Quick Navigation

Report Overview

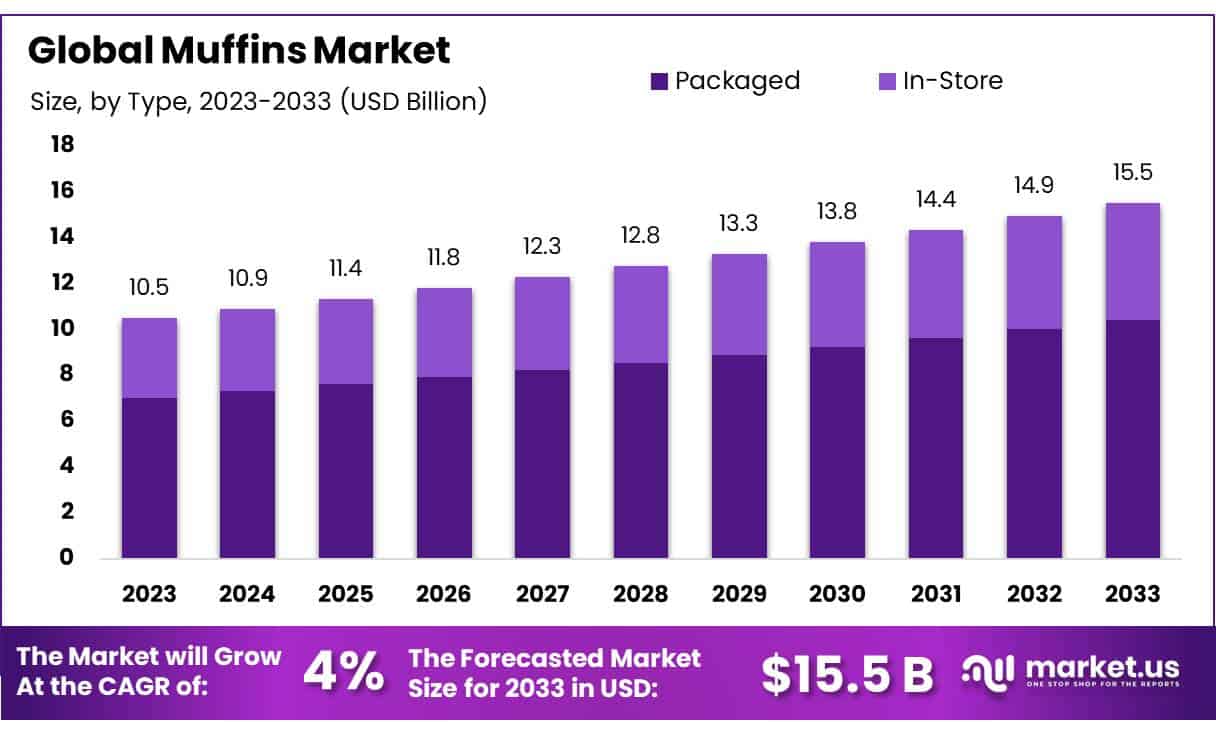

The Global Muffins Market size is expected to be worth around USD 15.5 Bn by 2033, from USD 10.5 Bn in 2023, growing at a CAGR of 4.0% during the forecast period from 2024 to 2033.

Muffins, individually portioned baked goods, are categorized into sweet quick breads and flatbreads. The more common type, “American muffins,” are made from a batter of flour, eggs, sugar, and leavening agents. These muffins are typically baked in cup-sized molds, resulting in a moist texture. Popular as breakfast items or snacks, they come in a variety of flavors, such as fruit, chocolate, or nuts.

The foodservice sector, including cafés, bakeries, and quick-service restaurants, accounts for a substantial portion of muffin consumption. In 2022, over 45% of global muffin market revenue came from the foodservice industry, driven by the rising demand for packaged and ready-to-eat bakery products.

The U.S. bakery product sector alone was valued at approximately USD 53.4 billion in 2022, with muffins contributing significantly to this market size, according to the USDA.

Regulatory trends are reshaping the industry, with governments promoting healthier food options. In the U.S., the FDA has issued guidelines to reduce added sugars in packaged foods, influencing muffin manufacturers to create healthier alternatives. Similarly, the European Union’s stricter labeling regulations aim to improve ingredient transparency, further encouraging the development of nutritious products.

The global muffin trade has witnessed significant growth. In 2023, the U.S. exported bakery goods worth approximately USD 1.2 billion, including muffins, with Canada, Mexico, and Japan as key markets. At the same time, imports are increasing in Asia-Pacific countries like China and India, driven by urbanization and a growing middle class.

Market players are expanding to meet growing demand. Grupo Bimbo’s acquisition of Canada Bread Company in 2023 highlights the focus on broadening product portfolios and geographic reach. Similarly, Hostess Brands and Flowers Foods are strengthening distribution in emerging regions such as Asia-Pacific and Latin America.

Key Takeaways

- Muffins Market size is expected to be worth around USD 15.5 Bn by 2033, from USD 10.5 Bn in 2023, growing at a CAGR of 4.0%.

- Packaged segment held a dominant market position in the muffins market, capturing more than a 67.2% share.

- Sweet segment held a dominant market position in the muffins market, capturing more than an 81.2% share.

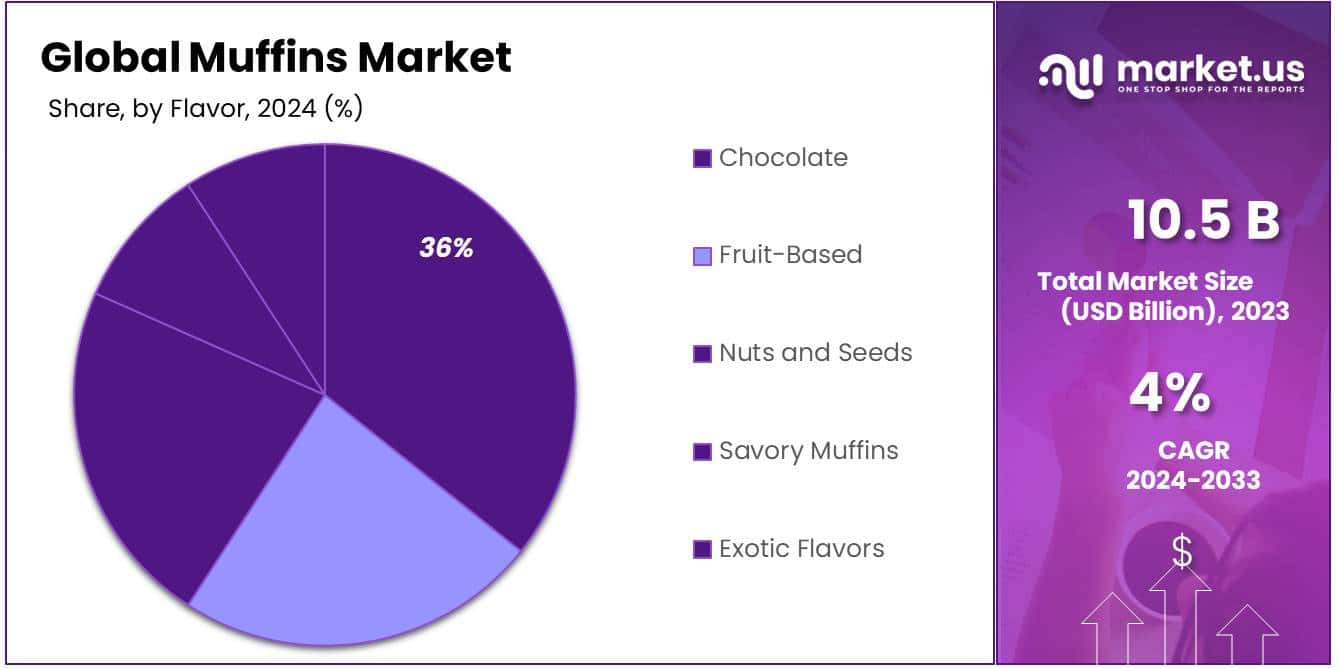

- Chocolate held a dominant market position in the muffins market, capturing more than a 35.6% share.

- Single-Serve held a dominant market position in the muffins market, capturing more than a 45.2% share.

- Adults held a dominant market position in the muffins market, capturing more than a 52.3% share.

- Hypermarkets & Supermarkets held a dominant market position in the muffins market, capturing more than a 57.1% share.

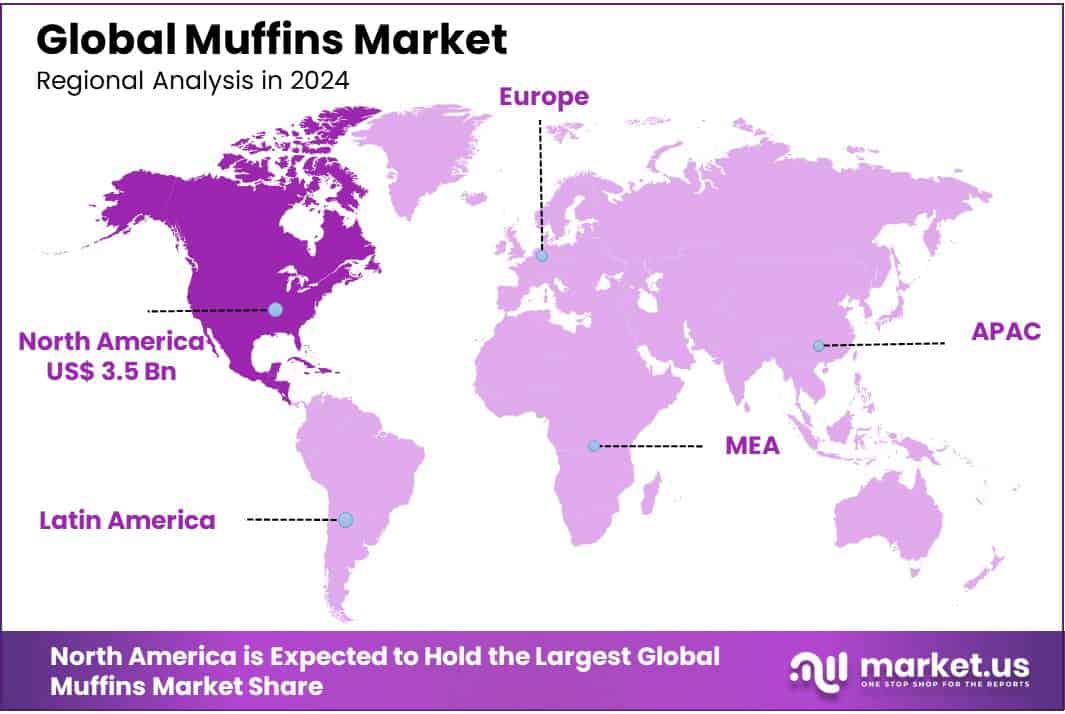

- North America is the dominant region, capturing a 32.1% market share with revenues reaching USD 3.5 billion.

By Type

By Taste

In 2023, the Sweet segment held a dominant market position in the muffins market, capturing more than an 81.2% share. This preference is largely due to the widespread popularity of sweet flavors among consumers who often consume muffins as snacks or desserts.

Flavors like blueberry, chocolate, and vanilla are especially favored, contributing significantly to the segment’s market dominance. The availability of a wide range of sweet muffin varieties in both packaged and in-store formats helps sustain its appeal across various consumer demographics.

By Flavor

In 2023, Chocolate held a dominant market position in the muffins market, capturing more than a 35.6% share. This segment’s popularity is driven by the universal appeal of chocolate, which makes it a preferred choice for both daily snacks and special occasions. Chocolate muffins offer a rich, indulgent experience that appeals to a wide range of consumers, from children to adults.

Fruit-Based muffins are also a popular choice, featuring ingredients like blueberries, bananas, and apples. These muffins are appreciated for their natural sweetness and perceived health benefits, making them a favored option for health-conscious consumers who still wish to indulge.

Nuts and Seeds segment offers a crunchy texture and added nutritional value, appealing particularly to those looking for a protein-rich snack or a healthier alternative within the muffin category.

Savory Muffins incorporate non-sweet ingredients such as cheese, herbs, and bacon, catering to consumers who prefer less sugary options. This segment is growing as more people choose savory muffins as a meal component or a substantial snack.

Exotic Flavors, which include unique combinations such as matcha, lavender, and pumpkin spice, target adventurous eaters looking to experiment with new and unusual taste profiles. This segment, though smaller, is significant for its ability to attract niche markets seeking innovation in traditional baked goods.

By Packaging Type

By Consumer Segment

In 2023, Adults held a dominant market position in the muffins market, capturing more than a 52.3% share. This segment’s strength is driven by adults’ purchasing power and their diverse preferences that span sweet, savory, and health-oriented muffin options. Adults often choose muffins as a convenient snack or a quick breakfast solution, balancing between indulgence and health-conscious choices.

Children form a significant consumer segment as well, with a preference for sweet and chocolate-flavored muffins. This group is particularly attracted to brightly packaged, single-serve muffins that are ideal for school lunches or as treats.

Seniors, while a smaller segment of the muffin market, prefer muffins that are softer and less sweet, often choosing fruit-based or nut and seed varieties that offer better nutritional profiles suitable for dietary needs. The availability of these options in single-serve and multi-pack formats also makes it convenient for seniors managing smaller household sizes or specific health conditions.

By Distribution Channel

In 2023, Hypermarkets & Supermarkets held a dominant market position in the muffins market, capturing more than a 57.1% share. These retail giants are popular for their wide assortment of muffin brands and types, from single-serve packs to bulk options, catering to a diverse consumer base. The convenience of one-stop shopping for a variety of grocery items, including bakery products like muffins, makes these outlets highly preferred by consumers.

Convenience Stores also play a significant role in the distribution of muffins, offering quick grab-and-go options that are essential for busy consumers looking for a fast snack or breakfast solution. Their strategic locations and extended hours cater to immediate consumer needs.

The Online distribution channel has seen growth with the rise of e-commerce and changing consumer behaviors. Online platforms offer the convenience of home delivery and often provide access to a broader range of specialty muffins that might not be available in traditional stores.

Specialty Stores, including bakeries and gourmet shops, focus on offering premium and artisanal muffins, often freshly baked. These outlets attract consumers looking for high-quality, unique flavors that differ from mass-produced options.

Key Market Segments

By Type

- Packaged

- In-Store

By Taste

- Sweet

- Savoury

By Flavor

- Chocolate

- Fruit-Based

- Nuts and Seeds

- Savory Muffins

- Exotic Flavors

By Packaging Type

- Single-Serve

- Multi-Pack

- Bulk Packaging

- Gift Packaging

By Consumer Segment

- Children

- Adults

- Seniors

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Online

- Specialty Stores

- Others

Drivers

Growth of On-the-Go Consumption

According to the Food and Agriculture Organization (FAO), the global demand for convenience foods has grown rapidly in recent years, particularly in urban areas. Muffins, with their convenient single-serve packaging and wide variety of flavors, align with this shift toward quick, easy-to-eat snacks. In particular, single-serve muffin packaging is increasingly appealing to consumers who are looking for on-the-go options.

Consumer Trends Towards Healthier Options

Additionally, there is a growing shift towards healthier snack options, which has contributed to the rise in demand for muffins made with organic ingredients, gluten-free flour, or those containing added nutritional benefits such as high fiber, protein, or low sugar.

According to the World Health Organization (WHO), more than 40% of the global population is estimated to consume snacks daily, with many preferring healthier alternatives. Muffin manufacturers are responding to this demand by creating healthier muffin options, such as those made with whole grains, nuts, seeds, and low-fat dairy, to cater to the increasing number of health-conscious consumers.

Increased Retail Availability and Innovations in Packaging

The widespread availability of muffins in various retail formats also supports market growth. Muffins are increasingly offered in major hypermarkets and supermarkets, as well as in convenience stores and online platforms, making them easily accessible to a larger consumer base.

In the U.S. alone, packaged bakery products, including muffins, accounted for over USD 7 billion in sales in 2023, driven by expanding distribution networks and growing consumer interest in ready-to-eat bakery products. Furthermore, innovations in muffin packaging, such as eco-friendly, resealable bags and multi-pack options, have further boosted their popularity.

Government Initiatives to Promote Healthy Eating

Several governments and organizations are encouraging healthier eating habits, which benefits the muffin sector by encouraging manufacturers to innovate with healthier ingredients.

For instance, in 2023, the U.S. Department of Agriculture (USDA) launched initiatives to promote better food labeling and ingredient transparency, allowing consumers to make more informed choices about what they consume. These initiatives are helping to increase demand for products that meet health-conscious standards, including muffins that are low in fat, sugar, and artificial additives.

Restraints

Growing Health Consciousness Among Consumers

According to the World Health Organization (WHO), global sugar consumption has been a major concern due to its link to health issues such as obesity, diabetes, and heart disease. WHO recommends that adults limit their intake of free sugars to less than 10% of total energy intake, with further benefits below 5%.

This translates to about 25 grams (or roughly 6 teaspoons) of sugar per day for an adult. However, many muffins, particularly the sweeter varieties, can contain up to 20-30 grams of sugar per serving, far exceeding the recommended intake. As a result, there is growing concern among health-conscious consumers about the excessive sugar content in these products, leading to a reduction in demand for traditional muffins.

Impact of Sugar Regulations and Taxes

Governments and health organizations are increasingly implementing policies to curb the consumption of sugary foods. For instance, several countries have introduced sugar taxes on sugary beverages and high-sugar foods, including baked goods like muffins. In the UK, the Soft Drinks Industry Levy (SDIL), implemented in 2018, imposed taxes on sugary drinks, which spurred the food and beverage industry to reduce sugar content in various products, including muffins.

In response to such regulations, many manufacturers have started to reformulate their products to lower sugar levels or offer sugar-free and low-sugar alternatives. However, these changes come at an additional cost, which can affect profit margins for muffin manufacturers.

In Mexico, the government has implemented a sugar tax of 1 peso per liter on sugary drinks, which has led to a reduction in sugar consumption in the country. Although this tax specifically targets sugary beverages, it has had a ripple effect on the overall baked goods market, as consumers become more aware of the health risks associated with excessive sugar intake. Similarly, in the U.S., the Healthy Hunger-Free Kids Act has set guidelines for school meals, which limits the amount of sugar in snacks like muffins, further influencing consumer behavior.

Consumer Shift Towards Natural and Organic Ingredients

As health concerns regarding artificial ingredients and preservatives rise, consumers are increasingly opting for organic, preservative-free, and naturally sweetened food products. The trend towards clean-label foods, where products contain minimal artificial ingredients, is reshaping the muffin market.

According to the U.S. Department of Agriculture (USDA), the organic food market in the U.S. grew by 12.4% in 2022, and the demand for organic baked goods is expected to follow a similar upward trend. However, producing muffins with organic ingredients and natural sweeteners such as stevia or honey can increase production costs. This shift towards healthier, cleaner alternatives may lead to higher prices for muffins, which could limit market accessibility, particularly in price-sensitive regions.

Opportunity

Health-Conscious Consumer Demand

The global shift toward healthier eating habits presents an opportunity for muffin manufacturers to develop products that align with consumer expectations for lower sugar, higher fiber, and protein-enriched baked goods.

According to the World Health Organization (WHO), globally, more than 2 billion adults are overweight or obese, highlighting the need for healthier food options. This has created an increased demand for products that are not only tasty but also provide functional benefits. As a result, consumers are seeking out muffins made with whole grains, oats, low glycemic index ingredients, and added superfoods like chia seeds, flax seeds, and oats.

For example, muffins enriched with plant-based proteins (such as pea protein or soy protein) or fiber from natural sources like psyllium husk or oats are gaining popularity. The U.S. Department of Agriculture (USDA) reports that nearly 20% of adults in the U.S. are now following a plant-based diet, further driving the demand for plant-based and vegan muffins.

This segment is expected to grow significantly in the coming years, with plant-based food sales projected to reach $85 billion by 2030, according to the Plant Based Foods Association (PBFA).

Rising Popularity of Clean-Label and Organic Muffins

Consumers are increasingly prioritizing clean-label products, which contain minimal or no artificial additives, preservatives, or colors. This demand for natural and organic ingredients has led to growth in the market for muffins made with organic flour, natural sweeteners, and non-GMO ingredients.

The USDA Organic Program reports that organic food sales in the U.S. reached $61.9 billion in 2022, growing by 12.4% from the previous year. This trend toward organic products is influencing the muffin market, where manufacturers are now incorporating organic and non-GMO ingredients into their recipes to meet consumer demand for transparency and healthier options.

Muffin brands that adopt clean-label and organic certifications can attract health-conscious consumers who are willing to pay a premium for products they perceive as healthier. In fact, according to the Organic Trade Association, 94% of U.S. consumers say they consider organic ingredients when making food purchase decisions, creating a significant opportunity for muffin manufacturers to tap into this growing consumer base.

Expansion of Convenience and On-the-Go Products

As busy lifestyles continue to dominate, consumers are increasingly seeking convenient and portable food options, and muffins are well-positioned to cater to this demand. The rise of single-serve packaging and grab-and-go formats has made muffins a popular snack choice for consumers on the move. According to the International Food Information Council (IFIC), 74% of consumers are interested in foods that offer both convenience and nutritional value.

Muffin manufacturers can capitalize on this trend by offering individually packaged muffins that are portion-controlled and available in various flavors and functional formats. The growing popularity of meal replacement muffins, which offer a combination of protein, fiber, and other nutrients, presents a significant opportunity for innovation. These muffins can serve as a nutritious breakfast or snack option for busy professionals, students, or individuals seeking healthier alternatives to traditional on-the-go snacks.

Focus on Sustainable Packaging and Eco-Friendly Practices

According to The World Economic Forum, approximately 8 million metric tons of plastic end up in the oceans each year, prompting increased demand for eco-friendly packaging solutions. Consumers are actively seeking brands that use sustainable materials, such as recyclable, biodegradable, or compostable packaging. Muffin manufacturers can capitalize on this trend by adopting sustainable packaging practices and promoting their eco-friendly initiatives.

Trends

Rise in Demand for High-Protein and Low-Sugar Muffins

Consumers today are looking for baked goods that align with their nutritional goals, especially products that are high in protein and low in sugar. According to the U.S. Department of Agriculture (USDA), protein consumption has steadily increased in the U.S., with high-protein snacks seeing a rise of over 20% in demand over the last five years.

The Academy of Nutrition and Dietetics states that a balanced protein intake is essential for overall health, and as such, there is a growing interest in products like muffins that offer protein in a convenient, snackable format.

The trend is particularly strong in the millennial and Generation Z demographics, where 41% of consumers are actively reducing sugar intake and 30% are seeking higher protein options, according to a 2022 survey by the International Food Information Council (IFIC). This has prompted manufacturers to innovate with muffin offerings that cater to these specific consumer preferences.

The Growth of Gluten-Free and Allergen-Free Muffins

Another major trend in the muffin market is the increased popularity of gluten-free and allergen-free muffins. The global gluten-free product market is growing rapidly, with a projected CAGR of 9.4% from 2023 to 2028, according to data from the National Institutes of Health (NIH). As the prevalence of gluten intolerance, celiac disease, and food allergies increases, more consumers are turning to baked goods that cater to these dietary restrictions.

The demand for gluten-free muffins is significant, and manufacturers are increasingly using almond flour, coconut flour, and rice flour to create muffins that are not only gluten-free but also low in carbohydrates.

The FDA has defined gluten-free foods as those containing less than 20 parts per million (ppm) of gluten, which has spurred confidence in gluten-free products and allowed manufacturers to enter this growing market segment with greater ease. In 2023, gluten-free muffins were estimated to capture 25% of the total muffin market, reflecting the growing consumer demand for allergen-free options.

Clean Label and Organic Muffins on the Rise

Consumers are also increasingly seeking clean-label muffins, meaning products made with natural, recognizable ingredients and no artificial preservatives or additives. The Clean Label Project, an independent organization, has noted that 50% of U.S. consumers now consider food transparency, including ingredient sourcing and the absence of artificial additives, as essential when making purchasing decisions.

In response to this demand, muffin manufacturers are incorporating organic ingredients into their products, including organic wheat flour, organic sugar, and organic fruits. In 2023, the organic food market in the U.S. reached $61.9 billion, according to the Organic Trade Association, with 9.7% of all food sales in the country now attributed to organic products.

This growth is expected to continue, further driving demand for organic muffins that appeal to consumers looking for healthier, more sustainable food choices. Manufacturers are also adopting more sustainable packaging in response to consumer concerns about the environmental impact of single-use plastics. According to World Economic Forum, more than 40% of global consumers are now willing to pay a premium for products with environmentally friendly packaging.

Regional Analysis

In the Muffins Market, North America is the dominant region, capturing a 32.1% market share with revenues reaching USD 3.5 billion. This leadership is driven by a robust demand for convenience foods and a cultural penchant for quick, indulgent snacks. The U.S. leads within this region, with consumers favoring a variety of flavors and health-conscious options, including gluten-free and whole-grain muffins.

Europe follows closely, characterized by a strong preference for artisanal and premium bakery products. The market here is bolstered by consumer demand for organic and minimally processed foods, with significant contributions from countries like the UK, Germany, and France. This region is also seeing a shift towards healthier eating habits, influencing product offerings in the muffin segment.

The Asia Pacific region is experiencing rapid growth, driven by urbanization and changing consumer lifestyles, particularly in emerging economies such as China and India. The rising middle class and increasing disposable income in these countries are amplifying the demand for convenient snack options, thereby expanding the muffin market.

In the Middle East & Africa, the market is expanding moderately, supported by increasing tourism and a growing openness to Western-style baked goods. The diverse cultural landscape is beginning to embrace more varied food options, including Western bakery products like muffins.

Latin America, while smaller in market share, is witnessing growth driven by urbanization and the influence of global food trends, which include a rising appetite for convenient and ready-to-eat bakery items among its youthful population.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The muffins market is characterized by the presence of several key players that dominate the industry through extensive product portfolios, distribution networks, and strategic market positioning. Major players such as ARYZTA AG, Grupo Bimbo, and Flowers Foods, Inc. are pivotal in shaping market trends, with a significant focus on premium and health-oriented muffin products.

ARYZTA AG and Grupo Bimbo have a wide-reaching presence in North America and Europe, offering a variety of muffins through multiple brands and distribution channels, while Flowers Foods continues to strengthen its position with a focus on both fresh and packaged muffin varieties.

Additionally, General Mills and Kellogg’s, known for their widespread presence in the breakfast and snack foods category, also contribute substantially to the muffin market with their portfolio of branded muffin products and innovation in flavors and formulations.

Dunkin’ Brands, Starbucks Corporation, and Hostess Brands, Inc. represent prominent players in the quick-service restaurant (QSR) sector, where muffins are a key part of the breakfast and snack menu. These companies drive significant demand for on-the-go muffin consumption, catering to a growing consumer preference for convenience.

Mondelez International and Nestlé S.A., with their well-established brands such as Oreo and Nestlé Muffins, focus on expanding their product offerings through innovative flavors and marketing strategies aimed at a broad consumer base. Pepperidge Farm and Otis Spunkmeyer are also major players, particularly in the packaged muffin segment, leveraging their extensive retail and foodservice distribution channels.

Top Key Players

- ARYZTA

- Aryzta AG

- Britannia Industries

- Dunkin’ Brands Group, Inc.

- Finsbury Food Group Limited

- Flowers Foods, Inc.

- Foodco Group Pty Ltd

- General Mills

- George Weston Limited

- Grupo Bimbo

- Hostess Brands, Inc.

- J.M. Smucker Company

- Kellogg’s

- McKee Foods

- Mondelez International, Inc.

- Nestlé S.A.

- Otis Spunkmeyer

- Pepperidge Farm, Inc.

- Rich Products Corporation

- Sara Lee Frozen Bakery

- Starbucks Corporation

- The Hain Celestial Group, Inc.

- The Hershey Company

- The J.M. Clayton Company

- Weston Foods Inc.

Recent Developments

In 2023, ARYZTA generated USD 3.4 billion in revenue, with a notable portion of this revenue coming from its baked goods and muffin products.

Britannia Industries reported a significant sale of goods valued at over 159 billion Indian rupees during this period, indicating a robust performance in its bakery segment, which includes muffins among other bakery products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 10.5 Bn |

| Forecast Revenue (2033) | USD 15.5 Bn |

| CAGR (2024-2033) | 4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Packaged, In-Store), By Taste(Sweet, Savoury), By Flavor (Chocolate, Fruit-Based, Nuts and Seeds, Savory Muffins, Exotic Flavors), By Packaging Type (Single-Serve, Multi-Pack, Bulk Packaging, Gift Packaging), By Consumer Segment (Children, Adults, Seniors), By Distribution Channel (Hypermarkets and Supermarkets, Convenience Stores, Online, Specialty Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ARYZTA, Aryzta AG, Britannia Industries, Dunkin’ Brands Group, Inc., Finsbury Food Group Limited, Flowers Foods, Inc., Foodco Group Pty Ltd, General Mills, George Weston Limited, Grupo Bimbo, Hostess Brands, Inc., J.M. Smucker Company, Kellogg’s, McKee Foods, Mondelez International, Inc., Nestlé S.A., Otis Spunkmeyer, Pepperidge Farm, Inc., Rich Products Corporation, Sara Lee Frozen Bakery, Starbucks Corporation, The Hain Celestial Group, Inc., The Hershey Company, The J.M. Clayton Company, Weston Foods Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |