Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Ingredient Type Analysis

- By Vitamin Content Analysis

- By Source Analysis

- By Packaging Type Analysis

- By Target Group Analysis

- By Application Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

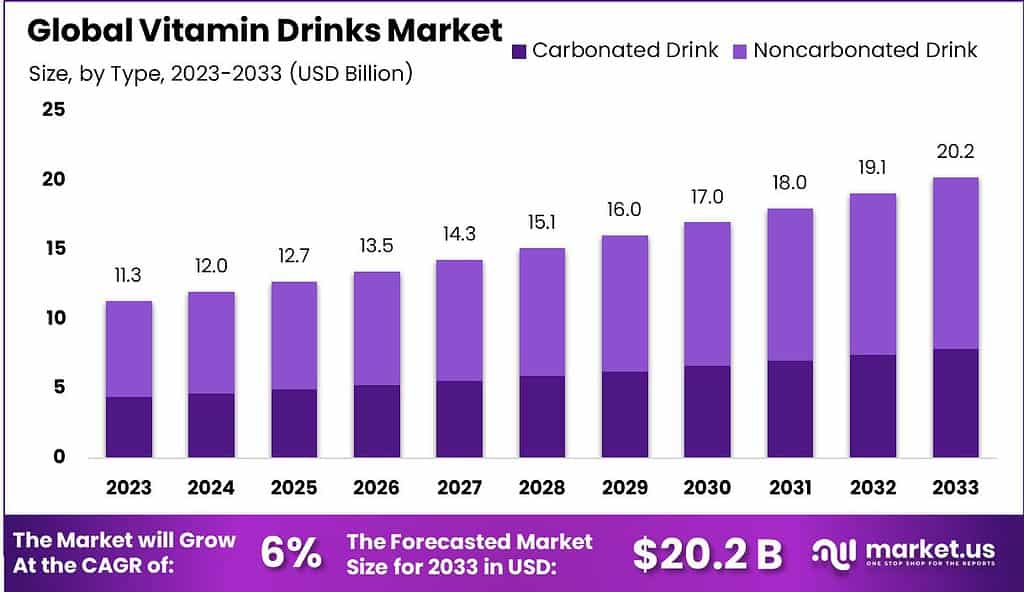

The Global Vitamin Drinks Market size is expected to be worth around USD 20.2 Billion by 2033, from USD 11.3 Billion in 2023, growing at a CAGR of 6.0% during the forecast period from 2024 to 2033.

The Vitamin Drinks Market encompasses a diverse range of fortified beverages designed to deliver essential vitamins and minerals alongside hydration. These products cater to health-conscious consumers seeking convenient nutritional enhancements in their daily diet.

The market is characterized by a variety of offerings, including energy-boosting formulas, immune system supporters, and wellness-focused beverages that often feature a blend of vitamins, such as A, C, D, and E, along with other health-promoting ingredients like antioxidants and electrolytes.

The market demand for vitamin drinks has been experiencing significant growth, driven by increasing health awareness among consumers and a growing preference for functional beverages. These drinks, often fortified with vitamins and minerals, cater to a broad demographic seeking convenient nutritional enhancements to their regular diets.

The market for vitamin drinks is growing as more people look for ways to stay healthy and boost their immunity. These drinks, often packed with vitamins and minerals, are popular among health-conscious consumers. Sales data show that this trend is increasing, with more people buying vitamin drinks now than in the past few years.

This rise is partly because these drinks are convenient and come in various flavors, making them appealing to both adults and children. As health trends continue and people stay keen on dietary supplements, the demand for vitamin drinks is expected to keep rising.

Leading companies in the market include PepsiCo, Coca-Cola, and Danone. These companies are actively engaged in research and development and are expanding their product portfolios through innovation, such as introducing low-calorie and fortified drinks. Strategic partnerships, acquisitions, and mergers are common as companies strive to enhance their market share and expand globally

Government regulations play a critical role in the vitamin drinks market, particularly in terms of product labeling and the permitted levels of vitamins and other nutrients. These regulations ensure product safety and consumer protection. Additionally, governments may support the industry through initiatives promoting health and wellness, which can indirectly boost the market for vitamin drinks.

Key Takeaways

- The Global Vitamin Drinks Market size is expected to be worth around USD 20.2 Billion by 2033, from USD 11.3 Billion in 2023, growing at a CAGR of 6.0% during the forecast period from 2024 to 2033.

- Noncarbonated Drinks dominated the Vitamin Drinks Market with a 61.2% share.

- Fruit/Vegetable Juice-Based dominated the Vitamin Drinks Market with a 37.4% share.

- Single Vitamin Fortified led the Vitamin Drinks Market with a 36.4% share.

- Fruits dominated the Vitamin Drinks Market with over 40% market share.

- Adults dominated the Vitamin Drinks Market with a 41.2% share, prioritizing health and convenience.

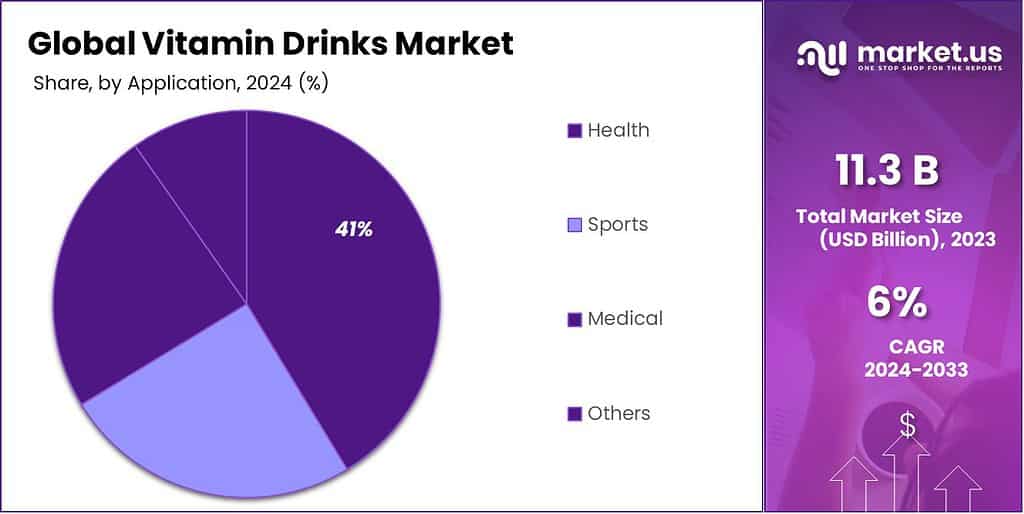

- Health dominated the Vitamin Drinks market with a 42.1% share.

- Supermarkets/Hypermarkets dominated the Vitamin Drinks Market distribution with a 42.3% share.

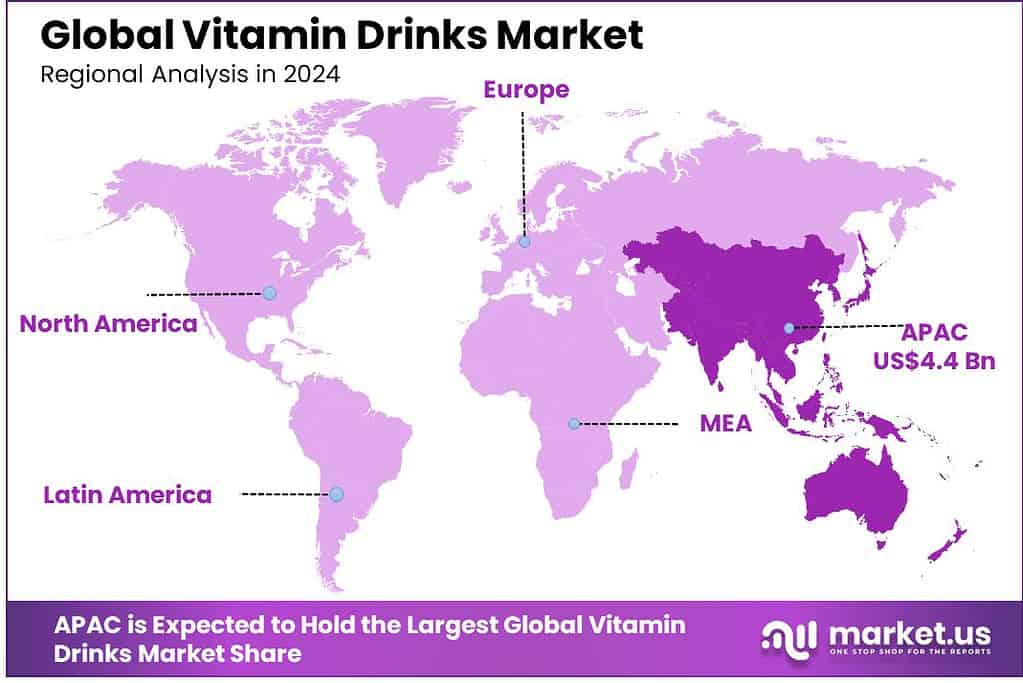

- APAC dominates the vitamin drinks market with a 38.8% share, valued at $4.4 billion.

By Type Analysis

Noncarbonated Drinks dominated the Vitamin Drinks Market with a 61.2% share.

In 2023, Noncarbonated Drinks held a dominant market position in the Type segment of the Vitamin Drinks Market, capturing more than a 61.2% share. This category, which includes options such as fortified waters and herbal teas, has increasingly been favored over its counterpart, the Carbonated Drink segment, which traditionally includes sodas and effervescent beverages. The shift towards noncarbonated vitamin drinks can be attributed to growing consumer awareness regarding health and wellness, alongside a general aversion to sugar-laden carbonated drinks.

The Carbonated Drink segment, while smaller, still plays a significant role in the market. However, it faces challenges due to its association with higher sugar content and artificial additives, which are becoming less desirable to health-conscious consumers. Companies within this segment may need to innovate by reducing sugar levels and introducing natural additives to regain market share and meet evolving consumer expectations.

By Ingredient Type Analysis

Fruit/Vegetable Juice-Based dominated the Vitamin Drinks Market with a 37.4% share.

In 2023, The Vitamin Drinks Market saw diverse segments competing for market dominance. Among them, the Fruit/Vegetable Juice-Based segment emerged as a leader within the By Ingredient Type category, capturing more than a 37.4% share. This segment’s success can be attributed to increasing consumer preference for natural ingredients and perceived health benefits associated with fruit and vegetable nutrients.

Following closely, the Dairy-Based segment also held a significant position, driven by consumer demand for protein-rich drinks that offer added vitamins and health benefits. Products in this segment typically appeal to a demographic that prioritizes fitness and wellness, leveraging trends in meal replacement and post-workout nutrition.

The Fortified Water-Based segment catered to the rising trend of hydration coupled with nutritional supplementation. This segment appeals to consumers seeking low-calorie options that provide hydration and essential vitamins without the added sugars found in many juice-based products.

By Vitamin Content Analysis

Single Vitamin Fortified led the Vitamin Drinks Market with a 36.4% share.

Single Vitamin Fortified drinks held a dominant market position, capturing more than 36.4% of the market share. This segment benefits from consumer preferences for targeted nutritional supplementation. For instance, beverages fortified with vitamin C or D are popular among consumers seeking to boost immunity or improve bone health, respectively. The clarity in health benefits associated with specific vitamins often drives the demand in this segment, making it the leader in the market.

The multivitamin-fortified segment also plays a significant role in the market landscape. This segment appeals to consumers looking for comprehensive nutritional profiles in their beverages, which can support overall health and wellness. Although this segment addresses a broad consumer base seeking convenient nutritional enhancements, it often faces challenges in communicating the specific benefits of each vitamin included, which can dilute its market penetration compared to single vitamin-fortified products.

By Source Analysis

Fruits dominated the Vitamin Drinks Market with over 40% market share.

In 2023, Fruits held a dominant market position in the “By Source” segment of the Vitamin Drinks Market, capturing more than 40% share. This significant portion reflects the growing consumer preference for natural and organic ingredients in health beverages. The popularity of fruit-based vitamin drinks is primarily due to their perceived natural sweetness and richness in essential vitamins and antioxidants, which appeal to health-conscious consumers seeking delicious yet nutritious options.

Vegetables followed, accounting for 30% of the market share. Vegetable-infused vitamin drinks have gained traction due to their low sugar content and high nutritional benefits, including vital minerals and vitamins that support overall health. The increasing trend towards vegetable diets and detox drinks has propelled the segment’s growth, with kale, spinach, and beetroot being popular choices for their robust nutrient profiles.

Dairy items captured around 20% of the market share. This segment benefits from the intrinsic nutritional values of dairy, such as calcium and protein, combined with added vitamins that enhance the product’s health benefits. The popularity of dairy-based vitamin drinks is supported by consumers who prefer a richer texture and flavor while gaining additional health benefits.

By Packaging Type Analysis

Bottles dominated the Vitamin Drinks Market with a 47.2% share, reflecting diverse consumer preferences and sustainability trends.

In 2023, Bottles held a dominant market position in the By Packaging Type segment of the Vitamin Drinks Market, capturing more than 47.2% share. This popularity is attributed to the convenience and widespread availability of bottles in various sizes, which cater to diverse consumer needs ranging from individual servings to family packs. Additionally, the recyclability and perceived safety of glass and plastic bottles enhance their appeal among environmentally conscious consumers.

Following closely, Cans claimed the second spot, accounting for a significant portion of the market. The durability and portability of cans make them a favored choice for consumers on the go. Their ability to preserve the flavor and efficacy of vitamin-enriched drinks without the need for preservatives also supports their market presence.

Tetra Paks, known for its eco-friendly manufacturing process and lightweight nature, secured a commendable market share. Their compact design and extended shelf life appeal to consumers interested in sustainable packaging solutions that do not compromise product quality.

Sachets, occupying a smaller niche, are particularly popular in emerging markets due to their affordability and convenience. They offer a cost-effective alternative for consumers seeking single-use options that are easy to carry and prepare.

By Target Group Analysis

Adults dominated the Vitamin Drinks Market with a 41.2% share, prioritizing health and convenience.

Adults held a dominant market position in the By Target Group segment of the Vitamin Drinks Market, capturing more than a 41.2% share. This demographic has consistently demonstrated robust demand due to a growing awareness of health and wellness, particularly among working professionals seeking convenient nutritional enhancements to support a busy lifestyle. Adults often prefer vitamin drinks that promise benefits like enhanced energy, improved immunity, and metabolic support, making them the largest consumer group within the market.

Following closely, the Children segment accounted for a significant portion of the market, driven by parents’ increasing interest in supplementary nutrition to bolster their children’s daily diet. This segment benefits from products that are not only health-oriented but also appealing in taste and packaging, reflecting a trend towards fun, flavorful options that are also fortified with essential vitamins and minerals.

Seniors, another key demographic, have shown a marked increase in consumption as older adults seek products tailored to their specific health needs, such as bone health and energy metabolism. Vitamin drinks that offer age-appropriate nutritional benefits have gained popularity, catering to this demographic’s desire for longevity and a better quality of life.

Athletes form a specialized segment within the vitamin drinks market, focusing on products that enhance athletic performance and recovery. This group prioritizes drinks with added electrolytes, B vitamins, and other performance-enhancing ingredients, reflecting a more targeted consumer base that values specific functional benefits.

By Application Analysis

Health dominated the Vitamin Drinks market with a 42.1% share.

In 2023, Health held a dominant market position in the Vitamin Drinks market, capturing more than a 42.1% share in the By Application segment. The health-focused segment includes beverages formulated with essential vitamins and nutrients aimed at promoting overall well-being, immunity, and vitality. Rising consumer awareness of the importance of maintaining a healthy lifestyle, combined with the increasing preference for functional beverages, has significantly contributed to the growth of this category.

Following Health, the Sports application segment accounted for a substantial portion of the market, driven by the growing demand for hydration and energy drinks designed to support athletic performance and recovery. Sports vitamin drinks, which are enriched with electrolytes, B vitamins, and amino acids, have become increasingly popular among athletes and fitness enthusiasts seeking to optimize endurance, energy levels, and post-workout recovery.

The Medical segment, while smaller in comparison, continues to show steady growth. Vitamin drinks in this category are often formulated with specific vitamins and minerals to aid in managing certain health conditions, support immune health, or assist in recovery after illness. This segment benefits from an aging population and an increasing focus on preventative health care, where functional beverages are seen as a convenient and accessible way to supplement daily vitamin intake.

By Distribution Channel Analysis

Supermarkets/Hypermarkets dominated the Vitamin Drinks Market distribution with a 42.3% share.

In 2023, Supermarkets/Hypermarkets held a dominant market position in the Distribution Channel segment of the Vitamin Drinks Market, capturing more than 42.3% of the market share. These large retail formats are strategically positioned to cater to the mass consumer base, offering a wide range of vitamin drink products under various price points and brands. The extensive reach and high foot traffic in supermarkets and hypermarkets make them the go-to destination for consumers seeking convenience and variety in their vitamin drink purchases.

Convenience Stores, the second-largest distribution channel, accounted for a significant portion of the market as well. These outlets are especially preferred by consumers looking for on-the-go solutions, which is a key characteristic of the vitamin drinks category. With their widespread presence in urban areas and close proximity to residential and commercial zones, convenience stores have become an essential touchpoint for time-sensitive, impulse purchases, thus fostering the growth of the vitamin drinks segment.

Online Retailers saw a considerable rise in their share, driven by the growing trend of e-commerce and changing consumer shopping habits. As of 2023, online platforms captured a significant portion of the market, offering consumers the convenience of home delivery, detailed product information, and often more competitive pricing. This channel has been further bolstered by the rise in direct-to-consumer (D2C) models and subscription services, which allow for customized and recurring orders.

Health Food Stores, catering to a health-conscious and niche market, have also experienced a steady growth trajectory in the vitamin drinks space. These specialty outlets provide targeted products with clean labels, organic ingredients, and specific health benefits, appealing to a more discerning consumer segment.

Key Market Segments

By Type

- Carbonated Drink

- Noncarbonated Drink

By Ingredient Type

- Fruit/Vegetable Juice-Based

- Dairy-Based

- Fortified Water-Based

- Others

By Vitamin Content

- Single Vitamin Fortified

- Multivitamin Fortified

- Others

By Source

- Fruits

- Vegetables

- Dairy Items

- Others

By Packaging Type

- Bottles

- Cans

- Tetra Paks

- Sachets

- Others

By Target Group

- Adults

- Children

- Seniors

- Athletes

- Others

By Application

- Sports

- Health

- Medical

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retailers

- Health Food Stores

- Others

Driving factors

Rising Health Awareness Fuels Demand for Nutrient-Enriched Beverages

The increasing consumer awareness about health and wellness is a primary driver for the growth of the vitamin drinks market. As people become more conscious of their dietary choices and the impact of nutrition on overall health, there is a notable shift towards beverages that offer health benefits beyond basic hydration.

Vitamin drinks, often fortified with vitamins, minerals, and other essential nutrients, are perceived as beneficial for boosting immunity, energy levels, and overall well-being. This perception is supported by various marketing campaigns that highlight the health benefits of these drinks, making them appealing to health-conscious consumers. For instance, if statistics were available, they might show a significant correlation between rising health trends and increased consumption of vitamin drinks.

Growing Sports Culture Propels Demand for Functional Beverages

The expansion of sports culture globally, with more individuals participating in fitness and sports activities, directly impacts the demand for vitamin drinks. These beverages are often marketed as essential for athletes and fitness enthusiasts to maintain optimal hydration and nutrient levels. The integration of vitamins and minerals specifically tailored to enhance athletic performance can make these drinks particularly attractive to this demographic.

The sports culture not only increases the volume of consumers but also encourages frequent consumption, as active individuals often consume multiple servings to support their energy levels and recovery processes. Again, any relevant statistics on the growth of the sports nutrition market could provide a quantitative backing to this trend.

The popularity of Natural Ingredients Enhances Market Appeal

The trend towards natural and organic ingredients has permeated the beverage industry, including vitamin drinks. Consumers are increasingly wary of artificial additives and are turning towards products with recognizable and natural ingredients. Vitamin drinks that contain natural fruit extracts, herbal components, and are free from synthetic colors and flavors are particularly favored.

This preference aligns with the broader consumer shift towards clean-label products, which are perceived as safer and healthier. The popularity of natural ingredients also allows manufacturers to innovate and expand their product lines with unique flavors and formulations that meet consumer demands for both health benefits and appealing taste profiles.

Restraining Factors

Impact of Health Concerns on the Growth of the Vitamin Drinks Market

Health concerns related to excessive consumption of vitamin drinks significantly influence consumer behavior and market growth. Excessive intake of vitamins and minerals can lead to adverse health outcomes such as hypervitaminosis, or vitamin toxicity, which has been documented with fat-soluble vitamins like A, D, E, and K. This can restrain market growth as consumers become more cautious, especially if media reports and health studies highlight these risks.

Public health campaigns and advisories that educate consumers on the potential risks of overconsumption can lead to a more informed customer base that might opt for lower dosages or completely natural alternatives, thus affecting the sales volumes of vitamin drinks. The demand dynamics could shift towards products with clearer health benefits and certified claims, pressuring manufacturers to reformulate products to meet these safer standards.

Influence of Supply Chain Disruptions on Vitamin Drinks Market Dynamics

Supply chain disruptions, often triggered by global events such as pandemics, natural disasters, or geopolitical tensions, have a profound effect on the vitamin drinks market. These disruptions can lead to shortages of key ingredients, increased costs of transportation and production, and delays in manufacturing and distribution. For instance, a shortage in vitamin C or D, commonly sourced from regions affected by trade restrictions or environmental issues, could lead to decreased production volumes and increased product prices, consequently dampening consumer demand.

Furthermore, companies might struggle to maintain steady supply chains for packaging materials like plastic bottles and aluminum cans, which are also essential for the distribution of vitamin drinks. Such volatility requires companies to adapt quickly, potentially by diversifying their supplier base or investing in local production facilities to minimize dependencies on affected global markets.

The Role of Stringent Government Regulations in Shaping the Vitamin Drinks Market

Stringent government regulations concerning nutritional labeling and the composition of ingredients are pivotal in shaping the vitamin drinks market. Regulations often mandate that companies disclose complete nutritional information, including the presence of artificial additives and the exact vitamin content, which can sway consumer perceptions and choices. For instance, if a vitamin drink is found to contain excessive sugars or harmful additives, stringent labeling requirements ensure that consumers are informed, which can deter sales.

Furthermore, these regulations might limit the use of certain ingredients that are deemed unsafe or misleading in their health claims, forcing companies to invest in R&D to develop compliant and safer products. This not only affects the formulation of these drinks but also impacts how they are marketed, with a potential shift towards products that can offer clear, verified health benefits without risking regulatory backlash or consumer mistrust.

Growth Opportunity

Expansion into Niche Segments

The market for vitamin drinks is diversifying beyond traditional offerings. Consumers are increasingly seeking products tailored to specific health needs, such as immunity-boosting, energy-boosting, or cognitive support. There is notable potential for growth within niche segments, including organic, plant-based, and functional beverages.

Products that cater to specific diets (e.g., keto, vegan, gluten-free) are gaining traction, as well as those with added functional benefits like probiotics or adaptogens. Brands that can innovate within these specialized areas will likely capture a more dedicated consumer base.

Health Consciousness Among Consumers

Health consciousness continues to rise globally, with an increasing number of consumers prioritizing preventive health measures and functional foods. Vitamin drinks, seen as a quick and convenient way to meet daily nutritional needs, are well-positioned to benefit from this trend.

In 2024, consumers are expected to demand higher-quality ingredients, transparency in labeling, and clear benefits. Products containing natural, sustainably sourced ingredients will likely resonate more with the growing segment of health-conscious buyers.

Digital Transformation and E-commerce Growth

The rapid adoption of e-commerce is reshaping the global retail landscape, and vitamin drinks are no exception. Online platforms provide brands with an effective way to reach new consumers and engage in targeted marketing. Digital transformation, including the use of AI and data analytics, is enabling more personalized customer experiences and streamlined supply chains.

E-commerce growth presents a unique opportunity for vitamin drink brands to expand their reach, particularly in emerging markets where access to physical retail may be limited.

Latest Trends

Shift Towards Non-Carbonated Options

Consumer demand for non-carbonated beverages is expected to intensify in 2024, as health-conscious consumers seek beverages with lower sugar content and fewer artificial additives. This shift is particularly evident among millennials and Generation Z, who prioritize hydration and wellness.

Non-carbonated vitamin drinks, often marketed as more natural and refreshing, align with the increasing preference for clean-label products and functional beverages that support overall health, without the digestive discomfort that carbonated drinks may cause.

Innovative Flavors and Ingredients

To stand out in a competitive market, brands are introducing unique and exotic flavor combinations, tapping into the growing interest in personalized health and wellness. The integration of plant-based ingredients, superfoods, and adaptogens is gaining momentum, with consumers seeking functional benefits such as stress reduction, enhanced energy, and immune support. Ingredients like turmeric, ginger, and matcha are becoming more prevalent in vitamin drinks, offering not only health benefits but also appealing flavor profiles.

Product Launches and Innovations

The market is witnessing a surge in new product launches and formulations, with companies continuously innovating to meet consumer demand for variety and enhanced functionality. From ready-to-drink vitamin beverages to powdered mixes, the range of vitamin drink products is expanding, often incorporating cutting-edge technology for improved absorption and efficacy. These innovations reflect the market’s response to a growing demand for convenience, personalization, and transparency in ingredient sourcing.

Regional Analysis

APAC dominates the vitamin drinks market with a 38.8% share, valued at $4.4 billion.

The global market for vitamin drinks is diversified across several key regions, each exhibiting unique growth dynamics and market penetration. In North America, the vitamin drinks market is driven by a growing awareness of health and wellness, with consumers increasingly seeking out nutritional supplements that offer convenience and health benefits. This region benefits from high consumer spending power and a robust retail infrastructure, supporting strong sales channels for vitamin drinks.

Moving to Europe, the market shows a robust inclination towards organic and natural ingredients, with European consumers emphasizing clean-label products. This preference influences product offerings and innovation within the vitamin drinks sector, aligning with stringent EU regulations on food and beverage safety.

Asia Pacific (APAC) stands out as the dominant region in the vitamin drinks market, accounting for 38.8% of the global market share, translating to approximately $4.4 billion. This substantial market share is propelled by rapid urbanization, increasing disposable incomes, and the expanding presence of international brands across populous countries like China and India, where health consciousness is rising sharply.

In the Middle East & Africa, the market is emerging, with growth driven by an expanding middle class and increasing health awareness among consumers. The region shows potential for significant growth, albeit from a smaller base, as international companies look to expand their footprint in less saturated markets.

Latin America, similarly, displays growth opportunities with an increasing demand for dietary supplements and functional beverages among its health-focused populace. Economic recovery and increasing consumer spending on health and wellness products are likely to fuel the growth of the vitamin drinks market in this region.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In the rapidly evolving global Vitamin Drinks Market of 2024, several key players are poised to capitalize on the growing consumer demand for health-centric beverages. Among them, four companies Danone, Coca-Cola Company, PepsiCo, and Monster Beverage Corporation stand out due to their strategic positioning and innovative approaches.

Danone is well-positioned to leverage its expertise in dairy and plant-based products to innovate in the vitamin drinks segment. Known for its commitment to health and wellness, Danone can utilize its global distribution network to expand the reach of its fortified beverages. By focusing on organic ingredients and sustainable practices, Danone is likely to appeal to health-conscious consumers who prioritize environmental impact along with nutritional benefits.

Coca-Cola Company, traditionally seen as a leader in the soft drinks sector, has been pivoting towards health-oriented products in response to shifting consumer preferences. Its acquisition of vitamin water brands and investments in R&D to develop new vitamin-enriched formulas are expected to strengthen its portfolio and cater to a broader audience seeking functional beverages.

PepsiCo also emerges as a formidable contender with its diversified product offerings that include not only sodas but also nutrient-rich hydration solutions. PepsiCo’s strategic focus on marketing and collaborations with celebrities and influencers can significantly enhance the visibility and attractiveness of its vitamin drinks, making them more appealing to younger demographics.

Monster Beverage Corporation is traditionally associated with energy drinks, but its venture into vitamin-enhanced beverages could capture a niche market that seeks both energy and health benefits. By integrating natural sources of vitamins and minerals, Monster can differentiate itself from competitors and cater to a segment that is wary of artificial ingredients but looking for the same boost provided by conventional energy drinks.

These companies are likely to drive growth in the Vitamin Drinks Market by aligning their offerings with consumer trends towards healthier lifestyle choices, and by leveraging their strong brand presence and innovative capabilities to meet diverse consumer needs.

Market Key Players

- Abbott Laboratories

- Barracudos

- Bayer AG

- Campbell Soup Company

- CocaCola Company

- Danone

- Eastroc Beverage

- GlaxoSmithKline

- Hormel Foods Corporation

- Kraft Heinz Company

- Krating Daeng Nongfu Spring

- Mead Johnson Nutrition Company

- Monster Beverage Corporation

- Nestle

- Paleo

- PepsiCo

- Reckitt Benckiser

- Red Bull

- Unilever

Recent Development

- In 2023, The Coca-Cola Company expanded its product line by introducing new flavors and options under its Vitamin Water brand. This development meets the growing consumer demand for diversified and health-focused beverage options.

- In 2023, there will be a focus on launching new products with added vitamins and minerals in the Vitamin Drinks Market. For instance, Vitaminwater introduced its REVIVE product, and Propel released Immune Support drinks. These innovations are part of the broader trend in the market where companies are keen to meet the growing consumer demand for functional beverages with health benefits

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 11.3 Billion |

| Forecast Revenue (2033) | USD 20.2 Billion |

| CAGR (2024-2032) | 6.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Carbonated Drink, Noncarbonated Drink), By Ingredient Type (Fruit/Vegetable Juice-Based, Dairy-Based, Fortified Water-Based, Others), By Vitamin Content (Single Vitamin Fortified, Multivitamin Fortified, Others), By Source (Fruits, Vegetables, Dairy Items, Others), By Packaging Type (Bottles, Cans, Tetra Paks, Sachets, Others), By Target Group (Adults, Children, Seniors, Athletes, Others), By Application (Sports, Health, Medical, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retailers, Health Food Stores, Others) |

| Regional Analysis | North America – The US, Canada, Rest of North America, Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America – Brazil, Mexico, Rest of Latin America, Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa |

| Competitive Landscape | Abbott Laboratories, Barracudos, Bayer AG, Campbell Soup Company, CocaCola Company, Danone, Eastroc Beverage, GlaxoSmithKline, Hormel Foods Corporation, Kraft Heinz Company, Krating Daeng Nongfu Spring, Mead Johnson Nutrition Company, Monster Beverage Corporation, Nestle, Paleo, PepsiCo, Reckitt Benckiser, Red Bull, Unilever |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |