Quick Navigation

Report Overview

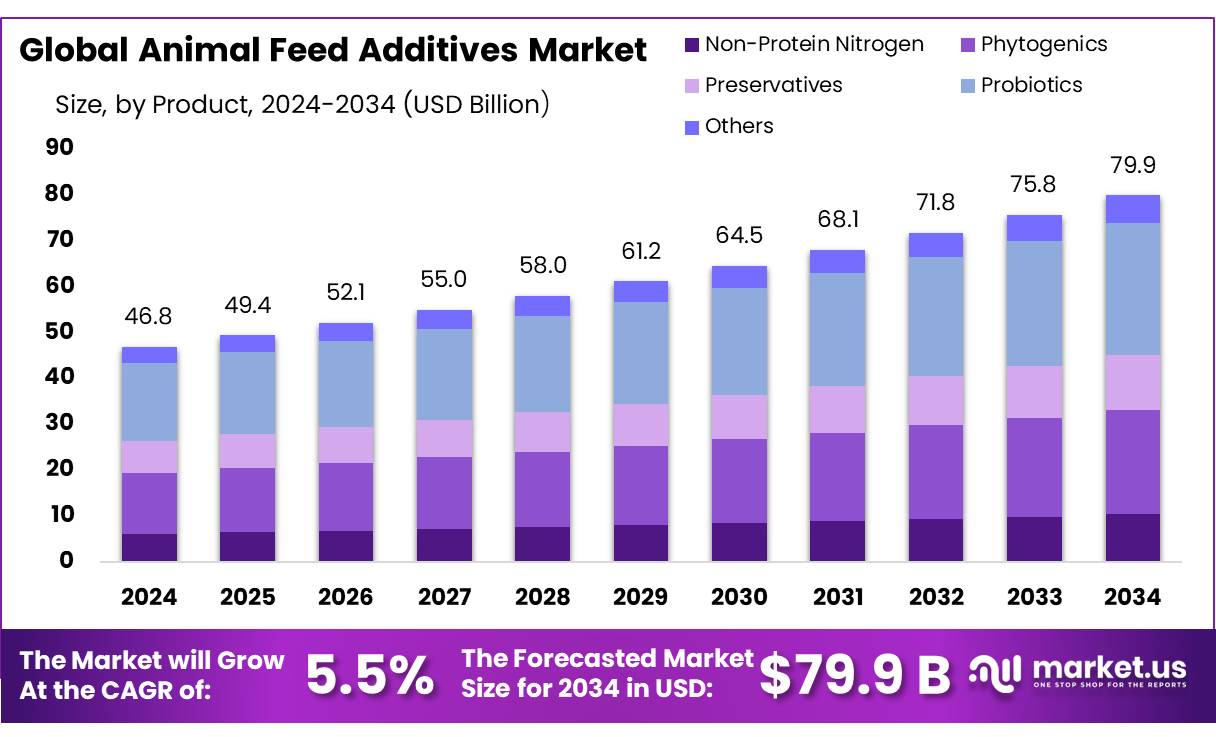

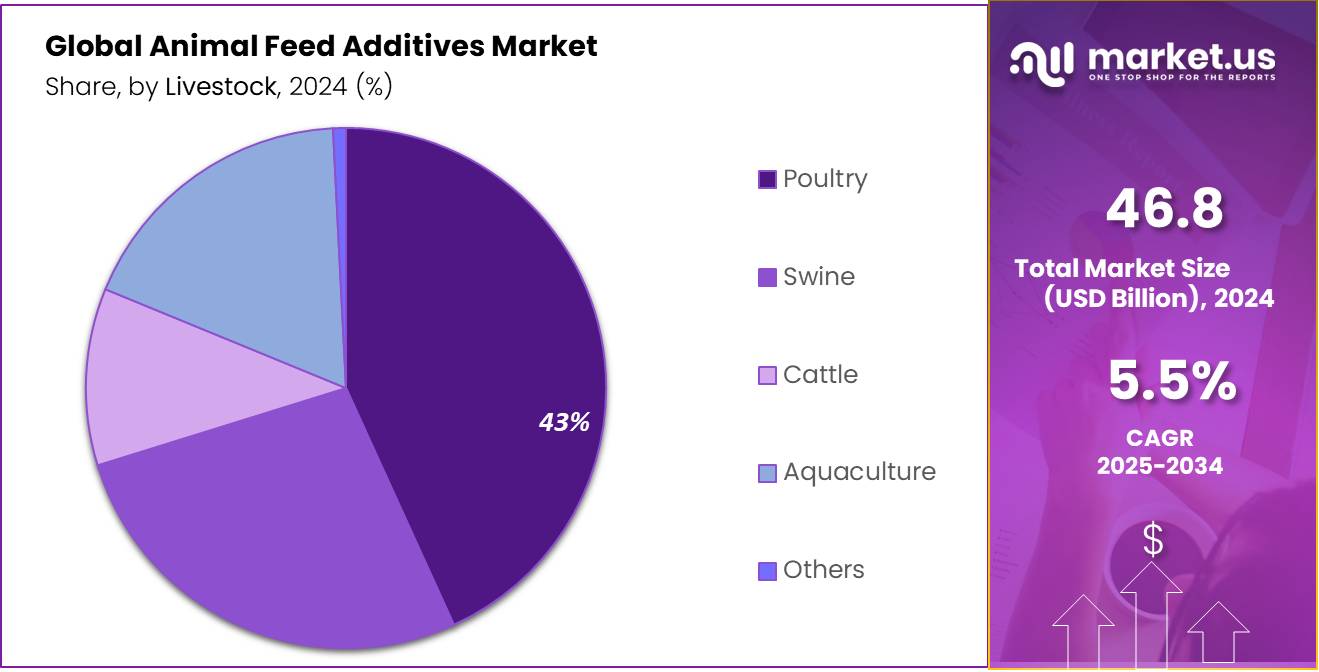

The Global Animal Feed Additives Market size is expected to be worth around USD 79.9 Billion by 2034, from USD 46.8 Billion in 2024, growing at a CAGR of 5.5% during the forecast period from 2025 to 2034.

The animal feed additives concentrates market plays a crucial role in enhancing livestock productivity, health, and feed efficiency. These additives encompass a broad range of substances including vitamins, amino acids, enzymes, probiotics, and minerals that are incorporated into animal feed to improve nutrition, disease resistance, and growth rates. Increasing global demand for meat, dairy, and poultry products driven by population growth and rising incomes has significantly amplified the consumption of animal feed additives concentrates.

According to the Food and Agriculture Organization (FAO), global meat consumption is expected to reach approximately 376 million tonnes by 2030, up from 340 million tonnes in 2020, highlighting the growing requirement for efficient feed additives to sustain this demand.

The industrial scenario reflects steady advancements in feed technology and additive formulations tailored to meet specific animal species’ nutritional needs. Government agencies worldwide have introduced regulations and initiatives to promote safe and sustainable animal nutrition practices. For instance, the U.S. Food and Drug Administration (FDA) enforces rigorous guidelines on feed additive safety under the Food Safety Modernization Act, ensuring additives do not pose risks to animals or humans. Furthermore, initiatives like the European Union’s Farm to Fork Strategy emphasize reducing antibiotic use in livestock, increasing the demand for natural feed additives such as probiotics and enzymes as alternatives to antibiotics.

In India, the animal feed sector is experiencing significant growth, driven by increasing demand for meat, dairy, and aquaculture products. The government’s proactive measures, such as the establishment of the ₹15,000 crore Animal Husbandry Infrastructure Development Fund (AHIDF) in 2020, aim to bolster private sector investment in developing animal husbandry infrastructure, including feed plants.

Several key drivers propel the animal feed additives concentrates market. The intensification of livestock farming to meet protein needs has increased the reliance on additives that enhance feed conversion ratios and improve animal growth. Growing awareness of animal welfare and the necessity for sustainable agricultural practices push manufacturers towards developing eco-friendly additives that reduce environmental impact, such as methane-reducing supplements.

Additionally, rising incidences of animal diseases and the subsequent demand for additives that boost immunity contribute to market growth. The World Organization for Animal Health (OIE) reported a 15% increase in disease outbreaks among livestock globally in 2024 compared to previous years, which accentuates the importance of health-promoting feed additives.

Key Takeaways

- Animal Feed Additives Market size is expected to be worth around USD 79.9 Billion by 2034, from USD 46.8 Billion in 2024, growing at a CAGR of 5.5%.

- Amino Acids held a dominant market position, capturing more than a 28.4% share of the global animal feed additives market.

- Probiotics held a dominant market position, capturing more than a 36.1% share of the global animal feed additives market.

- Synthetic held a dominant market position, capturing more than a 67.9% share of the global animal feed additives market.

- Dry held a dominant market position, capturing more than a 63.30% share of the global animal feed additives market.

- Poultry held a dominant market position, capturing more than a 43.2% share of the global animal feed additives market.

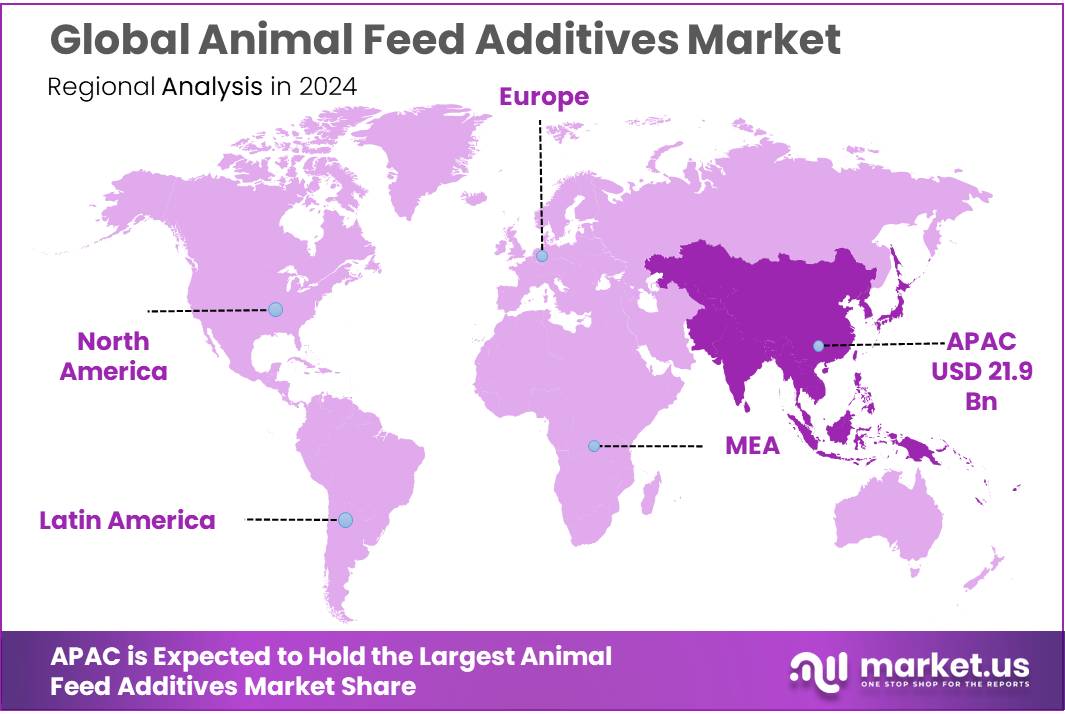

- Asia-Pacific (APAC) region solidified its position as the leading market for animal feed additives, commanding a substantial 46.8% share, equivalent to a market value of approximately USD 21.9 billion.

Analysts’ Viewpoint

Technological advancements are significantly impacting the sector. Innovations in biotechnology and the development of phytogenic feed additives—derived from herbs and plants—are enhancing animal health and productivity while aligning with consumer preferences for natural products. Moreover, the integration of artificial intelligence in predictive modeling is optimizing feed formulations, leading to improved feed efficiency and reduced environmental impact.

The regulatory environment, which varies across regions. In the European Union, stringent regulations necessitate thorough approval processes for feed additives, focusing on safety for animals, consumers, and the environment . Such regulatory frameworks, while ensuring product safety and quality, can pose challenges in terms of compliance and market entry. Therefore, while the market offers substantial growth opportunities, particularly in regions like Asia-Pacific, which held a significant market share in 2024, investors must navigate the complex regulatory landscapes and invest in innovation to meet evolving consumer demands and sustainability goals.

By Product

Amino Acids dominate with 28.4% share in 2024, driven by rising demand for protein-rich animal diets.

In 2024, Amino Acids held a dominant market position, capturing more than a 28.4% share of the global animal feed additives market. Their widespread adoption can be attributed to their essential role in enhancing animal growth, improving feed conversion efficiency, and reducing nitrogen excretion. Amino acids such as lysine, methionine, and threonine are especially critical in poultry and swine diets, where they help meet precise nutritional requirements without over-reliance on expensive protein-rich raw materials. This segment continues to benefit from advancements in synthetic amino acid production and increased awareness among livestock farmers regarding optimized feed formulations. With livestock industries under pressure to improve productivity sustainably, the use of amino acids is expected to remain strong in 2025 and beyond, particularly in Asia-Pacific and Latin America, where animal protein consumption is growing steadily.

By Minerals

Probiotics lead the way with 36.1% share in 2024 as livestock farmers shift towards gut health and natural solutions.

In 2024, Probiotics held a dominant market position, capturing more than a 36.1% share of the global animal feed additives market. This strong foothold is largely due to the growing demand for natural and antibiotic-free alternatives that support digestive health and boost immunity in livestock. As concerns over antibiotic resistance continue to mount, farmers and producers are turning to probiotics to maintain animal well-being without compromising food safety. These beneficial microbes help balance gut flora, improve nutrient absorption, and reduce the risk of gastrointestinal diseases, especially in poultry and pig farming. By 2025, the usage of probiotics is expected to increase further, supported by government regulations encouraging reduced antibiotic usage in animal feed and a global push toward more sustainable livestock practices.

By Source

Synthetic feed additives lead with 67.9% share in 2024, supported by cost efficiency and consistent performance.

In 2024, Synthetic held a dominant market position, capturing more than a 67.9% share of the global animal feed additives market. This segment’s leadership is mainly due to the large-scale use of synthetic additives like amino acids, vitamins, and minerals that ensure precise dosing, longer shelf life, and predictable results in animal nutrition. Compared to natural alternatives, synthetic feed additives are more affordable and widely available, making them the preferred choice for commercial-scale livestock operations across poultry, swine, and cattle farming. The growing demand for high-yield meat and dairy production continues to push adoption rates higher. By 2025, synthetic additives are expected to maintain their strong presence, especially in fast-developing regions, where efficient feed conversion remains a top priority for producers.

By Form

Dry feed additives dominate with 63.3% share in 2024 due to easy handling and long shelf life.

In 2024, Dry held a dominant market position, capturing more than a 63.30% share of the global animal feed additives market. The popularity of dry form additives comes from their longer shelf life, easier storage, and better mixing compatibility with feed rations. They are more stable during transportation and allow for precise dosing without the need for special storage conditions. These benefits are especially important in large-scale livestock operations where bulk feed production is routine. Dry additives like powdered amino acids, minerals, and enzymes are widely used across poultry and swine sectors. Looking into 2025, the demand for dry form additives is expected to remain strong, particularly in emerging economies, as feed manufacturers seek efficient and cost-effective solutions for mass feed production.

By Livestock

Poultry sector leads with 43.2% share in 2024, driven by soaring global demand for chicken meat and eggs.

In 2024, Poultry held a dominant market position, capturing more than a 43.2% share of the global animal feed additives market. This strong lead is largely due to the rapid expansion of poultry farming worldwide, especially in Asia and Latin America, where chicken remains a key source of affordable protein. Feed additives play a vital role in boosting feed efficiency, ensuring faster weight gain, and reducing mortality in broilers and layers. Poultry producers widely rely on amino acids, probiotics, and enzymes to maintain flock health and meet high productivity targets. With global poultry consumption expected to grow further in 2025, this segment is likely to sustain its dominance, backed by continued investment in feed optimization and disease prevention strategies.

Key Market Segments

By Product

- Antibiotics

- Vitamins

- Vitamin A

- Vitamin E

- Vitamin B

- Vitamin C

- Others

- Antioxidants

- Amino Acids

- Tryptophan

- Lysine

- Methionine

- Threonine

- Others

- Feed Enzymes

- Phytase

- Non-Starch Polysaccharides

- Others

- Feed Acidifiers

- Phosphates

- Carotenoids

- Mycotoxin Detoxifiers

- Flavors & Sweeteners

By Minerals

- Non-Protein Nitrogen

- Phytogenics

- Preservatives

- Probiotics

- Others

By Source

- Natural

- Synthetic

By Form

- Dry

- Liquid

By Livestock

- Swine

- Poultry

- Cattle

- Aquaculture

- Others

Drivers

Rising Global Meat Demand Fuels Growth in Animal Feed Additives

One of the primary drivers of the animal feed additives market is the increasing global demand for meat, particularly poultry, which necessitates enhanced livestock productivity and health management.

According to the Food and Agriculture Organization (FAO), global meat production is projected to reach 373 million tonnes in 2024, marking a 1.4% increase from the previous year. This growth is predominantly driven by the poultry and bovine sectors, reflecting strong consumer demand and favorable operational margins despite challenges such as avian influenza outbreaks in certain regions.

The surge in meat production underscores the necessity for efficient feed solutions to support animal growth and health. Feed additives, including amino acids, vitamins, enzymes, and probiotics, play a crucial role in enhancing feed efficiency, improving nutrient absorption, and bolstering the immune systems of livestock. These additives contribute to better growth rates and feed conversion ratios, which are essential for meeting the escalating meat consumption demands.

Government initiatives further bolster the feed additives market. For instance, in India, the government has launched several programs to promote the use of feed additives and improve animal health through subsidies and technical assistance. The Animal Husbandry Infrastructure Development Fund (AHIDF), with an allocation of INR 15,000 crore, aims to enhance private sector investment in animal husbandry infrastructure, including feed plants.

Restraints

High Raw Material Costs Challenge the Growth of Animal Feed Additives Market

One of the significant challenges facing the animal feed additives market is the rising cost of raw materials. Feed additives, such as amino acids, vitamins, and enzymes, are essential for enhancing animal health and productivity. However, the production of these additives heavily relies on raw materials like corn, soybean meal, and other agricultural commodities, whose prices have been volatile in recent years.

According to the Food and Agriculture Organization (FAO), feed costs can account for up to 70% of the total cost of livestock production. This high percentage underscores the significant impact that fluctuations in raw material prices can have on the overall cost structure of animal farming. For instance, the FAO reported that the global feed production was 1.2 billion metric tons in 2023, a slight decrease from the previous year, attributed to more efficient use of feed made possible by intensive production systems .

The volatility in raw material prices is influenced by various factors, including climate change, geopolitical tensions, and shifts in global demand and supply dynamics. For example, extreme weather events can disrupt crop yields, leading to shortages and price spikes. Additionally, geopolitical events can affect trade flows, further exacerbating price volatility.

These rising costs pose a significant challenge for feed manufacturers and livestock producers, particularly in developing countries where margins are already thin. The increased expenses can lead to higher prices for animal products, affecting affordability and accessibility for consumers. Moreover, the financial strain may discourage farmers from investing in high-quality feed additives, potentially compromising animal health and productivity.

Opportunity

Embracing Sustainable Livestock Practices: A Key Opportunity for Feed Additives Market Growth

The global shift towards sustainable livestock farming presents a significant growth opportunity for the animal feed additives market. As concerns over environmental impact and resource efficiency intensify, there’s a growing emphasis on practices that enhance animal health and productivity while minimizing ecological footprints.

According to the Food and Agriculture Organization (FAO), global meat production is projected to reach 373 million tonnes in 2024, marking a 1.4% increase from the previous year. This growth underscores the need for efficient and sustainable livestock production systems. Feed additives, such as probiotics, enzymes, and organic acids, play a crucial role in improving feed conversion ratios, reducing methane emissions, and enhancing overall animal health.

Government initiatives worldwide are reinforcing this trend. For instance, the European Union’s Common Agricultural Policy (CAP) promotes sustainable farming practices, including the use of environmentally friendly feed additives. Similarly, India’s National Livestock Mission emphasizes the adoption of scientific feeding practices to boost productivity and sustainability.

Moreover, consumer preferences are shifting towards ethically produced and environmentally sustainable animal products. This change is prompting producers to adopt feed additives that not only improve animal performance but also align with sustainability goals.

Trends

Adoption of Methane-Reducing Feed Additives: A Key Trend in Sustainable Livestock Farming

A significant trend shaping the animal feed additives market is the increasing adoption of methane-reducing feed additives, aimed at mitigating greenhouse gas emissions from livestock. Methane, primarily produced during the digestive processes of ruminants like cows, is a potent greenhouse gas with a global warming potential approximately 80 times greater than carbon dioxide over a 20-year period. The agricultural sector, particularly livestock farming, contributes substantially to global methane emissions.

Innovative feed additives, such as 3-nitrooxypropanol (3-NOP), commercially known as Bovaer, have demonstrated efficacy in reducing enteric methane emissions. Studies indicate that incorporating Bovaer into cattle feed can lead to a reduction of approximately 30% in methane emissions per cow annually, equating to about 1.2 metric tons of carbon dioxide equivalent per cow. These findings underscore the potential of such additives in achieving more sustainable livestock production practices.

Government initiatives are bolstering the adoption of these environmentally friendly feed additives. For instance, Denmark has allocated 518 million Danish crowns (approximately USD 74 million) to support farmers in integrating methane-reducing additives into cattle feed, aligning with the nation’s goal to reduce overall emissions by 70% by 2030 compared to 1990 levels.

In the United Kingdom, major retailers and dairy cooperatives are collaborating with farmers to implement feed additives like Bovaer and seaweed-based supplements, aiming to produce “greener” milk and beef. These initiatives are part of broader efforts to meet net-zero targets and reduce the carbon footprint of the agricultural sector.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region solidified its position as the leading market for animal feed additives, commanding a substantial 46.8% share, equivalent to a market value of approximately USD 21.9 billion. This dominance is primarily driven by the region’s extensive livestock and aquaculture industries, coupled with a growing demand for high-quality animal protein.

Southeast Asian countries, including Vietnam, Thailand, and Indonesia, are emerging as key contributors to the market’s expansion. These nations are experiencing rapid growth in their livestock and aquaculture sectors, leading to increased adoption of feed additives to enhance animal health and feed efficiency.

The APAC region’s market growth is further bolstered by the rising awareness of sustainable farming practices and the need to meet the nutritional requirements of a growing population. As urbanization and income levels rise, consumers are increasingly demanding safe and high-quality animal products, prompting producers to invest in advanced feed solutions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ADM remains a leading player in the animal feed additives sector, known for its wide portfolio of amino acids, enzymes, and premixes. With operations in over 190 countries, the company focuses on improving animal nutrition and farm productivity. In 2024, ADM continued investing in sustainable feed solutions, particularly in Asia and Latin America. Its extensive global supply chain and R&D efforts help it respond effectively to regional feed demand trends and evolving regulatory requirements.

Ajinomoto plays a critical role in the animal feed additives industry, primarily through its production of essential amino acids such as lysine and threonine. The company leverages advanced fermentation technologies and operates globally with a strong presence in Asia. In 2024, it emphasized reducing environmental impact in feed production while enhancing efficiency. Ajinomoto’s commitment to precision nutrition and its partnerships with local feed manufacturers strengthen its foothold in the global livestock and poultry feed markets.

Alltech, a global leader in animal health and nutrition, offers a diverse range of feed additives including probiotics, enzymes, and yeast-based products. The company has operations in more than 120 countries and focuses heavily on natural, antibiotic-free additives. In 2024, Alltech expanded its presence in Europe and Southeast Asia through joint ventures and sustainability initiatives. The company is also known for its investments in traceability technologies and livestock productivity tools aligned with eco-conscious farming practices.

Top Key Players in the Market

- ADM

- Ajinomoto Co., Inc.

- Alltech, Inc.

- Lallemand Inc.

- BASF SE

- BIOMIN Holding GmbH

- Cargill, Incorporated

- Centafarm SRL

- Novonesis.

- DSM

- Evonik Industries AG

- Nutreco

- Adisseo

- Kemin Industries, Inc.

- Elanco

Recent Developments

In 2024, Ajinomoto Co., Inc. maintained its significant presence in the animal feed additives market, focusing on amino acid-based solutions that enhance livestock nutrition and productivity. The company, with a global workforce of approximately 34,862 employees, reported consolidated sales of ¥1,439.2 billion (around $10.05 billion USD).

Lallemand’s commitment to innovation is evident in its development of products like BACTOCELL, a probiotic feed additive authorized in the European Union for use in poultry, swine, and aquaculture. BACTOCELL contains live lactic acid bacteria (Pediococcus acidilactici CNCM I-4622 – MA 18/5M) and has been used for over 20 years to support intestinal health and digestive efficiency in animals.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 46.8 Bn |

| Forecast Revenue (2034) | USD 79.9 Bn |

| CAGR (2025-2034) | 5.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Antibiotics, Vitamins, Antioxidants, Amino Acids, Feed Enzymes, Feed Acidifiers, Phosphates, Carotenoids, Mycotoxin Detoxifiers, Flavors and Sweeteners), By Minerals (Non-Protein Nitrogen, Phytogenics, Preservatives, Probiotics, Others), By Source (Natural, Synthetic), By Form (Dry, Liquid), By Livestock (Swine, Poultry, Cattle, Aquaculture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ADM, Ajinomoto Co., Inc., Alltech, Inc., Lallemand Inc., BASF SE, BIOMIN Holding GmbH, Cargill, Incorporated, Centafarm SRL, Novonesis., DSM, Evonik Industries AG, Nutreco, Adisseo, Kemin Industries, Inc., Elanco |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |