Quick Navigation

Report Overview

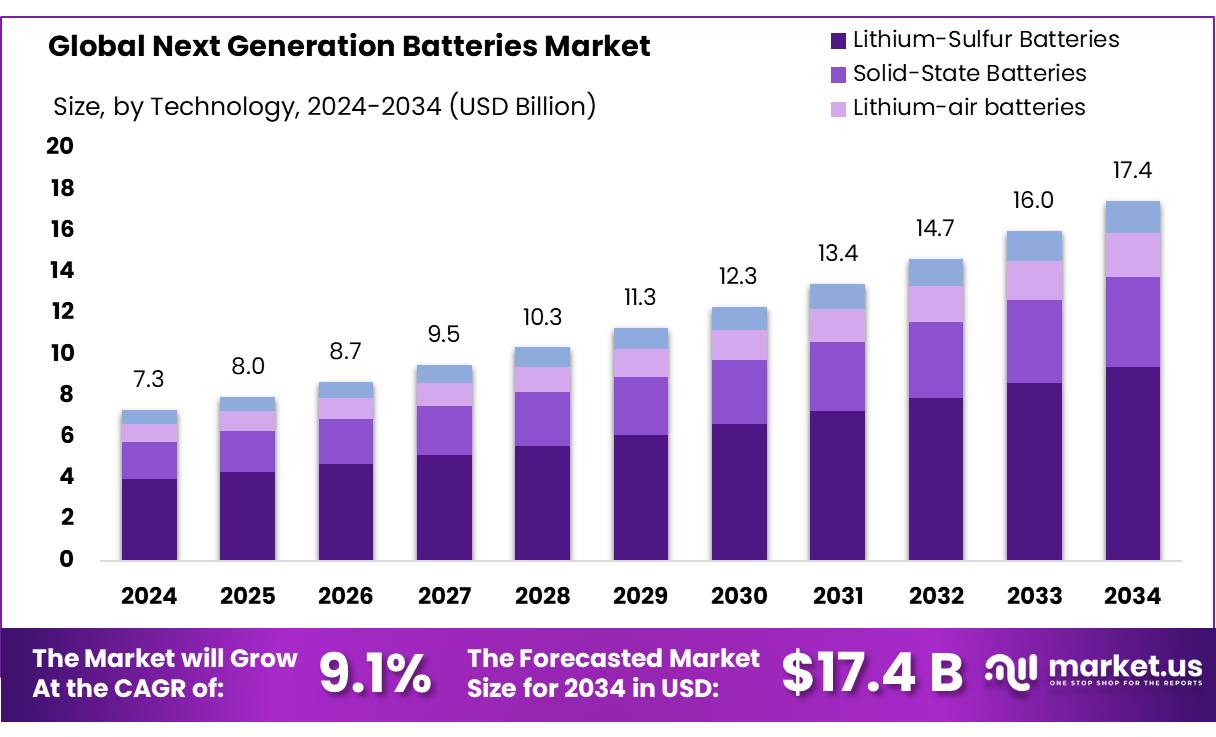

The Global Next Generation Batteries Market size is expected to be worth around USD 17.4 Bn by 2034, from USD 7.3 Bn in 2024, growing at a CAGR of 9.1% during the forecast period from 2025 to 2034.

The global next-generation batteries market is experiencing steady growth, fueled by the rising demand for advanced energy storage solutions, especially in the electric vehicle (EV) and renewable energy sectors. As industries and governments shift towards cleaner energy, the need for innovative battery technologies is becoming increasingly critical.

Next-generation batteries, including solid-state, lithium-sulfur, and sodium-ion batteries, are gaining traction due to their superior energy density, enhanced safety features, and improved performance compared to traditional lithium-ion batteries. These advancements are essential to support the transition to more sustainable energy systems and meet the growing demand for efficient energy storage.

Several factors are fueling this growth, including heightened concerns about environmental impact, government incentives promoting green technologies, and significant advancements in battery technologies. Consumers are increasingly drawn to EVs as a cleaner alternative to traditional vehicles, contributing to the rapid rise in sales.

Next-generation batteries, such as solid-state, lithium-sulfur, and sodium-ion batteries, are essential for supporting the evolving electric vehicle market. These batteries offer higher energy density, enhanced safety, and better performance compared to conventional lithium-ion batteries, addressing key challenges faced by internal combustion engines and enabling longer driving ranges for electric vehicles. As the electric vehicle market continues to grow, the demand for more efficient, sustainable battery solutions will intensify, propelling the next-generation batteries market forward throughout the forecast period.

Key Takeaways

- Next Generation Batteries Market size is expected to be worth around USD 17.4 Bn by 2034, from USD 7.3 Bn in 2024, growing at a CAGR of 9.1%.

- Solid-State Batteries held a dominant market position, capturing more than a 53.5% share.

- Electric Vehicles (EVs) held a dominant market position, capturing more than a 47.4% share.

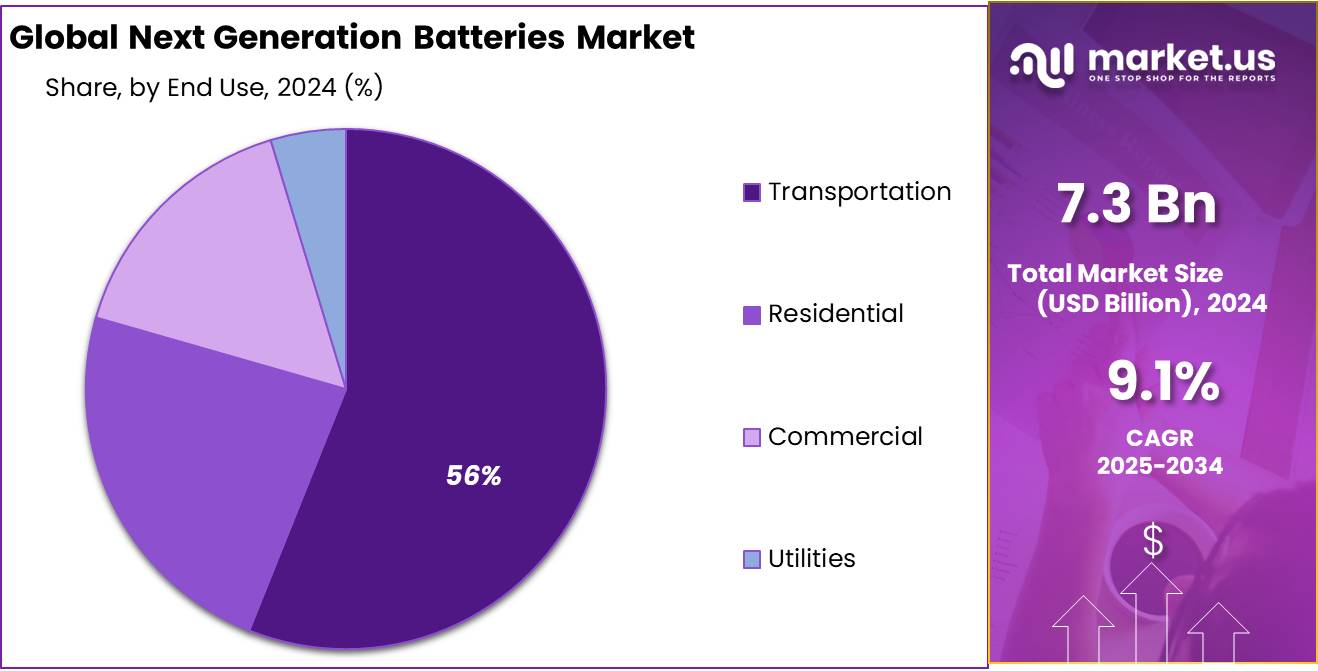

- Transportation held a dominant market position, capturing more than a 56.6% share.

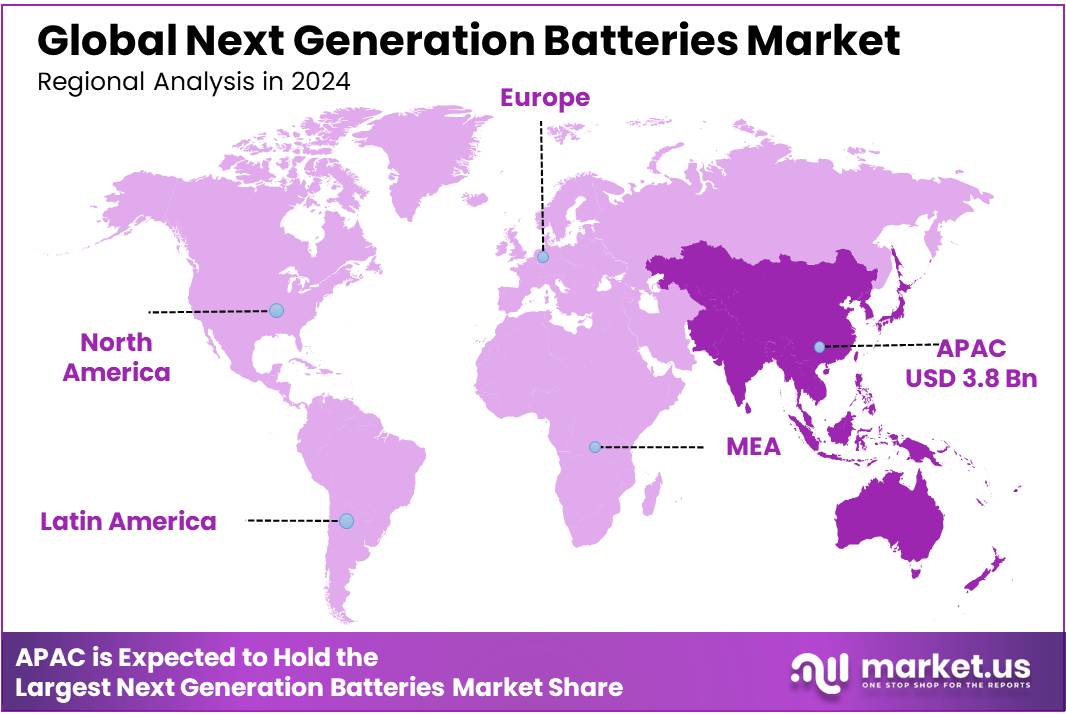

- Asia Pacific (APAC) dominated the Next Generation Batteries Market, capturing a significant 51.2% share.

By Technology

In 2024, Solid-State Batteries held a dominant market position, capturing more than a 53.5% share, as they gained significant traction in the next-generation battery space. The primary driver behind this growth is their potential to offer higher energy densities and improved safety compared to conventional lithium-ion batteries.

Lithium-Sulfur Batteries followed as the second leading technology in the market in 2024, capturing a noteworthy share due to their lighter weight and high energy density, which makes them a strong candidate for applications like aerospace, electric vehicles, and portable electronics.

Lithium-air Batteries, although still in the early stages of development, hold a lot of promise for the future. Their theoretical energy densities far exceed those of lithium-ion and even lithium-sulfur batteries, which positions them as an exciting technology for high-energy applications.

Lastly, Flow Batteries represent a niche but growing segment in the next-generation battery market. While they are not yet as widely adopted as lithium-based technologies, flow batteries offer advantages in large-scale energy storage applications, such as grid storage and renewable energy integration.

By Application

In 2024, Electric Vehicles (EVs) held a dominant market position, capturing more than a 47.4% share, reflecting the growing adoption of electric mobility worldwide. The increasing demand for EVs, driven by environmental concerns, government incentives, and advancements in battery technology, has led to substantial growth in this application. The rise in EV adoption is also supported by improvements in next-generation batteries, which provide longer ranges, faster charging times, and enhanced performance compared to traditional lithium-ion batteries.

Consumer Electronics follows as another major application, holding a significant portion of the market in 2024. With the continuous demand for high-performance gadgets such as smartphones, laptops, tablets, and wearables, next-generation batteries are becoming increasingly important. These advanced batteries offer improved energy density and longer battery life, which are essential for consumer electronics, where power efficiency and compactness are key.

Energy Storage Systems (ESS) are becoming increasingly crucial in the transition toward renewable energy. These systems use next-generation batteries to store energy from intermittent sources like solar and wind, ensuring a stable power supply when generation is low. In 2024, ESS accounted for a significant share of the market, driven by the growing need for grid stability and the push towards sustainable energy solutions.

Aerospace and Defense applications, while smaller in market share compared to EVs and consumer electronics, are still seeing increasing interest in next-generation batteries, particularly for their high energy density and reliability in critical situations. In 2024, this sector continued to adopt advanced battery technologies, including solid-state and lithium-sulfur batteries, to power everything from satellites to unmanned aerial vehicles (UAVs).

By End Use

In 2024, Transportation held a dominant market position, capturing more than a 56.6% share of the next-generation batteries market. This sector’s dominance is primarily driven by the booming electric vehicle (EV) industry, which has seen rapid growth as countries move toward decarbonization and sustainable transport solutions.

Residential end use also represents a growing segment of the next-generation batteries market. As consumers increasingly seek energy independence and sustainable living solutions, next-generation batteries are being utilized in home energy storage systems. These systems, powered by advanced battery technologies, allow homeowners to store excess energy from renewable sources like solar panels, which can then be used when demand is high or when renewable generation is low.

Commercial end use is also expanding, driven by businesses’ increasing interest in reducing energy costs and adopting cleaner technologies. Next-generation batteries are being integrated into commercial energy storage systems, helping businesses store energy from renewable sources, manage peak loads, and improve energy reliability.

Finally, Utilities are seeing increased adoption of next-generation batteries to stabilize the grid and store large amounts of energy from renewable sources. As the energy sector shifts toward more decentralized and sustainable energy generation, utilities are investing in energy storage systems that can help balance supply and demand.

Key Market Segments

By Technology

- Lithium-Sulfur Batteries

- Solid-State Batteries

- Lithium-air batteries

- Flow Batteries

By Application

- Electric Vehicles (EVs)

- Consumer Electronics

- Energy Storage Systems (ESS)

- Aerospace and Defense

By End Use

- Transportation

- Residential

- Commercial

- Utilities

Drivers

Government Support and Environmental Initiatives

The increasing demand for next-generation batteries is driven by a variety of factors, with government support and environmental initiatives playing a key role in accelerating innovation and adoption. The transition towards clean and sustainable energy has become a global priority, and next-generation batteries, such as solid-state and lithium-sulfur batteries, are at the forefront of this transformation. Governments worldwide are implementing policies and funding programs to support the development and commercialization of advanced battery technologies that can power everything from electric vehicles (EVs) to renewable energy storage systems.

Governments recognize that transitioning to clean energy requires not just generating renewable power but also ensuring that there are reliable and efficient means of storing that energy. This has led to significant investments in the next-generation battery sector.

For example, in the U.S., the Department of Energy (DOE) has allocated over $5 billion through its Advanced Vehicle Technologies and Energy Storage programs to help scale up battery technology and manufacturing capabilities. These initiatives are not only supporting technological advancements but also aiming to lower the cost of production and make these technologies commercially viable.

Similarly, the European Union has set ambitious goals for reducing carbon emissions, including a target to become the world’s first climate-neutral continent by 2050. In 2020, the European Commission proposed a €1 billion battery innovation program, the European Battery Alliance, to ensure the EU becomes a global leader in battery production and technology. The EU aims to produce up to 30% of global battery demand by 2030, and this is expected to be made possible through government-backed research and development projects.

Governments are also focusing on creating a stronger supply chain for critical materials used in battery production. With the growing demand for electric vehicles and renewable energy storage systems, securing the raw materials needed to produce these batteries—such as lithium, cobalt, and nickel—has become a strategic priority. In response, the U.S. and EU have been working to create more resilient supply chains for these critical materials through partnerships with mining companies and establishing domestic production capabilities.

Restraints

High Production Costs and Material Supply Challenges

Solid-state batteries, for example, are hailed for their potential to provide greater energy storage and faster charging times, but the cost of producing these batteries is still extremely high. According to a report from the U.S. Department of Energy, while solid-state batteries could theoretically lower costs in the long run, the manufacturing process is complex, and the materials used, like solid electrolytes, are expensive to produce. This makes it difficult to scale up production and bring down costs, limiting their commercial viability. Even though companies like Toyota are investing heavily in solid-state battery development, experts predict that it will take years, possibly even decades, to achieve mass production at a cost that is competitive with current lithium-ion batteries.

Another major issue is the reliance on rare materials like cobalt, nickel, and lithium, which are critical for the production of high-performance batteries. The extraction and processing of these materials can be costly and environmentally damaging, raising concerns about the sustainability of large-scale battery production.

According to a report by the World Bank, the demand for critical minerals such as lithium is expected to rise by over 400% by 2040, driven primarily by the transition to electric vehicles and renewable energy storage. This surge in demand puts pressure on the supply chain, and fluctuations in the availability of these materials can significantly impact battery production costs.

The high production costs of next-generation batteries also extend to the manufacturing infrastructure. Building the necessary factories and supply chains to produce these advanced batteries at scale requires substantial investment. The U.S. government, through initiatives like the Advanced Battery Manufacturing and Recycling program, is providing funding to support the development of manufacturing facilities for next-generation battery technologies. However, despite this support, the infrastructure costs are still high, and it will take significant time and resources to achieve the economies of scale needed to lower production costs.

Governments are aware of these challenges and are taking steps to address them. The European Union, for example, has been investing in research projects aimed at finding alternative materials for batteries, as well as improving battery recycling technologies. The European Commission’s European Battery Alliance is working to ensure that Europe can produce its own supply of critical materials and reduce dependency on imports from less stable regions. This includes funding for mining, recycling, and the development of new technologies to make battery production more sustainable.

Opportunity

Rising Demand for Electric Vehicles (EVs) and Clean Energy Storage

One of the most exciting growth opportunities for next-generation batteries lies in the rapidly expanding electric vehicle (EV) market and the increasing need for efficient, sustainable energy storage solutions. As governments and industries around the world push for decarbonization and a shift to renewable energy, next-generation batteries are seen as a critical enabler for this transformation.

According to the International Energy Agency (IEA), global EV sales are expected to reach 18 million units by 2030, representing about 30% of the total vehicle market share. With this surge in EV adoption, the demand for advanced battery technologies, which can deliver higher energy density, faster charging times, and longer life spans, will continue to rise.

In addition to EVs, the shift to renewable energy sources such as solar and wind is pushing the need for more efficient and affordable energy storage systems. Next-generation batteries, such as lithium-sulfur and solid-state technologies, have the potential to store large amounts of energy more efficiently than current lithium-ion batteries. This is particularly important as solar and wind power, despite their benefits, are intermittent by nature. To ensure a reliable and stable power supply, energy generated from these sources needs to be stored and released when demand is high or when weather conditions are unfavorable.

The European Union is equally committed to clean energy and sustainability, with the European Green Deal aiming to reduce net greenhouse gas emissions by 55% by 2030. As part of this initiative, the European Battery Alliance was created to ensure the region has the manufacturing capability to meet the growing demand for batteries used in electric vehicles and energy storage. The EU has allocated significant funding to battery research and development, particularly focusing on enhancing battery performance and reducing reliance on critical materials like lithium and cobalt. These efforts are expected to drive innovation in the battery sector, opening up new opportunities for next-generation battery technologies.

Trends

Advancements in Solid-State Batteries

One of the most promising trends in the next-generation battery sector is the development of solid-state batteries (SSBs). These batteries are seen as the next frontier in energy storage technology, offering a host of benefits over traditional lithium-ion batteries, such as higher energy density, improved safety, and longer life spans. Solid-state batteries replace the liquid electrolyte used in conventional batteries with a solid electrolyte, which enhances the performance and stability of the battery. This trend is gaining traction due to its potential to revolutionize various industries, including electric vehicles (EVs), consumer electronics, and renewable energy storage.

Another key benefit of solid-state batteries is their safety. Traditional lithium-ion batteries have been known to catch fire or explode in extreme conditions due to the flammability of their liquid electrolytes. Solid-state batteries, on the other hand, are much less prone to thermal runaway because their solid electrolytes are non-flammable. This makes them a safer option for applications where safety is a top priority, such as in electric vehicles, aerospace, and medical devices.

Safety concerns have been a major roadblock to the widespread adoption of electric vehicles. With more EVs on the road, ensuring that their batteries are safe is critical. Solid-state batteries could be the solution, as they offer a safer and more reliable alternative to liquid-based electrolytes. The improved safety features are one reason why automakers and battery manufacturers are so excited about the potential of solid-state batteries.

Governments are aware of the potential of solid-state batteries and are investing heavily in their development. In the United States, the Department of Energy (DOE) has allocated funding for research and development in solid-state battery technology, with the goal of reducing the cost of production and improving the performance of these batteries.

Regional Analysis

In 2024, Asia Pacific (APAC) dominated the Next Generation Batteries Market, capturing a significant 51.2% share, valued at approximately USD 3.8 Billion. The region’s strong market position can be attributed to rapid advancements in electric vehicle (EV) manufacturing, energy storage solutions, and the increasing adoption of renewable energy sources. Countries like China, Japan, and South Korea are leading the charge, with China alone accounting for a substantial portion of global EV production and battery demand.

North America follows with a strong share in the market, driven by the growing electric vehicle industry, particularly in the U.S. The Biden Administration’s infrastructure plan, which includes investing in EV charging stations and battery manufacturing, has created substantial growth opportunities for battery companies. The U.S. Department of Energy continues to fund projects related to next-generation battery technologies, fueling innovation in the sector.

Middle East & Africa and Latin America are emerging regions, witnessing a growing focus on renewable energy adoption and infrastructure development, though their market share remains relatively smaller compared to APAC, Europe, and North America.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Next Generation Batteries market is dominated by a mix of established global players and emerging innovators, all contributing to the evolution of battery technologies. 24M is a notable player in the market, focusing on the development of lithium-ion batteries with a semi-solid design, which significantly reduces manufacturing costs while enhancing performance.

Ambri Inc. is pushing forward with its liquid metal battery technology, which is designed to offer low-cost, long-life storage solutions, especially for grid-scale applications. Meanwhile, BYD Company Ltd., a leader in electric vehicle and energy storage solutions, has been expanding its efforts in next-generation battery technologies, particularly in the development of solid-state and lithium-sulfur batteries.

AESC Group Ltd., which has been focusing on solid-state battery technology for electric vehicles, and LG Chem, a major supplier of high-performance lithium-ion batteries for consumer electronics, electric vehicles, and energy storage systems. Panasonic Corporation, another major player, is making strides in solid-state battery research in collaboration with automakers like Toyota. On the emerging front, SES AI Corporation and Solid Power Inc. are actively advancing solid-state batteries, which promise to significantly increase energy density and improve safety compared to conventional lithium-ion solutions.

Sion Power and Phinergy are key innovators in the lithium-air and metal-air battery space, both of which have the potential to revolutionize energy storage by providing higher energy densities. ESS Tech, Inc., with its focus on iron flow batteries, is also addressing the long-duration storage challenges, targeting commercial and utility-scale applications. Companies like Toshiba Corporation and Mitsubishi Chemical are also working to develop next-generation energy storage technologies, with a particular emphasis on enhancing the performance and scalability of solid-state batteries.

Top Key Players

- 24M

- AESC GROUP LTD

- Ambri Inc.

- Amprius Inc.

- BYD Company Ltd.

- Envia Systems Inc.

- ESS Tech, Inc.

- Hitachi

- Hitachi High-Tech India Private Limited

- LG Chemicals

- Mitsubishi Chemical

- Panasonic Corporation

- Phinergy

- PolyPlus

- SAMSUNG SDI CO., LT

- Seeo

- SES AI Corporation

- Sion Power

- Solid Power Inc

- Toshiba Corporation

Recent Developments

In 2024, AESC is positioning itself as a critical supplier for major automakers, with a strong focus on advancing solid-state battery technology and improving battery efficiency and energy density.

In 2024, Ambri has secured over $150 million in funding, enabling it to continue scaling its operations and improve its battery technology. The company aims to begin commercializing its liquid metal batteries by 2025, with plans to initially target energy storage projects in North America and Europe.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 7.3 Bn |

| Forecast Revenue (2034) | USD 17.4 Bn |

| CAGR (2025-2034) | 9.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Lithium-Sulfur Batteries, Solid-State Batteries, Lithium-air batteries, Flow Batteries), By Application (Electric Vehicles (EVs), Consumer Electronics, Energy Storage Systems (ESS), Aerospace and Defense), By End Use (Transportation, Residential, Commercial, Utilities) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | 24M, AESC GROUP LTD, Ambri Inc., Amprius Inc., BYD Company Ltd., Envia Systems Inc., ESS Tech, Inc., Hitachi, Hitachi High-Tech India Private Limited, LG Chemicals, Mitsubishi Chemical, Panasonic Corporation, Phinergy, PolyPlus, SAMSUNG SDI CO., LT, Seeo, SES AI Corporation, Sion Power, Solid Power Inc, Toshiba Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |