Quick Navigation

- Report Overview

- Key Takeaways

- By Nature Analysis

- By Product Type Analysis

- By Fibre Analysis

- By Flavors Analysis

- By Source Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

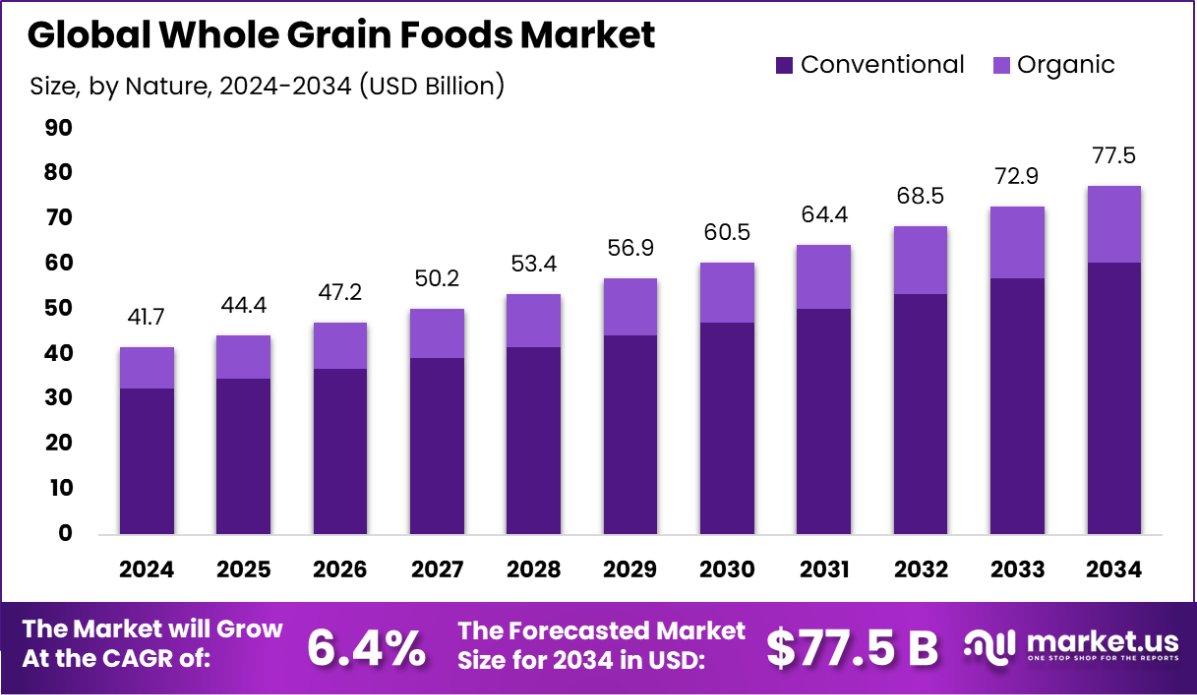

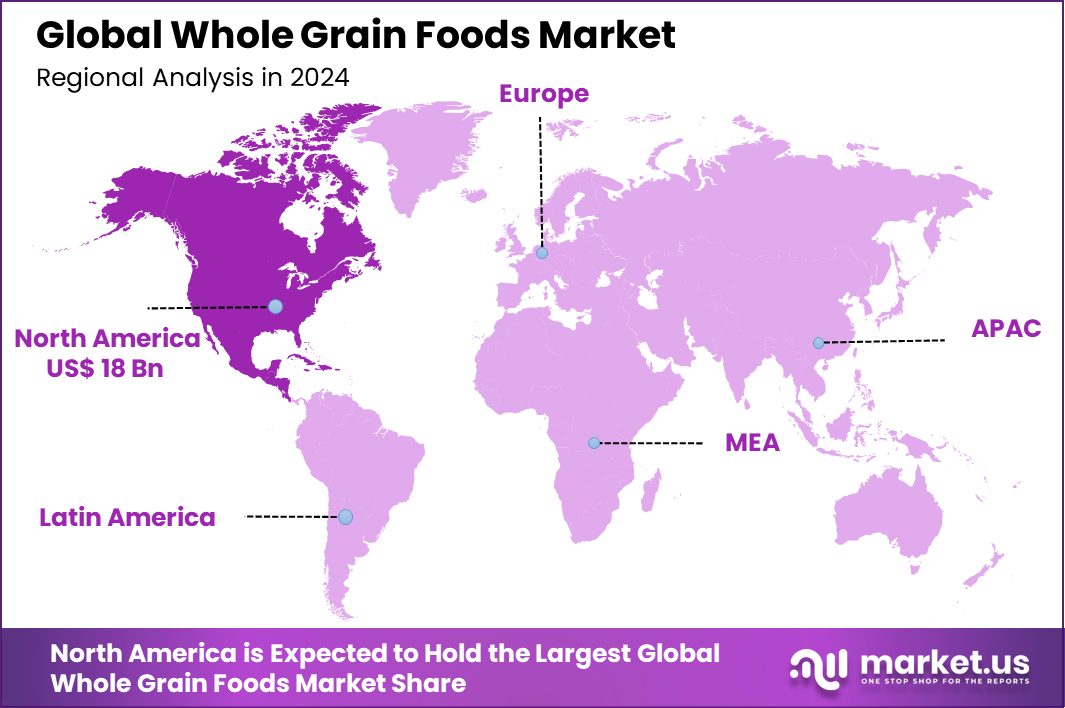

Global Whole Grain Foods Market is expected to be worth around USD 77.5 billion by 2034, up from USD 41.7 billion in 2024, and grow at a CAGR of 6.4% from 2025 to 2034. With a 43.20% market share, North America leads in whole grain food consumption, reaching USD 18 Bn.

Whole grain foods include cereals, bread, pasta, and rice that retain the entire grain kernel—bran, germ, and endosperm. These foods are rich in fiber, vitamins, and minerals, supporting digestion, heart health, and sustained energy. Unlike refined grains, whole grains provide essential nutrients like B vitamins, iron, and antioxidants.

Incorporating whole grains into daily diets can lower the risk of chronic diseases such as diabetes, obesity, and cardiovascular conditions. Despite their benefits, whole grain consumption remains low in many regions. The average whole grain intake in the US is low, with adults consuming about 20 g/day and children consuming about 13 g/day.

Consumer demand for whole grain foods is rising due to increasing awareness of healthy eating habits. People are shifting towards high-fiber diets to improve gut health and manage weight. Government campaigns and dietary guidelines promote whole grain consumption, encouraging food manufacturers to reformulate products. Additionally, the growth of plant-based diets is accelerating whole grain demand, as consumers look for natural, minimally processed food sources.

Opportunities in the whole grain food sector are expanding with innovation in food processing and packaging. The development of gluten-free whole grain options and fortified products attracts health-conscious consumers. A $10.5 million multi-year project called Cacao for Peace, financed by USAID and implemented by USDA, aims to strengthen Colombia’s cacao industry. Investments in agricultural sustainability and organic farming practices are further driving the availability of high-quality whole grains.

Government funding supports the growth of whole grain agriculture, benefiting both farmers and consumers. USDA has invested $33.7 million in the Colombian Cacao and Complementary Crops for Development program. Expanding research on whole grain nutrition enhances product development, making them more appealing to a wider audience. Increasing retail availability and improved marketing strategies are expected to boost whole grain consumption worldwide.

Key Takeaways

- Global Whole Grain Foods Market is expected to be worth around USD 77.5 billion by 2034, up from USD 41.7 billion in 2024, and grow at a CAGR of 6.4% from 2025 to 2034.

- The whole grain foods market is dominated by conventional products, accounting for 78.20% of total sales globally.

- Breads hold a significant share of the whole grain foods market, contributing 21.10% to the product segment.

- High-fiber foods are gaining popularity, representing 43.20% of the whole grain foods market by fiber content.

- Vanilla-flavored whole grain products capture 21.10% of market demand, reflecting consumer preference for flavored healthy options.

- Wheat remains the leading source in the whole grain foods market, making up 31.10% of total sales.

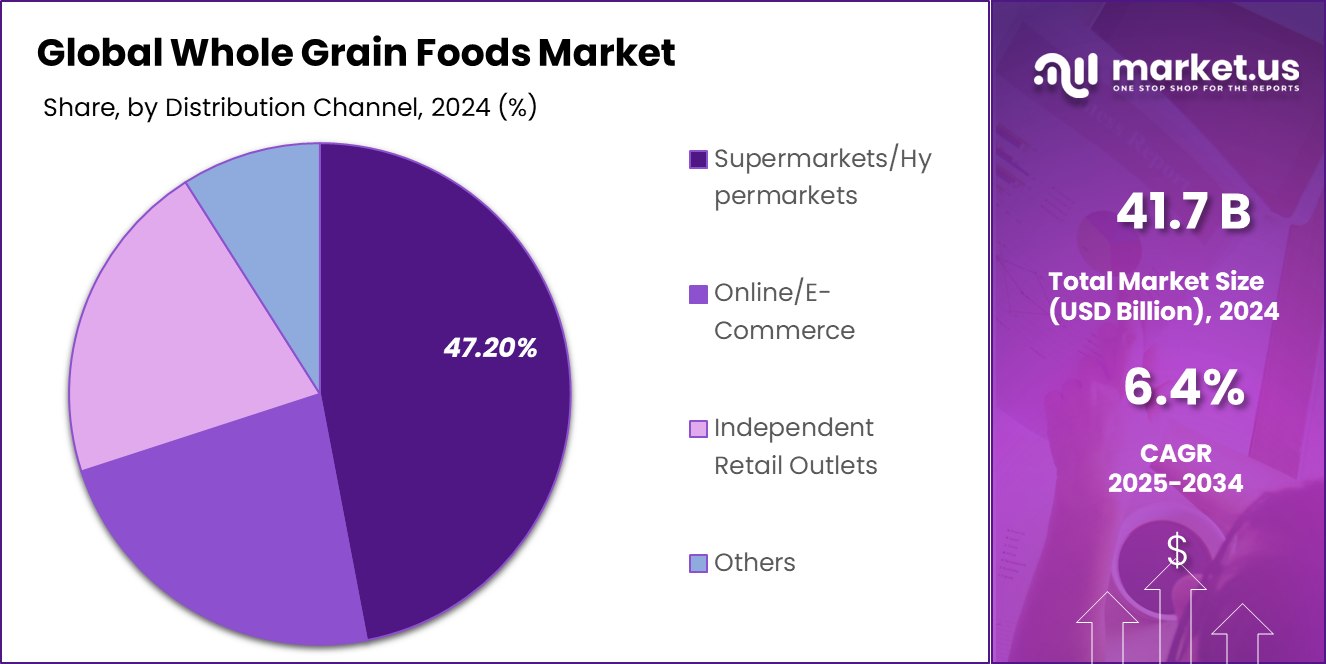

- Supermarkets and hypermarkets dominate distribution, accounting for 47.20% of whole-grain food purchases worldwide.

- The strong presence of health-conscious consumers in North America drives the Whole Grain Foods Market to USD 18 Bn.

By Nature Analysis

The whole grain foods market is dominated by conventional products at 78.20%.

In 2024, Conventional held a dominant market position in the “By Nature” segment of the Whole Grain Foods Market, with a 78.20% share. The substantial market share of the conventional segment can be attributed to its widespread availability, cost-effectiveness, and established consumer preference. Conventional whole grain products remain the preferred choice for a broad consumer base due to their lower price points compared to organic alternatives.

The dominance of conventional whole-grain foods is further reinforced by their extensive presence across retail chains, supermarkets, and online platforms. Manufacturers continue to focus on mass production, ensuring steady supply and affordability. Additionally, established brands benefit from strong distribution networks and brand loyalty, further solidifying their market share.

On the other hand, the organic segment, while growing, faces challenges such as higher production costs and premium pricing, which limits its penetration among price-sensitive consumers. However, rising consumer awareness regarding health benefits and sustainability factors is expected to drive organic growth in the coming years.

By Product Type Analysis

Breads hold a significant share of the market, accounting for 21.10%.

In 2024, Breads held a dominant market position in the “By Product” segment of the Whole Grain Foods Market, with a 21.10% share. The significant market presence of whole grain bread is driven by its widespread consumer preference as a staple food item, high nutritional value, and increasing demand for healthier alternatives to refined grain products. Whole grain breads are rich in fiber, vitamins, and minerals, making them a preferred choice for health-conscious consumers seeking better dietary options.

The growth of this segment is further fueled by the rising adoption of whole-grain diets among individuals looking to manage weight, improve digestion, and reduce the risk of chronic diseases such as diabetes and cardiovascular conditions. Additionally, major food manufacturers and bakery brands continue to innovate by introducing fortified, gluten-free, and multigrain variants to cater to evolving consumer preferences.

Supermarkets, hypermarkets, and online retail platforms play a crucial role in driving the sales of whole-grain bread, ensuring broad accessibility across urban and suburban markets. While other product categories, such as cereals and snacks, continue to gain traction, whole grain bread remains the leading category due to its daily consumption pattern and established presence in households globally.

By Fibre Analysis

High-fiber whole grain foods represent 43.20% of the total market demand.

In 2024, High Fibre Foods held a dominant market position in the “By Fibre” segment of the Whole Grain Foods Market, with a 43.20% share. The strong market share of high-fiber foods is primarily driven by increasing consumer awareness of the health benefits associated with fiber-rich diets.

High-fiber whole grain foods play a crucial role in digestive health, weight management, and reducing the risk of chronic diseases such as heart disease, diabetes, and obesity, making them a preferred choice among health-conscious consumers.

The demand for high-fiber foods is further supported by growing dietary shifts toward functional and fortified food products. Consumers are actively seeking food options that contribute to overall well-being, leading to increased consumption of whole-grain bread, cereals, pasta, and snacks that are naturally high in fiber. Additionally, regulatory bodies and health organizations continue to promote fiber intake, further driving the adoption of fiber-rich diets.

Retail expansion and product innovations in the food industry have also contributed to the segment’s growth. Major food brands are increasingly incorporating high-fiber ingredients in their product lines, ensuring better accessibility and variety for consumers. With fiber-rich diets becoming a global trend, this segment is expected to maintain its strong position in the Whole Grain Foods Market.

By Flavors Analysis

Vanilla-flavored whole grain products contribute to 21.10% of market sales.

In 2024, Vanilla held a dominant market position in the “By Flavors” segment of the Whole Grain Foods Market, with a 21.10% share. The widespread consumer preference for vanilla-flavored whole-grain foods is a key factor driving its market dominance. Vanilla is a versatile and widely accepted flavor, appealing to a broad consumer base across various product categories, including breakfast cereals, granola bars, flavored oatmeal, and baked goods.

The mild and naturally sweet taste of vanilla enhances the palatability of whole-grain foods, making them more appealing to both adults and children. Additionally, vanilla pairs well with other ingredients such as nuts, honey, and dried fruits, further increasing its application in the market. Food manufacturers are capitalizing on this trend by introducing new vanilla-infused product variants that cater to the growing demand for flavored, nutritious food options.

The retail presence of vanilla-flavored whole grain foods across supermarkets, convenience stores, and online platforms has also contributed to its significant market share. The increasing preference for clean-label, naturally flavored products further supports the growth of this segment. As consumer inclination toward healthier yet flavorful food choices continues to rise, vanilla is expected to maintain its strong position within the Whole Grain Foods Market.

By Source Analysis

Wheat remains the leading source, covering 31.10% of whole-grain foods.

In 2024, Wheat held a dominant market position in the “By Source” segment of the Whole Grain Foods Market, with a 31.10% share. The dominance of wheat in this segment is primarily attributed to its extensive use in various whole-grain food products, including bread, pasta, cereals, and baked goods. As a staple grain, wheat is widely cultivated and processed globally, making it a cost-effective and accessible option for both manufacturers and consumers.

The high consumer preference for wheat-based whole grain products is driven by its rich nutritional profile, which includes fiber, essential vitamins, and minerals. Whole wheat foods are often associated with health benefits such as improved digestion, better heart health, and weight management, further fueling their demand. Additionally, the versatility of wheat allows its incorporation into a wide range of food formulations, making it a preferred choice for product innovation.

Retail expansion, along with increasing awareness of whole grain consumption, has further strengthened wheat’s market position. Supermarkets, grocery stores, and online retail platforms offer a diverse range of wheat-based whole grain products, ensuring consistent availability. As consumers continue to shift towards healthier diets, wheat is expected to maintain its leading position in the Whole Grain Foods Market, supported by ongoing product developments and innovations.

By Distribution Channel Analysis

Supermarkets and hypermarkets drive 47.20% of whole grain food distribution.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Whole Grain Foods Market, with a 47.20% share. The significant market share of this distribution channel is primarily driven by the wide availability of whole grain food products, extensive product variety, and the convenience of one-stop shopping. Supermarkets and hypermarkets offer an extensive selection of whole grain products, including bread, cereals, pasta, and snacks, making them the preferred shopping destination for consumers.

The dominance of this channel is further reinforced by the strong presence of leading retail chains, aggressive promotional activities, and private-label offerings. Consumers prefer purchasing whole grain foods from supermarkets and hypermarkets due to the ability to compare brands, explore new product offerings, and take advantage of discounts and bulk purchase options.

Additionally, the increasing penetration of supermarket and hypermarket chains in emerging markets has contributed to the segment’s growth. These retail outlets have expanded their footprint in urban and suburban areas, ensuring greater accessibility of whole grain products. While e-commerce and specialty stores are gaining traction, supermarkets, and hypermarkets remain the primary distribution channels for whole grain foods, driven by their strong supply chain, consumer trust, and in-store shopping experience.

Key Market Segments

By Nature

- Conventional

- Organic

By Product Type

- Crackers

- Bread

- Cereals

- Tortillas

- Pasta

- Cookies

- Cakes

- Others

By Fibre

- High Fibre Foods

- Soluble Foods

- Insoluble Foods

By Flavors

- Vanilla

- Honey

- Chocolate

- Nuts

- Fruits

- Others

By Source

- Barley

- Wheat

- Farro

- Millet

- Quinoa

- Rice

- Black

- Brown

- Red

- Wild

- Others

- Oatmeal

- Popcorn

- Rye

- Maize

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Online/E- Commerce

- Independent Retail Outlets

- Others

Driving Factors

Rising Health Awareness Boosting Whole Grain Demand

The increasing awareness of health and nutrition is a major factor driving the growth of the Whole Grain Foods Market. Consumers are becoming more conscious of the benefits of whole grain consumption, which include better digestion, heart health, weight management, and a reduced risk of chronic diseases such as diabetes and obesity. Whole grains are rich in fiber, vitamins, and minerals, making them a preferred choice among health-conscious individuals.

Governments and health organizations are also promoting whole grain consumption through dietary guidelines and awareness campaigns. As a result, food manufacturers are expanding their whole-grain product lines to meet growing consumer demand. The shift towards healthier eating habits, coupled with rising disposable incomes, is expected to drive steady growth in the market.

Restraining Factors

High Prices of Whole Grain Products Limiting Growth

The higher cost of whole grain foods compared to refined grain alternatives is a key factor restraining market growth. Whole grain products require more processing, careful storage, and higher-quality raw materials, leading to increased production costs. As a result, they are often priced at a premium, making them less affordable for price-sensitive consumers, especially in developing markets.

Many consumers still prefer refined grain products due to their lower cost, longer shelf life, and familiar taste. Additionally, limited awareness about the long-term health benefits of whole grains further slows adoption. While demand is growing, overcoming price-related barriers through cost-effective production methods and increased consumer education will be crucial for the sustained expansion of the Whole Grain Foods Market.

Growth Opportunity

Innovation in Whole Grain Products Driving Demand

The increasing demand for diverse and innovative whole-grain food products presents a significant growth opportunity in the market. Consumers are looking for new and exciting ways to incorporate whole grains into their diets, driving manufacturers to introduce a wider variety of products such as fortified cereals, flavored whole grain snacks, and gluten-free options.

Companies are also focusing on product innovation by enhancing taste, texture, and convenience to attract a broader consumer base. The rise of plant-based and clean-label trends further supports the development of healthier whole-grain alternatives. As food brands invest in research and development to create appealing and nutritious options, the Whole Grain Foods Market is expected to witness strong growth in the coming years.

Latest Trends

Growing Demand for Gluten-Free Whole Grain Foods

A key trend in the Whole Grain Foods Market is the rising demand for gluten-free whole grain products. Consumers with gluten intolerance, celiac disease, or those choosing gluten-free diets for health reasons are actively seeking alternatives to traditional wheat-based products. This trend has led to increased production of gluten-free whole grain options such as quinoa, brown rice, millet, and sorghum.

Food manufacturers are responding by expanding their gluten-free product lines, offering better taste, texture, and nutritional value. Additionally, the growing popularity of plant-based and clean-label foods is further fueling demand for gluten-free whole-grain options. As awareness of dietary sensitivities rises, the gluten-free segment is expected to be a strong growth driver in the market.

Regional Analysis

In 2024, North America dominated the Whole Grain Foods Market with a 43.20% share, valued at USD 18 Bn.

The Whole Grain Foods Market exhibits varying growth dynamics across regions, influenced by dietary trends, health awareness, and regulatory frameworks. North America dominates the market, holding a 43.20% share, valued at approximately USD 18 billion, driven by increasing consumer preference for high-fiber, nutrient-rich diets and a surge in clean-label product demand.

Europe follows closely, with rising consumer inclination toward organic and whole grain-based bakery products, supported by stringent EU regulations on food labeling and nutrition claims.

Asia Pacific experiences significant growth due to urbanization, changing dietary habits, and a growing middle class increasingly seeking healthier food alternatives. Countries like China and India are witnessing increased whole grain product adoption due to government-backed nutrition programs and growing supermarket penetration.

In the Middle East & Africa, the market remains nascent but is expanding due to increasing awareness of diabetes and obesity-related health issues, prompting demand for fiber-rich diets. Meanwhile, Latin America shows moderate growth, with Brazil and Mexico leading due to rising disposable incomes and greater availability of whole grain foods in supermarkets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key players in the Whole Grain Foods Market, including Sanitarium, Bokomo, Pepsico SSA, and BARBARA’S, are driving market growth through product innovation, expanding distribution channels, and meeting rising consumer demand for healthier food choices.

Sanitarium continues to strengthen its market presence by focusing on plant-based and whole-grain products. The company’s strong brand reputation and commitment to nutrition-driven food options have helped it capture a significant consumer base, particularly in health-conscious regions. Its focus on clean-label and functional food products supports the growing demand for high-fiber diets.

Bokomo, a leading whole grain breakfast cereal manufacturer, maintains its competitive edge by offering a diverse product portfolio. The company leverages strong retail partnerships and a wide distribution network to expand its footprint. Its emphasis on affordability and accessibility makes it a preferred choice in emerging markets where demand for whole grain products is rising.

Pepsico SSA continues to expand its whole grain offerings through its well-established brands. The company capitalizes on its extensive distribution network and marketing capabilities to strengthen its position. With a growing emphasis on health and wellness, Pepsico SSA invests in product reformulation and the introduction of whole-grain snack alternatives.

BARBARA’S, known for its premium whole grain cereals and snacks, focuses on natural and organic ingredients to attract health-conscious consumers. The brand’s commitment to non-GMO and clean-label products aligns with evolving consumer preferences, further solidifying its role in the global whole-grain foods market.

Top Key Players in the Market

- Sanitarium

- Bokomo

- Pepsico SSA

- BARBARA’S

- The Quaker Oats Company

- Post Holdings, Inc.

- Barilla

- Nature’s Path Foods.

- Cargill

- Odlums

- Weetabix

- Nestle

- General Mills

- Allied Bakeries

- ARDENT MILLS

Recent Developments

- In 2024, ARDENT MILLS launched Ancient Grains Plus, a clean-label blend enhancing baking functionality. Their regenerative agriculture program enrolled over 598,000 acres across 12 regions, promoting sustainable farming practices. Additionally, Ardent Mills directed $19.75 million to diverse suppliers, underscoring their commitment to inclusivity.

- In 2024, Nestlé made substantial efforts to strengthen its position in the whole grain foods sector. The company reported achieving organic growth of 2.2%, demonstrating resilience despite the broader challenges of soft consumer demand. This growth was supported by strategic initiatives aimed at enhancing product offerings and optimizing pricing strategies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 41.7 Billion |

| Forecast Revenue (2034) | USD 77.5 Billion |

| CAGR (2025-2034) | 6.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Nature (Conventional, Organic), By Product Type (Crackers, Breads, Cereals, Tortillas, Pasta, Cookies, Cakes, Others), By Fibre (High Fibre Foods, Soluble Foods, Insoluble Foods), By Flavors (Vanilla, Honey, Chocolate, Nuts, Fruits, Others), By Source (Barley, Wheat, Farro, Millet, Quinoa, Rice(Black, Brown, Red, Wild, Others), Oatmeal, Popcorn, Rye, Maize, Others), By Distribution Channel (Supermarkets/Hypermarkets, Online/E- Commerce, Independent Retail Outlets, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Sanitarium, Bokomo, Pepsico SSA, BARBARA’S, The Quaker Oats Company, Post Holdings, Inc., Barilla, Nature’s Path Foods., Cargill, Odlums, Weetabix, Nestle, General Mills, Allied Bakeries, ARDENT MILLS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |