-CAE Training Services purchased the first CAE 3000 series full-flight simulator dedicated to Eve Air Mobility eVTOL pilot training. The simulator integrates the next-generation CAEProdigy Visual System powered by Unreal Engine, establishing a new certification precedent for eVTOL-category visual training requirements.

- November 2025 — AXIS Flight Simulation qualified the first U.S.-based Level D Bombardier Challenger 350 full flight simulator for VistaJet America. The simulator features an RSi XT6 visual system delivering a 200° × 45° field of view, meeting and exceeding FAA Part 60 Level D visual field minimums for this aircraft type.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.5 Billion |

| Forecast Revenue (2035) | USD 9.2 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Flight Simulation, Driving Simulation, Others), By End User (Aviation, Automotive, Defense, Others) |

| Competitive Landscape | CAE, Inc., L3Harris Technologies, Rockwell Collins Inc., Thales Group, Frasca International, Ansys, LIXIL, VELUX, YKKAP, Sankyo Alumi, CoeLux, Okalux |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |