Quick Navigation

Report Overview

The Global Cut Resistant Glove Market size is expected to be worth around USD 3.1 Billion by 2035, from USD 1.5 Billion in 2025, growing at a CAGR of 7.4% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 32.5% share, holding USD 4.1 Billion revenue.

The cut-resistant gloves market is shaped by increasing emphasis on occupational safety in environments where workers are exposed to sharp tools, metal components, and high-speed machinery. Adoption is widely observed across manufacturing, automotive, construction, oil & gas, and food processing activities, where hand injuries such as cuts and lacerations remain a persistent operational risk.

Demand is primarily supported by the shift toward safer workplace practices and the integration of standardized protective equipment into industrial procurement systems. Gloves designed with synthetic fibers, aramid blends, and advanced composites are increasingly preferred due to their ability to balance protection with dexterity, enabling efficient handling of tools and materials. Compliance with internationally recognized safety frameworks such as ANSI/ISEA 105 and EN 388 further reinforces product selection across industries.

Manufacturers are focusing on improving material performance, enhancing comfort, and developing task-specific solutions to meet diverse operational requirements. Similarly, growing industrial activity in emerging economies and heightened awareness of worker safety continue to support steady adoption of cut-resistant protective solutions across global end-use sectors.

Key Takeaways

- The global cut resistant glove market was valued at USD 1.5 billion in 2025.

- The global cut resistant glove market is projected to grow at a CAGR of 7.4% and is estimated to reach USD 3.1 billion by 2035.

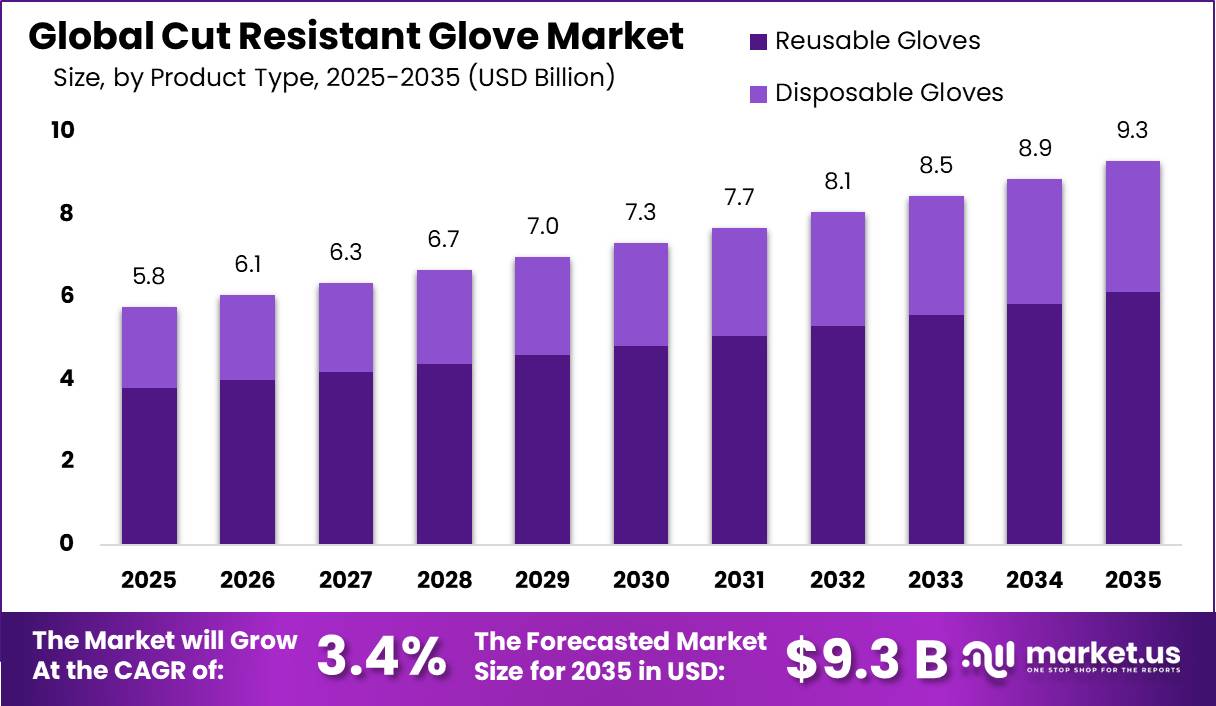

- On the basis of product types, reusable gloves dominated the market, constituting 65.8% of the total market share.

- Based on the material type, synthetic fibers cut resistant gloves dominated the market, with a substantial market share of around 35.7%.

- Among the cut resistance levels, ANSI level A1-A9 cut resistant gloves held a major share in the market, 35.4% of the market share.

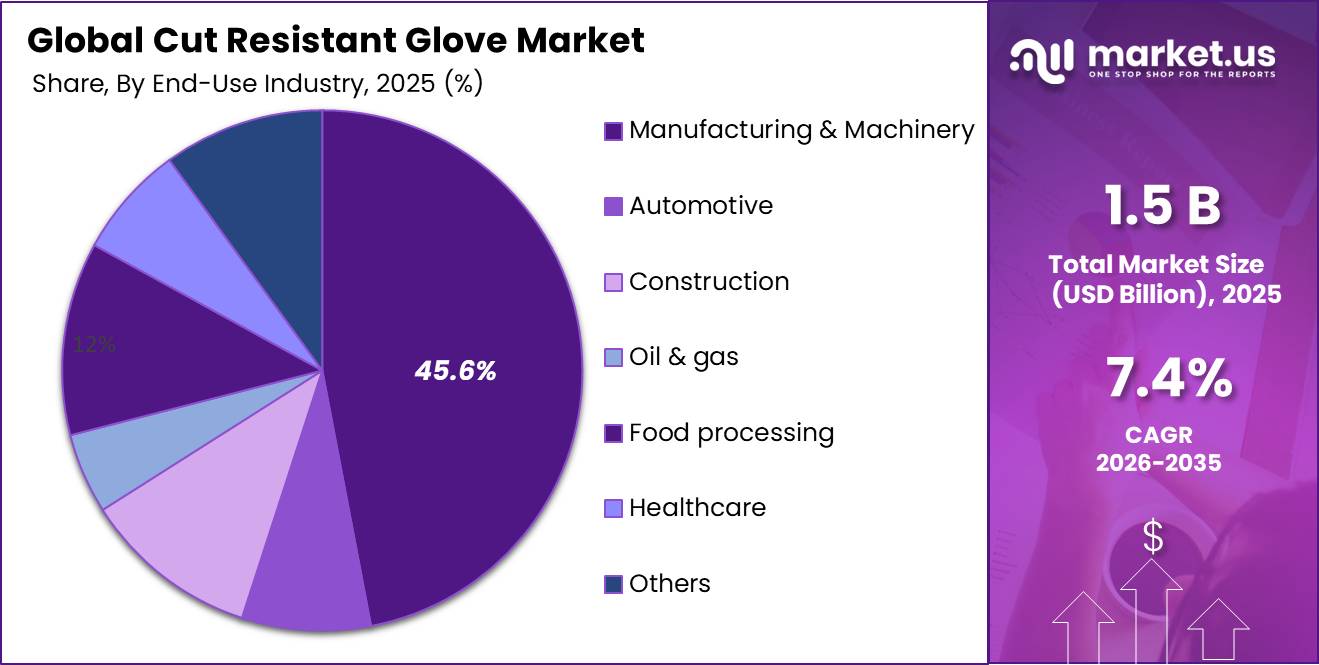

- Among the end-use industries, the manufacturing & machinery sector is the most considerable within the market, accounting for around 45.6% of the revenue.

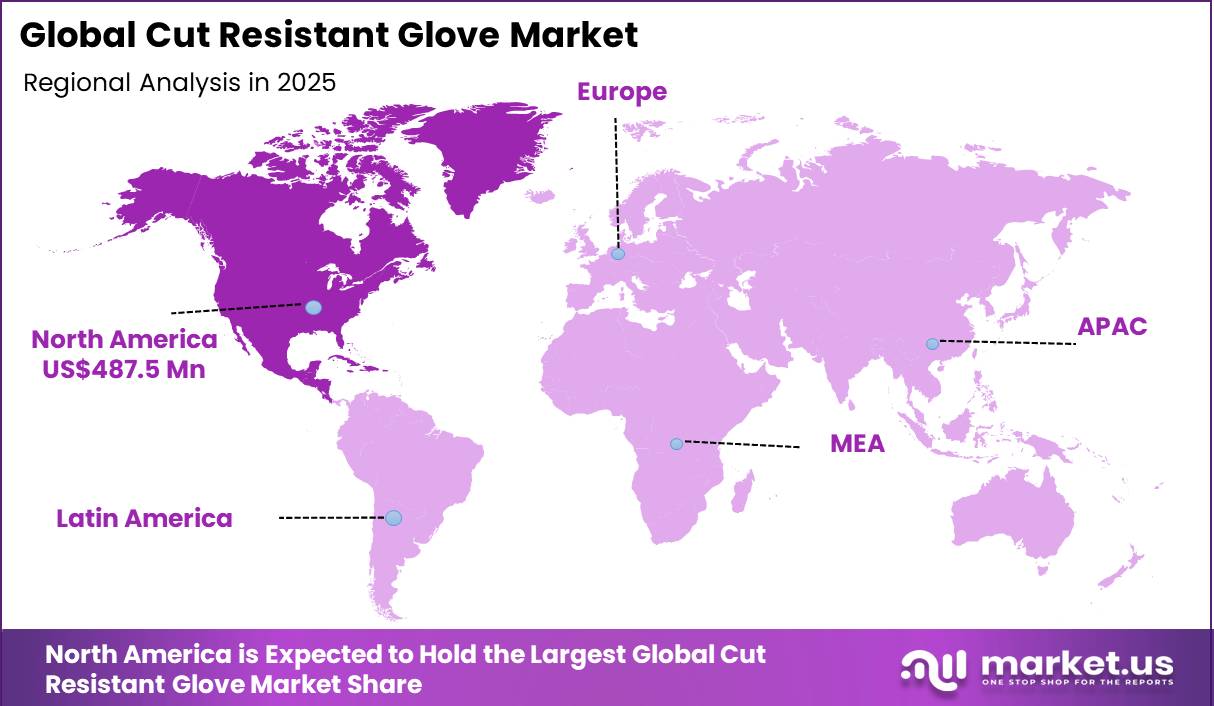

- In 2025, North America was the most dominant region in the cut resistant glove market, accounting for 32.5% of the total global consumption.

Product Type Analysis

Reusable Gloves are a Prominent Segment in the Market.

Reusable gloves dominate the cut-resistant gloves market, accounting for 65.8% share, driven by their extended service life and suitability for continuous industrial use. Their widespread adoption is closely linked to applications in manufacturing, automotive assembly, construction, and metal fabrication, where workers are exposed to repetitive handling of sharp components and require sustained hand protection. Unlike single-use alternatives, reusable variants offer cost efficiency over multiple cycles of use, making them more viable for large-scale industrial procurement strategies.

These gloves are commonly engineered using advanced materials such as aramid fibers and high-performance polyethylene, enabling compliance with safety requirements under standards such as EN 388 and ANSI/ISEA 105. Enhanced coatings, including nitrile and polyurethane, further improve abrasion resistance and grip performance, extending functional lifespan in both dry and oil-exposed environments. The segment further benefits from increasing emphasis on waste reduction and sustainable industrial practices, which favor durable, multi-use protective equipment over disposable alternatives in long-term occupational safety frameworks.

Material Type Analysis

Synthetic Fibers Cut Resistant Gloves Dominated the Market.

Synthetic fibers represent the dominant material segment in the cut-resistant gloves market, accounting for 35.7% share. Their strong positioning is primarily driven by a balanced combination of high cut resistance, lightweight construction, and flexibility, making them suitable for a broad range of industrial applications. These fibers, including high-performance polyethylene (HPPE) and engineered blends, are widely adopted in manufacturing, automotive assembly, logistics, and metal handling environments where dexterity and continuous wear comfort are essential.

Compared to traditional materials such as leather or metal mesh, synthetic fibers offer improved ergonomics while maintaining compliance with safety benchmarks such as EN 388 and ANSI/ISEA 105. Their adaptability to coating technologies such as nitrile and polyurethane further enhances grip performance and abrasion resistance. Additionally, scalability in production and compatibility with automated knitting processes support consistent quality output, reinforcing their widespread adoption across high-volume industrial PPE applications.

Cut Resistance Level Analysis

ANSI Level A1–A9 Cut Resistant Gloves Held a Major Share of the Market.

ANSI Level A1–A9 represents the dominant cut resistance classification segment, accounting for 35.4% share, reflecting its strong adoption across North American industrial procurement systems. The segmentation framework under ANSI/ISEA 105 provides a detailed performance scale that enables end users to match glove protection levels with specific hazard intensities, ranging from light-duty material handling (A1–A2) to high-risk cutting applications (A7–A9).

Its widespread usage is supported by its clear numerical grading system, which simplifies compliance verification and product selection across manufacturing, automotive, construction, and logistics sectors. Industrial buyers prefer this classification due to its compatibility with internal safety audits and regulatory inspections, particularly in the United States. Additionally, the structure of the ANSI system allows easier integration into procurement specifications compared to other frameworks such as EN 388 or ISO 13997, reinforcing its role as a preferred benchmark for standardized cut resistance assessment in industrial PPE selection processes.

End Use Industry Analysis

Cut Resistant Gloves Are Mostly Utilized in the Manufacturing & Machinery Sector.

Manufacturing & machinery is the dominant end-use industry segment, accounting for 45.6% share, reflecting its high exposure to sharp-edge handling, automated equipment, and repetitive industrial processing activities. This segment includes metal fabrication, machine assembly, and precision engineering operations where workers are frequently at risk of cuts and lacerations from raw materials and mechanical components.

High adoption of cut-resistant gloves in this sector is strongly influenced by compliance requirements under safety frameworks such as ANSI/ISEA 105 and EN 388, which guide procurement of task-appropriate protective equipment. The sector’s reliance on continuous production cycles necessitates durable and reusable glove solutions that balance protection with dexterity for machine operation and material handling. Additionally, increasing automation and human-machine interaction in modern factories has further reinforced the need for advanced hand protection solutions tailored to varying operational risk levels within manufacturing environments.

Key Market Segments

By Product Type

- Reusable Gloves

- Disposable Gloves

By Material Type

- Synthetic Fibers

- Aramid Fibers

- Metal Mesh

- Leather

- Others

By Cut Resistance Level

- ANSI Level A1-A9

- EN 388 Level 1-6

- ISO 13997 Level A-F

- ASTM standards

By End-Use Industry

- Automotive

- Manufacturing & Machinery

- Construction

- Oil & gas

- Food processing

- Healthcare

- Others

Drivers

Rising Enforcement of Workplace Safety Regulations Drives the Cut Resistant Glove Market.

Rising enforcement of occupational safety frameworks has materially strengthened compliance-driven adoption of cut-resistant gloves across high-risk industries. In the United States, the Occupational Safety and Health Administration (OSHA) requires employers to provide appropriate personal protective equipment when engineering and administrative controls cannot eliminate hazards, explicitly covering risks such as cuts, lacerations, and amputations under hand protection rules in 29 CFR standards. OSHA inspection data indicate that PPE-related violations are consistently recorded during workplace audits, reflecting gaps in adequate protective equipment deployment across facilities.

In parallel, injury surveillance data from U.S. labor statistics show that upper-extremity injuries remain among the most frequent nonfatal workplace incidents, with over 124,000 hand injuries reported in a single year in private industry, reinforcing the regulatory focus on preventive protection measures. A significant proportion of these injuries is linked to cuts and punctures, particularly in manufacturing environments handling sharp-edged materials.

European regulatory alignment under EN 388 and global cut-resistance classification systems such as ANSI/ISEA 105 have further standardized minimum performance expectations for protective gloves, making compliance a procurement requirement rather than an optional practice. These structured enforcement mechanisms collectively reduce tolerance for non-certified hand protection in audited environments, accelerating substitution toward certified cut-resistant glove solutions across industrial operations.

Restraints

Cost Sensitivity in Price-Competitive Markets Poses Challenges to the Cut Resistant Glove Market.

High cost pressure remains a structural constraint in the adoption of cut-resistant gloves, particularly in price-sensitive manufacturing ecosystems dominated by small and medium enterprises. The wide pricing spread often results in procurement decisions being driven by upfront expenditure rather than hazard severity, especially in outsourced production environments where safety budgets are tightly controlled.

The occupational safety assessments indicate that in several developing economies, a significant proportion of industrial workers still rely on substandard or non-certified protective gloves due to affordability constraints. This cost-driven substitution is reinforced by volatile raw material inputs such as aramid fibers and high-performance polyethylene, which directly influence production pricing structures and limit manufacturers’ ability to stabilize end-user costs.

Regulatory frameworks such as OSHA PPE compliance guidelines require hazard-appropriate hand protection, yet enforcement outcomes show recurring PPE-related violations during inspections, indicating persistent gaps between mandated safety provisioning and actual purchasing behavior. Consequently, the tension between compliance requirements and procurement affordability continues to moderate penetration rates of premium cut-resistant glove solutions, particularly in fragmented and highly competitive industrial markets.

Opportunity

Expansion in Emerging Industrial Economies Creates Opportunities in the Cut Resistant Glove Market.

Expansion of industrial activity across emerging economies is increasingly aligned with the formalization of occupational safety systems, directly influencing demand for hand protection solutions such as cut-resistant gloves. In India, the Ministry of Labour and Employment’s implementation of the Occupational Safety, Health and Working Conditions Code, 2020, consolidated earlier fragmented regulations into a unified compliance framework covering factories employing 20 or more workers, strengthening PPE adoption requirements in manufacturing units and construction sites. Similarly, regulatory tightening is observable in Southeast Asia, where government labor departments have expanded inspection coverage in export-oriented manufacturing clusters, particularly in electronics and automotive supply chains.

The U.S. Bureau of Labor Statistics reports over 110,000 annual lost-workday cases linked to hand injuries in industrial settings, with cuts and lacerations forming a significant proportion of incidents, a pattern that mirrors risks identified in developing manufacturing hubs transitioning toward mechanized production environments. As production scales in sectors such as metal fabrication, machinery assembly, and construction, exposure to sharp-edge handling increases proportionally.

Manufacturing expansion data further reflects structural momentum, with Asia-Pacific projected to record the fastest regional growth in protective glove adoption due to accelerating industrialization and infrastructure development across China, India, and Southeast Asia. Government-backed industrial corridors and export processing zones further institutionalize safety compliance, embedding certified protective equipment within procurement norms. Increasing integration of global supply chains amplifies adherence to international safety standards, reinforcing systematic uptake of high-performance cut-resistant gloves across newly industrializing economies.

Trends

Shift Toward High-Performance and Task-Specific Designs.

The increasing shift toward task-specific and high-performance glove designs reflects the tightening alignment between industrial hazard profiles and PPE engineering rather than reliance on generalized protection categories. Modern production environments, such as automotive stamping, sheet metal handling, and glass processing, are now differentiated by highly variable cut risks, prompting the adoption of application-calibrated glove specifications instead of uniform protection solutions.

For instance, gloves certified under ANSI/ISEA 105 and EN 388 are increasingly selected at higher cut levels (A3-A7 or equivalent Level D-F) specifically for metal fabrication and sharp-edge handling, while lower cut classes are maintained for precision assembly tasks where dexterity is critical. High-performance polyethylene (HPPE), para-aramid fibers, and composite yarn blends are being deployed in targeted configurations to balance protection and ergonomics across distinct job functions.

Industrial safety assessments indicate that medium cut resistance categories (ANSI A3-A4) still dominate general usage, but demand is progressively concentrating in higher cut tiers (A5 and above) in metal-intensive sectors where injury severity risk is elevated. This evolution is reinforced by the integration of composite yarn technologies and seamless knitting methods, which allow manufacturers to engineer zone-specific protection within a single glove structure, improving both compliance and task efficiency.

Geopolitical Impact Analysis

Geopolitical Supply Disruptions and Value Chain Volatility in Cut-Resistant Protective Equipment Markets.

Geopolitical tensions have increasingly reshaped cost structures and supply continuity in the cut-resistant gloves segment through their transmission effects on petrochemical feedstocks, logistics corridors, and trade policy measures. Cut-resistant gloves rely heavily on petrochemical-derived inputs such as nitrile, polyethylene, and polypropylene-based fibers, making them sensitive to upstream oil and gas disruptions. Recent disruptions in Middle Eastern supply routes have tightened the availability of key petrochemical intermediates, with global PPE supply chains reporting constrained flow and elevated input costs for polymer-based materials used in glove manufacturing.

Export restrictions and trade fragmentation have further amplified supply uncertainty. The export controls by major producing economies can accelerate shortage transmission across importing countries, particularly when production is concentrated among a limited set of suppliers. This dynamic has been reinforced in recent years as manufacturing hubs in Asia face intermittent logistics bottlenecks and rerouting of shipping lanes, increasing lead times for raw material procurement.

Price transmission effects are further evident across synthetic rubber and polymer value chains. Petrochemical volatility driven by geopolitical shocks can generate double-digit fluctuations in input costs, with oil-linked raw materials such as nitrile and polypropylene experiencing rapid cost escalation that directly feeds into glove production economics. In recent supply stress episodes, downstream glove pricing has reflected significant increases as manufacturers pass through elevated feedstock and energy costs, particularly in export-dependent production clusters.

Regional Analysis

North America Held the Largest Share of the Global Cut Resistant Glove Market.

In 2025, North America dominated the global cut resistant glove market, holding about 32.5% of the total global consumption, supported by deep industrial diversification and stringent occupational safety enforcement. Regulatory frameworks play a central role in shaping adoption patterns. The Occupational Safety and Health Administration (OSHA) mandates employers to provide appropriate hand protection where hazards such as sharp objects, lacerations, and punctures are present under 29 CFR PPE requirements. Over 70% of hand and arm injuries are considered preventable through proper PPE usage, reinforcing compliance-driven procurement behavior.

Standardization frameworks such as ANSI/ISEA 105 and adoption of international benchmarks such as EN 388 further reinforce product specification consistency, enabling widespread integration of certified cut-resistant gloves across industrial procurement systems. This combination of regulatory enforcement, high injury incidence, and mature industrial infrastructure sustains North America’s position as the most structurally developed regional market for cut-resistant protective handwear.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of cut-resistant gloves concentrate on strengthening material innovation and product differentiation to improve competitive positioning. A key focus is the development of advanced fiber blends such as high-performance polyethylene, aramid, and hybrid composites that enhance cut resistance while maintaining dexterity and comfort. Firms further invest in coating technologies to improve grip performance across dry, wet, and oily industrial conditions. Compliance with global safety benchmarks such as ANSI/ISEA 105 and EN 388 is prioritized to meet procurement requirements in regulated industries.

In parallel, manufacturers expand task-specific product lines tailored to automotive, construction, and metal fabrication applications, enabling closer alignment with end-use risk profiles. Strategic partnerships with industrial distributors and OEM suppliers strengthen market penetration, while investments in automated knitting and seamless manufacturing improve cost efficiency and product consistency. Sustainability initiatives, including recyclable materials and reduced-waste production processes, are increasingly integrated to align with corporate procurement standards and regulatory expectations.

The Major Players in The Industry

- Ansell Limited

- Honeywell International Inc.

- 3M Company

- Kimberly-Clark Corporation

- Top Glove Corporation Berhad

- Hartalega Holdings Berhad

- Kossan Rubber Industries Bhd

- Supermax Corporation Berhad

- Superior Glove Works Ltd.

- Protective Industrial Products Inc.

- TOWA Corporation

- Wells Lamont Industrial LLC

- SHOWA Group

- Uvex Group

- Delta Plus Group

- Other Key Players

Key Developments

- In April 2026, Ansell Limited launched the HyFlex Sustainable Cut Resistance Series, a range of industrial gloves offering advanced cut protection while promoting lower environmental impact.

- In March 2024, Protective Industrial Products (PIP) launched the ATG MaxiCut Ultra Gloves, an addition to its PPE portfolio. The gloves offer enhanced cut-resistant hand protection, reinforcing the company’s position in industrial safety solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Bn |

| Forecast Revenue (2035) | USD 3.1 Bn |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Machine Type (CO₂ laser cutting machines, Fiber laser cutting machines, and Diode laser cutting machines), By Laser Power (Low, Medium, and High), By Fabric Type (Natural and Synthetic), By Operation Mode (Manual, Semi-automatic, and Fully automatic), By End-Use Industry (Textile, Automotive, Aerospace, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Ansell Limited, Honeywell International Inc., 3M Company, Kimberly-Clark Corporation, Top Glove Corporation Berhad, Hartalega Holdings Berhad, Kossan Rubber Industries Bhd, Supermax Corporation Berhad, Superior Glove Works Ltd., Protective Industrial Products Inc., TOWA Corporation, Wells Lamont Industrial LLC, SHOWA Group, Uvex Group, Delta Plus Group, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |