Quick Navigation

Report Overview

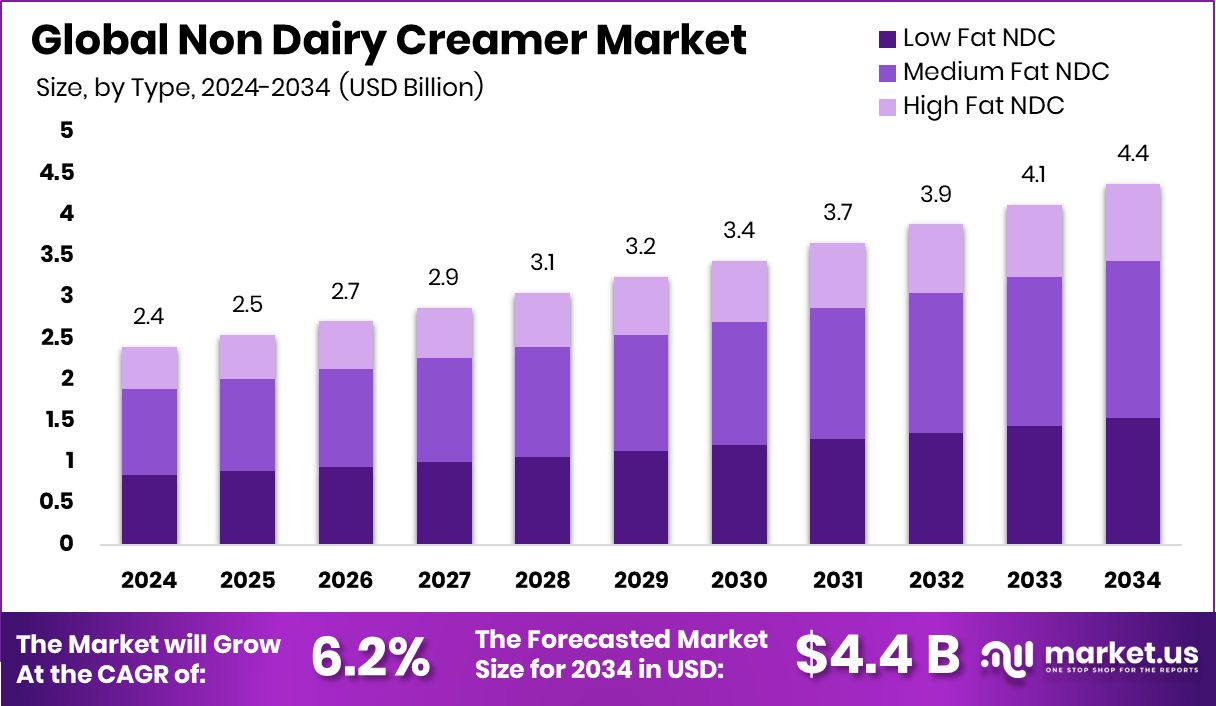

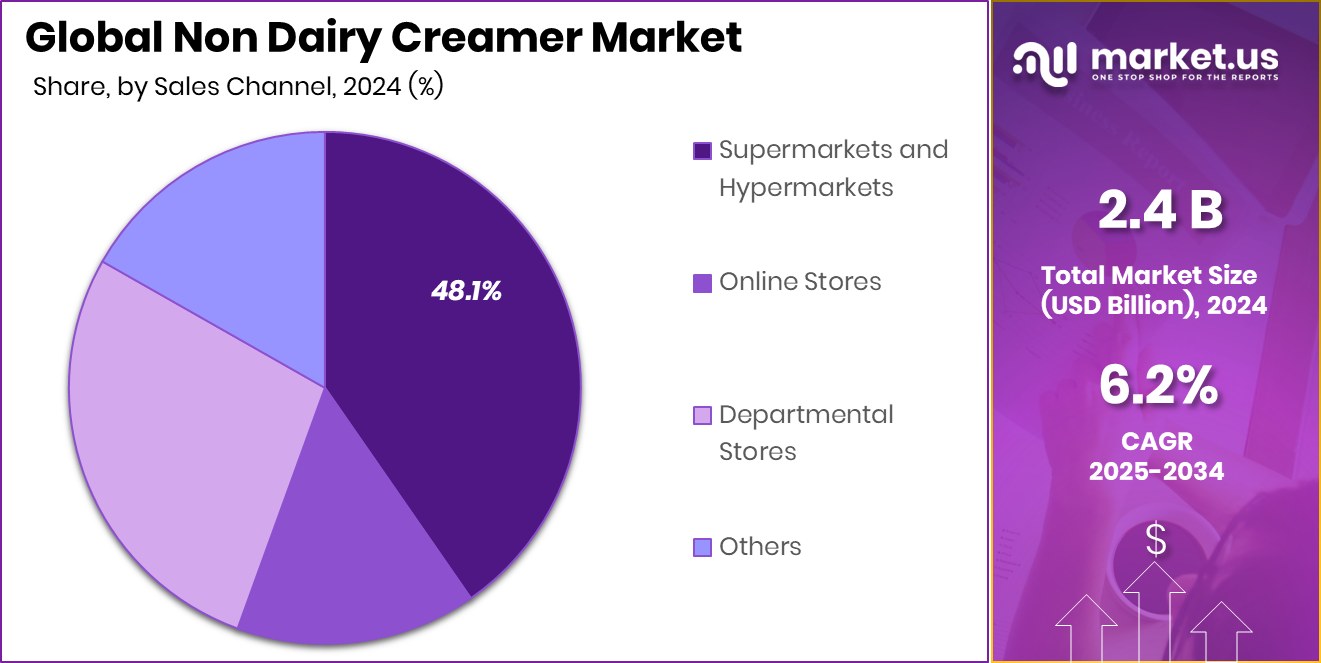

Global Non Dairy Creamer Market is expected to be worth around USD 4.4 billion by 2034, up from USD 2.4 billion in 2024, and grow at a CAGR of 6.2% from 2025 to 2034. USD 1.1 Bn in North America’s Non-Dairy Creamer Market reflects 46.9% dominance.

Non-dairy creamer is a powdered or liquid substitute for milk or cream, designed to provide the creamy texture and rich taste associated with dairy products without containing lactose. Typically made from vegetable oils, corn syrup solids, and various additives, it is popular among lactose-intolerant consumers, vegans, and those seeking shelf-stable alternatives to traditional cream.

The non-dairy creamer market is expanding rapidly as consumer preferences shift toward plant-based and lactose-free products. Rising awareness of lactose intolerance and vegan lifestyles is driving market demand. Product innovations such as flavored and organic creamers attract health-conscious consumers. The market is witnessing increased adoption in regions where dairy alternatives are gaining traction, particularly in North America and Europe.

The growing consumer focus on plant-based diets is a significant growth driver in the non-dairy creamer market. As more consumers opt for vegan and lactose-free products, the demand for plant-derived creamers, including soy, almond, and coconut-based options, is rising. Product diversification with innovative flavors and health-enhancing ingredients, such as probiotics and low-sugar formulations, further propels market growth.

The government plans to boost domestic palm oil production from 0.35 million tonnes (MT) to 1 MT by 2030 under the National Oil Palm Mission by expanding plantations by 0.1 million hectares (MH) annually over the next five to six years. In FY23, 42,000 hectares of new palm plantations were added, and at least 70,000 hectares are expected to be added in the current fiscal year.

Key Takeaways

- Global Non Dairy Creamer Market is expected to be worth around USD 4.4 billion by 2034, up from USD 2.4 billion in 2024, and grow at a CAGR of 6.2% from 2025 to 2034.

- In 2024, Medium Fat Non-Dairy Creamer held a dominant market share of 43.6%, driven by its versatile application across various beverages and bakery products.

- Powdered Non-Dairy Creamer accounted for 68.4% of the market in 2024, gaining popularity for its extended shelf life and convenient storage.

- Unflavored Non-Dairy Creamer secured 58.8% of the market share, preferred by consumers seeking neutral, versatile creamers.

- Plant-Based Milk emerged as the leading source in the Non-Dairy Creamer market, capturing 71.3% in 2024.

- Conventional Non-Dairy Creamers dominated the market, holding an impressive 86.9% share, attributed to widespread availability and affordability.

- Supermarkets and Hypermarkets accounted for 48.1% of the Non-Dairy Creamer sales, leveraging extensive distribution networks and product variety.

- With a 46.9% share, North America’s Non-Dairy Creamer Market leads at USD 1.1 Bn.

By Type Analysis

In 2024, Medium Fat NDC dominated with a 43.6% market share.

In 2024, Medium Fat NDC held a dominant market position in the By Type segment of the Non-Dairy Creamer Market, capturing a significant 43.6% share. This substantial market presence can be attributed to the growing consumer preference for medium-fat content products that provide a balanced texture and taste while maintaining a lower fat profile than full-fat alternatives.

Medium-fat NDC continues to gain traction among health-conscious consumers seeking dairy alternatives with a moderate fat content, aligning with dietary preferences and rising demand for plant-based options.

As a result, the segment is expected to sustain its leading market position in the near term, driven by expanding applications in food and beverage products and increasing consumer awareness regarding health and nutrition.

By Form Analysis

Powder form led the Non-Dairy Creamer Market, capturing a 68.4% share.

In 2024, Powder held a dominant market position in the By Form segment of the Non-Dairy Creamer Market, accounting for a substantial 68.4% share. The dominance of the powdered form is primarily driven by its extended shelf life, ease of storage, and versatility in various food and beverage applications.

Powdered non-dairy creamers are widely preferred in the food service sector, including coffee shops, bakeries, and quick-service restaurants, due to their convenient handling and cost-effectiveness. Additionally, the rising demand for plant-based, lactose-free creamers has further propelled the segment’s growth, solidifying its position as the leading form in the non-dairy creamer market.

By Flavor Analysis

Unflavored varieties accounted for 58.8% of the Non-Dairy Creamer Market demand.

In 2024, Unflavored held a dominant market position in the By Flavor segment of the Non-Dairy Creamer Market, capturing a notable 58.8% share. The preference for unflavored variants is driven by their broad applicability across diverse food and beverage products, allowing consumers to maintain the natural taste profile while achieving desired creaminess.

Unflavored non-dairy creamers are extensively used in coffee, tea, and bakery items, providing a neutral base without altering the original flavor. The segment’s strong market presence is further supported by the increasing demand for lactose-free and plant-based alternatives, solidifying its leadership within the non-dairy creamer market.

By Source Analysis

Plant-Based Milk emerged as the top source, securing 71.3% market share.

In 2024, Plant-Based Milk held a dominant market position in the By Source segment of the Non-Dairy Creamer Market, commanding a substantial 71.3% share. The segment’s strong performance is attributed to the rising consumer shift towards plant-based alternatives, driven by growing health consciousness and increasing lactose intolerance cases.

Plant-based milk creamers, derived from sources like almond, soy, and oat, have gained widespread acceptance as healthier, eco-friendly options compared to dairy-based counterparts.

Additionally, the expanding vegan population and the introduction of innovative plant-based formulations have further fueled the segment’s dominance, reinforcing its market leadership in the non-dairy creamer sector.

By Nature Analysis

Conventional nature products held 86.9% of the Non-Dairy Creamer Market segment.

In 2024, Conventional held a dominant market position in the By Nature segment of the Non-Dairy Creamer Market, securing a commanding 86.9% share. The extensive market presence of conventional non-dairy creamers is largely driven by their affordability, widespread availability, and established consumer acceptance across various regions.

These products are widely used in the food service industry, including cafes, restaurants, and institutional catering, due to their consistent quality and cost-effectiveness. Despite the growing trend toward organic and natural formulations, the conventional segment maintains its leading position, backed by robust demand from budget-conscious consumers and high-volume food manufacturers seeking reliable, shelf-stable non-dairy creamer solutions.

By Sales Channel Analysis

Supermarkets and Hypermarkets captured 48.1% of the Non-Dairy Creamer Market sales.

In 2024, Supermarkets and Hypermarkets held a dominant market position in the By Sales Channel segment of the Non-Dairy Creamer Market, accounting for a significant 48.1% share. The prominence of this distribution channel is attributed to its expansive reach, diverse product availability, and consumer preference for convenient, one-stop shopping experiences.

Supermarkets and hypermarkets effectively cater to a broad consumer base, offering a wide array of non-dairy creamer brands and formats, including both budget and premium options. Additionally, the increasing penetration of plant-based and lactose-free creamers within major retail chains has further reinforced the segment’s dominance, positioning it as the leading sales channel for non-dairy creamers in 2024.

Key Market Segments

By Type

- Low Fat NDC

- Medium Fat NDC

- High Fat NDC

By Form

- Powder

- Liquid

By Flavor

- Unflavored

- Flavored

- Vanilla

- Chocolate

- Coconut

- Hazelnut

- Others

By Source

- Plant-Based Milk

- Coconut Milk

- Oat Milk

- Almond Milk

- Macadamia Milk

- Others

- Vegetable Oil

- Palm Oil

- Coconut Oil

- Soybean Oil

- Others

By Nature

- Organic

- Conventional

By Sales Channel

- Supermarkets and Hypermarkets

- Online Stores

- Departmental Stores

- Others

Driving Factors

Rising Vegan Trend Boosts Non-Dairy Creamer Demand

The surge in veganism and plant-based diets is significantly driving the demand for non-dairy creamers globally. As consumers increasingly shift towards lactose-free and plant-derived products, the market for non-dairy creamers is experiencing robust growth. The rising health consciousness among individuals, coupled with the growing awareness of dairy alternatives, further fuels the demand for products made from almond, soy, coconut, and oat milk.

Additionally, the expanding vegan population, particularly in developed markets, has encouraged manufacturers to introduce innovative, nutrient-enriched, and flavored non-dairy creamer products. This trend is expected to continue gaining traction, creating substantial growth opportunities in the non-dairy creamer market in the coming years.

Restraining Factors

High Production Costs Hinder Non-Dairy Creamer Expansion

The high production costs associated with non-dairy creamers pose a significant restraint to market growth. Ingredients such as almond, soy, and oat milk require extensive processing and resource investment, driving up manufacturing expenses.

Additionally, sourcing quality plant-based raw materials can be cost-intensive, impacting the overall pricing of non-dairy creamers. This cost barrier can limit market penetration, especially in price-sensitive regions where consumers may opt for cheaper, dairy-based alternatives.

Furthermore, fluctuating prices of plant-based ingredients and supply chain disruptions further exacerbate the cost challenges. These factors collectively impede the widespread adoption of non-dairy creamers, posing a restraint to market expansion despite rising consumer demand for lactose-free products.

Growth Opportunity

Innovative Flavors Drive Non-Dairy Creamer Market Growth

The introduction of innovative and diverse flavors presents a substantial growth opportunity for the non-dairy creamer market. Consumers increasingly seek unique and exotic flavors, ranging from vanilla and caramel to matcha and hazelnut, to enhance their coffee and beverages.

Manufacturers are capitalizing on this trend by launching plant-based creamers infused with bold and trending flavors, attracting a broader consumer base. Additionally, the rising popularity of specialty coffee and flavored beverages is further fueling demand for flavored non-dairy creamers.

By catering to evolving taste preferences and introducing seasonal or limited-edition flavors, companies can effectively capture market share, expand their product portfolio, and drive growth in the highly competitive non-dairy creamer market.

Latest Trends

Innovative Flavors Expand Non-Dairy Creamer Appeal

In 2024, the non-dairy creamer market experienced a notable trend: the introduction of innovative and diverse flavors. Consumers increasingly sought unique taste experiences beyond traditional options, leading manufacturers to develop creamers infused with flavors like hazelnut, caramel, and seasonal spices. This diversification catered to evolving consumer preferences, particularly among those seeking plant-based and lactose-free alternatives.

The expansion of flavor offerings not only enhanced the appeal of non-dairy creamers but also positioned them as versatile additions to various beverages and recipes. As a result, the market witnessed increased consumer engagement and broadened its customer base, indicating a positive trajectory for continued growth in the non-dairy creamer sector.

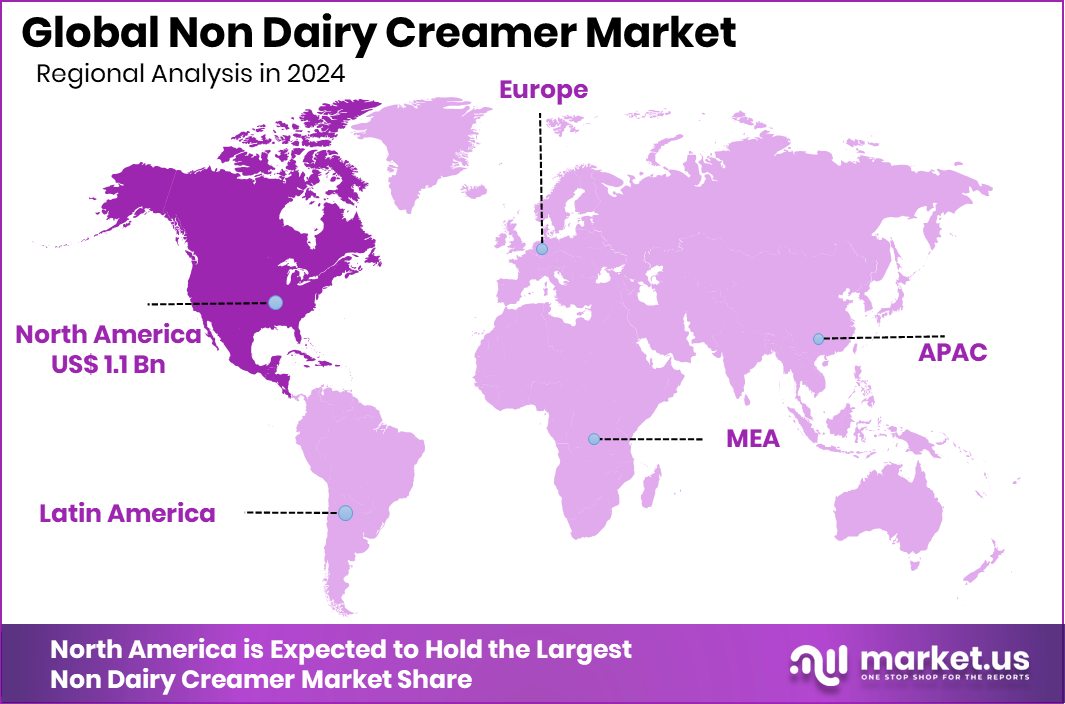

Regional Analysis

North America’s Non-Dairy Creamer Market reached USD 1.1 Bn, capturing 46.9% share.

In 2024, the Non-Dairy Creamer Market exhibited notable regional variations, with North America leading the market, holding a dominant 46.9% share and generating USD 1.1 billion. The region’s significant market position is attributed to the rising consumer inclination toward plant-based creamers, driven by increasing health awareness and lactose intolerance.

In Europe, the demand for non-dairy creamers remains steady, supported by the expanding vegan population and the presence of established food and beverage manufacturers. The Asia Pacific market is experiencing rapid growth due to increasing urbanization and the rising middle-class population adopting lactose-free and plant-based alternatives.

Meanwhile, the Middle East & Africa and Latin America markets are gradually expanding, propelled by growing consumer awareness and the introduction of innovative non-dairy creamer products.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Abbott Laboratories, renowned for its nutritional products, has maintained a strong presence in the non-dairy creamer segment through its specialized offerings. While primarily focused on health and wellness, Abbott’s non-dairy creamer products cater to consumers seeking lactose-free and plant-based alternatives. Their commitment to quality and innovation ensures that their products meet the evolving dietary needs of health-conscious consumers.

Califia Farms has solidified its position as a leader in the plant-based creamer market. In 2024, the company expanded its product line with the introduction of organic almond coffee creamers in flavors like Lavender, Brown Sugar, and Vanilla. These offerings, free from gums and oils, align with consumer preferences for clean-label products. Califia’s emphasis on innovation and sustainability continues to resonate with a growing base of health-conscious and environmentally aware consumers.

Chobani, traditionally known for its yogurt products, has made significant strides in the non-dairy creamer market. In 2024, the company launched its Zero Sugar Coffee Creamers in flavors such as Sweet Cream and Salted Caramel. These offerings cater to consumers seeking healthier, low-sugar alternatives without compromising on taste. Chobani’s commitment to quality and innovation has enabled it to capture a substantial share of the non-dairy creamer market, appealing to a broad spectrum of consumers.

Top Key Players in the Market

- Abbott Laboratories

- Califia Farms

- Chobani

- Danone

- Dean Foods

- Elmhurst 1925

- Fonterra

- FrieslandCampina

- Kraft Heinz

- Lactalis

- Meiji Dairies Corporation

- Nestlé

- Nutpods

- Oatly

- Rich Products Corporation

- Ripple Foods

Recent Developments

- In September 2024, Califia Farms unveiled a seasonal lineup of plant-based creamers, featuring flavors such as Pumpkin Spice Almond Creamer, Caramel Apple Crumble Oat Creamer, Maple Waffle Almond Creamer, and Sugar Cookie Almond Creamer.

- In September 2024, Chobani introduced Zero Sugar Coffee Creamers in two flavors: Sweet Cream and Salted Caramel. These creamers are crafted with farm-fresh cream and natural ingredients, catering to consumers seeking sugar-free options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.4 Billion |

| Forecast Revenue (2034) | USD 4.4 Billion |

| CAGR (2025-2034) | 6.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Low Fat NDC, Medium Fat NDC, High Fat NDC), By Form (Powder, Liquid), By Flavor (Unflavored, Flavored (Vanilla, Chocolate, Coconut, Hazelnut, Others)), By Source (Plant-Based Milk (Coconut Milk, Oat Milk, Almond Milk, Macadamia Milk, Others), Vegetable Oil (Palm Oil, Coconut Oil, Soybean Oil), Others), By Nature (Organic, Conventional), By Sales Channel (Supermarkets and Hypermarkets, Online Stores, Departmental Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Abbott Laboratories, Califia Farms, Chobani, Danone, Dean Foods, Elmhurst 1925, Fonterra, FrieslandCampina, Kraft Heinz, Lactalis, Meiji Dairies Corporation, Nestlé, Nutpods, Oatly, Rich Products Corporation, Ripple Foods |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |