Quick Navigation

Report Overview

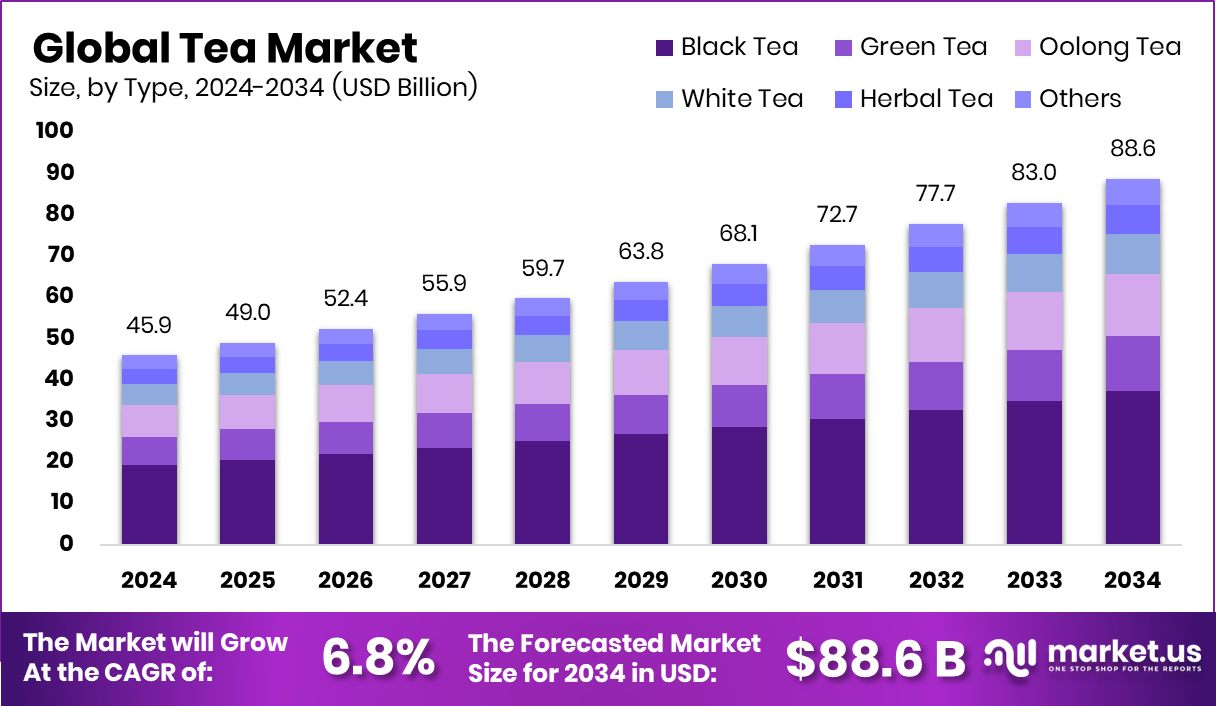

Global Tea Market is expected to be worth around USD 88.6 billion by 2034, up from USD 45.9 billion in 2024, and grow at a CAGR of 6.8% from 2025 to 2034. Rising consumption and cultural preference drive tea demand across Asia-Pacific 41.3%, holding market leadersh

Tea is a natural beverage made by steeping the processed leaves of the Camellia sinensis plant in hot water. It has been consumed for centuries for its calming properties, cultural value, and health benefits. Depending on how it’s processed, tea can be classified into green, black, oolong, white, or fermented varieties, each with its own flavor and antioxidant profile. It’s enjoyed both hot and cold, often with regional variations in preparation.

The tea market refers to the global industry focused on the cultivation, processing, packaging, distribution, and sale of tea in various forms. It includes loose-leaf tea, tea bags, instant tea, ready-to-drink products, and flavored blends. This market connects rural tea-growing regions with urban consumers across the world, bridging tradition and innovation through retail chains, cafés, and online platforms.

A major growth factor is increasing awareness about tea’s health benefits. More people are switching from sugary beverages to herbal tea and green teas due to their antioxidant and anti-inflammatory properties. This wellness shift is fueling demand in both developed and developing nations, especially among younger consumers looking for healthier lifestyle choices.

The Tea Development & Promotion Scheme has been launched with a total budget of ₹664.09 crore to support the overall growth of India’s tea industry. This scheme is designed to cover the entire value chain—from cultivation and processing to branding and marketing—ensuring a comprehensive “field to cup” approach.

A key focus of the scheme is the promotion of Indian teas, especially premium varieties like Darjeeling and other Geographical Indication (GI)-certified teas. For this, ₹72.42 crore has been specifically allocated to enhance the visibility of these teas in global markets through targeted export promotion activities. .

Key Takeaways

- Global Tea Market is expected to be worth around USD 88.6 billion by 2034, up from USD 45.9 billion in 2024, and grow at a CAGR of 6.8% from 2025 to 2034.

- In the Tea Market, Black Tea led the type segment with a strong 44.3% share.

- Tea Bags dominated the product form in the Tea Market, capturing a 43.3% share globally.

- The Tea Market saw 67.3% of sales coming from the Conventional category in 2024.

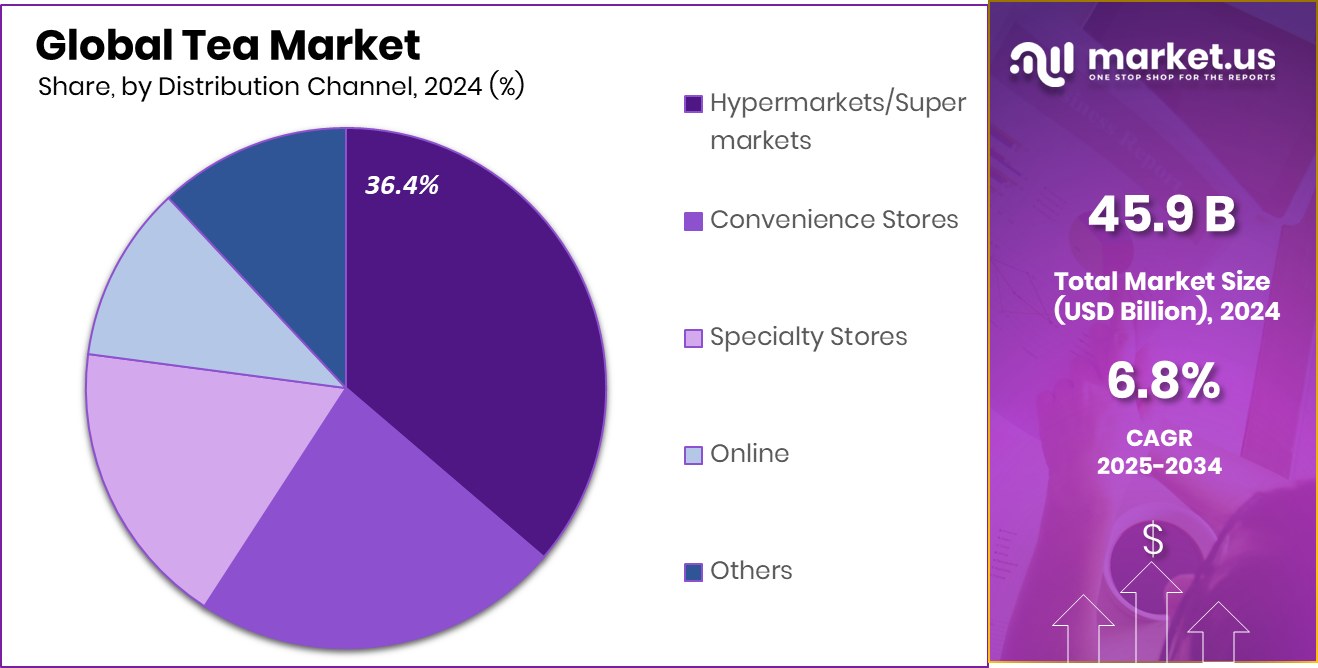

- Hypermarkets and Supermarkets held a 36.4% distribution share in the global Tea Market segment.

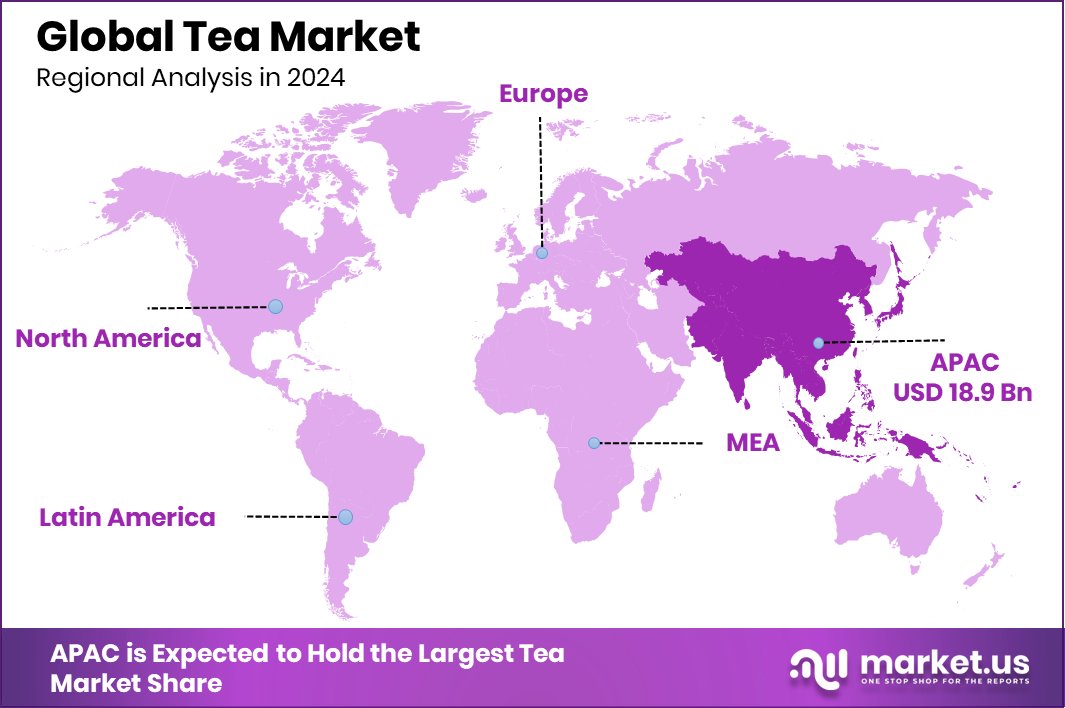

- The Asia-Pacific tea market reached a value of USD 18.9 Bn in 2024.

By Type Analysis

In Tea Market, Black Tea holds a 44.3% share, showing strong global consumer preference.

In 2024, Black Tea held a dominant market position in the By Type segment of the Tea Market, with a 44.3% share. This leadership can be attributed to its widespread global acceptance, bold flavor profile, and cultural integration in major tea-consuming countries. Black tea continues to be a staple in daily consumption patterns, especially in regions with traditional tea-drinking habits.

Its longer shelf life compared to green or herbal variants also contributes to its popularity in retail and export markets. Additionally, its use in blended and flavored formats, such as masala chai and iced teas, supports demand across both traditional and contemporary beverage formats.

Consumer loyalty towards black tea remains strong, particularly in regions where it is consumed as part of daily routines. Moreover, its cost-effectiveness and ease of preparation make it a preferred choice for households, foodservice chains, and institutional buyers.

Although other varieties like green and herbal teas are rising in popularity due to health trends, black tea continues to retain its dominance due to its rich taste, caffeine content, and pairing flexibility with milk or spices.

By Product Form Analysis

Tea Market sees Tea Bags dominate with a 43.3% share due to ease and convenience.

In 2024, Tea Bags held a dominant market position in the by-product form segment of the Tea Market, with a 43.3% share. This segment continues to lead due to its high convenience, portion control, and widespread availability across retail shelves. Tea bags offer a mess-free brewing experience, making them ideal for both home and office consumption. Their compact packaging also supports easy storage and transportation, increasing their appeal among urban consumers with fast-paced lifestyles.

The popularity of tea bags is further driven by their affordability and suitability for single-serve preparation. Consumers value the consistency in flavor and strength they offer, along with the reduced preparation time compared to loose-leaf variants. Innovations in biodegradable and eco-friendly tea bag materials are also helping brands address sustainability concerns without compromising user experience. The format is especially favored in developed markets where consumers prioritize convenience and hygiene.

Tea bags are also a preferred format for flavored and herbal blends, enabling companies to experiment with ingredients while maintaining quality and shelf stability. Their dominance reflects a balanced mix of tradition and innovation, making them a reliable choice across both mass-market and premium tea categories. This consistent demand secures their leadership in the product form segment.

By Category Analysis

Conventional tea leads the Tea Market category with a 67.3% share, reflecting traditional buying habits.

In 2024, Conventional held a dominant market position in the By Category segment of the Tea Market, with a 43.3% share. This segment continues to outperform due to its widespread availability, lower pricing, and strong consumer familiarity.

Conventional tea is deeply embedded in the daily routines of consumers across regions, particularly in price-sensitive markets where affordability plays a crucial role in purchasing decisions. Its broad distribution across supermarkets, local retailers, and food service outlets also supports higher volume sales.

The consistent taste profile and long-standing consumer trust in conventional tea products further boost their dominance. Unlike organic tea, which often comes at a premium, conventional tea offers budget-friendly options for everyday consumption. It is commonly available in bulk formats, tea bags, and ready-to-drink variants, catering to a wide demographic base.

Additionally, the conventional segment benefits from economies of scale in both production and distribution, allowing for greater market penetration. Although demand for organic and specialty teas is rising, particularly in urban and health-conscious consumer groups, conventional tea maintains a firm hold in the mainstream market.

By Distribution Channel Analysis

Hypermarkets/Supermarkets drive the Tea Market distribution, capturing a 36.4% share through mass retail availability.

In 2024, Hypermarkets/Supermarkets held a dominant market position in the By Distribution Channel segment of the Tea Market, with a 36.4% share. This dominance is driven by the widespread accessibility, organized retail infrastructure, and extensive shelf space available in these outlets. Consumers prefer purchasing tea from hypermarkets and supermarkets due to the ability to compare various brands, packaging formats, and pricing in a single visit.

The segment benefits from strong consumer footfall, especially in urban and semi-urban areas where weekly or monthly grocery shopping is common. Hypermarkets and supermarkets ensure greater product visibility and also serve as prime locations for promotional campaigns and in-store tastings, which help influence buying decisions. Additionally, their partnerships with both domestic and international tea brands allow them to maintain a wide and diverse product range.

This retail format also supports impulse purchases and introduces consumers to newer product lines like flavored, herbal, or ready-to-drink teas. While online and convenience store sales are growing, the structured layout, direct product experience, and price transparency in supermarkets continue to make them the most preferred channel in the tea market’s distribution segment.

Key Market Segments

By Type

- Black Tea

- Green Tea

- Oolong Tea

- White Tea

- Herbal Tea

- Others

By Product Form

- Loose Tea

- Tea Bags

- Instant Tea

- Compressed Tea

By Category

- Conventional

- VSS compliant

- Potentially VSS Compliant

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Others

Driving Factors

Health Awareness is Boosting Global Tea Demand

A major driving factor in the tea market is rising health awareness. People are becoming more mindful of what they consume and are switching from sugary drinks to healthier options like green, herbal tea and black tea.

Tea is known for its antioxidants, anti-inflammatory compounds, and natural calming effects, which attract health-conscious consumers. Many choose tea to support digestion, weight loss, and stress relief.

With increasing lifestyle diseases and focus on wellness, tea fits into daily routines without being too expensive. This shift is strong in both developed and developing countries, as tea is widely available and offers a natural health boost. The demand for low-calorie, plant-based beverages is helping tea grow fast.

Restraining Factors

Fluctuating Climate Conditions Impact Tea Production

One major challenge in the tea market is unstable weather patterns. Tea plants are very sensitive to climate, needing specific rainfall and temperatures to grow well. But with increasing droughts, floods, and unpredictable seasons, tea plantations are facing serious risks.

When growing conditions are poor, the quality and quantity of tea leaves drop, which raises costs for producers. Some regions even report declining yields year after year.

This directly affects supply chains and can lead to higher prices for consumers. Farmers may also face income losses, making it harder for them to sustain production. As climate change worsens, the tea market will need to find solutions to protect crops and maintain a consistent supply.

Growth Opportunity

Rising Demand for Organic and Premium Teas

A key growth opportunity in the tea market is the rising demand for organic and premium-quality teas. More consumers now prefer clean-label and chemical-free products that are ethically sourced and environmentally friendly.

Organic teas, free from pesticides and artificial flavors, are gaining popularity among health-conscious buyers. Premium blends, including handpicked leaves, rare herbs, or exotic infusions, also appeal to tea lovers willing to pay extra for better taste and quality.

This shift is especially strong in urban areas, where people are open to trying new flavors and care about the origin of what they drink. Brands that focus on transparency, sustainability, and unique offerings can grow quickly in this high-value segment.

Latest Trends

Functional Teas Gain Popularity Among Consumers

In 2025, a notable trend in the tea market is the growing consumer interest in functional teas. These are teas enhanced with ingredients that offer specific health benefits, such as boosting immunity, aiding digestion, or promoting relaxation. The shift toward health and wellness has led consumers to seek beverages that not only taste good but also contribute to their overall well-being. Functional teas often incorporate herbs, vitamins, and natural compounds known for their therapeutic properties.

This trend reflects a broader movement towards preventive health measures and natural remedies. As awareness of the health benefits associated with certain tea ingredients grows, the demand for functional teas is expected to continue rising, offering opportunities for innovation in product development and marketing strategies.

Regional Analysis

Asia-Pacific led the tea market in 2024 with a 41.3% share dominance.

In 2024, Asia-Pacific dominated the global tea market, accounting for 41.3% of the total share, with a market valuation of USD 18.9 billion. This stronghold is attributed to the region’s deep-rooted tea culture, especially in countries like China, India, and Japan, where daily consumption is significantly high. The region benefits from both strong domestic demand and large-scale production capacities.

In contrast, Europe holds a substantial share due to the rising preference for specialty and herbal teas among health-conscious consumers. North America is witnessing steady growth, driven by the increasing demand for organic and ready-to-drink (RTD) tea products. The Middle East & Africa market is gradually expanding as tea becomes a staple beverage in countries like Egypt and the UAE, with consumption rising across various demographics.

Meanwhile, Latin America is showing moderate growth supported by the rising adoption of iced teas and flavored variants among younger consumers. Across all regions, evolving consumer preferences and innovation in flavors and packaging are reshaping retail strategies and boosting market penetration.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global tea market experienced significant growth driven by health-conscious consumers and a shift toward premium and organic products. Key players like Tata Consumer Products, Unilever PLC, and Associated British Foods plc (ABF) played pivotal roles in shaping market dynamics.

Tata Consumer Products leveraged its strong presence in emerging markets, particularly India, to expand its wellness-oriented portfolio. The introduction of products like Tata Tea Tulsi Green and Tata Tea Gold Care catered to the growing demand for health-centric beverages. Additionally, the reformulation of Tetley Green Tea with added Vitamin C highlighted Tata’s commitment to functional beverages. This strategic focus on health and wellness positioned Tata favorably in the competitive landscape.

Unilever PLC, through its extensive brand portfolio, including Lipton and Pukka Herbs, capitalized on the rising demand for organic and specialty teas. The company’s emphasis on sustainability and ethical sourcing resonated with environmentally conscious consumers. Unilever’s global reach and investment in digital marketing further strengthened its market position, allowing it to tap into diverse consumer segments.

Associated British Foods plc (ABF), owner of Twinings, maintained its premium brand image by focusing on high-quality blends and innovative flavors. ABF’s commitment to sustainability and ethical sourcing practices appealed to a growing segment of consumers valuing transparency and responsibility.

Top Key Players in the Market

- Tata Consumer Products

- Unilever PLC

- Associated British Foods plc

- Twinings

- Apeejay Surrendra Group

- Celestial Seasonings, Inc.

- Bettys & Taylors Group Ltd.

- The Republic of Tea

- Bigelow Tea Company

- Reily Foods Company

- Gujarat Tea Processors and Packers Limited

- Finlays

- Mcleod Russel

- Future Generation Co. Ltd

- Vinatea

- Other Key Players

Recent Developments

- In February 2024, Hain Celestial initiated the “Hain Reimagined” program, aiming to focus on five key areas: Snacks, Baby & Kids, Beverages, Meal Preparation, and Personal Care. This strategic initiative is designed to streamline operations and invest in growth opportunities across these categories.

- In January 2024, Tata Consumer Products signed agreements to acquire up to 100% of Organic India, a brand known for its organic teas and herbal supplements. This move aims to strengthen Tata’s presence in the health and wellness segment, leveraging Organic India’s strong farmer network and certified organic supply chain.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 45.9 Billion |

| Forecast Revenue (2034) | USD 88.6 Billion |

| CAGR (2025-2034) | 6.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Black Tea, Green Tea, Oolong Tea, White Tea, Herbal Tea, Others), By Product Form (Loose Tea, Tea Bags, Instant Tea, Compressed Tea), By Category (Conventional, VSS compliant, Potentially VSS Compliant), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Stores, Online, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Tata Consumer Products, Unilever PLC, Associated British Foods plc, Twinings, Apeejay Surrendra Group, Celestial Seasonings, Inc., Bettys & Taylors Group Ltd., The Republic of Tea, Bigelow Tea Company, Reily Foods Company, Gujarat Tea Processors and Packers Limited, Finlays, Mcleod Russel, Future Generation Co. Ltd, Vinatea, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |