Global Non-GMO Soybean Market Size, Share, And Industry Analysis Report By Product (Whole Beans, Crushed Beans), By Application (Soybean Meal, Soy Oil, Livestock Feed, Pharmaceuticals, Others), By End User (Food and Beverages, Animal Feed, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181045

- Number of Pages: 225

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

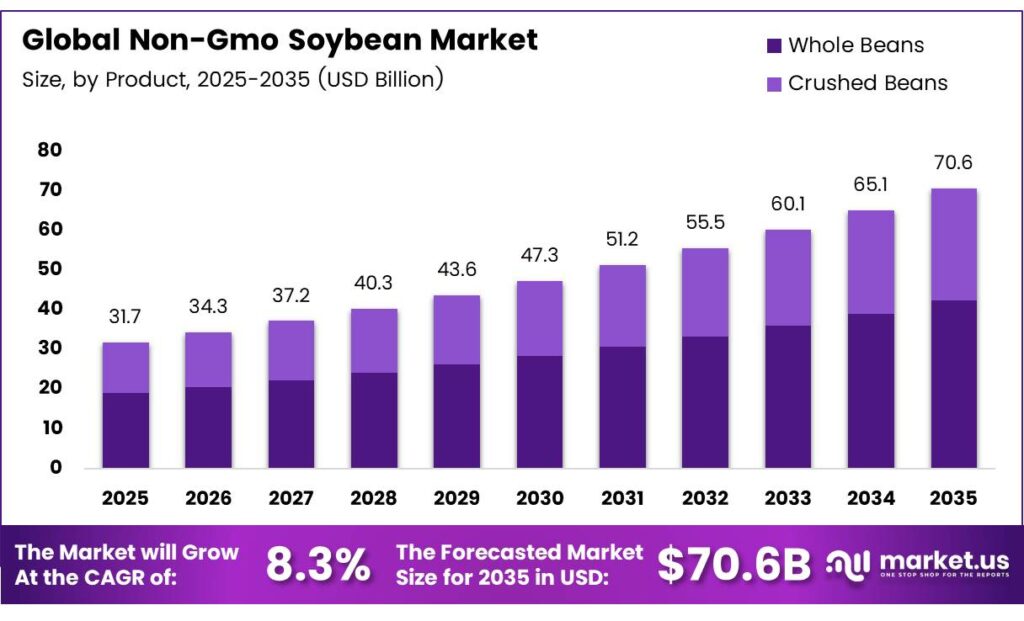

The Global Non-GMO Soybean Market size is expected to be worth around USD 70.6 billion by 2035 from USD 31.7 billion in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035.

The non-GMO soybean market covers the production, processing, and trade of soybeans that are verified free from genetic modification. These soybeans serve food manufacturers, animal feed producers, pharmaceutical companies, and industrial processors. Demand for identity-preserved, traceable supply chains continues to drive this segment apart from conventional soybean trade.

Consumers across North America, Europe, and the Asia Pacific increasingly prefer clean-label products. Food brands respond by sourcing certified non-GMO ingredients. This shift reshapes procurement strategies across the entire soy value chain, from farm-level identity preservation to retail shelf placement in premium natural food channels.

- U.S. soybean exports totaled $24.5 billion in 2024, down from $27.7 billion in 2023, keeping soybeans as the top U.S. farm export by value. This figure highlights the massive global soybean trade base from which the non-GMO segment continues to carve out a growing share.

Government regulations play a key role in shaping market behavior. The European Union mandates strict GMO labeling requirements, effectively pushing importers toward certified non-GMO supply chains. Similarly, Japan enforces traceability standards that favor identity-preserved soybeans. These regulatory frameworks create structured demand that supports premium pricing for non-GMO certified crops globally.

- Europe harvested 1.0 million tonnes of Donau Soja and Europe Soya certified soybeans in 2024 across 11 countries. This verified volume confirms a strengthening certified non-GMO processing ecosystem in Europe, supported by 14 crushers and 37 smaller soy processors operating under these recognized standards.

Investment in certification infrastructure, blockchain-based traceability, and regenerative farming practices strengthens supply chain integrity. Processors in Europe and North America expand non-GMO crushing capacity to meet growing demand from food manufacturers. Additionally, emerging markets in Southeast Asia and South Asia show rising interest in non-GMO soy-based food ingredients as middle-class consumption patterns evolve.

Key Takeaways

- The Global Non-GMO Soybean Market is valued at USD 31.7 billion in 2025 and is projected to reach USD 70.6 billion by 2035. The market grows at a CAGR of 8.3% during the forecast period 2026 to 2035.

- Whole Beans dominate the market with a 67.8% share in 2025.

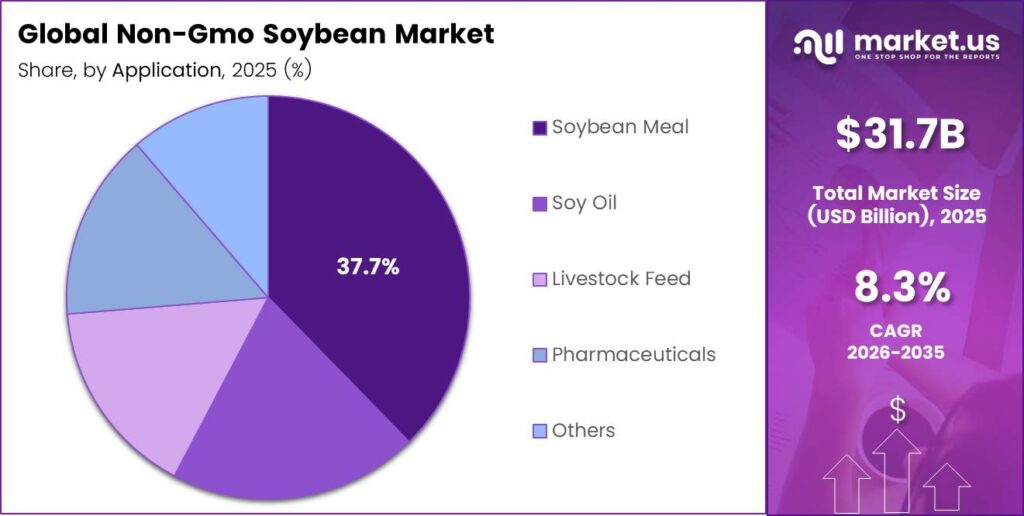

- Soybean Meal holds the leading position with a 37.7% share.

- Food and beverages lead the segment with a 59.2% share.

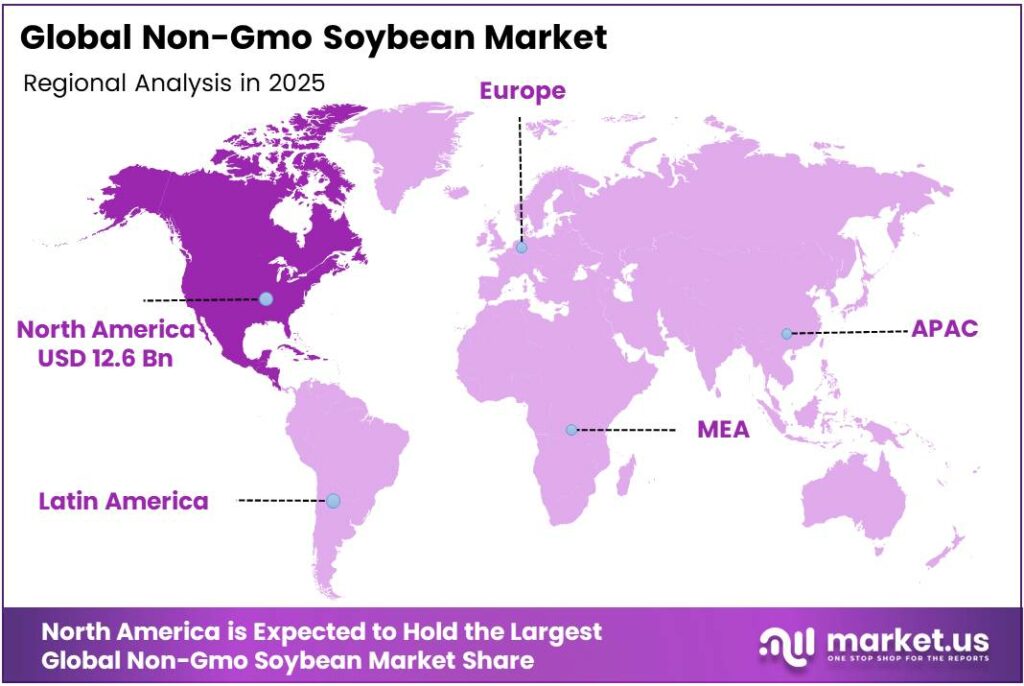

- North America dominates the regional landscape with a 39.6% market share, valued at USD 12.6 billion in 2025.

By Product Analysis

Whole Beans dominates with 67.8% due to strong demand from food-grade and identity-preserved supply chains.

In 2025, Whole Beans held a dominant market position in the By-Product segment of the Non-GMO Soybean Market, with a 67.8% share. Food processors and tofu manufacturers prefer whole beans for their identity-preserved traceability. Moreover, export markets in Japan and South Korea specifically source whole food-grade non-GMO beans at significant premiums over bulk commodity soybeans.

Crushed Beans represent the remaining share of the By-Product segment. Processors use crushed non-GMO soybeans to produce soy oil, soybean meal, and lecithin for food-grade applications. Additionally, the growing demand for non-GMO emulsifiers in the confectionery and bakery sectors continues to support crushing activity across North America and Europe.

By Application Analysis

Soybean Meal dominates with 37.7% due to high usage in animal nutrition and protein feed formulations.

In 2025, Soybean Meal held a dominant market position in the By Application segment of the Non-GMO Soybean Market, with a 37.7% share. Animal nutrition manufacturers rely on soybean meal as a primary protein source. Furthermore, premium livestock and poultry producers increasingly specify non-GMO meal to align with clean-label brand commitments in retail meat markets.

Soy Oil serves as a key application across food service, packaged foods, and industrial uses. Non-GMO soy oil commands a price premium in natural food retail channels. Consequently, crush facilities increasingly segregate non-GMO oilseed streams to capture higher margins from certified oil production for specialty food manufacturers.

Livestock Feed as a direct application category addresses producers who use whole or minimally processed non-GMO soybeans in feed rations. This application grows alongside organic livestock farming. Additionally, aquaculture producers are beginning to explore non-GMO soy protein ingredients as sustainable alternatives to fishmeal in feed formulations.

Pharmaceuticals represent a smaller but high-value application segment. Drug manufacturers and nutraceutical brands require non-GMO soy-derived phospholipids and isoflavones. Therefore, specialized processors supply pharmaceutical-grade non-GMO soy extracts with full traceability documentation to meet regulatory requirements in the United States, Europe, and Japan.

Others in this segment include industrial bioplastics, cosmetics, and bio-based chemical feedstocks. Manufacturers in these sectors increasingly seek non-GMO soy inputs for sustainability and brand positioning. Moreover, partnerships between non-GMO soybean processors and bioplastic manufacturers are emerging as a notable growth area in specialty industrial applications.

By End User Analysis

Food and Beverages dominate with 59.2% due to rising demand for clean-label and plant-based ingredients.

In 2025, Food and Beverages held a dominant market position in the By End User segment of the Non-GMO Soybean Market, with a 59.2% share. Food manufacturers across the United States, Europe, and the Asia Pacific prioritize non-GMO sourcing for soy milk, tofu, and plant-based protein products. Consequently, retail demand for non-GMO certified food products continues to accelerate market growth.

Animal Feed end users represent a significant secondary segment. Livestock producers, poultry integrators, and aquaculture farms seek non-GMO soybean meal to differentiate their products in premium meat and seafood markets. Moreover, organic certification requirements in the European Union mandate non-GMO feed inputs, creating a structurally supported demand base for this end-user category.

Others encompass pharmaceutical manufacturers, cosmetic ingredient producers, and industrial bioplastic companies. These end users value non-GMO soy inputs for regulatory compliance and sustainability reporting. Additionally, growth in bio-based materials and nutraceutical formulations continues to expand the breadth of non-GMO soybean end-use applications globally.

Key Market Segments

By Product

- Whole Beans

- Crushed Beans

By Application

- Soybean Meal

- Soy Oil

- Livestock Feed

- Pharmaceuticals

- Others

By End User

- Food and Beverages

- Animal Feed

- Others

Emerging Trends

Regenerative Agriculture and Clean-Label Innovation Reshape the Non-GMO Soybean Landscape

Regenerative agriculture practices increasingly align with non-GMO certification programs. Farmers adopting soil health initiatives such as cover cropping and reduced tillage find these practices compatible with non-GMO identity preservation. Consequently, certification bodies and food brands actively promote regenerative non-GMO supply chains as a differentiated value proposition for premium market segments.

- Japan’s soybean imports were forecast at 3.30 million metric tons in MY2025/26, driven by recovering crush margins. This stable import volume underlines continued Asian demand for identity-preserved non-GMO soybeans. Moreover, the shift toward non-GMO soy lecithin and emulsifiers in the bakery and confectionery sectors reflects product innovation trends across global food manufacturing.

Consolidation among regional non-GMO soybean processors accelerates market maturity. Smaller processors form strategic alliances to enhance distribution networks and achieve economies of scale. Additionally, the growing preference for non-GMO soy milk and yogurts over dairy alternatives in Europe and the Asia Pacific opens new volume channels for certified soy ingredient suppliers targeting health-conscious consumers.

Drivers

Surging Clean-Label Consumer Demand and Premium Pricing Drive Non-GMO Soybean Market Growth

Global consumer demand for clean-label and plant-based protein products drives non-GMO soybean adoption at scale. Food brands reformulate products with certified non-GMO ingredients to meet shopper expectations in natural retail channels. Moreover, plant-based protein manufacturers specifically require non-GMO soy to maintain brand integrity and consumer trust in competitive markets.

- The United States planted 3,484,000 acres of non-GMO soybeans in 2024, representing roughly 4.0% of total U.S. soybean acreage. This dedicated non-GMO production base reflects farmer confidence in premium price realization. Certified non-GMO soybeans command meaningful price premiums over conventional varieties, improving farm-level profitability and encouraging broader acreage adoption.

Expansion of specialty food retail channels dedicated to natural and organic products creates sustained structural demand. Retailers allocate more shelf space to non-GMO certified products as consumer purchasing habits shift. Additionally, stringent GMO labeling regulations in importing nations such as Japan and EU member states mandate traceable non-GMO supply chains, reinforcing demand from international trading partners.

Restraints

Cross-Contamination Risks and Higher Production Costs Restrain Non-GMO Soybean Market Expansion

Cross-contamination risk during supply chain transit represents a significant operational challenge. Non-GMO soybeans require strict segregation from genetically modified crops at every stage, from farm storage to processing and transport. Consequently, logistics costs rise substantially, and processors must invest in dedicated handling infrastructure to maintain certification integrity across the supply chain.

- Brazil’s 2024 non-GMO soybean exports were estimated at approximately 1.5 million tons, reflecting a significant reduction from the prior year following disruption at a major non-GMO processing plant in Paraná. This supply interruption illustrates how infrastructure vulnerabilities translate directly into market instability and reduced availability of certified supply.

Higher production costs and lower crop yields compared to genetically modified varieties create an economic disadvantage for non-GMO farmers. Without sufficient premium price support, farmer adoption remains limited. Therefore, the economic viability of non-GMO soybean production depends heavily on maintaining robust demand signals and transparent premium payment mechanisms throughout the supply chain.

Growth Factors

Emerging Applications, Strategic Partnerships, and Technology Drive Non-GMO Soybean Market Expansion

Development of non-GMO soy ingredients for aquafeed and alternative seafood sectors opens high-value new markets. Aquaculture producers actively seek sustainable, traceable protein sources to replace fishmeal. Moreover, pharmaceutical and industrial bioplastic manufacturers increasingly partner with certified non-GMO soybean processors to secure identity-preserved soy inputs for regulated and sustainability-driven production environments.

- Europe’s total soy output reached 12.130 million tonnes in 2023, up 23.1% from the previous year. This production growth demonstrates the scale of European non-GMO soy supply expansion. The EU-27 soybean harvest reached 2.907 million tonnes in 2023, with all EU soybean production described as non-GM, confirming Europe as a structurally non-GMO soy production region.

Blockchain technology adoption for end-to-end supply chain transparency creates new premium branding opportunities for non-GMO soybean suppliers. Digital traceability platforms allow buyers to verify identity preservation from the field to the facility. Consequently, untapped market potential in emerging economies with expanding middle-class health consciousness represents a major growth frontier for certified non-GMO soy products.

Regional Analysis

North America Dominates the Non-GMO Soybean Market with a Market Share of 39.6%, Valued at USD 12.6 Billion

North America leads the global non-GMO soybean market, holding a 39.6% share valued at USD 12.6 billion in 2025. The United States drives regional dominance through large certified non-GMO acreage, well-established identity preservation infrastructure, and strong export relationships with Japan and South Korea. Additionally, Canada’s substantial soybean exports to Asian markets reinforce North America’s position as the primary global supplier of food-grade non-GMO soybeans.

Europe represents a structurally non-GMO soybean production and consumption region. The EU mandates strict GMO labeling, effectively requiring non-GMO certification across food and feed supply chains. Moreover, Donau Soja and Europe Soya certification programs establish a verified regional supply base, with certified processors and crushers expanding capacity to reduce the continent’s significant non-GMO soy supply deficit.

Asia Pacific drives significant non-GMO soybean import demand, particularly from Japan and South Korea. Japan’s food safety standards and consumer preference for non-GMO tofu and soy milk create consistent premium import volumes. Furthermore, China’s growing food-grade soybean demand and expanding middle-class preference for clean-label products continue to reshape sourcing strategies across the Asia Pacific region.

The Middle East and Africa region represents an emerging frontier for non-GMO soybean demand. Growing health consciousness among urban consumers and expanding food processing sectors create new sourcing opportunities. Additionally, increasing regulatory interest in food safety and ingredient transparency drives importers in the region to explore certified non-GMO soy procurement options from established global suppliers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Archer Daniels Midland Company (ADM) operates as one of the largest agricultural processors and food ingredient providers globally. The company maintains extensive non-GMO soybean handling and processing capabilities across North America and Europe. ADM supports identity preservation programs that connect certified non-GMO farm supply with food-grade end users, giving it a significant structural advantage in premium ingredient supply chains.

Grain Millers, Inc. focuses on whole grain and specialty ingredient processing, including certified non-GMO soy products for natural and organic food manufacturers. The company sources identity-preserved soybeans directly from certified growers and processes them in dedicated non-GMO facilities. Moreover, Grain Millers serves a growing customer base of clean-label food brands that require full supply chain traceability and third-party certification documentation.

Zeeland Farm Services, Inc. provides grain handling, storage, and identity preservation services with a strong focus on specialty non-GMO soybeans. The company operates certified grain facilities that segregate non-GMO soybean varieties for export and domestic food processing markets. Consequently, Zeeland Farm Services plays an important role in connecting Midwest farmers growing non-GMO soybeans with high-value buyers in Asian and European food manufacturing sectors.

Laura Soybeans specializes exclusively in food-grade, non-GMO soybeans developed through traditional plant breeding programs. The company works directly with licensed farmers to grow proprietary soybean varieties with superior flavor and protein profiles. Additionally, Laura Soybeans supplies tofu makers, soy milk producers, and specialty food manufacturers across North America and export markets that require the highest quality food-grade non-GMO soybean identity preservation.

Top Key Players in the Market

- Archer Daniels Midland Company (ADM)

- Grain Millers, Inc.

- Zeeland Farm Services, Inc.

- Laura Soybeans

- Sinner Bros. & Bresnahan

- Soy Austria

- Sri Venkateshwara Feeds and Farms Group

- AVI Agri Business Pvt., Ltd.

Recent Developments

- In 2025, ADM, in partnership with Bayer, is significantly scaling up a sustainable soybean farming program in Maharashtra, India. The program. The program utilizes the ProTerra Foundation sustainability framework, which is highly relevant to non-GMO supply chains, as ProTerra standards include non-GMO requirements.

- In 2025, Zeeland Farm Services is a long-standing exporter of non-GMO soybeans and soybean meal, with significant export values in both food-grade and feed-grade products. The company continues to be a diversified agribusiness, involved in grain merchandising, soybean processing, and the production of non-GMO soybean meal and oil under its Zoye brand.

Report Scope

Report Features Description Market Value (2025) USD 31.7 Billion Forecast Revenue (2035) USD 70.6 Billion CAGR (2026-2035) 8.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Whole Beans, Crushed Beans), By Application (Soybean Meal, Soy Oil, Livestock Feed, Pharmaceuticals, Others), By End User (Food and Beverages, Animal Feed, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Archer Daniels Midland Company (ADM), Grain Millers, Inc., Zeeland Farm Services, Inc., Laura Soybeans, Sinner Bros. & Bresnahan, Soy Austria, Sri Venkateshwara Feeds and Farms Group, AVI Agri Business Pvt., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Archer Daniels Midland Company (ADM)

- Grain Millers, Inc.

- Zeeland Farm Services, Inc.

- Laura Soybeans

- Sinner Bros. & Bresnahan

- Soy Austria

- Sri Venkateshwara Feeds and Farms Group

- AVI Agri Business Pvt., Ltd.

Our Clients

- 181045

- March 2026