Quick Navigation

Report Overview

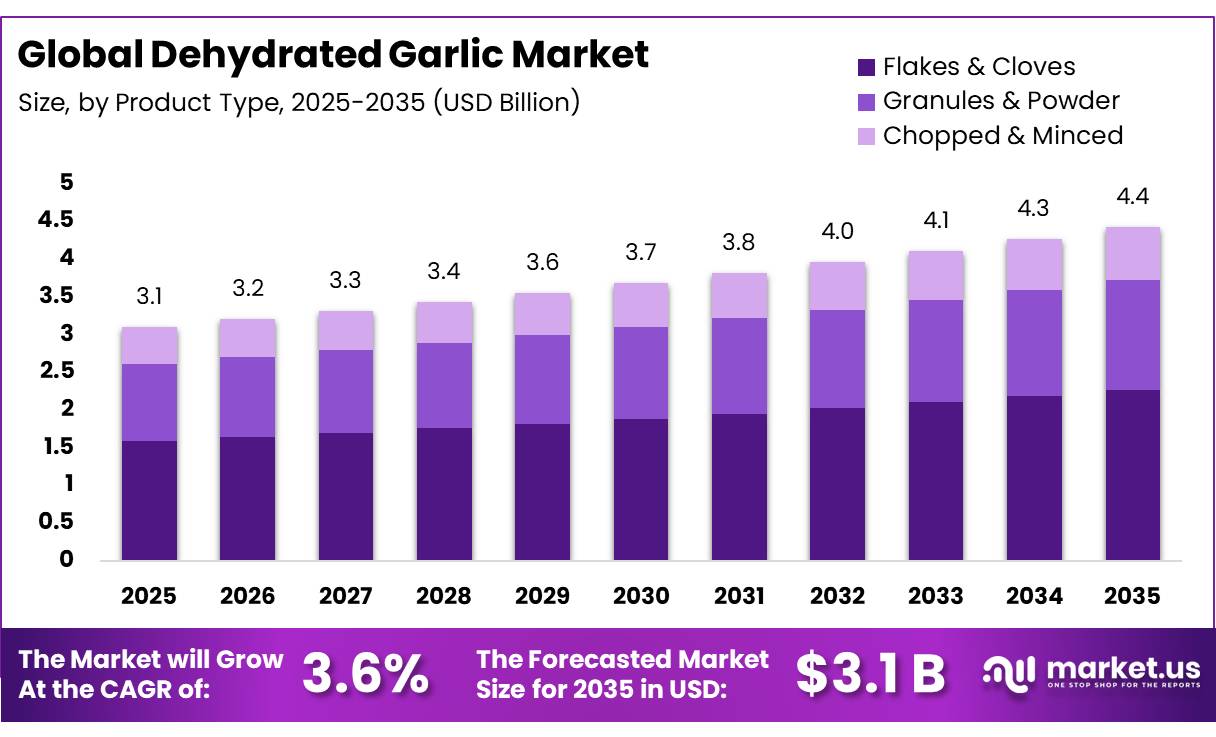

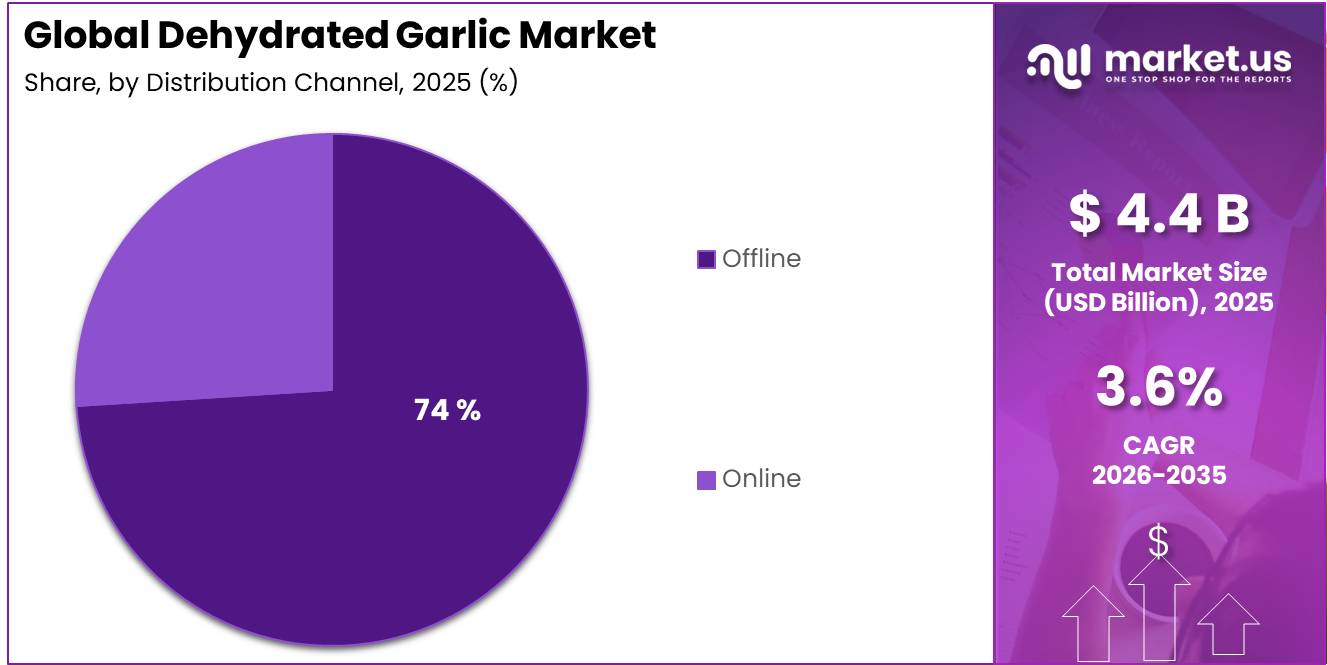

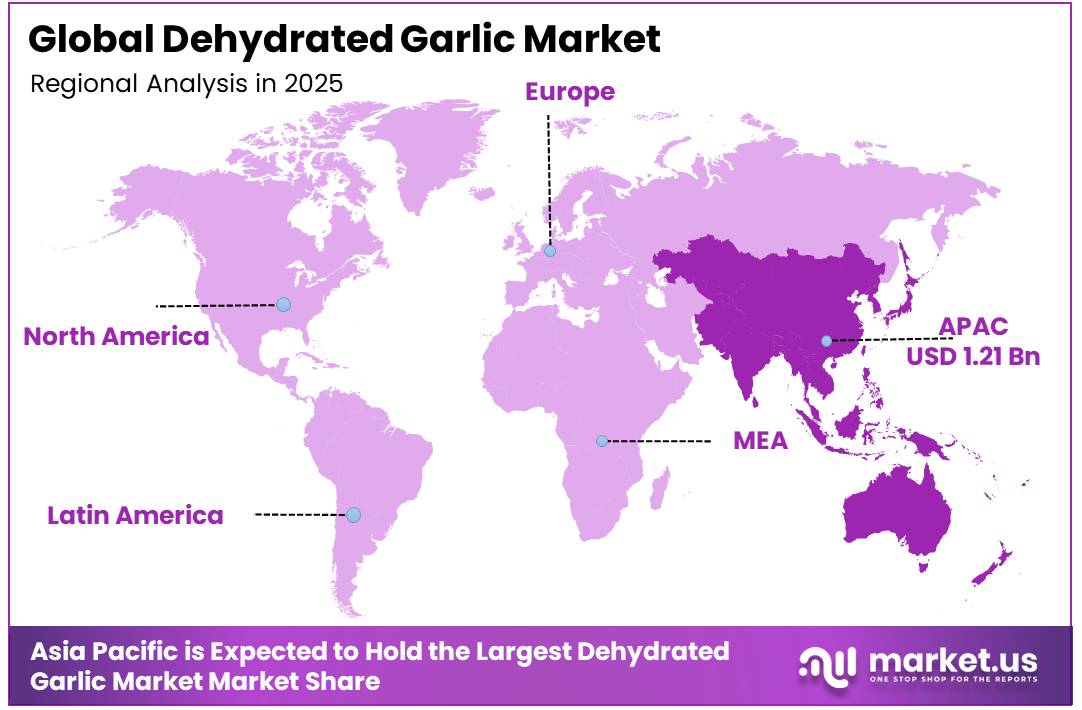

In 2025, the Global Dehydrated Garlic Market was valued at USD 3.1 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 3.6%, reaching about USD 4.4 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 39.10% share, holding USD 1.21 billion in revenue.

The dehydrated garlic industry plays a significant role in the global food ingredients sector by providing a stable, convenient, and cost-effective alternative to fresh garlic for food manufacturers, foodservice operators, and retail consumers. Through dehydration technologies that reduce moisture while preserving flavor compounds, dehydrated garlic is extensively used in seasonings, sauces, soups, bakery products, snacks, processed meats, and ready-to-eat meals.

- According to FAOSTAT, global garlic production reached approximately 7 million metric tons in 2024, demonstrating a strong agricultural base that supports the expanding dehydrated garlic value chain.

Key Takeaways

- The global dehydrated garlic market was valued at USD 3.1 billion in 2025.

- The global dehydrated garlic market is projected to grow at a CAGR of 3.6% and is estimated to reach USD 4.4 billion by 2035.

- On the basis of product type, Flakes & Cloves dominated the market, constituting 51.1% of the total market share.

- Based on the application, B2B dominated the market, accounting for 72.0% of the total market share.

- Based on the distribution channel, Offline led the market, comprising 74.0% of the total market share.

- In 2025, Asia-Pacific was the dominant region in the dehydrated garlic market, accounting for 39.1% of the total global market and representing a market value of approximately USD 1.21 billion

The industrial base remains closely linked to fresh-garlic farming and processing capacity. USDA data released in February 2026 show that the United States harvested 24,900 acres of garlic in 2025, with a yield of 140 hundredweight per acre and utilized production of 3.486 million hundredweight. The crop generated USD 244.6 million in utilized value. Processing absorbed 115,038 tonnes, valued at USD 60.9 million, compared with 135,015 tonnes in 2024, indicating that dehydrators and other processors must manage variable crop availability and input costs.

Demand is supported by expansion in packaged foods and foodservice channels. U.S. food spending reached USD 2.51 trillion in 2025, including USD 1.41 trillion spent on food away from home. USDA’s food-dollar analysis also showed that food processing represented 16.1 cents and foodservice represented 38.6 cents of each dollar spent on domestically produced food in 2024. These large downstream channels favour ingredients that provide standardised taste, long shelf life, compact transport and rapid preparation.

Food safety further shapes procurement decisions. An FDA retail survey tested 615 dehydrated-garlic samples and detected Salmonella in 3 samples, equal to an estimated prevalence of 0.49%. Its import-entry review found 1 positive sample among 59 tested, or 1.7%. Although historical, these official results explain why industrial buyers increasingly require validated pathogen-reduction treatments, supplier audits, environmental monitoring and full batch traceability.

Dehydrated Garlic Market Segmentation

Product Type Analysis

Flakes & Cloves dominate with 51.1% share due to their broad use in food processing and seasoning applications

In 2025, Flakes & Cloves held a dominant market position, capturing more than a 51.1% share of the global dehydrated garlic market. Their leadership was largely supported by strong demand from food manufacturers, restaurants, and seasoning producers that prefer larger garlic formats for flavor retention and ease of handling. Flakes and cloves are widely used in soups, sauces, ready-to-cook meals, spice blends, and processed food products, making them a preferred choice across commercial food preparation. Their longer shelf life and convenient storage characteristics further contributed to widespread adoption.

Granules & Powder represented the fastest-growing segment in the dehydrated garlic market. Growth was supported by increasing demand for fine-textured garlic ingredients in snack seasonings, instant food products, dry mixes, and packaged convenience foods. Their ability to blend uniformly into food formulations, along with ease of measurement and processing, made them increasingly attractive to food manufacturers. Rising consumption of processed and ready-to-eat food products continued to support the adoption of granules and powder formats across global food production facilities during 2025.

Application Analysis

B2B dominates with 72.0% share driven by strong demand from food manufacturers and commercial buyers

In 2025, B2B held a dominant market position, capturing more than a 72.0% share of the global dehydrated garlic market. The segment’s leadership was supported by extensive procurement from food processing companies, seasoning manufacturers, packaged food producers, restaurants, and catering businesses. Dehydrated garlic is widely used as a key ingredient in sauces, soups, snacks, ready meals, spice blends, and processed meat products, creating consistent demand from industrial buyers. Large-volume purchasing, product standardization, and the need for longer shelf-life ingredients further strengthened the preference for dehydrated garlic across commercial operations.

B2C emerged as the fastest-growing segment in the dehydrated garlic market. Growth was supported by increasing consumer preference for convenient cooking ingredients that offer extended shelf life and ease of use. Rising purchases through supermarkets, specialty food stores, and online retail channels encouraged greater household adoption of dehydrated garlic products. Consumers increasingly favored ready-to-use garlic formats for everyday meal preparation, supporting the segment’s expansion during 2025.

Distribution Channel Analysis

Offline dominates with 74.0% share due to strong presence across wholesale, retail, and foodservice supply networks

In 2025, Offline held a dominant market position, capturing more than a 74.0% share of the global dehydrated garlic market. The segment maintained its leading position through well-established distribution networks that connect manufacturers with wholesalers, distributors, supermarkets, specialty food stores, and commercial food buyers. Many food processing companies and foodservice operators continue to prefer offline procurement channels because they enable bulk purchasing, direct supplier relationships, and easier product quality verification. The availability of dehydrated garlic through traditional trade channels also supports consistent supply for industrial and commercial users.

The Online segment emerged as the fastest-growing distribution channel in the dehydrated garlic market. Growth was supported by increasing use of e-commerce platforms by both household consumers and small businesses seeking convenient purchasing options. Online channels offer broader product selection, easy price comparison, and direct access to suppliers, making them an attractive option for buyers. The continued shift toward digital purchasing and expanding online grocery platforms contributed to the segment’s growth during 2025.

Key Market Segments

Product Type

- Flakes & Cloves

- Granules & Powder

- Chopped & Minced

Application

- B2B

- B2C

Distribution Channel

- Offline

- Online

Drivers

A core structural driver is the economics of replacing fresh garlic with shelf-stable dehydrated formats in regions where labor, storage, or inbound spoilage costs remain elevated. Processed garlic trades at higher per-kilogram prices than fresh commodity bulbs, but it often lowers total delivered-use cost because water has already been removed, usable solids are concentrated, and manufacturers avoid shrink from sprouting, mold, trimming, and variable moisture; the broader garlic powder trade data also shows a wide 2024 global price band of roughly $1.20/kg to $5.75/kg, indicating buyers can ladder specifications by end use rather than depend on one uniform pricing point.

This flexibility matters in import-dependent markets and private-label food manufacturing, where procurement teams increasingly optimize on “cost per functional flavor unit” rather than headline ingredient price. The result is a durable +1.1 percentage point uplift to CAGR, especially in packaged foods, seasoning blends, and dry soup or snack applications where dehydrated garlic’s 12–24 month storage practicality supports better inventory turns and less production disruption than fresh inputs.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed food flavor loading | +1.4% | North America core, EU core, APAC manufacturing hubs | Short term (≤ 2 years) |

| Shelf-life and yield economics | +1.1% | Global, strongest in import-dependent markets | Short term (≤ 2 years) |

| Foodservice menu normalization | +0.9% | North America, EU, GCC, urban APAC | Short term (≤ 2 years) |

| China-India export capacity reset | +1.2% | APAC supply base, North America, EU, Middle East | Medium term (2-4 years) |

| Sodium reduction reformulation | +0.8% | North America core, selective EU spill-over | Medium term (2-4 years) |

| Organic and compliant premium trade | +0.7% | EU core, US premium retail, Australia, Japan | Medium term (2-4 years) |

Restraints

The category also faces conversion-cost pressure from labor, energy, packaging, and compliance overhead, which is particularly damaging in dehydration because drying is energy-intensive and product quality depends on controlled processing rather than commodity handling alone. Eurostat reported that average hourly labour costs across the whole EU economy reached €34.9 in 2025, up 4.1 percent from 2024, while third-quarter 2025 labour costs still increased 3.7 percent year over year across the EU; those figures do not map one-for-one into garlic plants, but they confirm the broader wage environment facing food processors, warehouses, and quality-control operations.

The strategic result is that processors either pass on higher costs and risk losing share to cheaper origins, or maintain pricing and accept lower EBITDA per ton; in both cases, CapEx on new dehydration lines or automation tends to be deferred until utilization and contract coverage improve, supporting an estimated -0.9 percentage point reduction to baseline CAGR in higher-cost processing geographies and premium specification segments.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw bulb price swings | -1.5% | APAC supply base, EU, North America | Short term (≤ 2 years) |

| Residue compliance risk | -1.2% | EU core, US imports, Japan | Medium term (2-4 years) |

| Freight cost spikes | -1.0% | Asia-Europe lanes, US imports, Middle East | Short term (≤ 2 years) |

| Processing cost inflation | -0.9% | EU, North America, premium APAC | Short term (≤ 2 years) |

| White rot and weather loss | -1.1% | China, India, Egypt, US, EU growers | Medium term (2-4 years) |

| Quality and contaminant scrutiny | -0.7% | US retail, EU private label, Australia | Medium term (2-4 years) |

Opportunity

This is an opportunity rather than a baseline driver because private-label capture requires deliberate channel strategy, formulation support, and retail account execution; it is not automatically embedded in underlying dehydrated garlic demand. Europe’s private-label share reached 38.8 percent across 17 countries in the 52 weeks to 2025, up 0.33 percentage points year over year, and ambient food remains one of the strongest value-share growth areas, while global private-label spices and seasonings are projected to compound at about 10 percent through 2030 from a 2024 base near $2.9 billion.

That creates a large white space for dehydrated garlic suppliers to move up the value chain from bulk ingredient sales into co-developed seasoning blends, retailer-exclusive garlic-herb mixes, and private-label refill packs; if even 3 to 5 percent of bulk volume is converted into branded-service or retailer-spec contracts, suppliers can expand realized EBITDA per ton by 200 to 400 basis points and add roughly +1.4 percentage points to category CAGR through faster SKU proliferation and stronger shelf presence.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Premium freeze-dried formats | +1.3% | North America, EU, Japan, Korea | Medium term (2-4 years) |

| Traceable clean-label supply | +1.1% | US core, EU core, Australia | Short term (≤ 2 years) |

| Private-label seasoning tie-ups | +1.4% | EU core, North America, APAC retail | Short term (≤ 2 years) |

| Plant-based flavor systems | +0.9% | North America, EU, urban APAC | Medium term (2-4 years) |

| Foodservice labor-saver packs | +1.0% | North America, GCC, EU, SE Asia | Short term (≤ 2 years) |

| M&A ingredient roll-ups | +1.2% | India, China, EU, US | Medium term (2-4 years) |

Challenges

Climate-driven crop variability is a systemic challenge rather than a discrete restraint because it rarely eliminates garlic production in a given year but continuously alters yield, bulb size distribution, and dry-matter content, forcing dehydrators to rework procurement and processing plans each season with 5 to 20 percent swings in available tonnage and solids yield.

At processor level, a 10 percent drop in usable bulb yield in a major origin can translate into a 12 to 15 percent reduction in dehydrated output once grading losses and higher moisture are accounted for, which in turn lifts unit conversion costs by 5 to 8 percent and forces more frequent price renegotiations, smaller contract volumes, and higher safety stocks in downstream blending and food manufacturing. Over the next decade, the need to continuously recalibrate sourcing geographies, diversify farms, and invest in disease monitoring and irrigation drives an estimated -1.0 percentage point friction drag on maximum attainable CAGR as operators allocate capital to resilience rather than pure capacity expansion.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Climate-driven crop variability | -1.0% | China, India, EU, US, MENA | Long term (≥ 4 years) |

| Volatile logistics and lead times | -0.8% | APAC–EU, APAC–US, GCC corridors | Medium term (2-4 years) |

| Quality and spec inconsistency | -0.9% | Global B2B, retail import hubs | Medium term (2-4 years) |

| Traceability and data gaps | -0.7% | US, EU, Japan, premium markets | Long term (≥ 4 years) |

| Fragmented processing capacity | -0.8% | India, China, Egypt, SE Asia | Long term (≥ 4 years) |

| Skilled operations talent strain | -0.6% | Global, esp. high-cost regions | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade Realignments and Food Security Policies Reshaping Global Dehydrated Garlic Supply Chains

Current geopolitical developments are influencing the dehydrated garlic market through shifting trade policies, supply chain diversification efforts, food security initiatives, and transportation disruptions. As dehydrated garlic relies on the cross-border movement of agricultural raw materials, packaging supplies, and processed food ingredients, changes in trade relations and logistics networks can directly affect production costs and product availability. Increasing geopolitical uncertainty has encouraged food manufacturers and distributors to diversify sourcing strategies and reduce reliance on concentrated supply regions.

Import regulations, tariff adjustments, and stricter food safety requirements across major consuming markets have increased compliance obligations for dehydrated garlic exporters. At the same time, disruptions in global shipping routes and fluctuations in freight costs have created challenges for ingredient suppliers serving international markets. These factors have encouraged buyers to strengthen regional procurement networks and establish more resilient supply chains to ensure uninterrupted product availability.

In parallel, governments are prioritizing food security and domestic food processing capabilities, leading to investments in agricultural value-addition and food preservation infrastructure. Such initiatives support the expansion of local dehydration capacity and improve supply stability for shelf-stable ingredients. While these developments create opportunities for regional market growth, dehydrated garlic manufacturers remain exposed to regulatory changes, trade uncertainties, and logistics-related risks.

Regional Analysis

Asia-Pacific dominated the dehydrated garlic market with a 39.1% share, accounting for approximately US$ 1.21 billion in 2025

In 2025, Asia-Pacific held the leading position in the global dehydrated garlic market, accounting for 39.1% of total revenue, equivalent to approximately US$ 1.21 billion. The region’s dominance was supported by its strong agricultural production base, established garlic processing industry, and extensive participation in global food ingredient trade. Demand for dehydrated garlic remained high across food manufacturing, seasoning production, packaged foods, and foodservice applications, supporting consistent market growth.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dehydrated garlic manufacturers focus on strengthening processing efficiency, product quality consistency, and supply chain reliability to maintain competitiveness in the market. A key priority is the development of advanced dehydration and drying techniques that help preserve flavor, aroma, color, and shelf life while reducing moisture content. Companies continue to expand production capacity and invest in modern processing equipment to meet growing demand from food manufacturers, seasoning producers, and foodservice operators. Product diversification across flakes, cloves, granules, powders, and customized ingredient formats also remains an important strategy for addressing varied customer requirements.

Market Key Players

- Apple Food Industries

- Asian Food Export

- Ganesh Dehy Foods

- Garlico Industries Ltd.

- Harsh Impex

- Jiyan Food Ingredients

- Kohinoor Food Industries

- Natural Agro Foods

- Nature Exports Co.

- Shandong Yummy Food Ingredients Co., Ltd.

- Handan Green and Healthy Dehydrated Vegetables Food Co. Ltd.

- Real Dehydrates Pvt. Ltd.

- Anyang General Foods

- Henan Sunny Foodstuff Co., Ltd.

- M.N. Dehy Foods

Key Development

- In March 2025, Japan’s Ministry of Health, Labour and Welfare removed enhanced monitoring requirements on garlic imports from China related to thiamethoxam residues, supporting smoother international garlic trade conditions for Chinese exporters.

- In June 2025, the 2025 China Garlic Annual Conference and Garlic Chain Innovation Conference was held in Shandong, bringing together garlic industry participants to discuss supply chain modernization, product quality improvement, and industry development initiatives.

- In September 2025, Henan Sunny Foodstuff Co., Ltd. confirmed its participation in ANUGA 2025 in Germany, strengthening its international market outreach and promoting dehydrated garlic products to global food industry buyers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$3.1 Bn |

| Forecast Revenue (2035) | US$4.4 Bn |

| CAGR (2026-2035) | 3.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Flakes & Cloves, Granules & Powder, and Chopped & Minced), By Application (B2B and B2C), By Distribution Channel (Offline and Online) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Apple Food Industries, Asian Food Export, Ganesh Dehy Foods, Garlico Industries Ltd., Harsh Impex, Jiyan Food Ingredients, Kohinoor Food Industries, Natural Agro Foods, Nature Exports Co., Shandong Yummy Food Ingredients Co., Ltd., Handan Green and Healthy Dehydrated Vegetables Food Co. Ltd., Real Dehydrates Pvt. Ltd., Anyang General Foods, Henan Sunny Foodstuff Co., Ltd., and M.N. Dehy Foods. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |