Quick Navigation

Report Overview

The Global Compound Feeds Market size is expected to be worth around USD 796.2 Billion by 2034, from USD 507.8 Billion in 2024, growing at a CAGR of 4.6% during the forecast period from 2025 to 2034.

The compound feed concentrates industry comprises premixed nutritional formulations designed to complement animal diets, particularly for poultry, swine, cattle, and aquaculture. Concentrates and premixes supplement on-farm formulations, ensuring precise nutrition that enhances animal health, productivity, and feed conversion efficiency. In 2023, global feed production reached approximately 1.29 billion metric tons, demonstrating the massive scale of the sector.

Government Support & Policy Framework Substantial public initiatives have bolstered sectoral performance. The Department of Animal Husbandry & Dairying launched the National Livestock Mission (2014–15) focusing on feed and fodder development, and the Rashtriya Gokul Mission to conserve indigenous cattle breeds . Under the National Animal Disease Control Programme, 500 million cattle and 36 million female bovines are being vaccinated annually against FMD and brucellosis, supported by 100% central funding through 2024.

The Animal Husbandry Infrastructure Development Fund (AHIDF), initiated in 2020 with ₹15,000 crore, supports establishment of feed plants, dairy processing, and enabling private sector participation. These programmes are complemented by the Dairy Entrepreneurship Development Scheme, offering 25–33% subsidies for infrastructure development.

Growth Opportunities and Outlook Rapid urban dietary transitions, income growth, and expansion of commercial livestock farming are expected to sustain compound feed demand. USDA projections suggest India’s corn-based feed requirement could reach 20 million tonnes by 2034 and 122 million tonnes by 2050, contingent on income trends and cultivation technologies. Similarly, soybean meal imports may climb from 2.1 million tonnes in 2020 to 10 million tonnes by 2030 with rapid growth, signifying potential for backward integration.

Key Takeaways

- Compound Feeds Market size is expected to be worth around USD 796.2 Billion by 2034, from USD 507.8 Billion in 2024, growing at a CAGR of 4.6%.

- Pellets held a dominant market position, capturing more than a 53.6% share of the global compound feed market.

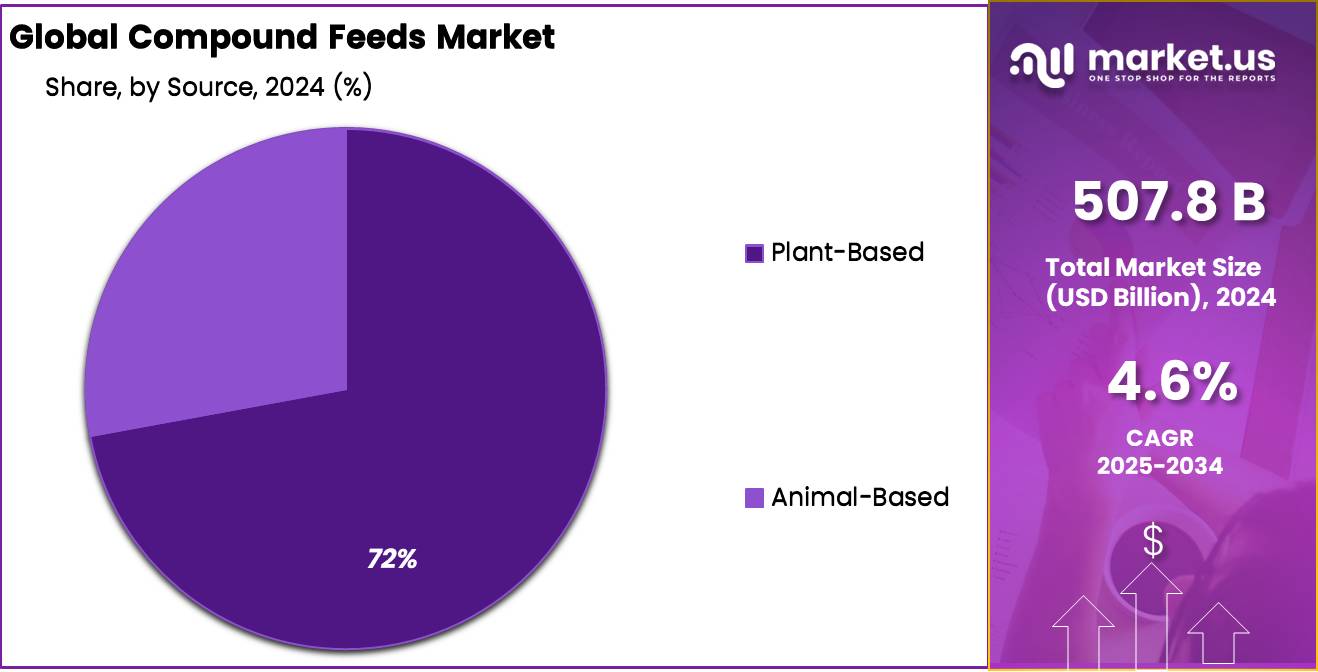

- Plant-Based held a dominant market position, capturing more than a 72.4% share of the compound feeds market.

- Solid held a dominant market position, capturing more than a 86.2% share of the compound feeds market.

- Feed Cereals held a dominant market position, capturing more than a 48.8% share of the compound feeds market.

- Poultry held a dominant market position, capturing more than a 46.3% share of the compound feeds market.

- North American compound feeds market stood out as the leading region, capturing 44.2% share of the global market, equivalent to approximately USD 224.4 billion.

By Form

Pellets dominate with 53.6% in 2024, driven by better digestibility and storage ease

In 2024, Pellets held a dominant market position, capturing more than a 53.6% share of the global compound feed market by form. Their widespread adoption is mainly due to better feed conversion ratios, improved palatability, and ease of handling during storage and transportation. Pelleted feed ensures more uniform nutrient intake among livestock, particularly in poultry and swine farming, where feed efficiency directly impacts productivity and profitability.

Additionally, pellets reduce feed wastage and improve animal digestion by breaking down fiber structures during the pelleting process. By 2025, this form is expected to maintain its leading position as more commercial farms move toward automated feeding systems that align better with pellet-based formulations. The consistent quality, longer shelf life, and suitability for bulk transport further reinforce the dominance of pellets in both developed and emerging markets.

By Source

Plant-Based feed dominates with 72.4% in 2024 as farmers prefer cost-effective and sustainable options

In 2024, Plant-Based held a dominant market position, capturing more than a 72.4% share of the compound feeds market by source. This dominance is mainly due to the wide availability, lower cost, and nutritional adequacy of plant-derived ingredients like soybean meal, corn, wheat, and rice bran. Farmers increasingly prefer plant-based feeds as they provide essential proteins and energy for livestock growth while being more affordable than animal-based alternatives.

The rise in vegetarian and plant-forward practices in animal farming, especially in dairy and poultry sectors, also supports this shift. In 2025, the demand for plant-based compound feeds is expected to remain strong, supported by government policies promoting sustainable agriculture and the growing emphasis on reducing dependency on animal-sourced raw materials. With feed costs making up over 60% of total livestock production expenses, plant-based feeds offer a reliable, scalable, and environmentally friendly solution for the industry.

By Form

Solid feed leads the market with 86.2% in 2024 thanks to its convenience and longer shelf life

In 2024, Solid held a dominant market position, capturing more than a 86.2% share of the compound feeds market by form. This strong preference is mainly driven by the ease of transport, storage, and handling that solid forms like mash, pellets, and crumbles offer across different livestock categories. Solid feed also allows better control over moisture levels, which helps reduce spoilage and prolong shelf life, especially in hot and humid climates.

Farmers across poultry, cattle, and aquaculture sectors continue to rely heavily on solid feed for its consistency and ability to deliver balanced nutrition in bulk quantities. By 2025, solid feed is expected to retain its leadership, as infrastructure and machinery at commercial farms remain largely designed for solid feed intake. Its cost-effectiveness and adaptability across species further strengthen its role as the standard choice in modern animal nutrition.

By Ingredient

Feed Cereals lead with 48.8% in 2024 as they remain a staple energy source for livestock

In 2024, Feed Cereals held a dominant market position, capturing more than a 48.8% share of the compound feeds market by ingredient. This strong share is due to the consistent use of cereals like corn, wheat, barley, and sorghum as primary energy sources across poultry, dairy, and aquaculture segments. These cereals are not only widely available but also offer balanced energy content that supports faster animal growth and efficient weight gain.

Their ease of processing and blending into mash or pellet form adds to their popularity among feed manufacturers. In 2025, the demand for feed cereals is expected to stay robust as grain-based rations continue to dominate in intensive livestock systems, particularly in Asia and Latin America. Their affordability and compatibility with protein-rich supplements further reinforce their role as a backbone of commercial feed formulations.

By Livestock

Poultry tops the chart with 46.3% in 2024 as rising meat and egg demand drives feed use

In 2024, Poultry held a dominant market position, capturing more than a 46.3% share of the compound feeds market by livestock. This leading position is largely due to the growing global demand for affordable animal protein in the form of chicken meat and eggs, especially in developing countries. Poultry farming requires consistent, high-energy feed to ensure quick growth cycles and high productivity, making compound feed essential for both broilers and layers.

The organized nature of poultry farming and the widespread use of automated feeding systems further support the high consumption of formulated feed. By 2025, this trend is expected to continue as urbanization and changing dietary habits push poultry consumption upward, keeping it as the largest user of compound feeds across all livestock categories.

Key Market Segments

By Form

- Pellets

- Mash

- Crumbles

- Others

By Source

- Plant-Based

- Animal-Based

By Form

- Solid

- Liquid

By Ingredient

- Feed Cereals

- Cakes & Meals

- Animal B-Products

- Others

By Livestock

- Poultry

- Ruminants

- Swine

- Aquaculture

- Others

Drivers

Rising Demand for Animal Protein Fuels Compound Feeds Growth

The Food and Agriculture Organization (FAO) reports that global food demand is expected to increase by 60% by 2050. Within this forecast, production of animal proteins is projected to grow at approximately 1.7% annually between 2010 and 2050. Specifically, meat production is anticipated to increase by nearly 70%, aquaculture by 90%, and dairy by 55%. These trends highlight the mounting requirement for optimized feed formulations that support higher productivity and sustainability in livestock farming.

Poultry and fish sectors, in particular, are expanding rapidly. FAO statistics show that farmed aquaculture reached 94.4 million tonnes in 2022, surpassing wild fish capture at 91 million tonnes. Average per capita fish consumption has more than doubled since the 1960s, reaching 20.7 kg annually. This shift underscores the essential nature of high-quality feed to support aquaculture’s growth and maintain environmental standards.

Governments around the world are responding through targeted initiatives to bolster feed efficiency. For example, China’s dietary guidelines issued in 2016 aim to reduce meat intake by 50% to curb emissions and improve public health. The country’s commitment to peak carbon emissions by 2030 and achieve carbon neutrality by 2060 is driving efforts to lower livestock farming’s environmental footprint, largely by enhancing feed conversion ratios. Additionally, the OECD–FAO Agricultural Outlook (2023–2032) indicates a link between input costs—such as fertiliser—and livestock feed expenses; a 1% rise in fertiliser prices corresponds to a 0.2% increase in overall food prices

Restraints

Feed Costs Squeeze Profit Margins Across Livestock Operations

One of the most significant restraining factors facing the compound feeds market is the steep share of production expenses absorbed by feed costs. According to the Food and Agriculture Organization, feed accounts for a substantial 60–80% of total livestock production costs, placing intense pressure on farming profitability. When farms manage tighter budgets, they often cut back on feed quality or volume, potentially undermining animal growth and output.

For instance, global commodity prices have soared: since 2005, soybean meal has surged by 67%, corn by 284%, and wheat by 225%. The steep increase in feed raw material prices disproportionately affects small and medium farms that lack scale economies. As FAO notes in its technical papers, these farms are particularly vulnerable, as feed expenses pose a direct risk to their financial viability.

Fertiliser price volatility further compounds the problem. The UN’s United Kingdom Food Security Report 2024 warns that disruptions in phosphate and potash supply chains have elevated fertilizer costs, which will likely ripple through to cereal prices and, by extension, feed ingredient costs. Given that feed cereals such as corn and wheat underpin most compound feeds, this trend adds another layer of cost risk.

Government responses have aimed to buffer farming communities from these shocks. For example, several G20 nations enacted fertilizer subsidy programmes in 2023, reducing farmer input costs by 20–30%. However, these measures are often temporary and lack precision, leaving feed cost dynamics largely in the hands of volatile commodity markets.

Opportunity

Insect-Based and Microbial Proteins Open New Doors for Feed Innovation

One of the major growth opportunities in the compound feeds market lies in the adoption of insect-based and microbial proteins, which can serve as sustainable, high-quality alternatives to traditional feed ingredients.

The United Nations Food and Agriculture Organization (FAO) has been advocating for insect proteins, stating that they offer excellent nutritional value and can be produced with lower environmental impact. Insects such as black soldier fly larvae can efficiently convert organic waste into up to 70% protein-rich biomass, making them a sustainable protein source for livestock and aquaculture. This approach aligns with a circular economy model by transforming low-value waste streams into high-value feed ingredients.

Similarly, single-cell proteins—derived from algae, yeast, bacteria, or fungi—present significant promise for animal feed. These microbial proteins can contain between 30% and 70% protein by dry weight and can be produced independently of traditional agricultural land, thereby reducing the strain on land and freshwater resources. The rapid growth rate of microorganisms allows feed producers to scale operations efficiently while maintaining nutritional consistency.

Trends

Precision Livestock Farming Takes Centre Stage in Compound Feeds

In 2024, global feed production increased by 1.2% to reach 1.396 billion tonnes, reflecting the livestock sector’s capacity to bounce back amid challenges like disease outbreaks and economic pressure. While this growth highlights scale, the real leap forward is in how feed is applied at the farm level.

According to USDA surveys, US farmers are increasingly integrating precision tools—like RFID ear tags, automated weighing, and health sensors—into livestock operations . One widely documented advancement is the use of smart ear tags in cattle and sheep, which continuously track behaviour and health, enabling early disease detection and improved growth monitoring.

The FAO stresses that precision farming—including PLF—is vital to doubling food production by 2050 while reducing environmental impact and resource use. These systems allow feed to be dosed precisely, tailored to each animal’s needs—reducing both waste and costs. Studies show that PLF adoption results in measurable gains: healthier animals, better feed conversion ratios, and reduced greenhouse gas emissions per unit of output.

Regional Analysis

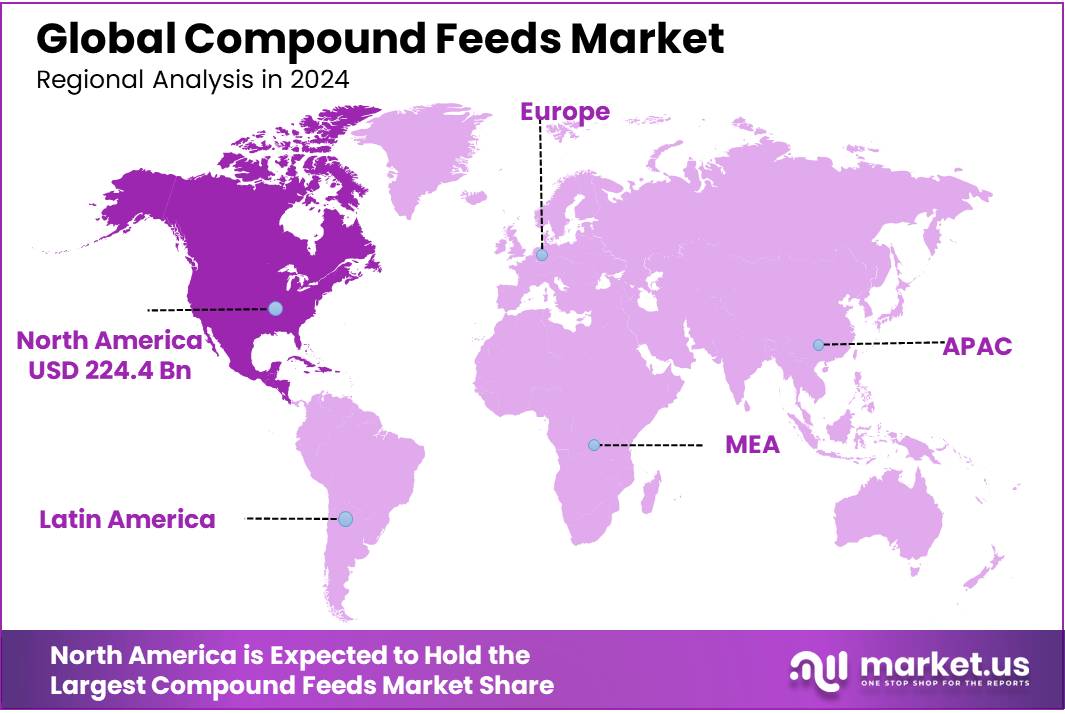

North America dominates with 44.2% share, representing a USD 224.4 billion market in 2024

In 2024, the North American compound feeds market stood out as the leading region, capturing 44.2% share of the global market, equivalent to approximately USD 224.4 billion in value. This leadership position is supported by well-established livestock sectors, advanced feed manufacturing infrastructure, and rising regional demand for animal protein.

North America’s dominance stems from its large livestock industry, high feed manufacturing capacity, strong growth in key segments like poultry and aquaculture, and proactive regulatory frameworks. These factors combine to secure its position as the most influential region in the global compound feeds market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ADM is a major global player in the compound feeds market, leveraging its vast grain sourcing and processing capabilities. The company supplies high-quality feed products for livestock, poultry, and aquaculture. In 2024, ADM strengthened its feed portfolio by investing in precision nutrition and sustainable ingredients. With a strong North American presence and expanding operations in Asia-Pacific and Latin America, ADM remains a trusted supplier for commercial farms seeking reliable, protein-rich, and environmentally conscious feed formulations.

Alltech is widely recognized for its innovative approach to animal nutrition, focusing on feed additives, yeast-based ingredients, and biotechnology. By 2024, the company had operations in over 120 countries, offering customized feed solutions that improve animal health and productivity. Its integrated farm solutions and investment in sustainable feed production have helped reduce methane emissions in livestock farming. Alltech’s emphasis on natural, traceable ingredients and global R&D centers places it at the forefront of performance-enhancing feed technologies.

BRF is one of the largest animal protein producers globally and operates its own vertically integrated feed manufacturing units. The company produces compound feed mainly for its poultry and swine operations, ensuring control over feed quality and supply chain efficiency. In 2024, BRF’s feed output supported its robust exports to Asia and the Middle East. The company continues to adopt sustainable sourcing and localized grain use, contributing to cost-effective feed solutions tailored to regional livestock markets.

Top Key Players in the Market

- ADM

- Alltech, Inc.

- BRF

- Cargill, Inc.

- De Heus Animal Nutrition

- Feed One Co.

- ForFarmers

- Guangdong Haid Group Co., Ltd

- Nutreco N.V.

Recent Developments

In 2024, ADM Animal Nutrition continued to play a vital role in the compound feeds sector by supplying high-quality premixes, amino acids, and specialty blends that support efficient animal growth. The division achieved an operating profit of US $19 million in Q3 2024—up 58% year-over-year—demonstrating recovery from earlier challenges

In 2024, Cargill reinforced its position as a key leader in the compound feeds market through strategic expansion, innovation, and operational adjustments. The company now operates 17 dedicated aqua feed mills across 11 countries, including six cold-water mills for salmon and 11 warm-water mills for shrimp and tilapia.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 507.8 Bn |

| Forecast Revenue (2034) | USD 796.2 Bn |

| CAGR (2025-2034) | 4.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Pellets, Mash, Crumbles, Others), By Source (Plant-Based, Animal-Based), By Form ( Solid, Liquid), By Ingredient (Feed Cereals, Cakes and Meals, Animal B-Products, Others), By Livestock (Poultry, Ruminants, Swine, Aquaculture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ADM, Alltech, Inc., BRF, Cargill, Inc., De Heus Animal Nutrition, Feed One Co., ForFarmers, Guangdong Haid Group Co., Ltd, Nutreco N.V |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |