Global Pulse Ingredient Market Size, Share, And Industry Analysis Report By Type (Pulse Flour, Pulse Starch, Pulse Protein, Pulse Fibers and Grits), By Function (Texturization, Emulsification, Gelation, Water-Holding, Adhesion, Film Forming, Blending), By Source (Peas, Lentils, Chickpeas, Beans), By Application (Food and Beverages, Feed), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181779

- Number of Pages: 223

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

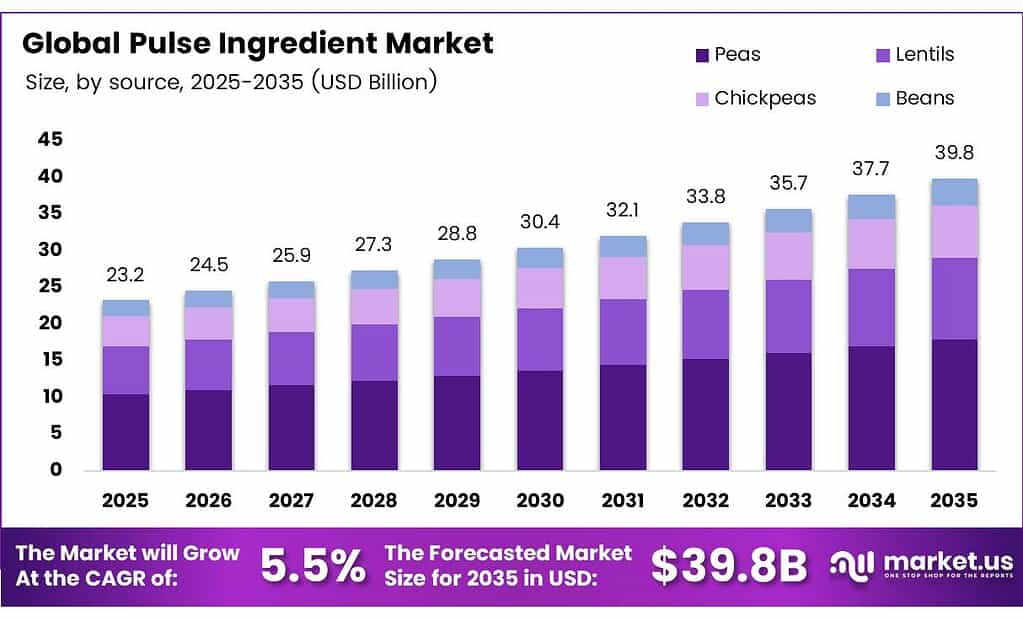

The Global Pulse Ingredient Market size is expected to be worth around USD 39.8 billion by 2035 from USD 23.2 billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026 to 2035.

Pulse ingredients refer to processed derivatives of legumes such as peas, lentils, chickpeas, and beans. These derivatives include pulse flours, starches, proteins, and fibers. Food manufacturers use pulse ingredients across bakery, dairy, snacks, and beverage applications to improve nutritional value and functionality.

The market gains traction as consumers increasingly shift toward plant-based diets. Pulse ingredients deliver high protein density, dietary fiber, and essential amino acids. Consequently, food companies reformulate products to meet growing demand for clean-label and allergen-free alternatives in both retail and foodservice channels.

Canada produced 3.0 million tonnes of peas in 2024, up 14.9% from 2023. This supply expansion strengthens raw material availability for global pulse ingredient processors, stabilizing input costs and supporting production scale-up.

India produced 252.38 lakh tonnes of pulses in 2024-25 under the Third Advance Estimate. This output confirms India’s scale as the largest global producer and a critical domestic market for pulse-based ingredient manufacturing and consumption.

Sustainability narratives also strengthen the market position of pulse ingredients. Pulses fix atmospheric nitrogen, reducing the need for synthetic fertilizers. Therefore, ingredient processors and food brands increasingly highlight pulses’ low carbon footprint and regenerative farming credentials to attract environmentally conscious buyers.

Key Takeaways

- The Global Pulse Ingredient Market is valued at USD 23.2 billion in 2025 and is projected to reach USD 39.8 billion by 2035 at a CAGR of 5.5% during the forecast period 2026–2035.

- Pulse Flour dominates with a 37.9% market share in 2025.

- Texturization holds the leading position with a 23.7% share.

- Peas represent the dominant raw material with a 38.4% share.

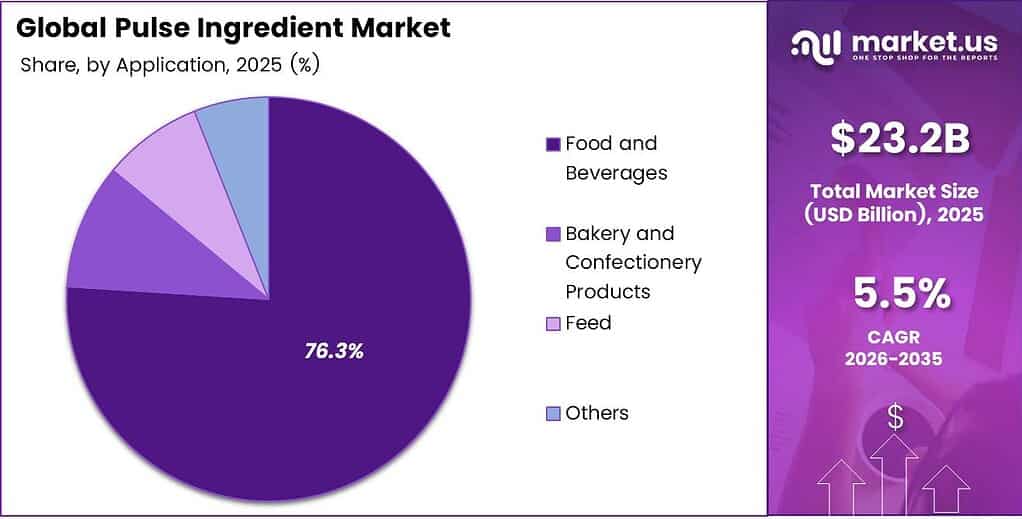

- Food and Beverages lead all end-use segments with a 76.3% share.

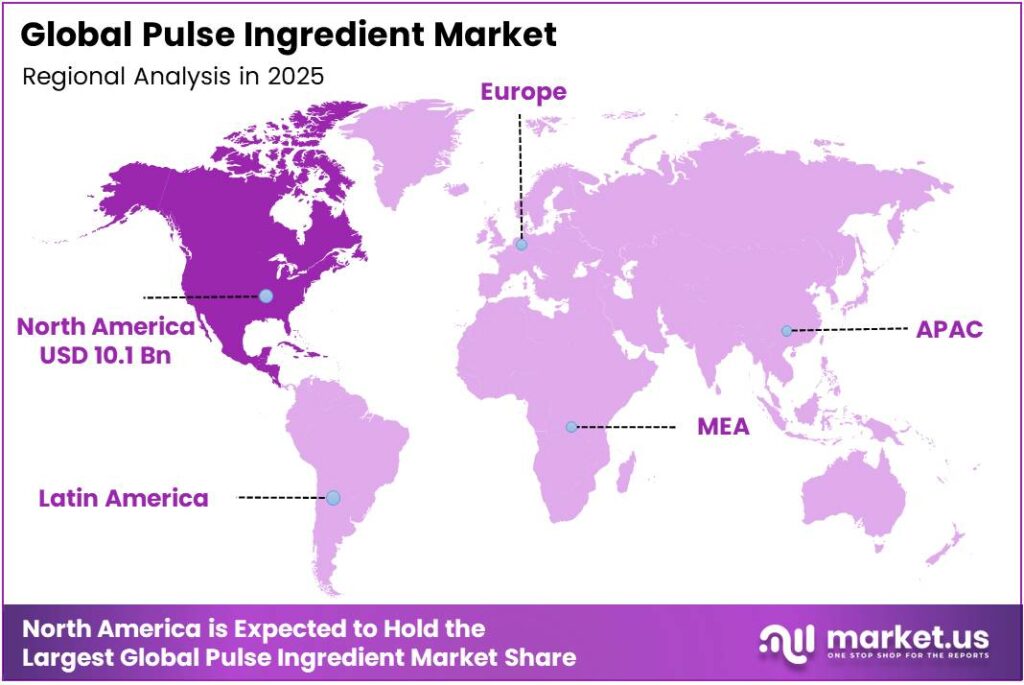

- North America dominates the regional landscape with a 43.6% market share, valued at USD 10.1 billion.

By Type Analysis

Pulse Flour dominates with 37.9% due to its versatile functional properties and wide adoption across bakery and snack applications.

In 2025, Pulse Flour held a dominant market position in the By Type segment of the Pulse Ingredient Market, with a 37.9% share. Food manufacturers prefer pulse flour for its binding, thickening, and nutritional fortification capabilities. Moreover, its allergen-free profile makes it a preferred substitute for wheat flour across gluten-free product lines globally.

Pulse Starch captures a meaningful share of the market due to its clean-label appeal and functional performance in processed foods. Food processors use pulse starch as a thickening and gelling agent in soups, sauces, and ready meals. Its neutral taste and transparent gel formation make it a favorable choice in dairy and beverage formulations.

By Function Analysis

Texturization dominates with 23.7% as food manufacturers prioritize pulse ingredients for improving mouthfeel and structural integrity in plant-based products.

In 2025, Texturization held a dominant market position in the By Function segment of the Pulse Ingredient Market, with a 23.7% share. Food companies use pulse-based texturizers to replicate the fibrous structure of meat in plant-based alternatives. Moreover, texturization enables manufacturers to deliver satisfying product experiences that meet mainstream consumer expectations for taste and mouthfeel.

Emulsification represents a key functional application for pulse ingredients in food processing. Pulse proteins and lecithins stabilize oil-water interfaces in dressings, sauces, and dairy analogues. Consequently, emulsification applications support the reformulation of conventional products into cleaner, plant-derived ingredient alternatives.

By Source Analysis

Peas dominate with 38.4% as their high protein content, functional versatility, and strong global supply chain position them as the preferred pulse source.

In 2025, Peas held a dominant market position in the By Source segment of the Pulse Ingredient Market, with a 38.4% share. Pea proteins and flours offer neutral flavor profiles and superior water solubility. Therefore, food manufacturers widely adopt pea-derived ingredients across protein beverages, meat analogues, and bakery products globally.

Lentils serve as a significant pulse source, particularly valued for their high iron content and easily digestible protein. Ingredient processors extract lentil flour and starch for use in soups, flatbreads, and pasta. Additionally, lentils attract growing interest in infant and clinical nutrition segments due to their gentle digestibility.

By Application Analysis

Food and Beverages dominate with 76.3%, as pulse ingredients deliver nutritional and functional benefits across the full spectrum of processed food categories.

In 2025, Food and Beverages held a dominant market position in the By Application segment of the Pulse Ingredient Market, with a 76.3% share. Food manufacturers integrate pulse ingredients across bakery, snacks, dairy, and beverage categories. Moreover, the shift toward plant-based and high-protein products continues to expand pulse ingredient penetration within this broad application segment.

Bakery and Confectionery Products represent the largest sub-category within food and beverage applications. Bakers use pulse flours and proteins to improve nutritional profiles and texture in breads, cookies, and crackers. Additionally, pulse-based formulations support gluten-free product development that meets growing consumer demand for dietary inclusivity.

Snacks and Dairy sub-segments both show strong growth as manufacturers reformulate toward cleaner and more protein-rich offerings. Snack brands incorporate pulse proteins and fibers to deliver high-protein positioning on packaging. Consequently, dairy alternative brands use pulse proteins to build creaminess and mouthfeel in plant-based yogurt and beverage applications.

Key Market Segments

By Type

- Pulse Flour

- Pulse Starch

- Pulse Protein

- Pulse Fibers and Grits

By Function

- Texturization

- Emulsification

- Gelation

- Water-Holding

- Adhesion

- Film Forming

- Blending

By Source

- Peas

- Lentils

- Chickpeas

- Beans

By Application

- Food and Beverages

- Bakery and Confectionery Products

- Snacks

- Dairy

- Beverages

- Others

- Feed

- Others

Emerging Trends

Advanced Fractionation Technologies Elevate Pulse Ingredient Purity and Performance

Food ingredient manufacturers actively invest in air classification and wet fractionation technologies to isolate pulse proteins and starches at higher purity levels. These processing advances deliver superior functional performance in plant-based meat and dairy alternatives. India exported legume flour worth $158.016 million and 216.454 million kg in 2024, confirming strong global demand for processed pulse ingredients.

Clean-Label Bakery and Sports Nutrition Drive Pulse Ingredient Adoption

Bakery and confectionery brands increasingly incorporate pulse-based solutions into clean-label product lines, responding to consumer demand for recognizable ingredient lists. Simultaneously, sports nutrition brands adopt pulse proteins in high-protein bars and snacks as sustainable alternatives to whey. Sustainability narratives around pulses’ low carbon footprint and regenerative farming further accelerate adoption across premium food categories.

Drivers

Rising Global Demand for Plant-Based Proteins Accelerates Market Growth

Consumers worldwide increasingly choose plant-based proteins for health, environmental, and ethical reasons. Pulse ingredients deliver superior amino acid profiles and nutritional density, making them ideal for fortified food products. Canada exported dried peas worth $1.097 billion and 2.615 billion kg in 2024, confirming pulses’ status as a critical global feedstock for ingredient processors.

Convenience Food Demand and Supportive Regulations Expand Market Reach

Commercial foodservice operators and convenience food manufacturers proliferate their use of pulse ingredients to meet growing on-the-go consumption trends. Supportive government dietary guidelines actively promote allergen-free and gluten-free alternatives, directly benefiting pulse ingredient adoption. Moreover, regulatory frameworks in North America and Europe provide favorable conditions for pulse-based product innovation and market expansion.

Restraints

Off-Flavor Profiles and Sensory Challenges Limit Mainstream Consumer Acceptance

Pulse ingredients often carry persistent beany off-flavors and gritty textures that reduce palatability in mainstream food products. Food manufacturers invest significantly in deodorization and processing technologies to overcome these sensory challenges. However, fully eliminating off-notes without compromising functional performance remains a technical hurdle that slows broader adoption in premium consumer categories.

Intensifying Competition from Alternative Protein Sources Pressures Market Share

Precision-fermented proteins and algae-based ingredients increasingly compete with pulse derivatives for market share in functional food formulations. These emerging alternatives offer unique functional profiles and can target niche markets with higher price tolerance. Consequently, pulse ingredient producers face pressure to differentiate on cost, sustainability credentials, and supply chain reliability to retain their competitive positioning.

Growth Factors

Functional Food and Nutraceutical Demand Opens New Pulse Ingredient Channels

Pulse fibers and proteins find growing demand in digestive health-focused functional foods and nutraceutical applications. BENEO invested approximately €50 million in 2025 to build a new pulse-processing plant in Germany, creating up to 25 new jobs. This investment signals strong industry confidence in long-term demand for pharmaceutical-grade pulse ingredient production.

Premium Pet Food and Emerging Markets Expand Revenue Opportunities

Premium pet food and livestock feed formulations represent significant expansion opportunities for pulse ingredient processors. Pet food brands seek high-quality plant proteins to meet premiumization trends in the animal nutrition segment. Additionally, geographic diversification into Asia-Pacific markets, particularly for chickpea derivatives, opens new revenue streams for global pulse ingredient manufacturers.

Regional Analysis

North America Dominates the Pulse Ingredient Market with a Market Share of 43.6%, Valued at USD 10.1 Billion

North America leads the global pulse ingredient market, capturing a 43.6% share valued at USD 10.1 billion in 2025. The region benefits from a well-established pulse supply chain, particularly in Canada, which accounts for a major share of global pea production and exports. Strong consumer demand for plant-based proteins and clean-label products further strengthens North America’s dominant market position.

Asia Pacific emerges as the fastest-growing regional market for pulse ingredients, driven by expanding middle-class populations and rising health consciousness. India, the world’s largest pulse producer, plays a dual role as both a raw material supplier and a growing domestic consumer market. Additionally, China and Southeast Asian markets show increasing interest in pulse-based protein ingredients for processed food applications.

The Middle East and Africa region presents a growing demand for pulse ingredients, driven by food security initiatives and population growth. Governments across the GCC invest in food diversification programs that create procurement opportunities for pulse-based ingredients. Moreover, Africa’s expanding food processing sector and increasing urban consumption patterns support the gradual adoption of pulse flour and protein ingredients.

Latin America shows steady growth in pulse ingredient demand, supported by Brazil and Mexico’s large food processing industries. The region benefits from domestic pulse production and a cultural tradition of bean and lentil consumption. Consequently, Latin American food manufacturers increasingly explore pulse ingredient applications in value-added convenience foods targeting growing urban consumer segments.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ingredion Inc. operates as one of the largest specialty ingredient companies globally, with a strong focus on plant-based and pulse-derived solutions. The company reflects its broad commercial scale. Its Texture and Healthful Solutions segment specifically targets pulse protein and starch applications for food manufacturers seeking functional, clean-label ingredient alternatives.

Cargill Inc. delivers pulse ingredient solutions through its extensive global agricultural supply chain and ingredient processing infrastructure. The company integrates pea and lentil derivatives into its plant-based protein portfolio, serving customers across food, feed, and industrial segments. Cargill’s investment in sustainable sourcing and traceability programs positions it strongly as demand for responsibly produced pulse ingredients continues to rise.

Roquette Frères holds a leading position in the global pulse protein market, particularly in pea protein isolates and concentrates used in plant-based food applications. The company operates large-scale processing facilities in Europe and North America dedicated to pulse fractionation and ingredient refinement. Roquette’s strong research and development capabilities allow it to deliver customized pulse ingredient solutions to food and nutrition manufacturers.

Emsland Group specializes in starch and protein derivatives from potatoes and pulses, supplying food manufacturers across Europe and international markets. The company produces pulse flours and pulse starches with precise functional profiles suited to bakery, snack, and convenience food formulations. Moreover, Emsland Group’s focus on processing innovation and quality control strengthens its competitive position within the European pulse ingredient landscape.

Top Key Players in the Market

- Ingredion Inc.

- Cargill Inc.

- Roquette Frères

- Emsland Group

- ADM

- The Scoular Company

- Coscura

- Puris

- Axiom Foods, Inc.

- AGT Food and Ingredients

- AM Nutrition

Recent Developments

- In 2025, Cargill Inc. is emphasizing pea protein pairings with native starches and Alberger salts in innovation kitchen developments to meet rising consumer protein demand in snacks and functional foods, enabling texture optimization and sodium reduction.

- In 2025, Emsland Group expanded the Empro pea-protein range with new applications across plant-based and clean-label food segments; developed authentic vegan mozzarella and feta concepts combining modified pea starch and pea proteins for realistic melt, texture, and mouthfeel; and continued progress on the ROxy starch production modernization and expansion project.

Report Scope

Report Features Description Market Value (2025) USD 23.2 Billion Forecast Revenue (2035) USD 39.8 Billion CAGR (2026-2035) 5.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Pulse Flour, Pulse Starch, Pulse Protein, Pulse Fibers and Grits), By Function (Texturization, Emulsification, Gelation, Water-Holding, Adhesion, Film Forming, Blending), By Source (Peas, Lentils, Chickpeas, Beans), By Application (Food and Beverages, Feed, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Ingredion Inc., Cargill Inc., Roquette Frères, Emsland Group, ADM, The Scoular Company, Coscura, Puris, Axiom Foods Inc., AGT Food and Ingredients, AM Nutrition Customization Scope Customization for segments and region/country levels will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Ingredion Inc.

- Cargill Inc.

- Roquette Frères

- Emsland Group

- ADM

- The Scoular Company

- Coscura

- Puris

- Axiom Foods, Inc.

- AGT Food and Ingredients

- AM Nutrition

Our Clients

- 181779

- March 2026