Quick Navigation

Report Overview

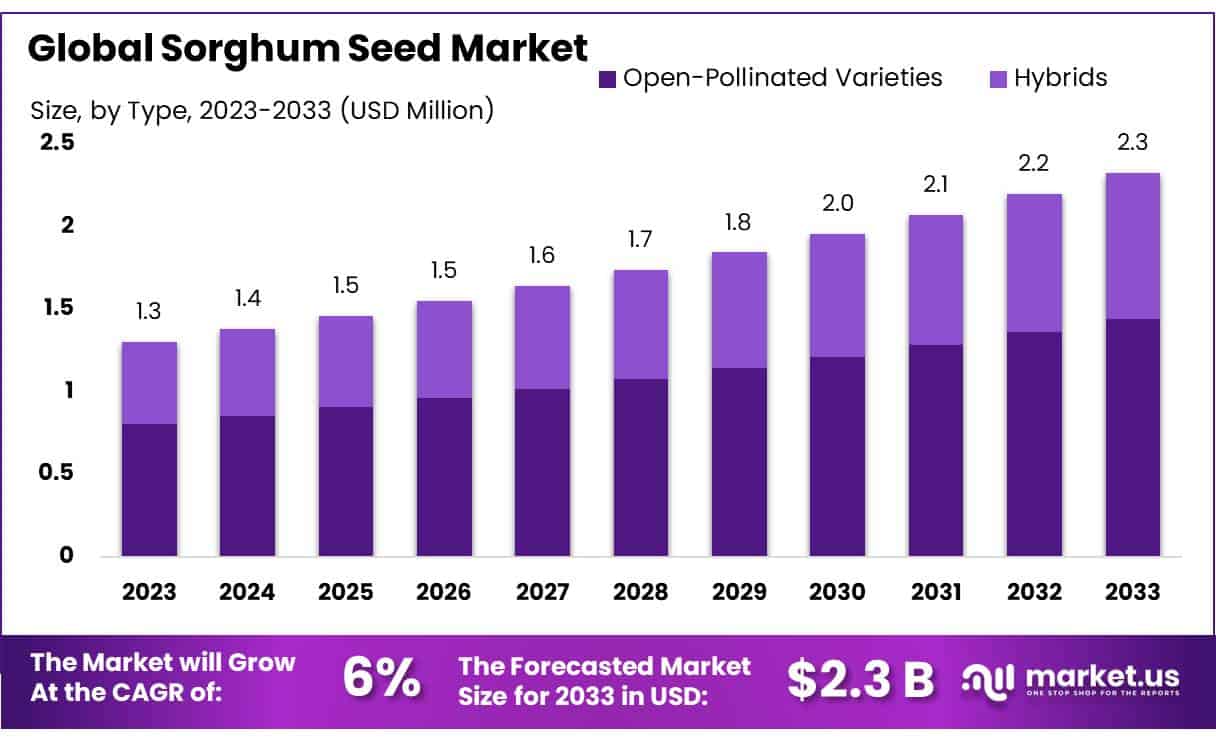

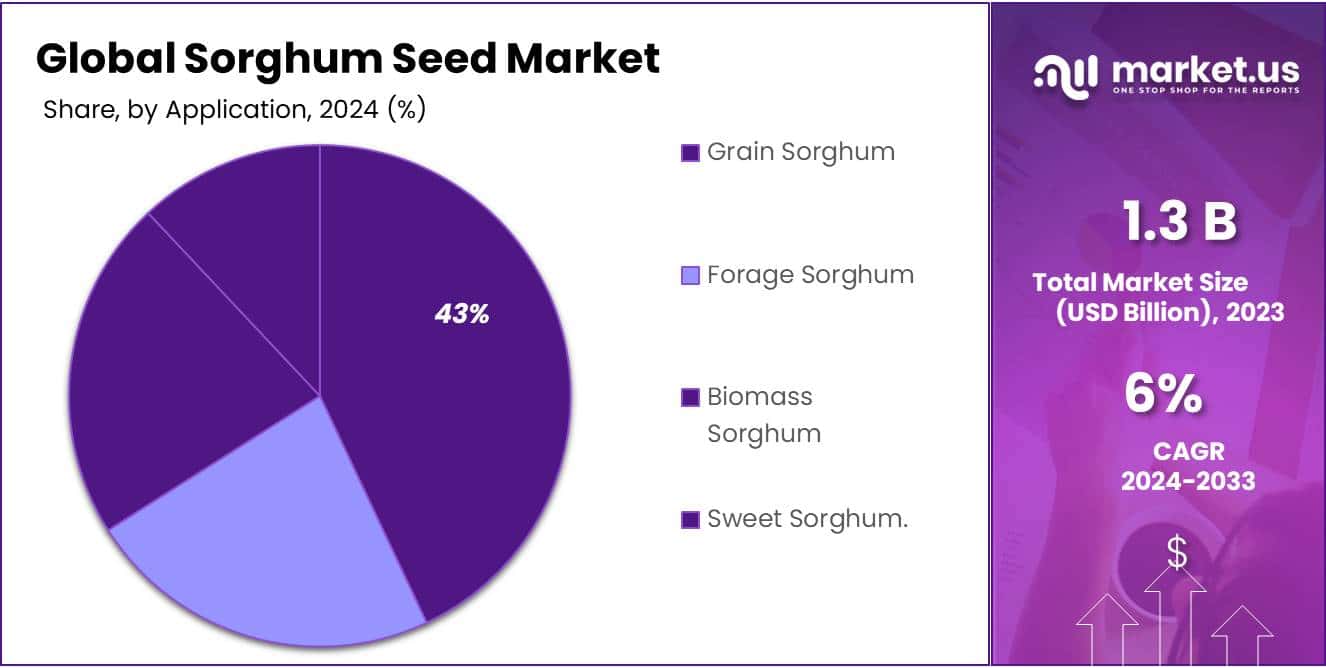

The Global Sorghum Seed Market size is expected to be worth around USD 2.3 Bn by 2033, from USD 1.3 Bn in 2023, growing at a CAGR of 6.0% during the forecast period from 2024 to 2033.

Sorghum seeds, derived from the sorghum plant native to Africa, are a crucial agricultural commodity with diverse applications across human consumption, livestock feed, and biofuel production. Sorghum’s drought resistance and adaptability to arid regions have made it a valuable crop globally.

In 2021, global sorghum production reached approximately 59 million tonnes, underscoring its significance, particularly in semi-arid areas where water scarcity is a concern. The United States is one of the leading producers, with exports of around 6.3 million metric tons during the 2021/2022 marketing year, primarily to China, which accounts for over 90% of U.S. sorghum exports.

The sorghum industry has seen substantial investments, particularly in the development of more resilient varieties. For instance, a major agricultural company invested over USD 200 million in 2020 to develop genetically enhanced sorghum seeds with improved drought resistance and higher yields.

This investment reflects the growing focus on enhancing the crop’s productivity, which is vital for ensuring food security in regions prone to drought and climate change impacts.

Government policies and initiatives have further supported the sorghum sector. In India, for example, farmers are encouraged to adopt improved seed varieties with a 50% subsidy on certified seeds, promoting sustainable agricultural practices.

Additionally, global sorghum seed trade remains strong, with 2,142 shipments recorded between March 2023 and February 2024. Key exporters include India (39% market share), the U.S. (35%), and Argentina (8%).

The demand for sorghum seeds is also evident in major importing countries such as Bangladesh, which led with 2,268 shipments, followed by Pakistan and Mexico. This robust trade and growing investments indicate the increasing global reliance on sorghum for food, feed, and fuel production.

Key Takeaways

- Sorghum Seed Market size is expected to be worth around USD 2.3 Bn by 2033, from USD 1.3 Bn in 2023, growing at a CAGR of 6.0%.

- Hybrids held a dominant market position, capturing more than a 62.3% share in the sorghum seed market.

- Grain Sorghum held a dominant market position, capturing more than a 43.2% share.

- Grain Gram Flour held a dominant market position, capturing more than an 18.5% share.

- Animal Feed held a dominant market position, capturing more than a 39.1% share.

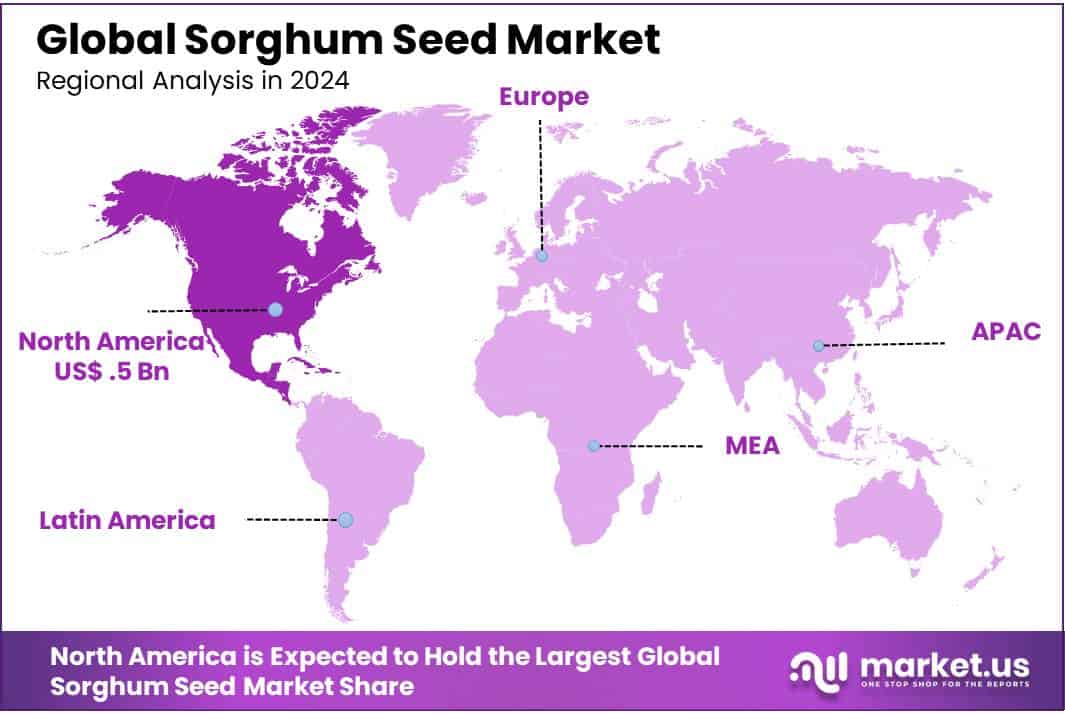

- North America dominated the global sorghum seed market, capturing a significant share of 43.3%

By Type

In 2023, hybrids held a dominant market position, capturing more than a 62.3% share in the sorghum seed market. This segment benefits from hybrid seeds’ enhanced traits, such as improved yield, drought tolerance, and disease resistance, which are highly valued by farmers seeking to maximize productivity and profitability.

Hybrid sorghum varieties are particularly favored in intensive farming operations where technological adoption is high, and the return on investment in improved seed varieties can be significant.

On the other hand, open-pollinated varieties also play a crucial role in the sorghum seed market. These varieties are often preferred by smallholder farmers, especially in developing regions where access to advanced agricultural inputs is limited.

Open-pollinated sorghum seeds are less expensive and can be saved from year to year, reducing the farmers’ dependency on seed companies. Although they generally offer lower yields compared to hybrids, their adaptability to local conditions and lower input requirements make them a sustainable option for resource-constrained environments.

By Product Type

In 2023, Grain Sorghum held a dominant market position, capturing more than a 43.2% share. This segment is primarily driven by the use of grain sorghum in food products for both humans and animals due to its nutritional benefits and gluten-free properties. Grain sorghum is also increasingly used in the production of alcoholic beverages, which has bolstered its market presence.

Forage Sorghum is another significant segment, valued for its use in animal feed. Its fast growth and high biomass yield make it ideal for forage or silage, particularly in regions where water scarcity limits the cultivation of more water-intensive crops. This type has been essential for livestock farmers, especially during dry seasons.

Biomass Sorghum has been gaining traction due to its application in bioenergy production. Its ability to produce a large amount of biomass with minimal input makes it a sustainable choice for biofuel production, contributing to renewable energy initiatives.

Sweet Sorghum, known for its high sugar content, is primarily used for syrup production but is also being explored for ethanol production. Its versatility and the growing interest in renewable energy sources have seen this segment gradually expand in the market.

By Application

In 2023, Grain Gram Flour held a dominant market position, capturing more than an 18.5% share. This segment benefits from the rising popularity of gluten-free and health-conscious diets, as sorghum flour is an excellent alternative to wheat flour. It’s widely used in baking and as a thickening agent in various cuisines, enhancing its market penetration.

Popped sorghum is another appealing segment, particularly as a snack option. It is similar to popcorn but smaller in size and with a nuttier flavor. This segment is growing due to increasing demand for healthy, whole-grain snack alternatives.

Sorghum Flakes are gaining traction as a breakfast cereal option, praised for their nutritional value and gluten-free properties. These attributes align well with current consumer trends toward healthier breakfast choices and whole-grain foods.

Sorghum Puffs have also carved out a niche in the healthy snack market, offering a light, airy texture that is appealing to both children and adults. Their ease of incorporation into various snack mixes boosts their appeal.

Chips made from sorghum are emerging as a popular gluten-free snack. Their unique flavor and crunchy texture provide a satisfying alternative to traditional potato chips.

Pasta made from sorghum flour is expanding in the gluten-free pasta market, offering a nutritious and tasty option that holds up well in cooking, similar to traditional pasta.

Sorghum Syrup is utilized in the food industry as a sweetener. Its use in baking and as a syrup for pancakes and waffles is cherished for its natural and mild sweetness.

By End User

In 2023, Animal Feed held a dominant market position, capturing more than a 39.1% share. This segment benefits from sorghum’s nutritional profile, which makes it an excellent feed grain for livestock due to its high protein and fiber content. Its resilience to harsh growing conditions also ensures a reliable supply for feed producers, supporting its strong market presence.

The Food Industry segment also plays a significant role in the sorghum seed market. Sorghum is used extensively in the production of gluten-free flours, cereals, and snack products, catering to the increasing consumer demand for healthy, gluten-free options. This versatility in food applications continues to drive growth in this segment.

Wine Making is another notable segment where sorghum is utilized, particularly in the production of traditional African and Asian spirits and beers. Sorghum’s natural properties impart unique flavors, making it a valued ingredient in niche alcoholic beverages.

Biofuel and Chemical Production is gaining momentum as sorghum proves to be an efficient feedstock for ethanol and bio-based chemicals. This segment is driven by the growing global emphasis on sustainable and renewable energy sources, positioning sorghum as a key component in eco-friendly production processes.

Key Market Segments

By Type

- Open-Pollinated Varieties

- Hybrids

By Product Type

- Grain Sorghum

- Forage Sorghum

- Biomass Sorghum

- Sweet Sorghum

By Application

- Gram Flour

- Popped

- Flake

- Puffs

- Chips

- Pasta

- Syrup

- Others

By End User

- Animal Feed

- Food Industry

- Wine Making

- Biofuel and Chemical Production

- Others

Drivers

Export Demand and Global Market Access

Export demand plays a pivotal role in driving the expansion of the sorghum seed market. Countries in Asia and Europe increasingly seek sorghum due to its versatility in food products, animal feed, and biofuel production.

This global demand is supported by trade agreements that improve market access for sorghum exporters, leading to higher sales and market reach, ultimately benefiting growers and producers with increased profitability.

Rising Demand for Biofuels and Renewable Energy

Sorghum’s use as a feedstock for biofuels significantly influences its market growth. The crop’s high starch content and efficient growth in various climatic conditions make it suitable for bioethanol production.

As the world shifts toward sustainable energy solutions and reduces greenhouse gas emissions, government policies and incentives are increasingly promoting the use of renewable resources like sorghum. This trend not only supports the growth of sorghum cultivation but also its utility in the renewable energy sector, enhancing the overall demand for sorghum seeds.

Government Support and Sustainable Agricultural Practices

Government initiatives such as subsidies for sorghum cultivation and the promotion of sustainable farming practices substantially affect the sorghum seed market.

These government actions include financial incentives, reduced input costs, and support for infrastructure development, which encourage the adoption of sorghum due to its lower environmental impact compared to other crops. Additionally, the focus on developing sorghum varieties with higher yields, pest resistance, and drought tolerance through funded research and development projects further enhances its market attractiveness and cultivation viability

Restraints

Impact on Grower Adoption and Crop Management

The short shelf life of pre-treated sorghum seeds significantly restricts their market expansion. These seeds are treated to reduce insect and pest infestation, which is crucial for maintaining crop health.

However, the treatment results in a rapid decline in seed vigor, complicating storage and handling for growers. This factor challenges the adoption of sorghum cultivation, as growers must use these seeds within a shorter timeframe to ensure optimal germination and crop development.

Agricultural Strategy Limitations

The physical and chemical properties of the formulations used for treating sorghum seeds impact the survival of beneficial microbes, which are essential for plant growth and soil health.

Growers face challenges in implementing beneficial agricultural strategies effectively, such as the restricted use of pesticides, proper application of fertilizers, and crop rotation. These limitations hinder the broader adoption of best practices in sorghum cultivation, affecting overall productivity and sustainability.

Economic and Operational Implications

The requirement for quick use of treated seeds due to their short shelf life imposes additional economic and operational burdens on farmers. They must plan more precisely for sowing times and may face increased costs if seeds are not used within their viability period.

This can lead to financial losses, especially for small-scale farmers who might not have the infrastructure to store seeds under ideal conditions. Consequently, this restraint affects the economic viability of growing sorghum, particularly in regions where resources and infrastructure are limited

Opportunity

Increasing Demand for Biofuels

One of the most significant growth opportunities for the sorghum seed market is its potential use in biofuel production. Sorghum, particularly biomass sorghum, is increasingly seen as a key crop for the production of bioethanol, a renewable energy source. Sorghum’s high cellulose content and efficient growth make it an attractive alternative to other biofuel crops like corn and sugarcane.

According to the U.S. Department of Agriculture (USDA), biomass sorghum is increasingly utilized for bioenergy purposes, especially in regions focusing on sustainable energy production. The U.S. alone produced approximately 59 million tons of sorghum in 2021, with a substantial portion of this being directed towards biofuel production, including a 5-6% contribution to the nation’s total bioethanol production.

With the global push toward reducing carbon emissions and dependence on fossil fuels, biofuels derived from crops like sorghum are gaining momentum. Government incentives and policies aimed at promoting renewable energy, such as the U.S. Renewable Fuel Standard (RFS), are expected to drive growth in the sorghum biofuel market.

In 2022, bioethanol production from sorghum in the U.S. saw a 6% increase compared to previous years, reflecting the growing demand for sorghum as a biofuel feedstock. This trend offers substantial growth potential for sorghum seed producers and bioenergy companies alike.

Government Initiatives and Investment in Renewable Energy

Government support plays a crucial role in unlocking the growth potential for sorghum as a biofuel crop. In many countries, including the U.S. and Brazil, governments are actively promoting the use of biofuels to reduce greenhouse gas emissions and meet energy sustainability targets.

The U.S. Renewable Fuel Standard (RFS) is a prime example of how government policies are encouraging the adoption of sorghum in biofuel production. The RFS mandates that a certain percentage of transportation fuels be derived from renewable sources, including bioethanol, which is often made from sorghum. In 2023, the U.S. federal government set a target to blend 15 billion gallons of ethanol into the nation’s gasoline supply, driving increased demand for sorghum as a bioethanol feedstock.

Additionally, in 2022, the U.S. Department of Energy announced a $30 million investment into research projects aimed at improving biofuel crop yields, including sorghum. This type of government backing is likely to expand the market for sorghum seed producers by encouraging both technological innovation and increased adoption of bioenergy solutions in agriculture.

Similarly, Brazil, one of the largest bioethanol producers, has increased its focus on using sorghum as a biofuel crop, with projections indicating a rise in sorghum bioethanol production by over 5% annually over the next five years.

Shifting Global Focus Towards Sustainable Agriculture

In addition to biofuels, sorghum is well-positioned to benefit from the increasing global emphasis on sustainable and climate-resilient agriculture. Sorghum’s drought resistance and adaptability to marginal soils make it an ideal crop for regions affected by water scarcity and climate variability.

According to the Food and Agriculture Organization (FAO), approximately 60% of sorghum production occurs in semi-arid regions, with Africa and parts of Asia and South America leading global production. This trend is expected to continue as governments and agricultural institutions push for the adoption of crops that can withstand extreme weather conditions and contribute to food security.

For example, in 2022, the Indian government announced a new initiative under its National Food Security Mission to increase the cultivation of drought-resistant crops, including sorghum, to combat the effects of water scarcity.

The Indian government aims to increase sorghum production by 10% over the next decade, driven by the crop’s resilience and growing demand in both food and bioenergy sectors. This alignment with sustainability goals creates significant opportunities for sorghum producers, especially in regions where climate change is predicted to have a greater impact on traditional crop yields.

Trends

Growing Demand for Gluten-Free Products

One of the major trends in the sorghum seed market is the increasing consumer demand for gluten-free products. Sorghum, being naturally gluten-free, has emerged as a key ingredient in various gluten-free foods, such as flour, pasta, snacks, and breakfast cereals. Sorghum, with its high nutritional value, including fiber, antioxidants, and essential minerals, fits well within this market trend.

According to the U.S. Department of Agriculture (USDA), the production of sorghum in the United States reached 59 million tons in 2022, with a notable increase in the volume of sorghum being processed for gluten-free food products.

In recent years, sorghum has become increasingly popular among health-conscious consumers who are avoiding wheat, barley, and rye due to gluten sensitivities or celiac disease. In the U.S. alone, gluten-free food products made from sorghum saw a growth of 10-12% in 2022.

This trend is expected to continue, driven by rising health awareness and the expanding availability of gluten-free sorghum-based food items in supermarkets and restaurants worldwide.

Sustainable Farming Practices and Drought-Resistant Varieties

Sorghum’s role in sustainable farming is another prominent trend. As global agricultural systems face increasing challenges from climate change, sorghum’s drought tolerance and resilience to harsh growing conditions make it a valuable crop for sustainable farming practices.

Sorghum requires less water than traditional cereals like rice or maize, which makes it an ideal crop in regions with water scarcity or unreliable rainfall patterns. According to the Food and Agriculture Organization (FAO), more than 60% of global sorghum production comes from regions that are highly prone to drought, such as Sub-Saharan Africa, India, and the U.S. Great Plains.

In response to these challenges, governments and agricultural research organizations have intensified efforts to develop and promote drought-resistant sorghum varieties. For instance, in 2022, the U.S. Department of Agriculture (USDA) allocated $15 million to research projects focused on enhancing sorghum’s resistance to drought and pests.

In India, the government launched a program to increase sorghum cultivation by 10% over the next five years, emphasizing the crop’s ability to withstand harsh environmental conditions. This trend is expected to expand as farmers increasingly adopt drought-resistant and low-input crops like sorghum to adapt to changing climate conditions.

Adoption of Sorghum in Biofuel Production

Another significant trend is the increasing use of sorghum as a feedstock for biofuels, particularly ethanol. Sorghum is being recognized as a sustainable alternative to corn and sugarcane in biofuel production due to its high energy yield per acre and its ability to grow in arid and semi-arid regions.

The U.S. alone produced around 6.5 million metric tons of sorghum for biofuel in 2022, with a substantial portion being used in ethanol production. The U.S. Renewable Fuel Standard (RFS), which mandates the blending of renewable fuels into transportation fuels, continues to drive demand for bioethanol produced from sorghum.

The government’s focus on increasing biofuel production is evident from the $30 million investment announced by the U.S. Department of Energy in 2022 to support research on improving sorghum as a biofuel crop. This investment is expected to further increase the economic viability of sorghum as a biofuel feedstock, boosting its demand and production in the coming years.

Similarly, Brazil, one of the world’s largest bioethanol producers, has increased its focus on using sorghum for biofuel production, forecasting an annual growth of 5-7% in the use of sorghum for ethanol in the next five years. This trend presents a major growth opportunity for sorghum producers and biofuel companies.

Regional Analysis

In 2023, North America dominated the global sorghum seed market, capturing a significant share of 43.3%, valued at approximately USD 1.5 billion. This dominance can be attributed to the United States, the largest producer and consumer of sorghum, accounting for nearly 50% of global sorghum production.

The U.S. benefits from advanced agricultural technologies, strong government support through initiatives such as the Renewable Fuel Standard (RFS), and a robust biofuel industry, which uses sorghum as a key feedstock for ethanol production. The region’s favorable climate and high adoption of modern farming practices further contribute to the region’s market leadership.

Europe holds a smaller share in the sorghum seed market but continues to experience steady growth, driven by increasing demand for gluten-free products and the rise of sustainable agriculture practices. The adoption of sorghum as a rotational crop and its use in animal feed are particularly gaining traction in countries like Spain and Italy, where it is cultivated as a drought-resistant alternative to maize.

The Asia Pacific region, particularly India and China, is witnessing rapid expansion in sorghum seed adoption. India, with its government-backed initiatives promoting drought-resistant crops, and China, which has a growing need for feed grains, are driving this growth. This region is projected to see a CAGR of 7-8% over the next five years, fueled by rising demand for animal feed and biofuel production.

Middle East & Africa is primarily driven by the demand for drought-tolerant crops in arid regions, while Latin America benefits from growing biofuel production, especially in Brazil, where sorghum is used extensively for ethanol production.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The sorghum seed market is characterized by a competitive landscape with several major players involved in seed production, distribution, and related agricultural solutions. Leading companies such as ADM, Archer Daniels Midland (ADM), and Cargill, Incorporated play a dominant role in the market, leveraging their extensive distribution networks and expertise in crop genetics to drive growth.

These global agribusiness giants not only supply sorghum seeds but also contribute to the biofuel sector, where sorghum is increasingly utilized as a feedstock for ethanol production. Corteva Agriscience and Bayer Cropscience, with their strong focus on agricultural innovation, are also significant players, providing high-quality hybrid sorghum varieties and integrated crop management solutions.

Other important contributors include Advanta Seeds, KWS SAAT SE, and Groupe Limagrain, which specialize in seed breeding, production, and distribution. These companies focus on enhancing sorghum varieties with improved resistance to pests, diseases, and drought, as well as higher yields.

Seed Co Limited, Pannar Pty Ltd, and Seedway, LLC are also notable regional players, with a strong presence in markets such as Africa, India, and the U.S., where sorghum is an important staple for both food and feed. Nu Life Market and Nuseed are focused on developing sorghum for specialty applications, including biofuels and animal feed, contributing to the growing demand for sustainable agriculture practices.

In addition to these key players, organizations like Ernst Conservation Seeds and Welter Seed & Honey Co. provide niche products and services, such as seed conservation and local farming support.

National Sorghum Producers and Mabele Fuels Pty Ltd are also vital in advocating for sorghum cultivation and biofuel production, helping to drive industry initiatives and policy changes. With diverse players covering various aspects of the sorghum seed value chain, the market is poised for continued innovation and growth across global regions.

Top Key Players in the Market

- ADM

- Advanta seeds

- Allied Seed LLC

- American Seed Co.

- Archer Daniels-midland company

- Ardent Mills

- Bayer Cropscience LLC

- Cargill, Incorporated

- Corteva Agriscience

- Ernst Conservation Seeds

- Groupe Limagrain

- KWS SAAT SE

- Mabele fuels pty (Ltd)

- National sorghum producers

- Nu Life Market

- Nufarm (Nuseed)

- Nuseed

- Pannar Pty Ltd

- Richardson seeds, Ltd.

- Seed Co Limited

- Seedway, LLC.

- The Scoular Company

- UPL Limited

- Welter Seed & Honey Co.

Recent Developments

In 2023, ADM’s ethanol production facilities were projected to use approximately 2.5-3 million tons of sorghum for biofuel, which aligns with the company’s broader strategy to increase renewable energy usage.

In 2023, Advanta’s R&D investments, estimated at USD 10-15 million annually, are focused on improving seed genetics for higher productivity and sustainability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.3 Bn |

| Forecast Revenue (2033) | USD 2.3 Bn |

| CAGR (2024-2033) | 6.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Open-Pollinated Varieties, Hybrids), By Product Type (Grain Sorghum, Forage Sorghum, Biomass Sorghum, Sweet Sorghum), By Application (Gram Flour, Popped, Flake, Puffs, Chips, Pasta, Syrup, Others), By End User (Animal Feed, Food Industry, Wine Making, Biofuel and Chemical Production, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ADM, Advanta seeds, Allied Seed LLC, American Seed Co., Archer Daniels-midland company, Ardent Mills, Bayer Cropscience LLC, Cargill, Incorporated, Corteva Agriscience, Ernst Conservation Seeds, Groupe Limagrain, KWS SAAT SE, Mabele fuels pty (Ltd), National sorghum producers, Nu Life Market, Nufarm (Nuseed), Nuseed, Pannar Pty Ltd, Richardson seeds, Ltd., Seed Co Limited, Seedway, LLC., The Scoular Company, UPL Limited, Welter Seed & Honey Co. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |