Quick Navigation

Report Overview

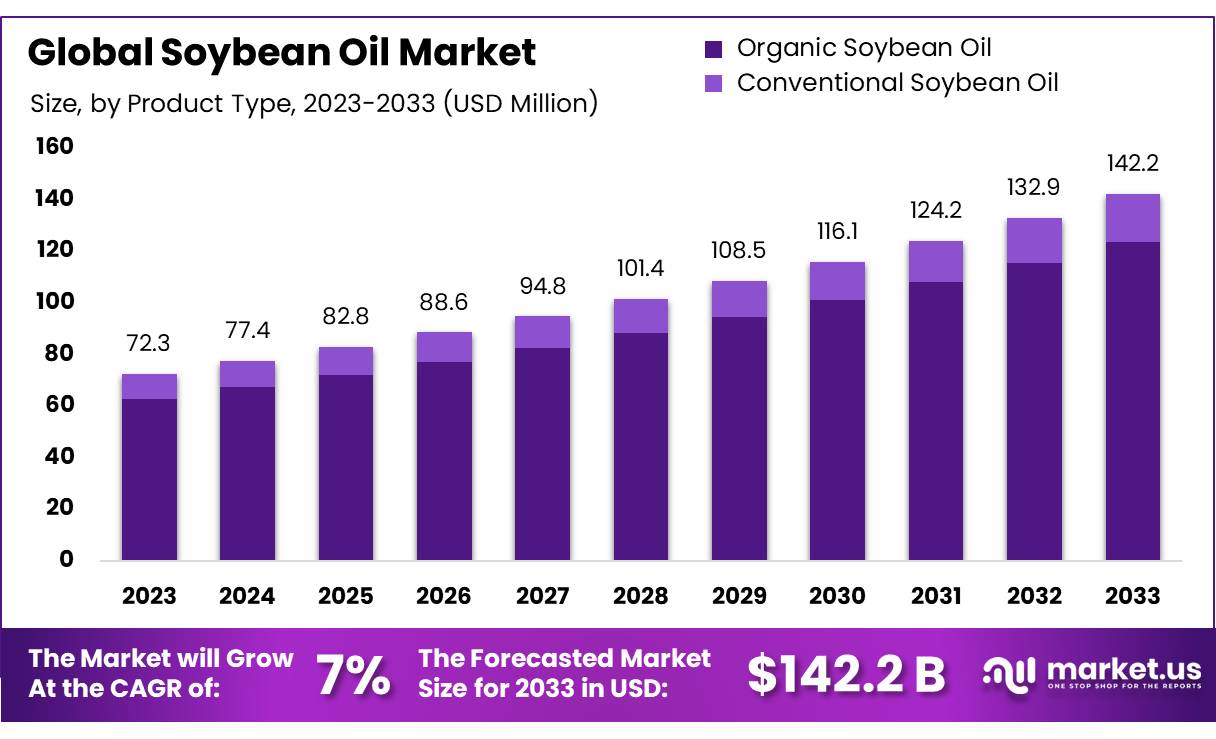

The Global Soybean Oil Market size is expected to be worth around USD 142.2 Bn by 2033, from USD 72.3 Bn in 2023, growing at a CAGR of 7.0% during the forecast period from 2024 to 2033.

Soybean Oil is a widely used edible vegetable oil extracted from the seeds of the soybean plant (Glycine max). It is one of the most popular oils globally due to its versatile use in cooking, food processing, and industrial applications. Soybean oil is rich in polyunsaturated fats, including omega-3 and omega-6 fatty acids, which are beneficial for heart health when consumed in moderation.

The U.S. alone contributed approximately 25% of the global production, making it the largest producer of soybean oil. Soybean oil is also used in non-food industries, such as biodiesel production, which has been growing due to environmental concerns and government initiatives promoting biofuels. As of 2023, global demand for soybean oil is projected to grow by about 3-4% annually, driven by its affordability, versatility, and the increasing popularity of plant-based oils.

The U.S. accounted for approximately 25% of the global supply, followed by Brazil at 23% and Argentina at 18% (FAO, 2023). The food processing sector remains the largest consumer of soybean oil, particularly in the production of cooking oils, margarine, snacks, and prepared foods. The increasing shift toward plant-based diets has further amplified the demand for vegetable oils, including soybean oil, in processed food manufacturing.

Government regulations and initiatives are also playing a significant role in shaping the market. For example, in the U.S., the Renewable Fuel Standard (RFS) mandates the use of biofuels, which has led to an increase in the use of soybean oil for biodiesel production.

The U.S. Environmental Protection Agency (EPA) reported that in 2023, soybean oil accounted for nearly 50% of the biodiesel feedstock used in the country. This has significantly boosted domestic soybean oil demand, with the U.S. biodiesel production rising by 8% year-over-year from 2022 to 2023 (EPA, 2023).

In terms of international trade, soybean oil continues to be a major export product for the U.S. In 2023, U.S. soybean oil exports were valued at USD 3.1 billion, with key markets including Mexico, Canada, and China. However, China’s import of U.S. soybean oil fell by 5% in 2023 due to domestic production increases.

In terms of innovation, companies like Cargill and ADM have been investing in soybean oil production technologies, focusing on improving oil quality and efficiency. In 2023, Cargill announced a USD 200 million investment in expanding its soybean crushing and oil refining operations in Brazil to meet the increasing demand from both food and biofuel sectors.

Key Takeaways

- Soybean Oil Market size is expected to be worth around USD 142.2 Bn by 2033, from USD 72.3 Bn in 2023, growing at a CAGR of 7.0%.

- Conventional Soybean Oil held a dominant market position, capturing more than a 87.3% share.

- Polyunsaturated Fats held a dominant market position, capturing more than a 66.3% share.

- Cooking & Frying held a dominant market position, capturing more than a 57.3% share.

- Commercial held a dominant market position, capturing more than a 73.3% share. This large share.

- Supermarket or Hypermarket held a dominant market position, capturing more than a 58.2% share.

- In 2023, APAC captured approximately 43.3% of the global market, valued at USD 31.3 billion.

By Product Type

In 2023, Conventional Soybean Oil held a dominant market position, capturing more than a 87.3% share. This high market share is attributed to the widespread use of conventional soybean oil in various industries, including food production, cooking, and industrial applications.

The affordability and availability of conventional soybean oil make it a popular choice for consumers and businesses alike. Over the years, this segment has consistently outperformed the organic segment, with steady growth in demand due to its low cost and large-scale production capabilities.

Organic Soybean Oil is a smaller but growing segment. In 2023, it represented a relatively modest share of the market, but it has shown significant growth in recent years. With increasing consumer preference for healthier and environmentally friendly products, organic soybean oil has witnessed a rise in demand.

The conventional soybean oil segment is expected to continue dominating the market, maintaining its large market share. However, organic soybean oil is projected to see further growth as consumer preferences shift towards healthier, sustainably produced products. The gap between the two segments may narrow slightly, driven by the increasing demand for organic options, but conventional soybean oil will likely remain the leading choice for most applications.

By Ingredients

In 2023, Polyunsaturated Fats held a dominant market position, capturing more than a 66.3% share. This significant share can be attributed to the wide acceptance of polyunsaturated fats as a healthier option for cooking and food preparation.

Polyunsaturated fats are considered heart-healthy, making them a popular choice among consumers who are increasingly aware of the importance of good fats in their diets. Due to their beneficial effects on cholesterol levels and cardiovascular health, polyunsaturated fats are commonly used in vegetable oils like soybean oil. As a result, this segment has seen consistent demand growth, particularly in markets where consumers prioritize heart health and wellness.

Omega-3 Fats, while not as dominant as polyunsaturated fats, have shown considerable growth in recent years. In 2023, omega-3 fats represented a smaller share of the market but are gaining popularity due to their numerous health benefits, including improved brain function, reduced inflammation, and heart disease prevention.

Vitamin E and Low Saturated Fats are also key ingredients in soybean oil, but they occupy a smaller share of the market. Vitamin E, known for its antioxidant properties, is increasingly being added to functional foods and supplements, contributing to its steady growth. Meanwhile, Low Saturated Fats, often highlighted as a selling point for health-conscious consumers, have seen moderate demand, especially as people continue to move away from diets high in saturated fats.

Polyunsaturated Fats will likely maintain their market leadership, but Omega-3 Fats are expected to experience an uptick in consumer interest. Both Vitamin E and Low Saturated Fats will continue to serve niche markets, with steady growth in areas focused on natural health products and functional foods.

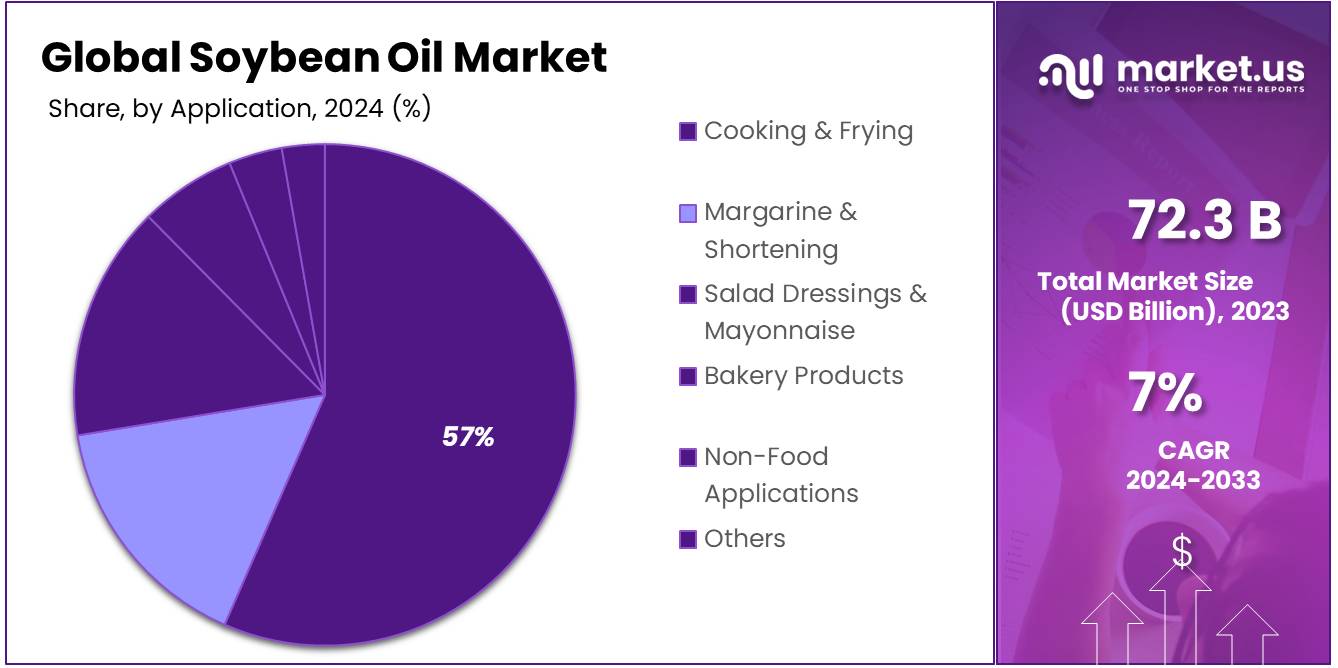

By Application

In 2023, Cooking & Frying held a dominant market position, capturing more than a 57.3% share. This large share is driven by the widespread use of soybean oil in everyday cooking and frying applications. Soybean oil’s affordability, neutral taste, and high smoke point make it a preferred choice for both households and foodservice businesses.

The demand for cooking and frying oils remains robust, especially in regions where deep-frying and pan-frying are common methods of preparing food. As health-conscious consumers continue to opt for oils with higher polyunsaturated fats, soybean oil’s position in the cooking and frying segment remains strong.

The Margarine & Shortening segment, while smaller in comparison to Cooking & Frying, has shown steady demand. In 2023, this segment benefited from the increasing use of soybean oil in the production of margarine and shortening products, commonly used in baking and food manufacturing. As consumers continue to seek lower-cost alternatives to animal fats, soybean oil remains a popular ingredient in margarine and shortening due to its desirable fatty acid profile and versatility.

Salad Dressings & Mayonnaise is another key application for soybean oil, with a growing presence in 2023. As more consumers opt for healthier, plant-based options, soybean oil is frequently used in the production of dressings and mayonnaise due to its light texture and mild flavor. This segment has benefitted from the rise in popularity of salads, healthy eating habits, and the increased demand for vegetarian and vegan-friendly products.

The Bakery Products segment has also shown consistent growth, particularly in the production of cakes, pastries, and bread. In 2023, soybean oil’s role in improving texture, moisture, and shelf life of baked goods supported its use in this application. As the demand for packaged bakery goods continues to rise, soybean oil remains a key ingredient for manufacturers looking to create affordable, high-quality products.

By End User

In 2023, Commercial held a dominant market position, capturing more than a 73.3% share. This large share is mainly due to the extensive use of soybean oil in the foodservice industry, including restaurants, fast-food chains, and food processing companies. Commercial users rely on soybean oil for its affordability, high smoke point, and versatility in frying, cooking, and food manufacturing.

The growing demand for ready-to-eat and convenience foods has further fueled the consumption of soybean oil in the commercial sector. As foodservice businesses look for cost-effective and high-quality oils, soybean oil remains the top choice for large-scale cooking and food production needs.

The Household segment, while smaller in comparison, continues to see steady demand. In 2023, more consumers are turning to soybean oil for home cooking due to its health benefits and neutral flavor. As families become more conscious of the types of oils they use in everyday cooking, soybean oil has gained favor, especially in households looking for an affordable yet healthier alternative to other oils.

The increasing trend of home cooking, particularly during the post-pandemic period, has kept the Household segment stable, with soybean oil being a staple in kitchens for a wide range of culinary applications, from sautéing to baking.

By Distribution Channel

In 2023, Supermarket or Hypermarket held a dominant market position, capturing more than a 58.2% share. This significant share is primarily due to the convenience and wide selection that these large retail outlets offer to consumers. Supermarkets and hypermarkets are the go-to places for families and individuals looking to purchase daily essentials, including cooking oils like soybean oil.

The availability of multiple brands, packaging sizes, and promotions in these stores makes them the preferred choice for consumers. Additionally, the ability to purchase in bulk at competitive prices has further contributed to the dominance of this distribution channel in the soybean oil market.

Convenience Stores, while representing a smaller share of the market, have experienced steady growth in 2023. These stores cater to customers who seek quick and easy shopping experiences, especially for smaller quantities of products like cooking oils. As more consumers look for convenient, on-the-go shopping options, the demand for soybean oil through convenience stores has risen.

The convenience store segment is particularly strong in urban areas and regions where consumers prioritize speed and convenience over large shopping trips. However, despite growth, convenience stores still account for a relatively small portion of the overall market.

Wholesalers also play a crucial role in the soybean oil distribution landscape, especially in supplying businesses and large-scale consumers. In 2023, this segment was stable, serving as a key channel for foodservice providers, manufacturers, and other commercial users who need bulk quantities of soybean oil at competitive prices. Wholesalers ensure that soybean oil is readily available for businesses that require larger quantities for production or resale. As the food service and manufacturing sectors continue to expand, wholesalers are expected to maintain a steady share of the market.

Key Market Segments

By Product Type

- Organic Soybean Oil

- Conventional Soybean Oil

By Ingredients

- Omega-3 Fats

- Vitamin E

- Low Saturated Fats

- Polyunsaturated Fats

By Application

- Cooking & Frying

- Margarine & Shortening

- Salad Dressings & Mayonnaise

- Bakery Products

- Non-Food Applications

- Others

By End User

- Commercial

- Household

By Distribution Channel

- Supermarket Or Hypermarket

- Convenience Stores

- Wholesaler

- Others

Drivers

Increasing Health Awareness Driving Soybean Oil Demand

One of the key driving factors for the growth of the soybean oil market is the rising consumer awareness around health and wellness. As people become more health-conscious, there is a growing preference for oils with better nutritional profiles.

Soybean oil, known for its heart-healthy benefits, has gained popularity in recent years, particularly because it is rich in polyunsaturated fats, including omega-3 fatty acids and vitamin E. This shift towards healthier dietary fats is a significant factor influencing the demand for soybean oil.

According to the American Heart Association (AHA), the consumption of polyunsaturated fats, like those found in soybean oil, can help reduce the risk of heart disease by improving cholesterol levels and reducing inflammation. The AHA states that replacing saturated fats with polyunsaturated fats in the diet can lower the risk of heart disease by up to 10%. As more consumers focus on heart-healthy eating habits, they are turning to oils like soybean oil, which is considered a healthier alternative to oils high in saturated fats, such as coconut oil or palm oil.

Government initiatives have also played a crucial role in promoting healthier oils. For instance, the U.S. Department of Agriculture (USDA) and other public health organizations have been actively educating the public about the benefits of replacing saturated fats with unsaturated fats. This public health push, combined with consumer-driven trends toward healthier eating, has led to a significant rise in the adoption of soybean oil, especially in households and commercial food industries.

In addition to its health benefits, soybean oil’s versatility and widespread availability make it an attractive option for various food applications, from cooking and frying to salad dressings and margarines. It is one of the most widely produced vegetable oils globally, which helps keep prices competitive and ensures a stable supply to meet growing consumer demand.

As health concerns around obesity, cardiovascular disease, and diabetes rise globally, the trend toward healthier oils like soybean oil is expected to continue. A report from the World Health Organization (WHO) shows that cardiovascular diseases are the leading cause of death globally, accounting for approximately 31% of all deaths. In response to these health challenges, the demand for oils with lower saturated fat content, like soybean oil, will likely increase.

Restraints

Rising Raw Material Costs Restraining Soybean Oil Market Growth

One of the major restraining factors for the soybean oil market is the increasing cost of raw materials. Soybean oil production heavily depends on the availability and price of soybeans, which are subject to fluctuations due to various factors like weather conditions, global supply chain disruptions, and changes in agricultural policies. As soybean prices rise, so too does the cost of soybean oil production, which can limit the affordability and accessibility of the oil in key markets.

The rise in raw material costs also puts pressure on food companies that rely on soybean oil as a key ingredient in products such as baked goods, salad dressings, margarine, and snacks. In many cases, these companies have to either absorb the increased costs, which can squeeze their profit margins, or pass the higher costs onto consumers. As a result, the price sensitivity of consumers in certain markets can limit the growth of the soybean oil segment, particularly in price-sensitive regions or during periods of economic uncertainty.

Additionally, the volatility of global soybean supply is a significant concern for soybean oil producers. The USDA reports that global soybean production in 2023 is estimated at 383 million metric tons, up slightly from 2022, but production in key growing regions like Brazil and Argentina has been impacted by droughts and other environmental factors. Any unexpected changes in the global supply of soybeans can lead to price volatility, making it difficult for manufacturers to forecast costs and plan for production.

Government policies, such as subsidies for alternative oils or changes in trade agreements, can also impact soybean oil’s competitiveness. For instance, in some regions, palm oil and canola oil are subsidized, which makes them cheaper alternatives to soybean oil. As a result, consumers and food manufacturers might shift towards these oils, especially if the price of soybean oil continues to rise due to increased raw material costs.

Opportunity

Growing Demand for Plant-Based and Sustainable Oils Creating Growth Opportunities for Soybean Oil

One of the most promising growth opportunities for the soybean oil market is the increasing consumer demand for plant-based and sustainable oils. As more individuals adopt plant-based diets, the preference for plant-derived oils, including soybean oil, has grown.

This trend is not only driven by health-conscious consumers but also by those concerned with environmental sustainability and the ethical treatment of animals. Soybean oil, which is considered a healthy and eco-friendly alternative to animal fats, is well-positioned to capitalize on this shift in consumer behavior.

In addition to the health and ethical motivations behind the rise in plant-based consumption, sustainability is playing a key role in this shift. Soybean oil is considered a more environmentally sustainable option compared to oils derived from animal sources or those that require intensive resource use, such as palm oil.

The sustainability of soybean oil, which can be produced with lower carbon emissions and requires less land use compared to animal-based fats, aligns with the growing consumer demand for environmentally friendly products. According to the United Nations Food and Agriculture Organization (FAO), plant-based oils have a significantly lower environmental footprint than animal-derived fats. This makes soybean oil an attractive option for environmentally conscious consumers and businesses aiming to reduce their carbon footprint.

Trends

Rise in Demand for Non-GMO and Organic Soybean Oil

A notable trend in the soybean oil market is the increasing demand for non-GMO (genetically modified organism) and organic soybean oil. This shift in consumer preference is driven by growing concerns over the potential health risks associated with GMOs, as well as the desire for more natural and sustainably sourced food products.

As consumers become more health-conscious and environmentally aware, they are opting for oils that are free from genetic modifications and produced with fewer chemicals, aligning with broader trends toward organic and natural foods.

This shift toward non-GMO and organic soybean oil is not just a consumer-driven trend; it is also being supported by government and industry initiatives aimed at promoting sustainable agriculture. The U.S. Department of Agriculture (USDA) has invested in organic farming programs and certifications, supporting farmers who grow crops like soybeans without the use of genetically modified seeds.

The USDA’s National Organic Program, for example, helps ensure that organic products meet strict standards, providing consumers with greater confidence in their purchase decisions. These government efforts, alongside consumer demand, are helping to boost the availability and market share of organic and non-GMO soybean oils.

The growth of e-commerce and direct-to-consumer sales channels has further contributed to the rise in demand for organic and non-GMO soybean oil. Online platforms are making it easier for consumers to access a variety of oils, including non-GMO and organic options. As more consumers embrace online shopping for food products, the convenience of purchasing specialized oils like organic soybean oil has helped drive its market growth.

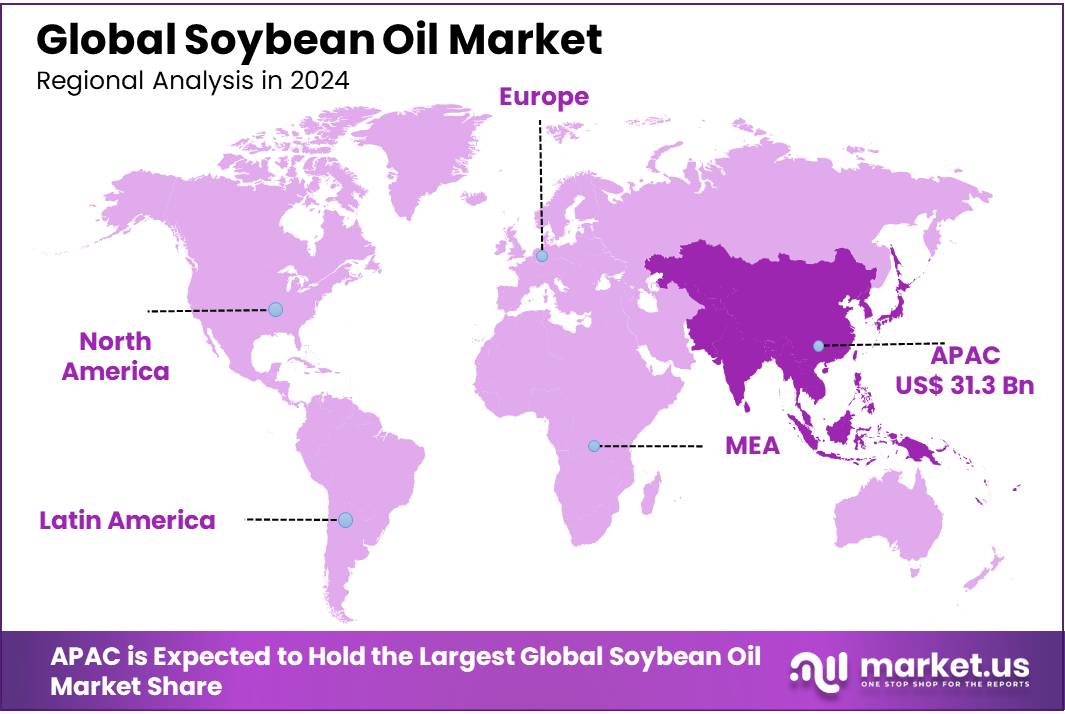

Regional Analysis

The global soybean oil market is experiencing significant regional variation, with the Asia Pacific (APAC) region holding the dominant share. In 2023, APAC captured approximately 43.3% of the global market, valued at USD 31.3 billion. This dominance is driven by the increasing consumption of soybean oil in countries like China and India, where it is used extensively in cooking, food processing, and manufacturing.

North America is another significant market for soybean oil, accounting for around 25% of the global share. The U.S., as a major producer and consumer, dominates this region, with soybean oil widely used in food applications, including frying, margarine, and salad dressings.

The North American market is also supported by a steady demand for organic and non-GMO soybean oil, driven by consumer preference for cleaner and healthier food products. The U.S. Department of Agriculture’s initiatives to promote sustainable agriculture have further boosted the region’s production and use of soybean oil.

Europe holds a smaller but steadily growing share of the soybean oil market. With an increased focus on sustainability and healthier fats, European consumers are opting for plant-based oils, including soybean oil, in cooking and food preparation. The region is projected to see moderate growth in the coming years as the demand for plant-based products rises.

Latin America and the Middle East & Africa are emerging markets, showing growth potential but contributing less to the overall market share. In these regions, increasing awareness of the health benefits of vegetable oils is driving demand, though they still lag behind in overall consumption compared to APAC and North America.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The soybean oil market is highly competitive, with several key players dominating production and distribution across global markets. Archer Daniels Midland Company (ADM), Bunge, Cargill, and Louis Dreyfus Company are among the leading global players in the industry, leveraging their vast supply chains, extensive processing capacities, and strong market presence.

ADM and Bunge are particularly dominant in North America, where they have substantial control over soybean processing and distribution. These companies are actively involved in sourcing, refining, and selling soybean oil to both domestic and international markets. Cargill, with its integrated supply chain, and Louis Dreyfus, a major commodity trader, also hold significant shares in both the food and industrial sectors, benefiting from their global footprint and robust logistical capabilities.

Other prominent players like Wilmar International Limited, Unilever, and DuPont are leading the soybean oil market with a focus on value-added products, sustainability, and innovative solutions. Wilmar, with a stronghold in the Asia Pacific region, is one of the largest agribusiness groups involved in soybean oil production, catering to the growing demand in countries like China and India.

Unilever, a major player in consumer goods, uses soybean oil in its food products and is also increasingly focused on sourcing oils sustainably. DuPont, known for its focus on biotechnology, plays a role in developing soybeans that are optimized for oil production, further enhancing its position in the market.

Additionally, regional players like AMAGGI Group, SunOpta, Arkema, and COFCO are also key contributors, with strong production capabilities, especially in Latin America and Asia. Companies such as Shandong Bohi Industry, Henan Sunshine Group Corporation, and Yihai Kerry Shandong Sanwei are significant in China and other parts of Asia, tapping into the growing regional demand for soybean oil.

Top Key Players

- Archer Daniels Midland Company

- Associated British Foods, plc

- Bunge

- Cargill, Inc.

- Louis Dreyfus Company

- Wilmar International Limited

- DuPont

- Unilever plc

- AMAGGI Group

- SunOpta, Inc.

- ADM

- Bunge Cargill

- Louis Dreyfus

- Wilmar International

- Arkema

- Cofco

- Donlinks

- Shandong Bohi Industry

- Henan Sunshine Group Corporation

- Nanjing Bunge

- Xiamen Zhongsheng

- Hunan Jinlong

- Sanhe hopefull

- Xiangchi Scents Holding

- Dalian Huanong

- Yihai Kerry Shandong Sanwei

Recent Developments

In 2023, ADM’s Oilseeds Processing segment, which includes soybean oil, reported revenues of USD 27.1 billion, reflecting a significant increase from USD 24.5 billion.

In 2023 Associated British Foods, plc soy-based oils are also used in industrial applications, and the company is expanding its reach in emerging markets where soybean oil consumption is growing due to changes in consumer preferences toward plant-based oils.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 72.3 Bn |

| Forecast Revenue (2033) | USD 142.2 Bn |

| CAGR (2024-2033) | 7% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Organic Soybean Oil, Conventional Soybean Oil), By Ingredients (Omega-3 Fats, Vitamin E, Low Saturated Fats, Polyunsaturated Fats), By Application (Cooking and Frying, Margarine and Shortening, Salad Dressings and Mayonnaise, Bakery Products, Non-Food Applications, Others), By End User (Commercial, Household), By Distribution Channel (Supermarket Or Hypermarket, Convenience Stores, Wholesaler, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Archer Daniels Midland Company, Associated British Foods, plc, Bunge, Cargill, Inc., Louis Dreyfus Company, Wilmar International Limited, DuPont, Unilever plc, AMAGGI Group, SunOpta, Inc., ADM, Bunge Cargill, Louis Dreyfus, Wilmar International, Arkema, Cofco, Donlinks, Shandong Bohi Industry, Henan Sunshine Group Corporation, Nanjing Bunge, Xiamen Zhongsheng, Hunan Jinlong, Sanhe hopefull, Xiangchi Scents Holding, Dalian Huanong, Yihai Kerry Shandong Sanwei |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |