Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Infant Formula

- By Type Analysis

- By Ingredient Analysis

- By Product Type Analysis

- By Form Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

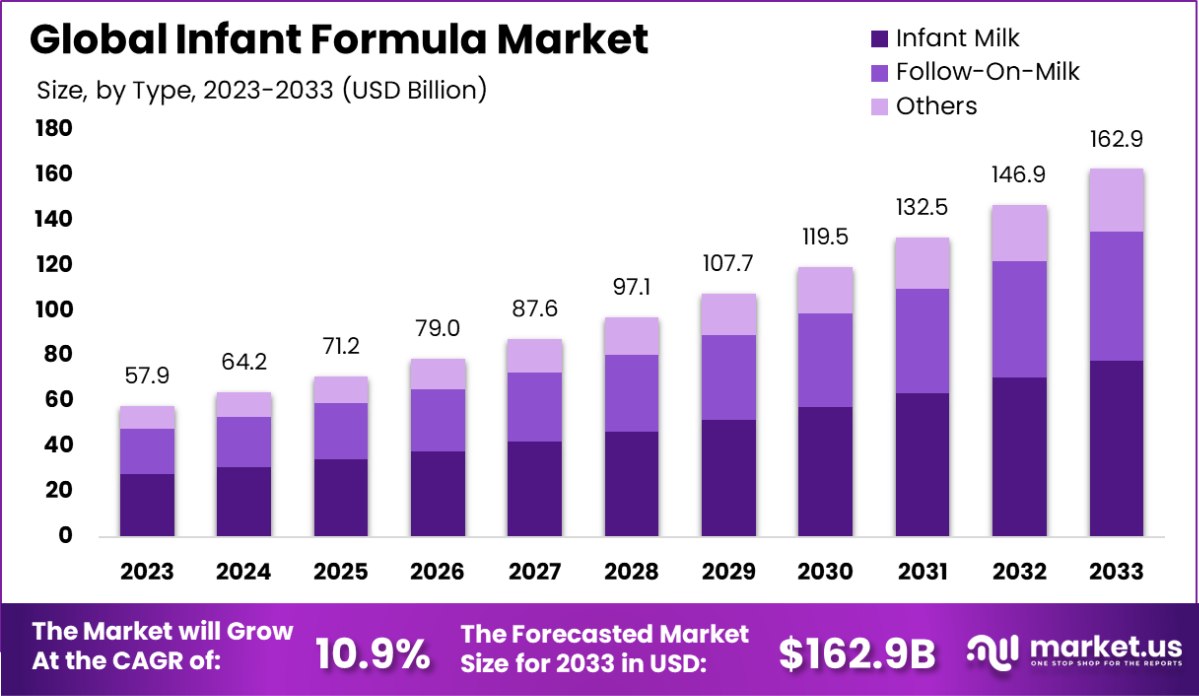

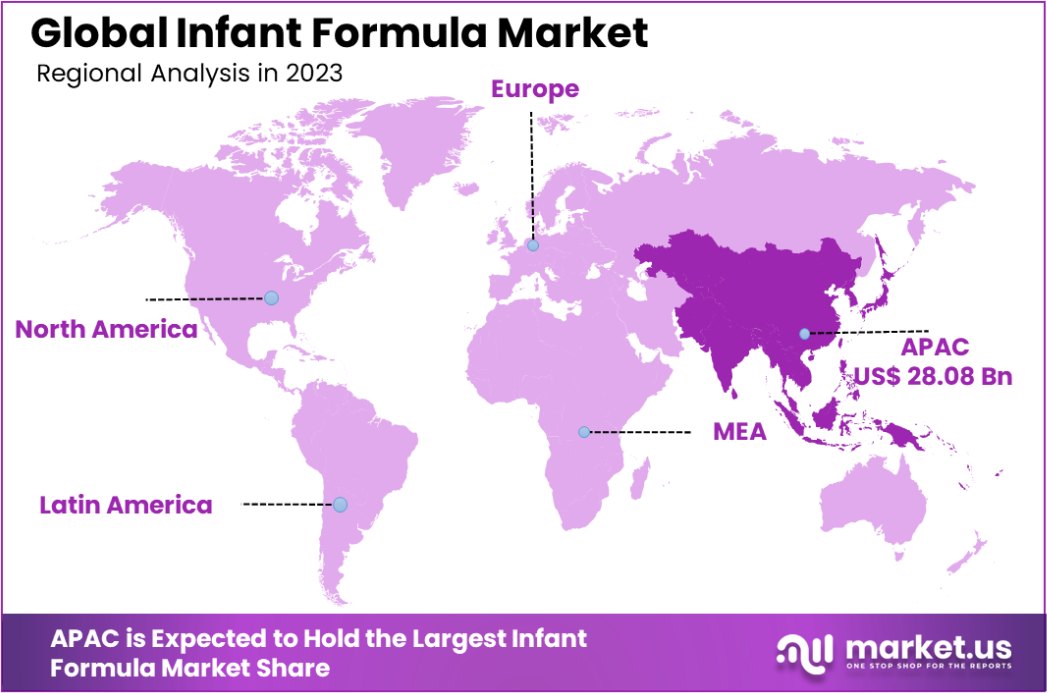

The Global Infant Formula Market is expected to be worth around USD 162.9 Billion by 2033, up from USD 57.9 Billion in 2023, and grow at a CAGR of 10.9% from 2024 to 2033. Asia-Pacific holds 48.2% of the Infant Formula Market, USD 28.08 Bn.

The infant formula market has emerged as a critical segment within the global food and nutrition industry, driven by evolving consumer preferences, increasing working mothers, and rising awareness regarding infant nutrition.

This sector encompasses various product types, including standard milk-based formulas, soy-based variants, and specialized formulations addressing unique dietary requirements.

The infant formula market is characterized by a blend of innovation and regulatory oversight. According to data from the U.S. Food and Drug Administration (FDA), infant formula products are among the most heavily regulated food products, ensuring safety and nutritional adequacy for infants.

Market players are continuously investing in R&D to cater to the diverse nutritional needs of infants while adhering to stringent safety standards. The growing preference for premium and organic formulations has led to a surge in investments in the organic and clean-label categories.

The industry is witnessing a shift toward organic and plant-based formulations, reflecting broader consumer trends toward sustainability and health-consciousness. Innovative product launches with enhanced bioactive ingredients, such as prebiotics, probiotics, and DHA, are gaining traction. The rise of e-commerce platforms has also revolutionized product accessibility, offering convenience and extensive product information to consumers.

The infant formula market is poised for robust growth, underpinned by expanding middle-class populations in emerging economies and increasing government initiatives promoting infant health.

For instance, data from the USDA highlights the significance of fortified formulas in combating malnutrition in developing regions. Technological advancements, such as precision fermentation for human milk oligosaccharides (HMOs), present transformative opportunities for product differentiation.

The U.S. infant formula market presents a nuanced landscape, influenced significantly by socio-economic programs and fluctuating supply dynamics. A pivotal aspect of the market is the interplay between federal nutrition assistance programs and consumer purchasing patterns.

Notably, the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) is a critical driver, with approximately 56% of all infant formula purchases in the U.S. attributed to families enrolled in this program. This underscores the significant role of government subsidies in sustaining demand within the sector.

Moreover, demographic trends provide additional context to market dimensions. As of 2019, the U.S. had about 3.4 million infants under the age of one, more than half of whom were recipients of formula provided through WIC. This statistic highlights the dependency on subsidized nutrition and indicates a substantial, steady market segment reliant on formula products.

Supply chain challenges have also shaped market dynamics, as evidenced by varying availability issues. In the fall of 2022, approximately 34.7% of U.S. households with infants faced difficulties in obtaining infant formula, a situation that improved by the summer of 2023, with the figure decreasing to 19.8%.

This improvement suggests a gradual stabilization in the supply chain, likely influenced by both regulatory actions and market adaptations. The resilience and adaptability of the market are crucial for meeting ongoing consumer needs and shaping strategic approaches for stakeholders within this sector.

Key Takeaways

- The Global Infant Formula Market is expected to be worth around USD 162.9 Billion by 2033, up from USD 57.9 Billion in 2023, and grow at a CAGR of 10.9% from 2024 to 2033.

- Infant milk dominates the type segment, holding a significant 48.1% share of the infant formula market.

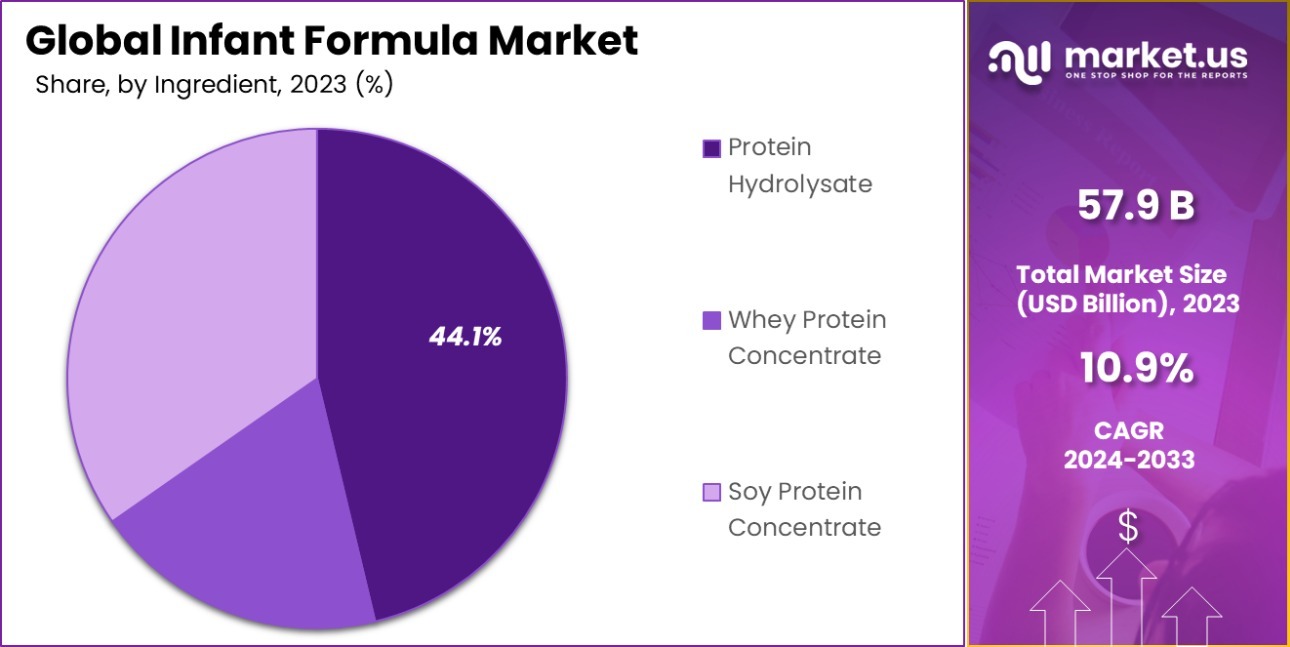

- Protein hydrolysate is a leading ingredient in infant formulas, accounting for 44.1% of the market.

- Special milk products represent 37.1% of the product type segment in the infant formula industry.

- Powdered infant formula is the most common form, comprising 67.1% of the market.

- Hypermarkets and supermarkets are the primary distribution channels, with a 48.1% market share.

- In 2023, Asia-Pacific held 48.2% of the Infant Formula Market, valued at USD 28.08 billion.

Business Benefits of Infant Formula

The business benefits of infant formula are multifaceted and significantly supported by government programs, particularly within the United States. The Women, Infants, and Children (WIC) program plays a crucial role by ensuring access to infant formula for eligible families, which supports the growth and development of infants.

This program not only provides vital nutritional support but also stabilizes demand for infant formula products by establishing a consistent customer base through state agency contracts with formula manufacturers.

Furthermore, economic reports suggest that large buyers like WIC can exert market power to negotiate lower prices, which can influence pricing strategies across the entire market.

Manufacturers may sell infant formula at lower prices within the WIC market to secure contracts, hoping to offset these lower margins with higher-volume sales in the non-WIC market. This strategy can lead to increased shelf space for these brands in retail settings, potentially boosting overall sales

By Type Analysis

Infant milk dominates the market by type, holding a substantial 48.1% share.

In 2023, Infant Milk held a dominant market position in the “By Type” segment of the Infant Formula Market, with a 48.1% share. This segment, primarily consisting of initial-stage formulas designed for newborns to six-month-old infants, continues to capture the largest slice of the market due to its essential role in infant nutrition, particularly for mothers who are unable to breastfeed or choose not to.

The prominence of Infant Milk is attributed to its formulation, which closely mimics human breast milk, thereby making it a preferred choice for early infant nutrition.

Following Infant Milk, the Follow-On-Milk segment, designed for infants aged six months to one year, also represents a significant portion of the market. These formulas are tailored to complement the introduction of solid foods, helping to meet the nutritional requirements of growing babies. As infants transition to more diverse diets, Follow-On-Milk includes additional nutrients necessary to support this critical stage of development.

Together, these segments highlight the diverse needs addressed by the Infant Formula market, catering to different stages of infant growth and dietary requirements. The strategic focus on segmented marketing and product development by leading companies helps in addressing the specific needs of each age group, thereby driving the overall market growth.

By Ingredient Analysis

Protein hydrolysate is a major ingredient, comprising 44.1% of the formula market.

In 2023, Protein Hydrolysate held a dominant market position in the “By Ingredient” segment of the Infant Formula Market, with a 44.1% share. This ingredient is highly valued for its hypoallergenic properties, making it ideal for infants with allergies or sensitivities to cow’s milk protein.

Protein Hydrolysate formulas are processed to break down proteins into smaller sizes, significantly reducing the risk of immune reactions and aiding in easier digestion for infants.

Following Protein Hydrolysate, Whey Protein Concentrate and Soy Protein Concentrate are also significant contributors to the market. Whey Protein Concentrate is favored for its high nutritional value and digestibility, closely resembling the protein balance found in natural breast milk, thus supporting optimal growth and development in infants.

Meanwhile, organic Soy Protein Concentrate offers a viable alternative for infants who are lactose intolerant or need to avoid dairy due to dietary restrictions or allergies, marking its importance in the market.

Together, these ingredients underline the market’s adaptability and responsiveness to the diverse nutritional needs and health concerns of infants. Manufacturers are continuously innovating in this space, developing specialized formulas that cater to the specific health requirements of infants, thereby driving consumer preference and market growth within each sub-segment.

By Product Type Analysis

Special milk products account for 37.1% of the market by product type.

In 2023, Special Milk held a dominant market position in the “By Product Type” segment of the Infant Formula Market, with a 37.1% share. This segment caters specifically to infants with particular dietary needs, including allergies, lactose intolerance, and other digestive or metabolic issues. The high demand for Special Milk reflects the growing awareness and diagnosis of infant health conditions that require specialized nutritional formulations.

Following Special Milk, Toddler’s Milk, Follow-On-Milk, and Starting Milk also hold significant positions within the market. Toddler’s Milk, designed for children aged one to three years, supports the transition from infant formula to solid foods, providing necessary nutrients during this critical growth phase.

Follow-On-Milk, suitable for babies six months to one year, complements the introduction of solids, ensuring balanced nutrition. Starting Milk, intended for newborns up to six months, is formulated to closely mimic breast milk, offering an essential option for feeding infants during the early months.

This segmentation allows manufacturers to address the nuanced nutritional requirements across different developmental stages of children, enhancing parental confidence in product offerings and fueling market growth. The tailored approach in each sub-category underlines the market’s commitment to supporting child health from infancy through toddlerhood.

By Form Analysis

Powdered formulas lead by form, capturing a dominant 67.1% market share.

In 2023, Powder held a dominant market position in the “By Form” segment of the Infant Formula Market, with a 67.1% share. Powdered infant formulas are favored for their cost-effectiveness and long shelf life, making them a practical choice for families worldwide.

Their ease of storage and transport also adds to their popularity, particularly in regions where access to immediate resources may be limited. This form requires mixing with water before feeding, allowing parents to control the consistency and amount, which can be adjusted based on the infant’s age and dietary needs.

Following Powder, the market segments of Liquid and Ready Feed formulas also maintain substantial shares. Liquid formulas offer convenience as they are pre-mixed and require no preparation, ideal for on-the-go feeding. Ready to Feed options, while similar in convenience to liquid formulas, come in smaller, single-serve packages which are perfect for travel or in situations where measuring and mixing are not feasible.

These different forms cater to the varied lifestyles and preferences of consumers, ensuring that there are options suitable for every need. The powder segment, however, continues to lead due to its versatility and economic benefits, resonating with a broad consumer base looking for reliable, accessible infant nutrition solutions.

By Distribution Channel Analysis

Hypermarkets and supermarkets are key channels, distributing 48.1% of infant formulas.

In 2023, Hypermarkets and Supermarkets held a dominant market position in the “By Distribution Channel” segment of the Infant Formula Market, with a 48.1% share. This channel’s strength lies in its widespread accessibility and the ability to offer a broad range of infant formula brands and types under one roof, providing convenience and choice to consumers.

Hypermarkets and supermarkets also benefit from high consumer foot traffic and the ability to provide competitive pricing through economies of scale, which makes them a preferred shopping destination for family-centric purchases like infant formula.

Following closely, Pharmacy and Medical Stores and Specialty Stores also play crucial roles in the distribution landscape. Pharmacies and medical stores are trusted for their provision of health-related products and advice, making them a key channel for consumers seeking specialized infant formulas tailored to specific health needs.

Specialty stores, on the other hand, cater to niche markets and often offer higher-end, specialized products not typically found in larger retail outlets.

The segmentation of these distribution channels highlights the diverse consumer purchasing behaviors and the need for manufacturers to tailor their distribution strategies accordingly. By leveraging the strengths of each channel, brands can optimize their market reach and meet the varied preferences and needs of their customer base.

Key Market Segments

By Type

- Infant Milk

- Follow-On-Milk

- Others

By Ingredient

- Protein Hydrolysate

- Whey Protein Concentrate

- Soy Protein Concentrate

By Product Type

- Special Milk

- Toddlers Milk

- Follow-On-Milk

- Starting Milk

By Form

- Liquid

- Powder

- Ready to Feed

By Distribution Channel

- Hypermarkets and Supermarkets

- Pharmacy/Medical Stores

- Specialty Stores

- Others

Driving Factors

Increasing Demand for Convenient Feeding Solutions

The global rise in dual-income households has escalated the demand for convenient feeding solutions, making infant formula an appealing option for working parents. This trend is driven by the need for efficient, time-saving products that support active lifestyles.

Infant formula provides a reliable and nutritious alternative to breast milk, suitable for on-the-go feeding without the preparation time required for other infant foods. As more parents seek practical feeding options that do not compromise nutritional value, the market for infant formula is expected to continue expanding.

Growth in Awareness of Infant Nutrition

There is a growing awareness among parents about the critical role of nutrition in an infant’s development. This heightened consciousness is supported by widespread educational campaigns by health organizations and formula manufacturers, which emphasize the benefits of fortified infant formulas that include essential vitamins and minerals similar to those found in breast milk.

As a result, parents are increasingly opting for commercially prepared infant formulas to ensure their infants receive adequate nutrition during the crucial early stages of life, driving market growth.

Rise in Population of Infants Globally

The global increase in the infant population directly correlates with the demand for infant formula. With birth rates stabilizing or growing in many parts of the world, particularly in emerging economies, there is a significant need for infant nutritional products.

This demographic factor ensures a steady consumer base for infant formula, as more parents seek out reliable and nutritionally complete feeding options for their children. This demographic trend is a fundamental driver behind the sustained growth of the infant formula market.

Restraining Factors

Regulatory Challenges in Infant Formula Production

Infant formula is subject to stringent regulatory standards globally, aimed at ensuring safety and nutritional adequacy for infants. These regulations can be a significant barrier to entry for new manufacturers and can delay the introduction of new products in the market.

Compliance with these standards requires substantial investment in research, development, and quality assurance, which can limit the speed and scalability of production. These regulatory hurdles not only increase production costs but also impact the overall agility of companies to respond to market demands and innovate freely.

High Cost of Premium Infant Formulas

The high cost associated with premium infant formulas can be a significant restraint in the market, particularly in lower-income regions. These formulas are often enhanced with additional nutrients and organic ingredients, which drive up the price.

For many families, the expense is prohibitive, making these premium options less accessible to a broader audience. This economic factor limits market penetration and growth, especially in economically disadvantaged segments, where consumers might opt for less expensive alternatives that do not offer the same quality or nutritional benefits.

Breastfeeding Initiatives Reducing Formula Demand

Global health organizations and governments actively promote breastfeeding as the best source of nutrition for infants, which can restrain the demand for infant formula. Breastfeeding campaigns emphasize the health benefits such as immune support and mother-child bonding, which formula cannot replicate.

These initiatives can sway public perception, leading to a preference for breastfeeding over formula feeding, particularly among new mothers. As a result, these advocacy efforts can significantly impact the market share of infant formula by reducing its adoption among the target demographic.

Growth Opportunity

Expansion into Emerging Markets Boosts Formula Sales

Emerging markets present significant growth opportunities for the infant formula industry due to rising urbanization and increasing female workforce participation. These factors contribute to a growing demand for convenient and nutritious feeding options, such as infant formula.

By entering these markets, manufacturers can tap into a new consumer base looking for quality and convenience in infant nutrition. Strategic investments in these regions, coupled with localized marketing efforts, can help brands establish a strong presence and meet the specific needs and preferences of consumers in diverse economic landscapes.

Innovations in Formula Composition and Variety

There is a growing opportunity for innovation in the composition and variety of infant formulas to meet evolving consumer preferences and dietary needs. This includes the development of formulas that cater to specific health concerns like allergies, digestion problems, or nutritional deficiencies.

Additionally, incorporating organic and non-GMO ingredients can appeal to health-conscious parents seeking the safest and most natural options for their infants. By continuously innovating and expanding their product lines, companies can differentiate themselves in a competitive market and cater to a broader range of consumer needs.

Leveraging E-commerce for Direct-to-Consumer Sales

The rise of e-commerce platforms offers a lucrative opportunity for infant formula manufacturers to reach consumers directly. This channel allows for broader distribution, particularly in areas where traditional retail presence is limited. Additionally, online sales enable manufacturers to engage directly with consumers, providing tailored information and better-managing consumer relations.

This direct engagement can enhance brand loyalty and customer satisfaction. As more consumers turn to online shopping for convenience, leveraging e-commerce can significantly increase market reach and sales volumes for infant formula products.

Latest Trends

Rise of Organic and Natural Ingredient Infant Formulas

There’s a growing trend towards organic and natural ingredient infant formulas, reflecting broader consumer preferences for healthier, more sustainable products. Parents are increasingly seeking out formulas that are free from synthetic additives and pesticides, driven by concerns about the potential impact of chemicals on infant health.

This shift is influencing manufacturers to develop and market a range of organic options that comply with strict organic standards, offering transparency in ingredient sourcing and production practices. As demand continues, this trend is reshaping the competitive landscape, compelling more brands to prioritize organic certifications and clean labels.

Increased Focus on Specialized Formulas

The infant formula market is witnessing an increased focus on specialized products designed to address specific health issues such as colic, allergies, lactose intolerance, and reflux. These specialized formulas often include hydrolyzed proteins, probiotics, and other additives that help alleviate symptoms and support overall health.

This trend is driven by a growing body of research and greater awareness among parents about these health issues. As a result, the segment for specialized formulas is expanding rapidly, offering growth opportunities for brands that can innovate and effectively market these differentiated products.

Technological Advancements in Product Development

Technological advancements are playing a crucial role in the development of new and improved infant formulas. Modern biotechnology and food science are enabling manufacturers to replicate human milk more closely than ever before.

Innovations such as structurally modified fats and prebiotic fiber mimic the composition and functional benefits of breast milk, enhancing the nutritional profile of infant formulas. These advancements not only improve the quality and appeal of formula products but also boost consumer confidence in formula feeding as a viable alternative to breastfeeding, fostering growth in the market.

Regional Analysis

In 2023, the Asia-Pacific infant formula market held a 48.2% share, valued at USD 28.08 billion.

The global Infant Formula Market is characterized by its significant regional diversity, with Asia-Pacific, North America, Europe, Middle East & Africa, and Latin America each displaying unique consumer behaviors and market dynamics.

Dominating the global landscape, Asia-Pacific commands a hefty 48.2% market share, amounting to USD 28.08 billion. This dominance is driven by high birth rates and increasing female workforce participation, which elevate the demand for convenient and nutritious feeding options.

In contrast, North America and Europe maintain robust markets, supported by advanced healthcare systems and high consumer awareness regarding infant nutrition. These regions focus on innovative, specialized formulas that cater to specific dietary needs and health concerns, reflecting more mature markets with stringent regulatory standards and high consumer expectations.

The Middle East & Africa and Latin America, though smaller in market size, are rapidly emerging as significant growth areas due to urbanization and the gradual increase in disposable incomes.

These regions exhibit a rising demand for premium and specialized infant formula products, although market penetration is still in the early stages compared to the dominating regions. As these markets develop, there is a considerable opportunity for expansion, driven by an increasing awareness of and demand for high-quality infant nutrition products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Infant Formula Market continues to be shaped by the activities of key players, each contributing uniquely to the industry’s dynamics and competitive landscape. Companies like Nestlé S.A., Danone S.A., and Abbott Laboratories lead with extensive product portfolios, advanced R&D capabilities, and strong global distribution networks.

Nestlé and Danone, in particular, leverage their vast experience in nutrition science to innovate and expand their specialized formula offerings, appealing to health-conscious consumers seeking formulas that mimic breast milk closely or address specific dietary needs.

Emerging players like Ausnutria Dairy Corporation Ltd. and Beingmate Group have been instrumental in capitalizing on the rapid market growth in Asia-Pacific, introducing products tailored to regional dietary preferences and regulatory requirements. Their growth is supported by increasing urbanization and consumer purchasing power, particularly in China and Southeast Asia.

Companies such as Arla Foods and Friesland Campina are strengthening their positions by focusing on sustainability and the organic segment, resonating with European and North American consumers who prioritize environmental impact and product naturalness.

The U.S.-based firms such as Mead Johnson Nutrition and The Kraft Heinz Company remain pivotal in the North American market, driven by innovation in product functionality and marketing strategies that emphasize nutritional benefits and child development.

Moreover, specialty and organic-focused companies like Bellamy’s Organic and Hain Celestial Group are gaining traction by catering to niche markets that demand organic, non-GMO ingredients, tapping into a growing segment of consumers looking for clean-label products.

Top Key Players in the Market

- Abbott Laboratories

- Arla Foods

- Ausnutria Dairy Corporation Ltd.

- Beingmate Group

- Bellamy’s Organic

- Danone S.A.

- Friesland Campina

- Hain Celestial Group

- HIPP

- Mead Johnson Nutrition

- Meiji Holdings Co. Ltd.

- Nestle S.A.

- Perrigo Company plc

- Pfizer

- Reckitt Benckiser Group PLC

- Synutra International

- The Kraft Heinz Company

- Yili Group

Recent Developments

- In 2023, Abbott Laboratories focused on innovation and supply recovery in the infant formula market, notably resuming specialty formula production and enhancing product offerings with 2′-FL HMO in Similac formulas, mimicking the benefits of breast milk.

- In 2023, Arla Foods enhanced its infant formula sector by investing in high-quality production facilities in Denmark and Argentina, doubling whey permeate capacity and initiating infant formula-grade protein production. Arla focuses on organic, sustainable products like Baby&Me, using certified organic milk.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 57.9 Billion |

| Forecast Revenue (2033) | USD 162.9 Billion |

| CAGR (2024-2033) | 10.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Infant Milk, Follow-On-Milk, Others), By Ingredient (Protein Hydrolysate, Whey Protein Concentrate, Soy Protein Concentrate), By Product Type (Special Milk, Toddlers Milk, Follow-On-Milk, Starting Milk), By Form (Liquid, Powder, Ready to Feed), By Distribution Channel (Hypermarkets and Supermarkets, Pharmacy/Medical Stores, Specialty Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Abbott Laboratories, Arla Foods, Ausnutria Dairy Corporation Ltd., Beingmate Group, Bellamy’s Organic, Danone S.A. , Friesland Campina, Hain Celestial Group, HIPP, Mead Johnson Nutrition, Meiji Holdings Co. Ltd., Nestle S.A., Perrigo Company plc, Pfizer, Reckitt Benckiser Group PLC, Synutra International, The Kraft Heinz Company, Yili Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |