Quick Navigation

Report Overview

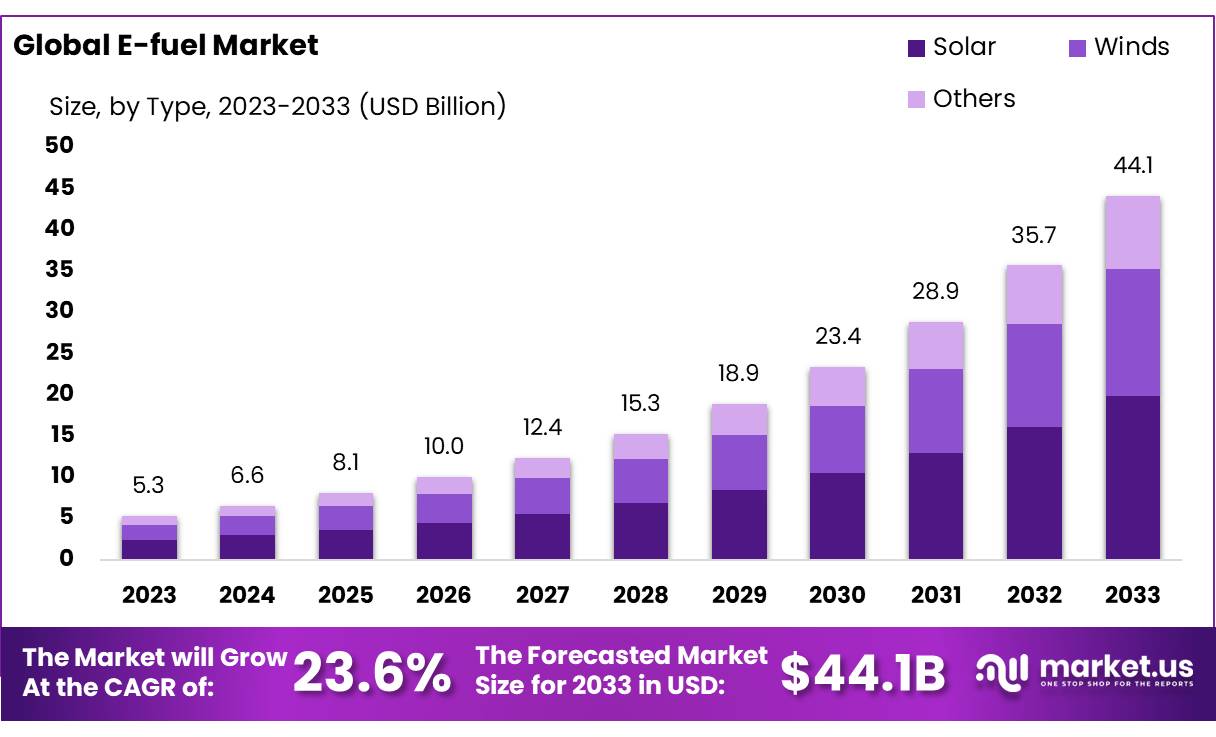

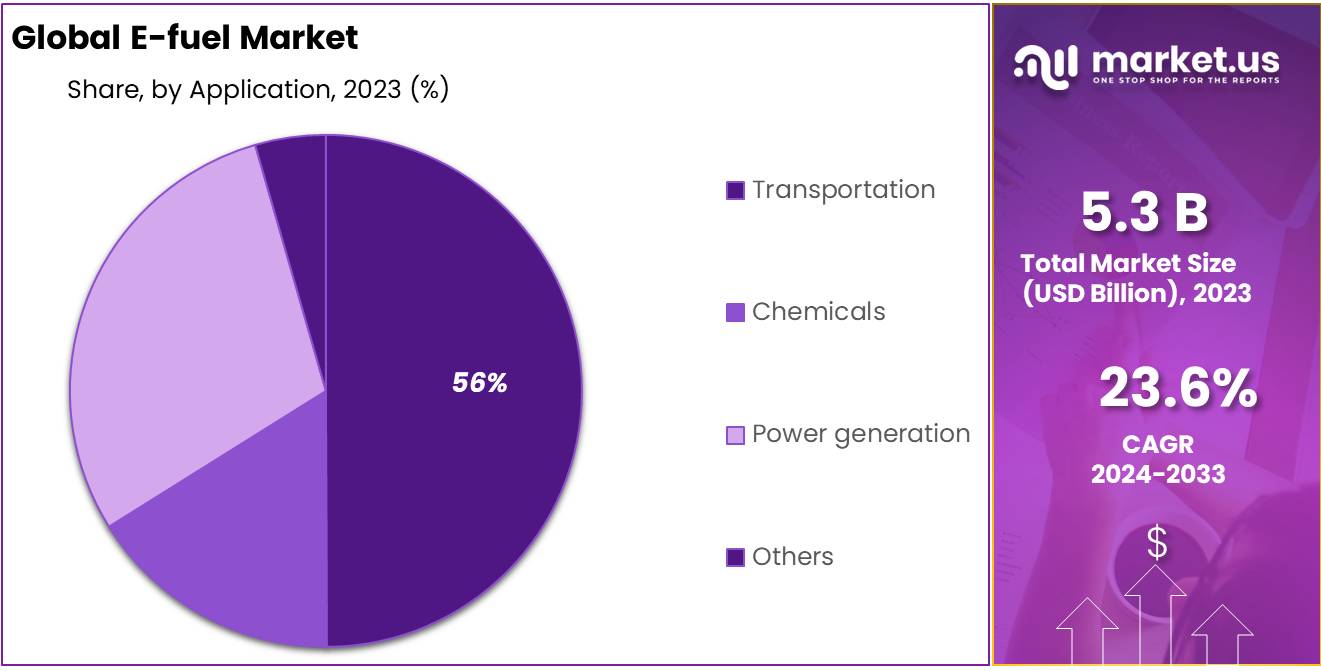

The Global E-fuel Market size is expected to be worth around USD 44.1 Bn by 2033, from USD 5.3 Bn in 2023, growing at a CAGR of 23.6% during the forecast period from 2024 to 2033.

E-fuels, or electronic fuels, are synthetic fuels produced by combining hydrogen—derived from renewable electricity through electrolysis—with carbon dioxide captured from the atmosphere or industrial processes.

This method creates fuels like e-methane, e-kerosene, and e-methanol, which can serve as direct replacements for conventional fossil fuels in existing combustion engines, thereby facilitating a reduction in greenhouse gas emissions without necessitating significant changes to current infrastructure.

E-fuels are considered a potential alternative to fossil fuels, offering a way to reduce carbon emissions, particularly in sectors that are difficult to electrify, like aviation, shipping, and heavy-duty transport.

E-fuels can be used in existing internal combustion engines and infrastructure, which could make them an attractive option for decarbonizing industries reliant on liquid fuels. These fuels are often categorized into e-methanol, e-diesel, e-kerosene, and e-gasoline, depending on the specific chemical structure.

The global e-fuel market has been experiencing considerable growth due to several factors, including tightening government regulations, increased investments in green technologies, and advancements in e-fuel production methods.

According to the International Energy Agency (IEA), global energy-related CO2 emissions in 2023 remained stable at around 36.8 gigatonnes, indicating that governments are under significant pressure to reduce emissions further (IEA, 2023). E-fuels play an essential role in meeting these objectives, particularly in industries like aviation, shipping, and heavy-duty transport, where electrification is challenging.

In 2024, global investments in green hydrogen and e-fuels are projected to surpass $10 billion, with governments such as the European Union, the U.S., and Japan spearheading the drive. In Europe alone, the European Commission has set an ambitious target to reach a capacity of 10 million tonnes of renewable hydrogen by 2030, with a significant portion of this being converted into e-fuels for transportation and industry.

Governments worldwide are incentivizing e-fuel development through favorable regulations and funding. For instance, the U.S. Department of Energy (DOE) has committed over $400 million in funding for projects that focus on the production and commercialization of advanced fuels, including e-fuels. This funding is part of a broader $2 billion initiative to develop sustainable aviation fuel (SAF), which includes synthetic fuels.

On the international front, countries with significant renewable energy resources are emerging as key players in e-fuel production. Chile, with its abundant solar and wind power, is becoming a hub for green hydrogen and e-fuel production.

The country exported the first batch of e-fuels to Europe in 2023, marking a milestone in international e-fuel trade. Similarly, Australia, with its vast renewable energy capacity, is set to increase its e-fuel exports, targeting markets in Asia and Europe. According to the Australian Renewable Energy Agency (ARENA), the country’s e-fuel production capacity is expected to grow fivefold by 2030, driven by increased international demand.

Key Takeaways

- E-fuel Market size is expected to be worth around USD 44.1 Bn by 2033, from USD 5.3 Bn in 2023, growing at a CAGR of 23.6%.

- Solar held a dominant market position in the e-fuel market, capturing more than a 45.5% share.

- E-methane held a dominant market position in the e-fuel sector, capturing more than a 25.5% share.

- Power-to-Liquid (PtL) method dominated the production techniques in the e-fuel market, accounting for a 44.5% significant share.

- E-Hydrogen Technology (Electrolysis) held a dominant market position in the e-fuel technology landscape, capturing more than a 48.4% share.

- E-Gas held a dominant market position in the e-fuel industry, capturing more than a 58.9% share.

- Transportation sector held a dominant market position in the e-fuel industry, capturing more than a 56.4% share.

- APAC dominated the e-fuel landscape, accounting for approximately 47.7% of the global market, translating into a value of USD 1.9 billion.

By Renewable source

In 2023, Solar held a dominant market position in the e-fuel market, capturing more than a 45.5% share. This substantial market share can be attributed to the extensive deployment of solar farms and the declining cost of solar photovoltaic (PV) systems.

Solar energy’s cost-effectiveness and scalability have made it a preferred renewable source for e-fuel production. Innovations in solar technology have enhanced the efficiency of converting solar energy into electrical energy, which is then used in the electrolysis process to produce hydrogen, a primary component of e-fuels.

Wind energy followed as the second largest contributor to the e-fuel market, accounting for a significant portion of the market.

In 2023, the wind energy segment benefitted from favorable government policies and advancements in turbine technology, which have decreased the cost per megawatt-hour of wind-generated electricity. These advancements have enabled more efficient harnessing of wind power for the synthesis of e-fuels, particularly in regions with high wind resources.

By Fuel Type

In 2023, E-methane held a dominant market position in the e-fuel sector, capturing more than a 25.5% share. Its prominence in the market can be largely attributed to its versatility and compatibility with existing natural gas infrastructure, which allows for seamless integration into current energy systems. E-methane is primarily used in heating and power generation, making it a critical component in the transition towards greener energy alternatives.

Following closely, E-kerosene accounted for a substantial market share, driven by increasing demand in the aviation industry. Airlines are actively exploring sustainable fuel options to reduce their carbon footprint, and e-kerosene offers a viable solution without requiring significant modifications to aircraft engines. Its adoption is expected to rise as more airlines commit to reducing emissions in response to global climate change initiatives.

E-methanol also captured a notable share of the market, particularly in the shipping and chemical manufacturing sectors. As a cleaner alternative to traditional marine fuels, e-methanol has gained traction due to stricter environmental regulations in maritime transport. Additionally, its use as a feedstock in the production of formaldehyde and other chemicals underscores its importance in industrial applications.

E-ammonia, primarily utilized in the agricultural and power generation sectors, has seen increased interest due to its potential in both direct applications and as an intermediate for producing other e-fuels. It is particularly appealing in regions where renewable energy sources are abundant, allowing for the sustainable production of ammonia via electrolysis of water.

The market shares for E-diesel and E-gasoline, while smaller, are nonetheless significant. These fuels are crucial for the automotive industry’s shift towards sustainability. E-diesel offers a renewable alternative for diesel engines, which are widely used in commercial transportation and heavy machinery. Similarly, E-gasoline provides an eco-friendly substitute for gasoline engines, with ongoing developments aimed at enhancing its performance and emission profiles.

By Production Method

In 2023, the Power-to-Liquid (PtL) method dominated the production techniques in the e-fuel market, accounting for a 44.5% significant share. This process, which involves converting electricity into liquid fuels, is particularly appealing because of its ability to produce high-density fuels suitable for sectors like aviation and heavy transportation that are difficult to electrify. PtL’s versatility in creating products such as e-kerosene and e-diesel is a key driver behind its widespread adoption, especially as industries seek sustainable alternatives to conventional fossil fuels.

Power-to-Gas (PtG) also held a considerable portion of the market. This method is essential for producing e-fuels like e-methane and e-hydrogen, which can be integrated into existing gas networks or used for electricity generation.

The advantage of PtG lies in its ability to store surplus renewable energy, offering a solution to the intermittency of solar and wind power sources. By converting excess electricity into gas, this method plays a crucial role in balancing grid demand and supply, thus supporting energy security and continuity.

The Gas-to-Liquid (GtL) process, though less prevalent than PtL and PtG, has its niche in the e-fuel landscape, particularly in regions rich in natural gas resources but distant from major fuel-consuming markets. GtL technology converts natural gas into more valuable liquid fuels, such as diesel and gasoline, which are easier to transport and use with existing vehicle technologies. This method is instrumental in leveraging existing gas reserves while reducing reliance on crude oil imports.

Biologically derived fuels represent an innovative segment of the e-fuel market, focusing on producing fuels from biological processes such as fermentation or the use of bio-catalysts. Although this segment currently holds a smaller market share, it is gaining traction due to its potential to create fuels from a variety of biomass sources, including agricultural waste, thereby contributing to waste reduction and sustainable agriculture practices.

By Technology

In 2023, E-Hydrogen Technology (Electrolysis) held a dominant market position in the e-fuel technology landscape, capturing more than a 48.4% share. This technology is fundamental in the production of green hydrogen, which is achieved by splitting water into hydrogen and oxygen using electricity derived from renewable sources.

The appeal of electrolysis lies in its ability to provide a clean, sustainable fuel source that emits no carbon during production. Its widespread adoption is largely driven by the global push for decarbonization, particularly in industries such as transportation and heavy manufacturing, where hydrogen can serve as a direct fuel or as an intermediate in the production of other e-fuels.

The Fischer-Tropsch (FT) process also plays a critical role in the e-fuel market, especially in the production of liquid hydrocarbons from carbon monoxide and hydrogen. While it holds a smaller share compared to electrolysis, its importance cannot be understated.

The FT process is particularly valuable for its ability to produce a range of synthetic fuels, including diesel and gasoline, that are compatible with existing fuel infrastructure. This technology’s adaptability to utilize both biomass and gasified coal as feedstock further enhances its applicability in diverse geographic and economic contexts.

The Reverse Water Gas Shift (RWGS) process, though less common than the other two technologies, is integral in converting carbon dioxide back into carbon monoxide by reacting it with hydrogen. This capability makes RWGS a critical component in the circular carbon economy, helping to reduce overall carbon emissions by recycling CO2 into usable fuel.

In 2023, its adoption was primarily seen in pilot projects and specialized applications, emphasizing its potential in waste-to-fuel schemes and as a complement to carbon capture technologies.

By Basis of State

E-Gas held a dominant market position in the e-fuel industry, capturing more than a 58.9% share. This segment’s strength stems from its ability to integrate seamlessly with existing infrastructure, such as natural gas pipelines and storage systems, which significantly lowers the barriers to adoption and scales up use. E-Gas, including hydrogen and synthetic natural gas, is increasingly used across various sectors, notably in power generation and industrial processes, where its high energy density and clean combustion properties are highly valued.

On the other hand, E-Liquid fuels also constitute a significant part of the e-fuel market, though with a smaller share compared to gases. E-Liquids, such as e-diesel, e-gasoline, and e-kerosene, are particularly important in the transportation sector, including aviation, marine, and automotive industries.

These fuels are crucial for applications where energy density and ease of transport are paramount. Despite the challenges of higher production costs compared to E-Gas, E-Liquids are essential for enabling a broader transition to renewable energy in sectors that are harder to decarbonize due to current technological and infrastructural limitations.

By End Use

In 2023, the Transportation sector held a dominant market position in the e-fuel industry, capturing more than a 56.4% share. This segment’s prominence is largely due to the critical need for sustainable fuel alternatives in automotive, aviation, and maritime transportation, which are significant contributors to global carbon emissions.

E-fuels, such as e-diesel, e-gasoline, and e-kerosene, have been pivotal in enabling these industries to transition towards greener alternatives without extensive modifications to existing engines and fuel distribution systems.

The Chemicals sector also utilizes e-fuels, primarily as a feedstock in various industrial processes. While the share is smaller than that of Transportation, the role of e-fuels in producing chemicals is vital for reducing reliance on petroleum-based raw materials and minimizing the environmental footprint of chemical production. E-fuels offer a renewable solution that can be integrated into existing chemical manufacturing processes, fostering a more sustainable industry practice.

Power generation is another significant end-use sector for e-fuels. Utilizing e-fuels like e-methane and e-hydrogen for electricity generation helps to mitigate the variability of renewable energy sources such as wind and solar. By converting excess renewable energy into e-fuels, power plants can maintain stable energy supply and enhance grid reliability, particularly during periods of low solar or wind activity.

Key Market Segments

By Renewable source

- Solar

- Winds

- Others

By Fuel Type

- E-methane

- E-kerosene

- E-methanol

- E-ammonia

- E-diesel

- E-gasoline

By Production Method

- Power-to-Liquid

- Power-to-Gas

- Gas-to-Liquid

- Biologically derived fuels

By Technology

- Hydrogen technology (Electrolysis)

- Fischer-Tropsch

- Reverse-Water-Gas-Shift (RWGS)

By Basis of State

- Gas

- Liquid

By End Use

- Transportation

- Chemicals

- Power generation

- Others

Drivers

Regulatory Support and Environmental Policies

Governments worldwide are implementing policies that incentivize the production and use of e-fuels as part of broader climate change initiatives. For instance, the European Union’s Green Deal aims to achieve carbon neutrality by 2050, which has led to enhanced support for renewable energy technologies, including e-fuels.

In 2023, significant numbers indicate the impact of these policies on the industry. The International Energy Agency (IEA) reports that global investment in renewable energy production, including e-fuels, has surged, with an estimated $500 billion allocated towards renewable energy sectors by 2024. This substantial investment underscores the pivotal role of governmental and regulatory frameworks in driving the adoption of e-fuels.

Further demonstrating the influence of regulatory support, the U.S. Department of Energy launched initiatives totaling over $100 million in funding to support research and development in hydrogen and e-fuel technologies. This initiative aims to reduce the cost of green hydrogen production to under $1 per kilogram, making it a competitive alternative to conventional fuels and accelerating its market adoption.

Moreover, major chemical industries are also pivoting towards e-fuels to align with these regulatory mandates and to future-proof their operations against increasingly stringent emissions standards.

For example, BASF, one of the world’s leading chemical companies, has committed to reducing its greenhouse gas emissions by 25% by 2030 compared to 2018 levels. Part of this reduction strategy includes the integration of e-fuels into their energy mix, utilizing them for both energy generation and as raw materials in chemical production.

The adoption of e-fuels in the transportation sector, particularly in commercial airlines and maritime operations, further illustrates the sector’s response to regulatory pressures. Several airlines have announced plans to incorporate e-kerosene, aiming to reduce flight-related carbon emissions.

Similarly, shipping companies are exploring e-methanol as a substitute for heavy fuel oil to comply with the International Maritime Organization’s (IMO) goal to halve greenhouse gas emissions from ships by 2050.

Restraints

High Production Costs

The production of e-fuels, particularly through methods such as electrolysis and Fischer-Tropsch processes, requires substantial energy inputs, most of which must come from renewable sources to ensure the sustainability of the end product. This requirement can lead to higher operational costs compared to traditional fossil fuels.

Leading chemical organizations have also voiced concerns over the economic scaling of e-fuel technologies. For instance, BASF has reported that while they are investing in e-fuel technologies as part of their decarbonization strategy, the higher production costs pose a risk to their competitive positioning in the global market. Similarly, other major industry players such as Dow and LyondellBasell have emphasized the need for further technological breakthroughs and cost reductions to make e-fuels a viable alternative.

The impact of high production costs is particularly evident in sectors like aviation and shipping, where the switch to e-fuels requires not only new fuel formulations but also modifications to existing engines and infrastructure. For example, adapting commercial aircraft to use e-kerosene can involve significant upfront investments, which may deter airlines from transitioning away from conventional jet fuel, especially given the current price differentials.

Moreover, these high costs also affect the adoption rates among consumers and industries, who may be reluctant to switch to more expensive fuel options without substantial financial incentives or regulatory mandates. This hesitancy can slow down the market penetration of e-fuels and delay the broader energy transition goals.

Addressing these cost challenges will be crucial for the future growth of the e-fuel market. Continued investment in research and development, along with supportive government policies that include subsidies and tax incentives, could help reduce production costs and enhance the economic attractiveness of e-fuels.

As the technology matures and scales up, there is potential for costs to decrease, making e-fuels a more competitive and widely adopted energy solution. However, until these economic barriers are overcome, high production costs will remain a significant restraining factor for the e-fuel market.

Opportunity

Expanding Applications in Heavy Industries

In 2023, the steel industry began adopting e-fuels more broadly, particularly e-hydrogen, to replace coking coal in the iron reduction process. Companies like Thyssenkrupp and ArcelorMittal have been leading the charge, investing in hydrogen-based steel production technologies that can reduce carbon emissions by up to 95% compared to traditional methods.

Thyssenkrupp, for instance, has launched a series of pilot projects aimed at testing the efficiency and scalability of hydrogen in steel production, with the goal of transitioning to a lower-carbon production model by 2030.

The cement industry is another area where e-fuels are gaining traction. The chemical processes required for cement production are among the largest sources of industrial CO2 emissions globally. Companies like LafargeHolcim have started to explore the use of e-fuels as a substitute for conventional fossil fuels in their kilns. By utilizing e-methanol or e-gasoline, these companies can significantly reduce their carbon footprint while maintaining the high temperatures necessary for cement production.

Furthermore, large-scale manufacturing sectors that produce chemicals, plastics, and other materials also stand to benefit from the adoption of e-fuels. These sectors require high levels of thermal energy, which e-fuels can provide without the associated carbon emissions of traditional energy sources. For example, Dow Chemical has announced initiatives to incorporate e-fuels into their manufacturing processes, aiming to reduce both direct and indirect emissions from their operations.

The adoption of e-fuels in these heavy industries not only represents a substantial growth opportunity for the e-fuel market but also aligns with global sustainability goals. As these industries transition away from fossil fuels, the demand for e-fuels is expected to increase, driven by both environmental regulations and the industries’ commitments to achieving carbon neutrality.

Investment in infrastructure to support e-fuel production and utilization is also a critical factor in harnessing this growth opportunity. Governmental incentives, such as tax breaks or subsidies for green energy projects, could accelerate the adoption of e-fuels in these heavy industries by offsetting the initial capital expenditures and reducing the overall financial risk.

Trends

Integration of Artificial Intelligence and IoT

In 2023, leading chemical companies have begun to harness the power of AI to optimize the operations of e-fuel production facilities. For example, BASF has implemented AI-driven systems to monitor and adjust the electrolysis process in real time, ensuring optimal energy usage and maximizing the output of hydrogen. This use of AI not only improves the efficiency of the production process but also helps in maintaining the quality and purity of the hydrogen produced, which is crucial for its various applications.

IoT technology is also making significant inroads into the e-fuel sector. Companies like Shell and BP are utilizing IoT sensors to monitor the condition and performance of e-fuel infrastructure. These sensors collect data on everything from pipeline pressure to the temperature of storage tanks, providing a comprehensive overview of the system’s status.

This data is then analyzed to predict maintenance needs, prevent downtime, and enhance the safety of operations. For instance, Shell reported a reduction in operational disruptions by 20% through the adoption of IoT for predictive maintenance in their e-fuel operations.

Moreover, IoT and AI are facilitating better integration of renewable energy sources into e-fuel production. By predicting fluctuations in wind and solar power availability, these technologies enable e-fuel producers to adjust their operations in real time. This dynamic adjustment not only ensures a steady supply of e-fuels but also optimizes the use of renewable energy, which is often intermittent and unpredictable.

The economic impact of these technological integrations is significant. According to industry estimates, the adoption of AI and IoT in e-fuel production can lead to cost savings of up to 30% in operational expenses through improved energy efficiency and reduced downtime. These savings are crucial for making e-fuels more competitive with traditional fossil fuels and enhancing their market penetration.

In addition to operational improvements, AI and IoT are playing a critical role in the logistics and distribution of e-fuels. Advanced tracking and routing systems are being employed to ensure that e-fuels are delivered efficiently and sustainably, reducing the carbon footprint associated with their distribution.

This trend of integrating advanced technologies into the e-fuel sector is not just a passing phase but a significant shift towards more intelligent and sustainable energy solutions. As the technology evolves and more companies adopt these innovations, the e-fuel industry is expected to see substantial growth in efficiency and a reduction in costs, further propelling the adoption of e-fuels in global markets.

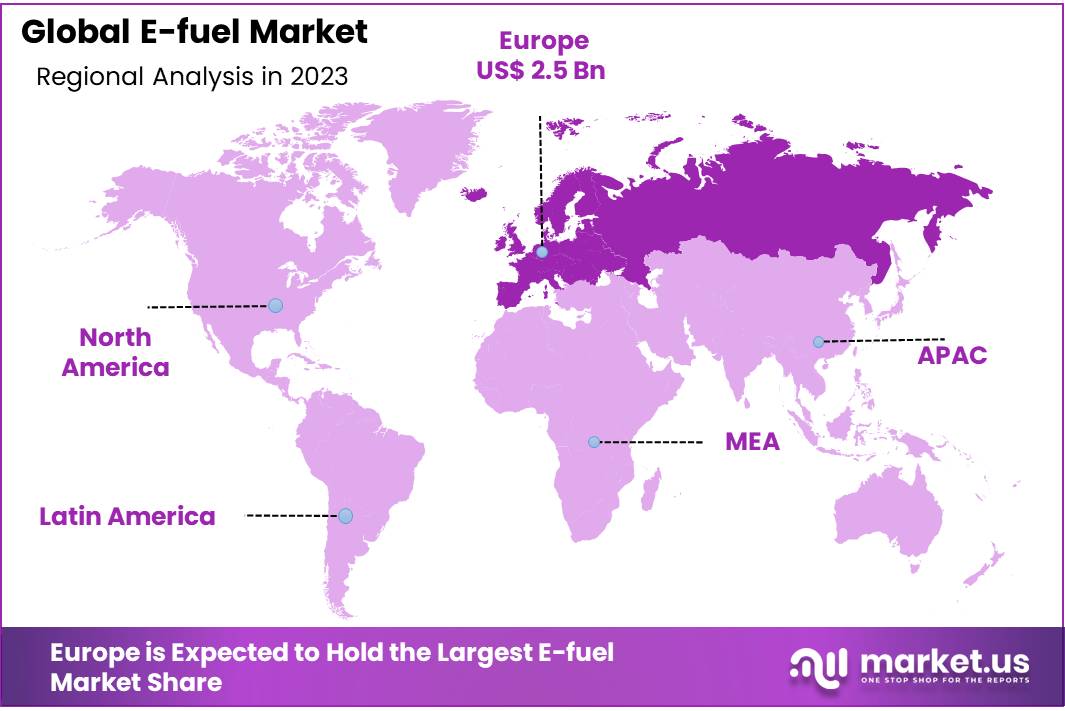

Regional Analysis

The e-fuel market exhibits dynamic regional variations, with Asia Pacific (APAC) leading in market size and growth. In 2023, APAC dominated the e-fuel landscape, accounting for approximately 47.7% of the global market, translating into a value of USD 1.9 billion.

This substantial share is largely due to the aggressive renewable energy initiatives and governmental support across countries like China, India, and Japan, which are heavily investing in technologies such as hydrogen fuel and synthetic fuels to reduce their carbon footprints and enhance energy security.

Europe also represents a significant portion of the e-fuel market, driven by stringent EU regulations on carbon emissions and high levels of technological advancement in renewable energy technologies. The region’s commitment to achieving the Green Deal objectives has spurred extensive investments in e-fuel production facilities, particularly in Germany, the UK, and Scandinavia, where there is a strong focus on integrating renewable energy sources with existing infrastructure.

North America, while having a smaller share compared to APAC and Europe, is rapidly expanding its e-fuel capabilities, particularly in the United States and Canada. This growth is supported by both public and private sector investments aimed at decreasing dependency on oil imports and increasing the production of sustainable and clean energy solutions.

Meanwhile, the Middle East & Africa and Latin America are gradually entering the e-fuel market. The Middle East, with its vast solar energy resources, is beginning to leverage these for e-fuel production, particularly in countries like Saudi Arabia and the UAE.

Africa’s market is emerging, with South Africa leading in renewable energy initiatives. Latin America shows potential due to its rich bioenergy resources and growing investments in renewable energy sectors in countries like Brazil and Argentina.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The e-fuel market features a diverse array of key players, each contributing uniquely to the sector’s evolution and expansion. Prominent companies like Aramco and Audi AG are spearheading efforts to develop and commercialize e-fuels, leveraging their extensive resources and technological expertise. Aramco is actively investing in carbon capture and utilization technologies to produce e-fuels, while Audi AG has been pioneering in the development of e-gasoline and e-diesel as part of its sustainable mobility strategy.

In the realm of specialized e-fuel technologies, companies like Ballard Power Systems, Inc., Ceres Power Holding Plc, and Siemens Energy are playing critical roles. Ballard Power Systems is known for its hydrogen fuel cell innovations that power electric vehicles, whereas Ceres Power and Siemens Energy focus on solid oxide fuel cell technology and high-efficiency power generation systems, respectively. These technological advancements are pivotal in enhancing the efficiency and scalability of e-fuel production.

Furthermore, startups and niche players such as Climeworks AG and Ineratec GmbH are pushing the boundaries of the e-fuel industry with cutting-edge solutions. Climeworks specializes in direct air capture technology to supply carbon dioxide for synthetic fuel production, a critical component in creating carbon-neutral fuels.

Ineratec GmbH, on the other hand, offers compact and modular chemical plants for the synthesis of renewable fuels, essential for decentralized production setups. The diverse capabilities and focus areas of these companies collectively drive the e-fuel market forward, fostering innovations that could potentially revolutionize the energy sector.

Top Key Players

- Aramco

- Archer Daniels Midland Co.

- Audi AG

- Ballard Power Systems, Inc.

- Ceres Power Holding Plc

- Clean Fuels Alliance America

- Climeworks AG

- E-Fuel Corporation

- eFuel Pacific Limited

- ENOWA

- Hexagon Agility

- HIF Global

- Ineratec GmbH

- Infinium

- Liquid Wind SE

- Mitsubishi Heavy Industries Ltd.

- Neste

- Norsk e-Fuel AS

- Orsted

- Porsche AG

- Repsol

- Siemens Energy

- Sunfire GmbH

- Uniper SE

Recent Developments

In 2023 Archer Daniels Midland Co, the company emphasized its commitment to reducing greenhouse gas emissions and enhancing its sustainability efforts across various operations.

In 2023, Saudi Aramco, in collaboration with NEOM’s energy and water subsidiary ENOWA, initiated a significant project in the e-fuel sector by developing a first-of-its-kind synthetic electro-fuel (e-fuel) demonstration plant.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 5.3 Bn |

| Forecast Revenue (2033) | USD 44.1 Bn |

| CAGR (2024-2033) | 23.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Renewable source (Solar, Winds, Others), By Fuel Type (E-methane, E-kerosene, E-methanol, E-ammonia, E-diesel, E-gasoline), By Production Method (Power-to-Liquid, Power-to-Gas, Gas-to-Liquid, Biologically derived fuels), By Technology (Hydrogen technology (Electrolysis), Fischer-Tropsch, Reverse-Water-Gas-Shift (RWGS)), By Basis of State (Gas, Liquid), By End Use (Transportation, Chemicals, Power generation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Aramco, Archer Daniels Midland Co., Audi AG, Ballard Power Systems, Inc., Ceres Power Holding Plc, Clean Fuels Alliance America, Climeworks AG, E-Fuel Corporation, eFuel Pacific Limited, ENOWA, Hexagon Agility, HIF Global, Ineratec GmbH, Infinium, Liquid Wind SE, Mitsubishi Heavy Industries Ltd., Neste, Norsk e-Fuel AS, Orsted, Porsche AG, Repsol, Siemens Energy, Sunfire GmbH, Uniper SE |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |