Quick Navigation

- Report Overview

- Key Takeaways

- By Matrix Type Analysis

- By Reinforcement Type Analysis

- By Production Technology Analysis

- By Reinforcement Material Analysis

- By End-Use Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Opportunity

- Regional Insights

- Key Players Analysis

- Recent Industry Developments

- Report Scope

Report Overview

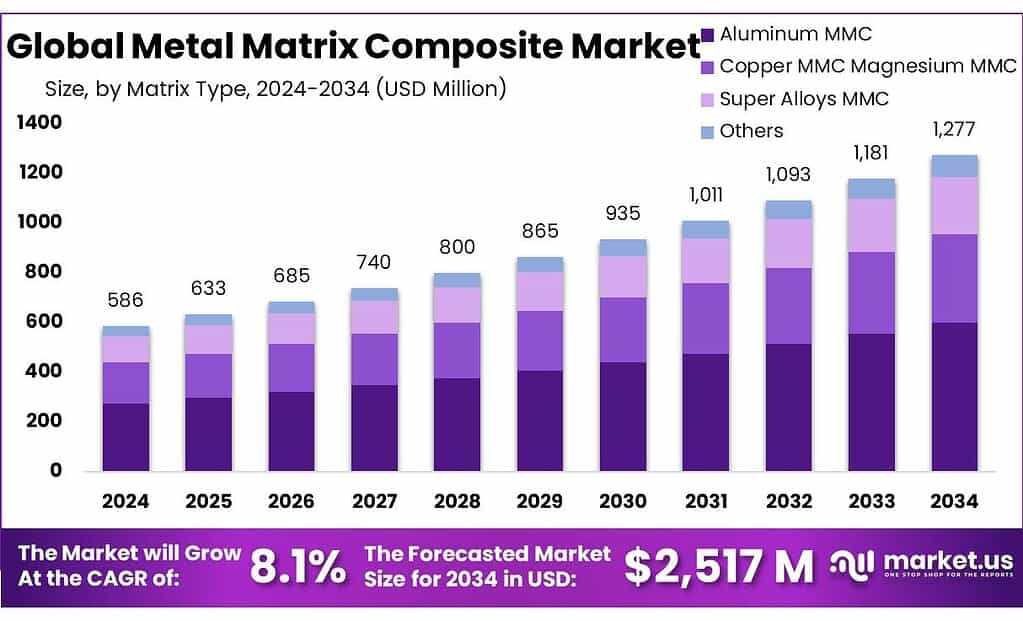

Global Metal Matrix Composite Market size is expected to be worth around USD 1277 Million by 2034, from USD 586 Million in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034. In 2024 Europe held a dominant market position, capturing more than a 39.5% share, holding USD 57.6 Million in revenue.

Metal matrix composites (MMCs) are engineered materials where a metal such as aluminium, magnesium, titanium, or copper is reinforced with ceramics to achieve a performance mix that monolithic metals struggle to deliver. In industrial terms, MMCs sit between conventional alloys and advanced composites: they keep a metal’s machinability and thermal conductivity while adding higher stiffness, improved wear resistance, better high-temperature strength, and tighter dimensional stability.

The current industrial scenario is shaped by two realities: end-use demand is rising, and metal supply chains are under pressure. Primary aluminium output remains massive, reaching 6,296 thousand metric tonnes in December 2025 alone, which underscores how aluminium-based MMCs can scale when cost and processing are optimized.

At the same time, U.S. domestic primary aluminium production was 54,600 metric tons in September 2024, highlighting the continued importance of regional refining capacity for downstream specialty materials. On the demand side, aerospace build rates matter because MMCs are frequently qualified for high-value platforms; Airbus delivered 766 commercial aircraft in 2024 and reported a backlog of 8,658 aircraft—an installed base and pipeline that sustains long qualification cycles for advanced materials.

Key driving factors are anchored in efficiency, electrification, and extreme-environment performance. Lightweighting remains a direct economic lever: the U.S. Department of Energy notes that a 10% vehicle weight reduction can improve fuel economy by about 6%–8%, which is a practical justification for MMC use in rotating, sliding, or thermally loaded parts where thinner sections still must resist wear.

Electrification adds a second pull: global electric car sales topped 17 million in 2024, with China exceeding 11 million sales—creating a large addressable need for thermal management, structural housings, and wear-resistant drivetrain parts where MMCs can outperform standard aluminium alloys. Defense and space applications also support MMC adoption because they reward high-temperature and high-stiffness materials; for instance, U.S. hypersonic R&D budget requests were $6.9 billion for FY2025 and $3.9 billion for FY2026, sustaining materials work on heat, erosion, and structural survivability.

In Europe, the Clean Aviation Joint Undertaking is positioned as a major technology push with a total budget of €4.1 billion, split into €1.7 billion EU funding and no less than €2.4 billion private funding—supporting lighter airframes, higher-efficiency propulsion architectures, and next-generation thermal solutions where MMCs can be engineered into certified structures over time. In the U.S., the DOE’s Advanced Materials and Manufacturing Technologies Office announced $16,926,260 in selections under a 2024 Critical Materials Accelerator, reinforcing the trend toward scale-up funding that can de-risk MMC processing routes.

Key Takeaways

- Metal Matrix Composite Market size is expected to be worth around USD 1277 Million by 2034, from USD 586 Million in 2024, growing at a CAGR of 8.1%.

- Aluminum MMC held a dominant market position, capturing more than a 47.7% share.

- Discontinuous held a dominant market position, capturing more than a 58.2% share.

- Powder Metallurgy held a dominant market position, capturing more than a 48.5% share.

- Silicon Carbide held a dominant market position, capturing more than a 53.6% share.

- Non-residential held a dominant market position, capturing more than a 59.9% share.

- North America held the leading position in the metal matrix composite (MMC) market, accounting for 39.4% and reaching USD 230.8 Mn.

By Matrix Type Analysis

Aluminum MMC leads the Metal Matrix Composite Market with a commanding 47.7% share in 2024

In 2024, Aluminum MMC held a dominant market position, capturing more than a 47.7% share, driven by its lightweight structure, strong thermal conductivity, and wide industrial suitability. The segment benefited from rising demand across automotive, electronics, aerospace, and defense applications, where companies increasingly prefer materials that reduce weight without compromising strength. In many high-performance parts—such as brake components, engine housings, heat sinks, and structural panels—aluminum MMCs offer a balance of stiffness and durability that conventional alloys cannot match. Manufacturers across North America, Europe, and Asia continued expanding production volumes, supported by rapid growth in EV component manufacturing and modern lightweighting programs.

By Reinforcement Type Analysis

Discontinuous Reinforcement leads the Metal Matrix Composite Market with a strong 58.2% share in 2024

In 2024, Discontinuous held a dominant market position, capturing more than a 58.2% share, supported by its versatility, cost-efficiency, and suitability for mass-production environments. Discontinuous reinforcements—such as particulates, whiskers, and short fibers—allowed manufacturers to produce components with enhanced stiffness, wear resistance, and thermal stability without the high processing complexities associated with continuous fibers. Industries such as automotive, industrial machinery, and consumer electronics increasingly adopted discontinuous MMCs because they blend mechanical performance with smoother machining, consistent dispersion, and lower overall production costs. This made the segment particularly attractive for brake pads, pistons, cylinder liners, gears, housings, and thermal management structures that needed uniform material behavior.

By Production Technology Analysis

Powder Metallurgy leads the Metal Matrix Composite Market with a solid 48.5% share in 2024

In 2024, Powder Metallurgy held a dominant market position, capturing more than a 48.5% share, mainly because it allows precise control over reinforcement distribution and delivers components with excellent dimensional accuracy. Industries preferred this production route for its ability to create high-performance MMC parts with uniform properties, minimal defects, and strong bonding between metal matrices and reinforcements. Powder metallurgy also enabled the manufacturing of complex shapes with reduced material waste, making it especially suitable for automotive engine parts, aerospace components, industrial tools, and thermal management structures. As manufacturers pushed for lighter and more durable materials, powder-based processing became the most reliable and scalable method for producing MMCs at commercial volumes.

By Reinforcement Material Analysis

Silicon Carbide leads the Metal Matrix Composite Market with a strong 53.6% share in 2024

In 2024, Silicon Carbide held a dominant market position, capturing more than a 53.6% share, supported by its exceptional hardness, high thermal conductivity, and impressive wear-resistant behavior. Manufacturers favored silicon carbide reinforcement because it provides a significant improvement in stiffness and dimensional stability, especially in high-load and high-temperature environments.

Automotive, aerospace, and industrial machinery sectors used SiC-reinforced MMCs for brake rotors, pistons, engine components, heat sinks, and structural parts where durability and thermal performance are essential. The material’s ability to enhance strength without adding excess weight made it a preferred choice across multiple industries pursuing lightweight design strategies in 2024.

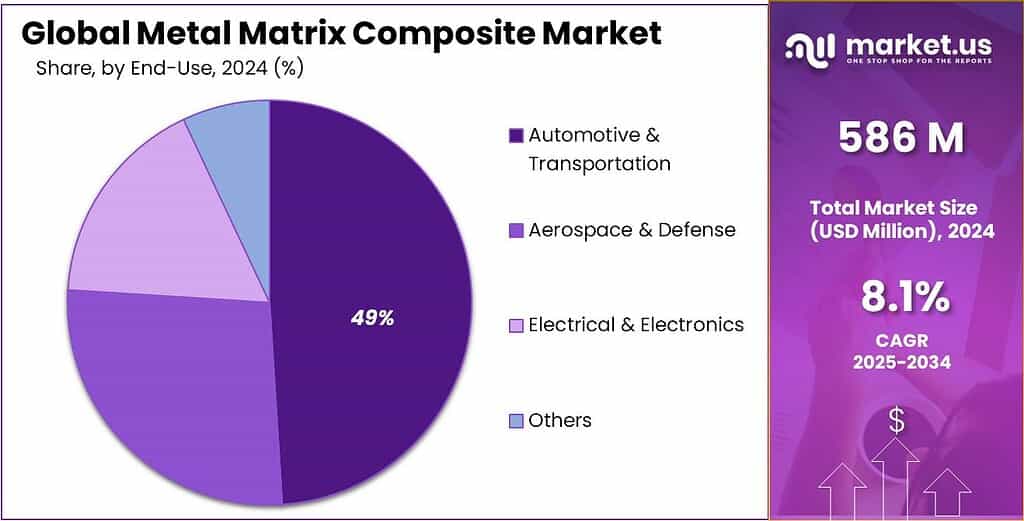

By End-Use Analysis

Non-residential end-use leads the Metal Matrix Composite Market with a strong 59.9% share in 2024

In 2024, Non-residential held a dominant market position, capturing more than a 59.9% share, supported by rising demand from industrial facilities, transportation infrastructure, aerospace operations, defense establishments, and large-scale manufacturing units. Metal matrix composites gained traction across these sectors because they provide high strength, strong thermal stability, and longer service life—qualities that traditional metals often struggle to deliver in heavy-duty environments. Industries used MMCs for structural components, high-performance tools, mechanical housings, powertrain parts, and thermal management systems, helping them improve efficiency and reduce downtime. The non-residential market also benefited from major investments in high-performance materials across factories, transportation hubs, and energy systems, reinforcing its dominance in 2024.

Key Market Segments

By Matrix Type

- Aluminum MMC

- Copper MMC Magnesium MMC

- Super Alloys MMC

- Others

By Reinforcement Type

- Continuous

- Discontinuous

- Particles

By Production Technology

- Liquid Metal Infiltration

- Powder Metallurgy

- Casting

- Deposition Techniques

By Reinforcement Material

- Alumina

- Silicon Carbide

- Carbon Fiber

- Others

By End-Use

- Automotive & Transportation

- Aerospace & Defense

- Electrical & Electronics

- Others

Emerging Trends

MMCs are increasingly being positioned as “circularity enablers” for high-speed beverage and food packaging equipment

One clear latest trend in the Metal Matrix Composite (MMC) space is that buyers are linking material choice to circular packaging goals, especially in food and beverage operations that run high-speed, high-wear lines. In 2024, large beverage brands sharpened their recycled-content and collection targets, which indirectly pushes plants to upgrade tooling and wear parts. For example, The Coca-Cola Company updated its goals in December 2024, targeting 35% to 40% recycled material in primary packaging and aiming to help ensure collection of 70% to 75% of the equivalent number of bottles and cans introduced each year.

In 2025, the same circularity push is showing up as a practical “reliability trend” in can-making and filling environments: plants want longer maintenance intervals while they scale up aluminum circularity. Ball Corporation notes the U.S. currently recycles 38% of aluminum cans, and it highlights the upside of moving that rate toward 90%.

A parallel policy trend reinforces this shift. The European Commission states that all packaging must be recyclable by 2030, pushing brand owners and converters to redesign packaging and modernize processes. Energy numbers make this trend even more urgent: the International Aluminium Institute reports primary energy demand of 186 gigajoules per tonne for global primary aluminium versus 8.3 gigajoules per tonne for recycled aluminium—an energy saving of 95.5%. As food and beverage supply chains chase these savings, the latest MMC trend is less about “new materials for the lab” and more about durable, production-ready MMC parts that keep high-speed circular packaging lines running with fewer stops.

Drivers

Lightweighting and energy-efficiency targets are pushing Metal Matrix Composite adoption

A major driving factor for Metal Matrix Composites (MMCs) is the global push to cut energy use while keeping performance high—especially in transport equipment where every kilogram matters. OEMs are under steady pressure to make vehicles and aircraft lighter without sacrificing stiffness, heat resistance, or durability. MMCs respond well to that need because they can deliver higher wear resistance and better thermal stability than standard alloys in demanding parts such as braking systems, housings, structural brackets, and heat-handling components.

In road transport, lightweighting is directly linked to fuel and energy savings. The U.S. Department of Energy explains that a 10% reduction in vehicle weight can improve fuel economy by about 6%–8%. That kind of relationship makes materials a board-level lever, not just an engineering detail. It also helps explain why MMCs are increasingly evaluated for parts where conventional aluminum or steel either wears too fast or distorts under heat. The same DOE material programs note that using lightweight components and high-efficiency engines enabled by advanced materials in one quarter of the U.S. fleet could save more than 5 billion gallons of fuel annually by 2030.

Electrification strengthens this driver further because electric platforms carry heavy batteries and must manage heat more aggressively. The International Energy Agency (IEA) reports that electric car sales exceeded 17 million globally in 2024, rising by more than 25% year over year. China alone recorded electric car sales of more than 11 million in 2024, which is a strong signal of how quickly powertrain and thermal management supply chains are expanding.

Aerospace adds a second, high-value pull. Large production backlogs and steady deliveries keep suppliers focused on weight reduction, reliability, and lifecycle cost. Airbus delivered 766 commercial aircraft in 2024 and reported a year-end backlog of 8,658 aircraft. This matters because aerospace qualification is slow and expensive; when build pipelines stay full, suppliers are more willing to invest in advanced materials that can reduce maintenance, extend component life, and improve thermal performance in critical zones. In practice, that supports continued evaluation and adoption of MMC solutions in selected structures and high-temperature or wear-prone parts.

Restraints

High production cost and recycling complexity restrain MMC scale-up despite strong performance demand

A major restraining factor for Metal Matrix Composites (MMCs) is that they are still expensive and difficult to scale cleanly, especially when buyers compare them with conventional aluminium alloys that are easier to cast, machine, and recycle. Many MMC routes (powder metallurgy, squeeze casting, infiltration) need tighter process control and higher-grade inputs, which raises scrap risk and per-part cost. This matters in real procurement decisions: even when an MMC part performs better, purchasing teams often choose a simpler alloy solution if it is “good enough” and easier to source in volume.

Energy and sustainability targets also create a practical barrier, because MMCs can complicate recycling streams. Primary metal production is power-hungry: one industry sustainability indicator reports electrical energy consumption of 14,863 kWh per metric ton of aluminium produced. In parallel, the International Aluminium Institute highlights how much the industry depends on recycling economics: global primary aluminium production consumed 186 gigajoules per tonne, while recycled aluminium required 8.3 gigajoules per tonne, delivering an energy saving of 95.5%.

Manufacturing friction adds another restraint: MMCs can be tougher on tools during machining. Research on MMC machining reports that abrasive hard particles can reduce tool life and increase cutting forces as reinforcement content rises, which pushes up cycle time and tooling spend. In 2025, this combination—higher process cost, recycling complexity, and tougher machinability—continued to limit MMC adoption mainly to parts where performance benefits clearly outweigh total cost.

Opportunity

Food and beverage packaging upgrades open a scalable opportunity for MMC wear-resistant, high-speed production parts

One major growth opportunity for Metal Matrix Composites (MMCs) is the fast modernization of food and beverage packaging systems, where brands are pushing harder on recycling, collection, and recycled-content goals. These targets are not just marketing lines—they force real changes in packaging formats and in the equipment used to form, fill, seal, and move containers at high speeds. The Coca-Cola Company updated its packaging goals in December 2024, aiming to use 35% to 40% recycled material in primary packaging (including aluminum) and to help ensure collection of 70% to 75% of the equivalent number of bottles and cans introduced annually.

In parallel, recycling performance is becoming a measurable KPI, and it creates a bigger installed base for aluminum formats. Ball Corporation points out that the U.S. currently recycles 38% of aluminum cans, and it highlights the upside if the rate moves toward 90%. Meanwhile, a global study cited by Packaging Dive reported the global aluminum can recycling rate reached about 75% in 2023. As more brands shift volume into cans and improve collection, canmakers and beverage plants must expand capacity while keeping uptime high. That is a practical opening for MMCs in high-wear machine parts, where even small reductions in maintenance stops can protect output and quality consistency.

Policy pressure adds another tailwind. The European Commission states that all packaging must be recyclable by 2030, pushing manufacturers toward designs and materials that can repeatedly run through recycling and sorting systems. This kind of rulemaking encourages equipment upgrades and process re-engineering, and it increases the value of materials that improve reliability in harsh, continuous operations—an environment where MMC parts can justify their higher upfront cost through longer operating cycles.

Regional Insights

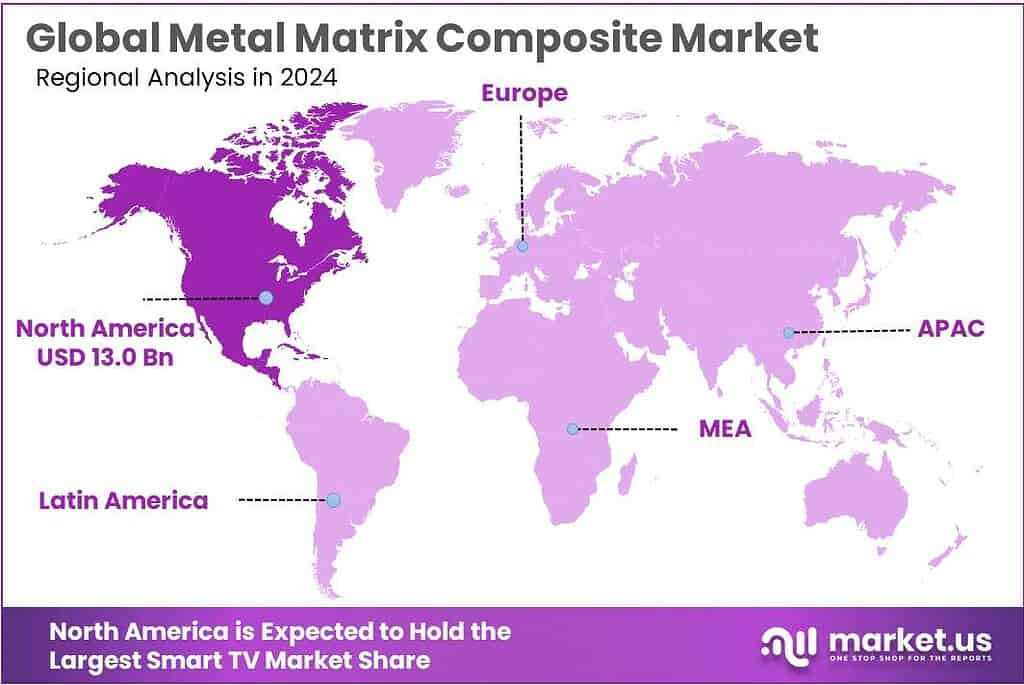

North America dominates the Metal Matrix Composite Market with a share of 39.4%, valued at USD 230.8 Mn in 2024

In 2024, North America held the leading position in the metal matrix composite (MMC) market, accounting for 39.4% and reaching USD 230.8 Mn. This lead is closely tied to the region’s strong demand for lightweight, wear-resistant materials in aerospace, mobility, industrial machinery, and high-performance manufacturing. MMC adoption is supported by a mature supplier base for aluminium and engineered materials, along with customers that are willing to pay for longer component life and tighter thermal stability in critical parts.

A key regional tailwind is electrification and the growth of advanced vehicle platforms. In the United States, electric car sales rose to 1.6 million in 2024, with EV share moving to “more than 10%” of car sales, reinforcing the need for improved thermal and wear performance in powertrain and heat-management components where MMCs can fit.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

CPS is a direct MMC specialist known for metal matrix and thermal management solutions. For full-year 2024, it reported revenue of about $21.12M, reflecting a smaller but focused MMC footprint. In Q4 2024, revenue was $5.9M, with results influenced by the timing of large defense-related contracts—common in advanced materials production cycles.

3M’s role in advanced manufacturing supports MMC ecosystems through adhesives, abrasives, and engineered solutions used in precision production. In 2024, 3M delivered $23.6B in (adjusted) sales and launched 169 new products, showing steady innovation and industrial throughput. This scale matters because MMC machining and finishing depend on high-performance abrasive and process technologies.

GKN is widely recognized in aerospace supply chains where lightweight, high-strength materials matter. Its owner, Melrose, guided 2025 revenue at £3,550–£3,700M, signaling sustained aerospace production and aftermarket pull that supports MMC adoption in wear and thermal-stress parts. Melrose also set a 2029 revenue target of about £5B, showing long runway for advanced material demand.

Top Key Players Outlook

- Materion Corporation

- GKN plc

- 3M

- CPS Technologies Corporation

- DWA Aluminum Composites USA, Inc.

- TISICS Ltd.

- Plansee Group

- Sandvik AB

- AMETEK Specialty Metal Products

- Thermal Transfer Composites LLC

Recent Industry Developments

In 2024, CPS reported revenue of $5.9 million in the fourth quarter, reflecting a sequencing of contracts and production activity, and secured government and commercial development awards, such as three Phase I SBIR contracts valued at ~$250,000 each, which are helping fund next-generation MMC solutions.

In 2024, 3M reported $24.6 billion in total sales, with $23.6 billion on an adjusted basis, reflecting modest organic growth of 1.2% as customers invested in performance materials across transportation and industrial applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 586 Mn |

| Forecast Revenue (2034) | USD 1277 Mn |

| CAGR (2025-2034) | 8.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Matrix Type (Aluminum MMC, Copper MMC Magnesium MMC, Super Alloys MMC, Others), By Reinforcement Type (Continuous, Discontinuous, Particles), By Production Technology (Liquid Metal Infiltration, Powder Metallurgy, Casting, Deposition Techniques, By Reinforcement Material, Alumina, Silicon Carbide, Carbon Fiber, Others), By End-Use (Automotive And Transportation, Aerospace And Defense, Electrical And Electronics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Materion Corporation, GKN plc, 3M, CPS Technologies Corporation, DWA Aluminum Composites USA, Inc., TISICS Ltd., Plansee Group, Sandvik AB, AMETEK Specialty Metal Products, Thermal Transfer Composites LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |