Quick Navigation

Report Overview

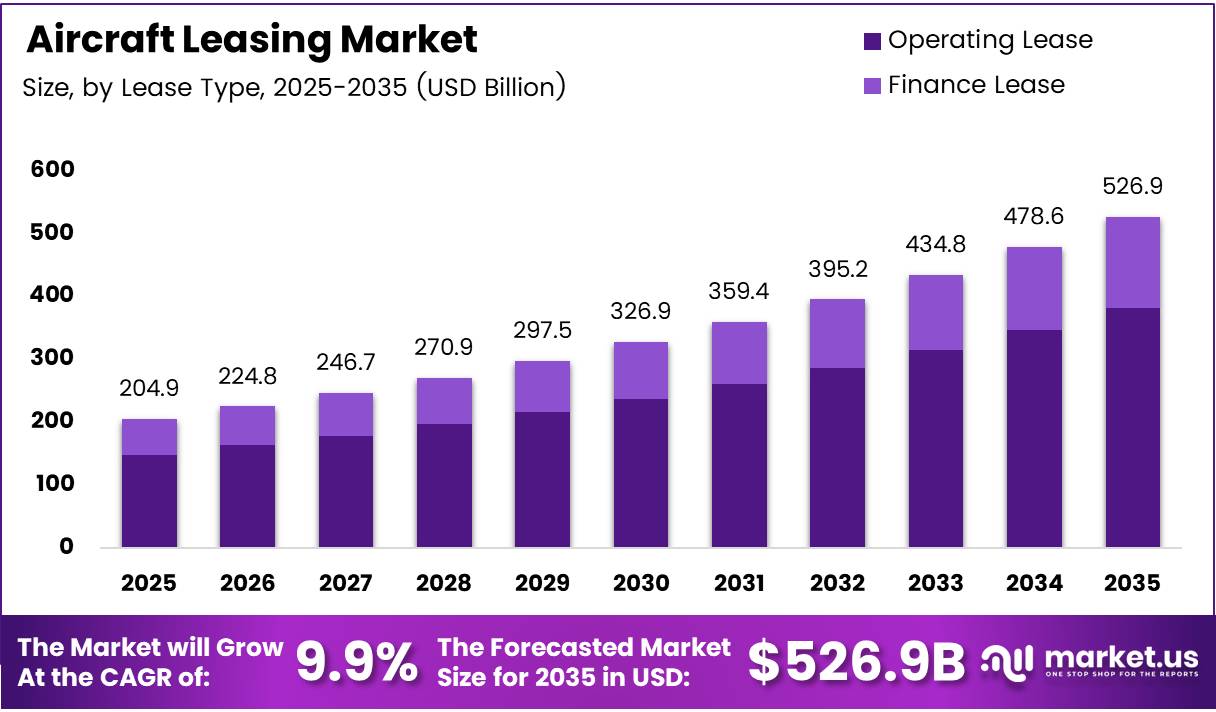

Global Aircraft Leasing Market size is expected to be worth around USD 526.9 Billion by 2035 from USD 204.9 Billion in 2025, growing at a CAGR of 9.9% during the forecast period 2026 to 2035.

Aircraft leasing allows airlines to operate fleets without the capital burden of direct ownership. Lessors purchase aircraft from manufacturers and lease them to carriers under operating or finance structures. This model separates asset ownership from fleet operations, giving airlines access to modern aircraft while preserving balance sheet flexibility.

Operating leases dominate this market because they let airlines return aircraft at contract end rather than carry depreciation risk. This structure is especially attractive when aircraft values fluctuate or when carriers want to scale capacity without committing to long-term asset ownership. The lease model has become a structural pillar of global commercial aviation finance.

Low-cost carriers and full-service airlines alike rely on leasing to manage fleet composition. For budget operators, leasing enables rapid expansion with minimal upfront capital. For legacy carriers, it provides route flexibility — adding or reducing capacity in response to demand shifts without the friction of direct asset disposal.

Consolidation is reshaping lessor market structure. In September 2025, Sumitomo Corporation and SMBC Aviation Capital announced a USD 7.4 billion acquisition of Air Lease Corporation at USD 65 per share, to be renamed Sumisho Air Lease Corporation (Ireland) DAC. This deal signals that institutional capital is treating aviation assets as a scaled, long-duration investment class rather than a niche sector.

According to Aviation Week, the active commercial fleet is projected to grow from 34,008 aircraft in 2025 to 44,600 aircraft by 2034. This fleet expansion of over 10,000 aircraft represents direct incremental demand for lease financing, since the majority of new deliveries will enter service under operating lease agreements rather than airline-owned structures.

According to IATA, industry-wide fuel efficiency improvements slowed to just 0.3% in 2025 versus the historical 2.0% annual rate, due to delayed fleet renewal. This slowdown tells us that older, less efficient aircraft remain in service longer than planned — creating direct pressure on airlines to accelerate fleet replacement through leasing rather than absorbing the operating cost of aging fleets.

Emerging aviation economies in Asia Pacific, the Middle East, and Latin America are expanding lessor pipelines as local carriers pursue fleet growth without deep capital markets access. These regions now represent the next phase of aircraft leasing demand, as full-service and low-cost carriers in high-growth travel markets require modern narrow body and widebody aircraft on flexible terms.

Key Takeaways

- The global Aircraft Leasing Market was valued at USD 204.9 Billion in 2025 and is forecast to reach USD 526.9 Billion by 2035, at a CAGR of 9.9%.

- By Lease Type, Operating Lease leads with a 72.4% share, reflecting airline preference for off-balance-sheet fleet access.

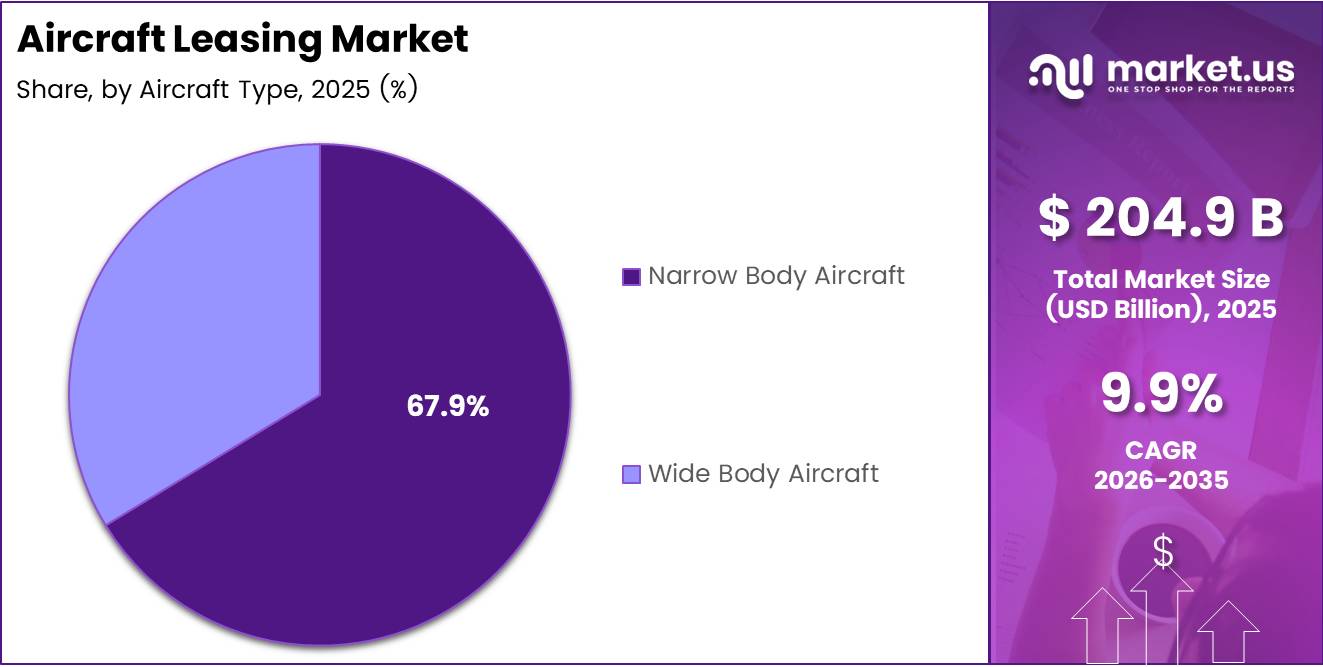

- By Aircraft Type, Narrow Body Aircraft holds the dominant position with a 66.3% share, driven by short-haul route expansion.

- By Airline Type, Full-Service Carriers account for 56.2% of market share, anchoring lessor revenue through large, long-term fleet agreements.

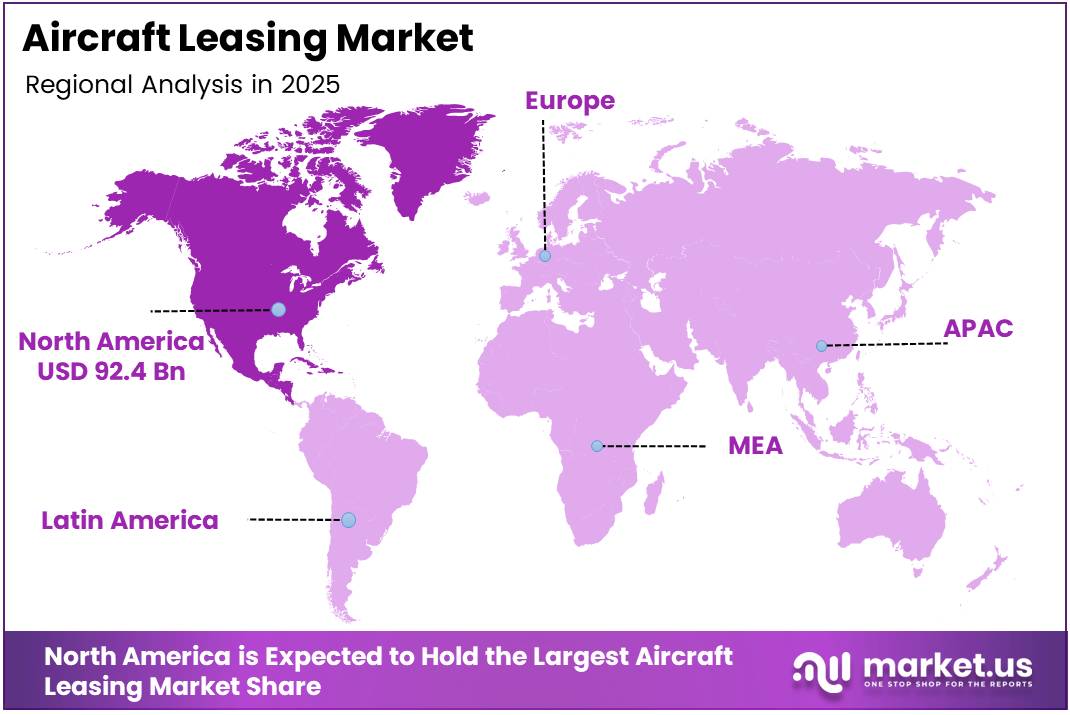

- North America dominates regional markets with a 45.30% share, valued at approximately USD 92.4 Billion.

- The active commercial fleet is projected to grow from 34,008 aircraft in 2025 to 44,600 by 2034, expanding total lessor addressable supply.

Product Analysis

Operating Lease dominates with 72.4% due to off-balance-sheet flexibility for airlines.

In 2025, Operating Lease held a dominant market position in the By Lease Type segment of the Aircraft Leasing Market, with a 72.4% share. Airlines choose operating leases because they avoid aircraft depreciation risk, preserve debt capacity, and allow fleet adjustments at contract end. This structure suits carriers operating in demand-volatile routes where long-term asset commitment carries financial risk.

Finance Lease serves airlines that seek long-term control over specific aircraft without full purchase capital. Under a finance lease, the airline carries the asset on its balance sheet and assumes residual value risk at term end. Consequently, this structure appeals to larger carriers with stable revenue forecasts and a preference for eventual ownership of mission-critical fleet types.

Aircraft Type Analysis

Narrow Body Aircraft dominates with 66.3% due to short-haul route dominance and LCC fleet growth.

In 2025, Narrow Body Aircraft held a dominant market position in the By Aircraft Type segment of the Aircraft Leasing Market, with a 66.3% share. Narrowbody types — primarily the Boeing 737 and Airbus A320 families — form the operational core of both low-cost and regional full-service fleets. High delivery volumes and standardized maintenance profiles make narrowbodies the most liquid asset class in the secondary leasing market.

Wide Body Aircraft carries the highest per-unit lease value within the aircraft type segment. Long-haul routes require widebody capacity, and full-service carriers lease these assets to serve intercontinental networks without committing to outright purchase of aircraft valued above USD 200 million per unit. However, widebody lessors carry higher residual value risk given thinner secondary market depth and longer remarketing cycles.

Airline Type Analysis

Full-Service Carriers dominate with 56.2% due to large fleet scale and long-term lease commitments.

In 2025, Full-Service Carriers held a dominant market position in the By Airline Type segment of the Aircraft Leasing Market, with a 56.2% share. These carriers operate diverse fleets spanning narrowbody, widebody, and regional aircraft — requiring lease agreements across multiple aircraft types. Their size and credit standing allow them to negotiate favorable lease terms, making them anchor clients for major lessors.

Low-Cost Carriers differentiate through high asset utilization and single-fleet-type strategies that simplify lease management. LCCs typically concentrate on narrowbody operating leases, cycling aircraft on shorter terms to maintain fleet recency. Moreover, their growth in Asia Pacific and Latin America is creating a new pipeline of lessor clients in markets where aviation infrastructure is expanding faster than carrier capital access.

Key Market Segments

By Lease Type

- Operating Lease

- Finance Lease

By Aircraft Type

- Narrow Body Aircraft

- Wide Body Aircraft

By Airline Type

- Full-Service Carriers

- Low-Cost Carriers

Drivers

Fleet Expansion and Capital Efficiency Force Airlines Toward Operating Lease Structures

Airlines worldwide face a structural tension: passenger traffic keeps rising, but purchasing aircraft outright consumes capital that most carriers cannot afford to deploy. Operating lease agreements resolve this tension directly. Airlines access modern aircraft immediately, preserve balance sheet capacity, and return assets at contract end — transferring ownership risk entirely to the lessor.

Low-cost carriers accelerate this shift. LCC business models depend on rapid fleet scaling with minimal fixed capital. Leasing lets them add routes and capacity in response to demand without the lag of direct purchase financing. In December 2025, SMBC Aviation Capital executed a purchase and leaseback of 20 Boeing 737 MAX 9 aircraft with United Airlines for deliveries in 2025 and 2026, demonstrating that even large full-service carriers use leaseback structures to monetize fleet assets.

Global passenger traffic growth amplifies lessor demand at scale. According to Aviation Week, the active commercial fleet will grow from 34,008 aircraft in 2025 to 44,600 by 2034 — an addition of over 10,000 aircraft. Since most new deliveries enter service under lease agreements, this fleet growth translates directly into expanding lessor portfolios and a sustained long-term revenue base for aircraft leasing companies.

Restraints

Airline Credit Risk and Aircraft Residual Value Uncertainty Constrain Lessor Returns

Aircraft lessors face a fundamental credit exposure: their revenue depends on airline financial health, but airlines operate in one of the most economically sensitive industries. When carriers face bankruptcy or cash shortfalls, lease payment defaults follow. Lessors must then repossess, remarket, and re-lease aircraft — a process that can take 12 to 18 months and erodes portfolio yield significantly.

Residual value risk compounds this exposure. Aircraft values in the secondary market fluctuate with fuel prices, manufacturer delivery backlogs, and technology cycles. A lessor holding aging narrowbody or widebody aircraft faces potential write-downs if next-generation replacements compress secondary market pricing. According to IATA, fuel efficiency gains slowed to just 0.3% in 2025 against a historical 2.0% rate — meaning older aircraft remain in fleets longer, reducing lessor flexibility to cycle assets at optimal residual values.

Together, these risks raise the cost of aircraft leasing capital. Institutional investors and lenders price airline credit exposure into portfolio financing terms, which reduces lessor margins and limits their ability to offer competitive lease rates. Consequently, smaller lessors with concentrated airline exposure face a structural disadvantage compared to diversified global platforms with spread credit risk and broader remarketing networks.

Growth Factors

Next-Generation Narrowbodies, Sale-Leaseback Structures, and Emerging Markets Open New Lessor Revenue Streams

Fuel-efficient next-generation narrowbody aircraft — specifically the Boeing 737 MAX and Airbus A320neo families — represent the highest-demand asset class in the leasing market. Airlines replacing aging narrowbodies prioritize these types for their lower operating costs per seat. Lessors that build early positions in these delivery pipelines capture premium lease rates and face lower remarketing risk given strong secondary demand.

Sale-leaseback transactions give airlines a mechanism to raise immediate capital by selling owned aircraft to lessors and leasing them back under operating terms. In February 2026, Aviation Capital Group acquired a 24-aircraft portfolio from Avolon — comprising 18 narrowbody and 6 widebody aircraft on lease to 17 airlines across 16 countries — demonstrating active portfolio trading as a growth strategy for well-capitalized lessors seeking diversified asset exposure.

Emerging aviation economies in Southeast Asia, South Asia, the Middle East, and Latin America now represent the fastest-expanding lessor client base. Carriers in these regions lack deep domestic capital markets but need modern fleets to compete. Additionally, sustainable aviation fleet financing — linking lease terms to ESG criteria — is creating new institutional investor appetite for aviation assets that were previously considered outside impact mandates.

Emerging Trends

Consolidation, Institutional Capital, and Digitalization Restructure the Aircraft Leasing Industry

Consolidation is concentrating aircraft leasing into fewer, larger platforms with greater balance sheet depth and airline negotiating power. In September 2025, the USD 7.4 billion acquisition of Air Lease Corporation by Sumitomo Corporation and SMBC Aviation Capital confirmed that industrial conglomerates and financial institutions view leasing scale as a durable competitive advantage. Smaller lessors face growing pressure to merge or exit the market.

Institutional investors — pension funds, sovereign wealth vehicles, and infrastructure allocators — increasingly treat aircraft as a long-duration asset class comparable to infrastructure. This capital shift lowers the cost of funding for well-structured leasing platforms and extends lease terms as both lessor and investor seek stable, long-dated cash flows. Long-term lease agreements reduce remarketing risk and provide airlines with fleet certainty over multi-year planning cycles.

Digitalization is transforming lease administration and asset tracking. Lessors adopting data-driven lease management platforms reduce manual overhead in aircraft monitoring, maintenance coordination, and contract compliance. Moreover, digital asset tracking improves residual value management by providing real-time condition data that supports more accurate aircraft valuations — a capability that becomes a competitive differentiator as portfolio complexity and global fleet scale increase.

Regional Analysis

North America Dominates the Aircraft Leasing Market with a Market Share of 45.30%, Valued at USD 92.4 Billion

North America commands 45.30% of the global aircraft leasing market, valued at USD 92.4 Billion. The region’s dominance reflects its concentration of global lessor headquarters, deep capital markets, and mature airline procurement infrastructure. Major leasing platforms based in the US and Ireland (operated under US-affiliated ownership) originate a significant share of global lease transactions from this base.

Europe Aircraft Leasing Market Trends

Europe hosts several of the world’s largest aircraft lessors, benefiting from Ireland’s favorable leasing legal framework and established aviation finance ecosystem. European lessors maintain diversified global portfolios, reducing regional credit concentration. The region also benefits from strong intra-European narrowbody demand as budget carriers expand point-to-point networks across EU member states.

Asia Pacific Aircraft Leasing Market Trends

Asia Pacific represents the highest-growth leasing market globally, driven by fleet expansion among carriers in China, India, and Southeast Asia. Chinese lessors — backed by state capital — have built significant narrowbody and widebody portfolios in the past decade. Additionally, India’s rapid aviation sector expansion positions it as a primary source of incremental lessor demand through the forecast period.

Middle East and Africa Aircraft Leasing Market Trends

The Middle East hosts expanding full-service carriers that combine owned and leased aircraft across widebody and narrowbody types. Gulf carriers use leasing selectively to manage fleet transitions and peak-capacity requirements. Africa’s underpenetrated aviation market presents longer-term lessor opportunities, though weak airline credit quality and infrastructure gaps currently constrain activity levels.

Latin America Aircraft Leasing Market Trends

Latin America’s aircraft leasing demand reflects the region’s mix of financially constrained carriers with high fleet replacement needs. LCCs in Brazil and Mexico rely almost entirely on operating leases to fund narrowbody fleet operations. However, currency risk and periodic airline insolvencies — particularly in Argentina and Colombia — create residual value and payment recovery challenges for lessors active in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Carter Airline operates as a specialized aviation services provider with a focused leasing profile targeting specific regional or carrier segments. Its strategy centers on niche positioning — serving markets or fleet types underserved by the largest global platforms. This concentration gives it speed and flexibility in deal execution, though it carries higher client concentration risk compared to diversified multi-portfolio lessors.

AerCap Holdings N.V. holds the position of the world’s largest aircraft lessor by fleet size, with a portfolio spanning narrowbody, widebody, and turboprop types across global airline clients. Its scale advantage translates directly into procurement leverage with Boeing and Airbus, lower per-unit financing costs, and superior remarketing depth. AerCap’s diversified geographic and airline exposure reduces the impact of any single carrier default on portfolio performance.

Air Lease Corporation built its portfolio around direct orders with manufacturers, giving it early delivery positions on next-generation aircraft that command premium lease rates. However, the announced acquisition by Sumitomo Corporation and SMBC Aviation Capital in September 2025 — valued at USD 7.4 billion at USD 65 per share — will integrate ALC into a larger platform, reshaping its strategic independence and potentially accelerating its Asian market penetration under new ownership.

Aviation Capital Group has pursued active portfolio acquisition as its primary growth lever. Following its February 2026 acquisition of a 24-aircraft portfolio from Avolon — with assets on lease to 17 airlines across 16 countries — ACG became the largest lessor customer for the Boeing 737–10 variant. This positions ACG at the front of the next-generation narrowbody cycle, where delivery slots translate into durable lease placement advantages.

Key Players

- AerCap Holdings N.V.

- Air Lease Corporation

- Aviation Capital Group

- Avolon

- BOC Aviation

- Carlyle Aviation Partners

- Carter Airline

- CDB Aviation

- Dubai Aerospace Enterprise (DAE)

- ICBC Leasing

- Jackson Square Aviation

- Macquarie AirFinance

- Nordic Aviation Capital

- SMBC Aviation Capital

- TrueNoord

Recent Developments

- February 2026 — Aviation Capital Group signed definitive agreements with Avolon Aerospace Leasing to acquire a portfolio of 24 aircraft (18 narrowbody, 6 widebody), on lease to 17 airlines across 16 countries, with an average portfolio age of 4.5 years. This transaction diversified ACG’s global airline client exposure while strengthening its narrowbody fleet depth ahead of next-generation delivery cycles.

- February 2026 — Aviation Capital Group became the largest lessor customer for the Boeing 737–10 variant following its 24-aircraft Avolon portfolio acquisition. This positioning at the front of a high-demand next-generation narrowbody variant gives ACG a structural advantage in lease placement and manufacturer relationship leverage through the forecast period.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 204.9 Billion |

| Forecast Revenue (2035) | USD 526.9 Billion |

| CAGR (2026-2035) | 9.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Lease Type (Operating Lease, Finance Lease), By Aircraft Type (Narrow Body Aircraft, Wide Body Aircraft), By Airline Type (Full-Service Carriers, Low-Cost Carriers), By Region and Companies |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Carter Airline, AerCap Holdings N.V., Air Lease Corporation, Aviation Capital Group, Avolon, BOC Aviation, Carlyle Aviation Partners, CDB Aviation, Dubai Aerospace Enterprise (DAE), ICBC Leasing, Jackson Square Aviation, Macquarie AirFinance, Nordic Aviation Capital, SMBC Aviation Capital, TrueNoord |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |