Quick Navigation

Report Overview

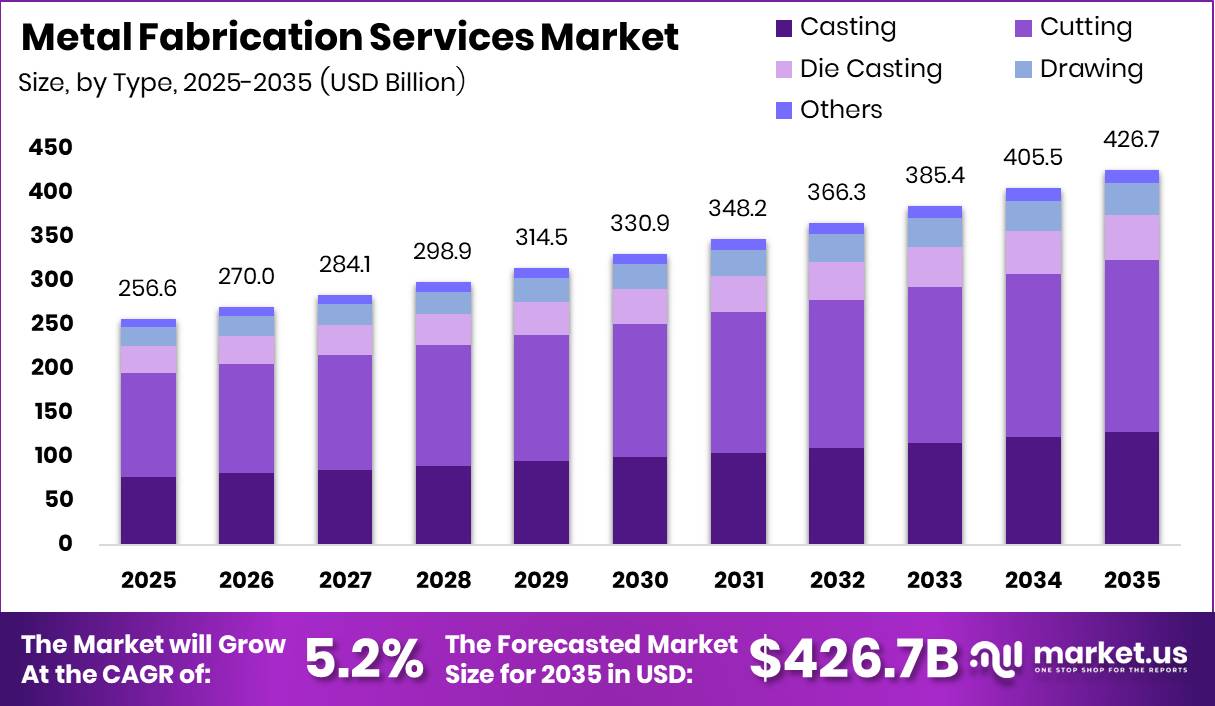

Global Metal Fabrication Services Market size is expected to be worth around USD 426.7 Billion by 2035 from USD 256.6 Billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035. This trajectory signals a market producing sustained, compounding revenue across a decade. Investors entering before 2027 position themselves ahead of the steepest volume accumulation phase.

The Metal Fabrication Services market covers industrial processes that convert raw metals into finished or semi-finished components through cutting, casting, forming, drawing, and die casting. It serves end-use industries including oil and gas, construction, aerospace, automotive, marine, and military. The market spans both job-shop and integrated production models, operating across steel, aluminum, stainless steel, and copper material categories.

Key Takeaways

- The global Metal Fabrication Services Market is valued at USD 256.6 Billion in 2025 and is forecast to reach USD 426.7 Billion by 2035.

- The market grows at a CAGR of 5.2% during the forecast period 2026 to 2035.

- Casting dominates the Type segment with a 30.1% share in 2025.

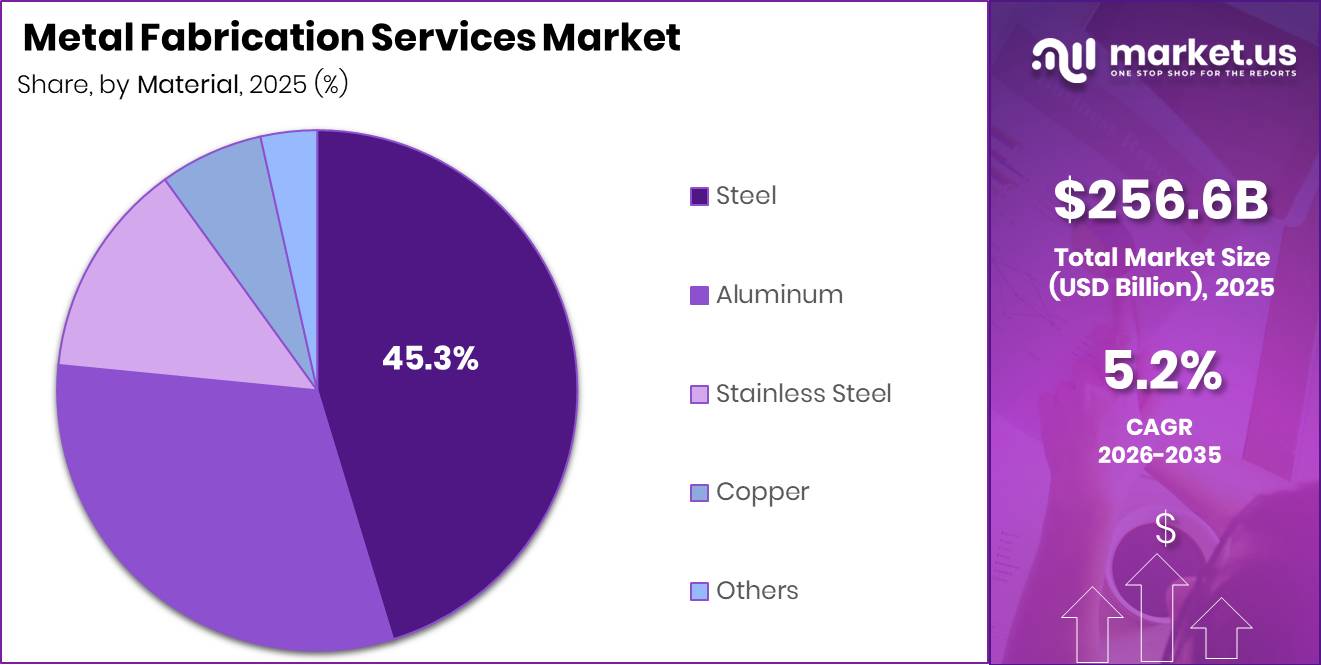

- Steel dominates the Material segment with a 45.3% share in 2025.

- Construction dominates the End Use Industry segment with a 30.3% share in 2025.

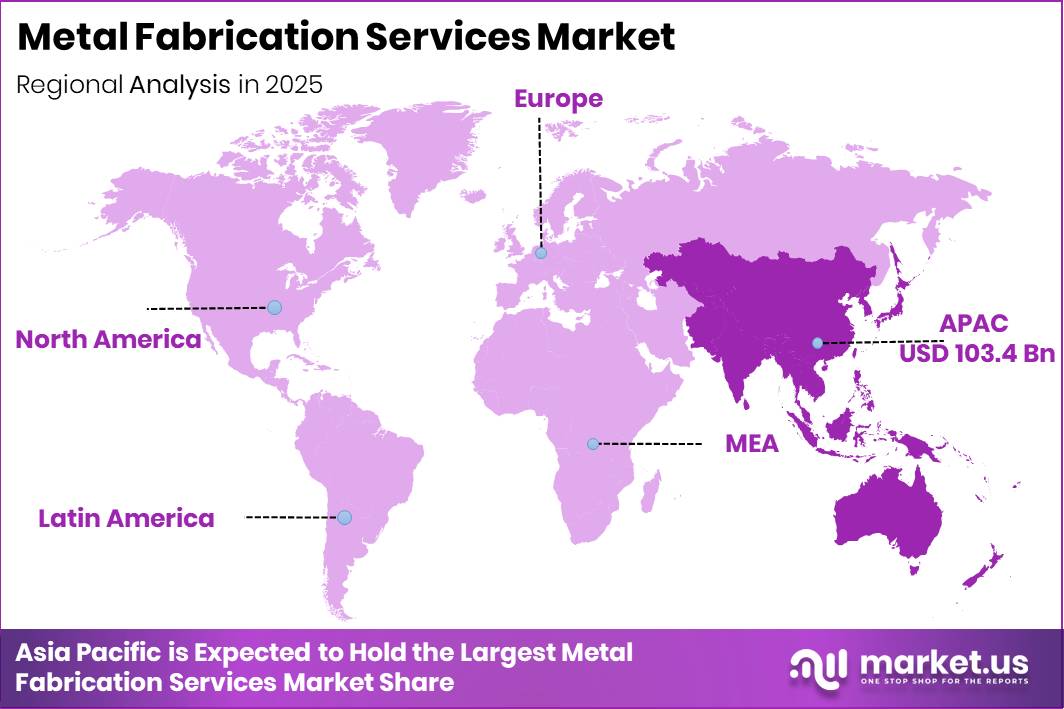

- Asia Pacific dominates the regional landscape with a 40.3% share, valued at USD 103.42 Billion in 2025.

As per our research, 51% of metalforming companies expected no change in economic activity over the following three months, reflecting a cautious but stable demand environment. This stability reduces revenue volatility for fabricators with diversified customer portfolios. Operators with long-term contracts are better insulated from short-cycle demand fluctuations than those relying on spot orders.

As per our research, 39% of metalforming companies reported stable shipping levels, confirming that output volumes held steady despite broader macroeconomic uncertainty. This reflects a market floor supported by construction and industrial base demand. Fabricators maintaining reliable fulfillment rates hold a measurable advantage in retaining repeat buyers over contract cycles.

Type Analysis

Casting dominates with 30.1% due to broad structural component demand across industries.

In 2025, Casting held a dominant market position in the By Type segment of the Metal Fabrication Services Market, with a 30.1% share. Casting produces complex, near-net-shape components at scale, which reduces downstream machining time. This efficiency makes casting the preferred method for high-volume structural and mechanical parts across automotive, construction, and industrial equipment end users.

Cutting serves as the entry process for most fabrication workflows, shaping raw metal stock before forming or assembly. Its universal applicability across steel, aluminum, and stainless steel makes it indispensable to nearly every production line. Fabricators with advanced cutting capabilities, including laser and waterjet systems, command higher contract values and shorter lead times.

Die Casting delivers tight dimensional tolerances and smooth surface finishes suited for aerospace, automotive, and military components. This precision reduces post-process finishing costs and supports high repeatability across large production runs. Buyers in specification-driven sectors increasingly require die casting documentation as part of supplier qualification.

Drawing and other process types, including forming and stamping, serve niche production requirements where sheet metal or wire-form geometry is specified. These processes support lighter structural and enclosure applications. They collectively hold the remaining share of the Type segment and serve primarily construction, marine, and consumer-adjacent industrial buyers.

Material Analysis

Steel dominates with 45.3% due to cost efficiency and structural versatility.

In 2025, Steel held a dominant market position in the By Material segment of the Metal Fabrication Services Market, with a 45.3% share. Steel’s combination of tensile strength, weldability, and competitive pricing makes it the default choice across construction, oil and gas, and heavy industrial applications. Fabricators that optimize steel processing capacity capture the broadest addressable project pipeline in the market.

Aluminum serves weight-sensitive applications in aerospace, automotive lightweighting, and enclosure manufacturing. Its corrosion resistance and machinability support premium-priced fabrication contracts. Buyers in electric vehicle and clean-energy sectors are increasing aluminum specification rates, creating a structurally growing sub-segment within the material category.

Stainless Steel addresses corrosion-critical environments in food processing, chemical handling, marine, and medical-adjacent manufacturing. Its higher material cost elevates contract values per tonne compared to carbon steel. Fabricators that develop stainless steel welding and finishing expertise access a higher-margin niche with fewer qualified competitors.

Copper and other specialty materials including titanium and alloy-grade metals serve precision and conductivity-critical applications. These materials are used in power transmission, defense, and high-frequency electronics fabrication. They represent the remaining material share and command premium processing fees due to handling complexity and certification requirements.

End Use Analysis

Construction dominates with 30.3% due to sustained global infrastructure investment.

In 2025, Construction held a dominant market position in the By End Use Industry segment of the Metal Fabrication Services Market, with a 30.3% share. Structural steel demand from commercial buildings, industrial facilities, bridges, and energy infrastructure projects drives this position. Fabricators aligned with construction supply chains benefit from large-volume, repeating project flows tied to multi-year development pipelines.

Oil and Gas generates demand for pressure vessels, pipe spools, structural supports, and subsea components that require high-specification fabrication and third-party inspection. Contract values in this sector are among the highest per unit across all end-use categories. Fabricators certified to ASME, API, or equivalent standards access a restricted pool of high-margin project work.

Aerospace and Automotive together represent specification-intensive, tolerance-driven fabrication demand. These sectors require certified material traceability, dimensional accuracy documentation, and first-article inspection protocols. Suppliers that achieve OEM approval status gain access to long-term purchase agreements that provide volume predictability and reduce customer concentration risk.

Marine, Military, and other end-use categories including energy transition and data center infrastructure account for the remaining segment share. Military fabrication requires defense-grade certifications and controlled supply chain access. Marine and energy transition sectors generate demand for corrosion-resistant and high-durability assemblies with extended lifecycle performance requirements.

Key Market Segments

By Type

- Casting

- Cutting

- Die Casting

- Drawing

- Others

By Material

- Steel

- Aluminum

- Stainless Steel

- Copper

- Others

By End Use Industry

- Oil and Gas

- Construction

- Aerospace

- Marine

- Automotive

- Military

- Others

Drivers

Factory-buildout fabrication intensity remains a strong demand driver as manufacturing expansion continues to generate large volumes of downstream metal fabrication work. U.S. manufacturing construction spending reached USD 185.7 Billion annualized in April 2026, indicating sustained investment in new industrial facilities. Industrial development programs have mobilized up to USD 1 Billion in financing for manufacturing capacity expansion across solar, wind, battery, grid, and energy-efficiency supply chains.

Each new facility requires extensive fabricated components beyond the main structure, including process skids, pipe racks, mezzanines, platforms, utility supports, and safety guarding systems. These projects create demand throughout both construction and commissioning phases. Follow-on modifications and capacity expansions further extend fabrication requirements after initial plant completion, supporting a sustained pipeline of fabrication-intensive project work.

According to our Smart Manufacturing Survey, 85% of manufacturers believe smart manufacturing initiatives will transform how products are made, improve agility, and attract new talent. This widespread conviction signals capital allocation toward connected fabrication systems. Vendors supplying automation-compatible cutting, forming, and welding equipment position themselves as preferred partners in this investment cycle.

According to our Survey found that 49% of surveyed manufacturers identified operational benefits as the primary value sought from smart manufacturing investments. This focus on efficiency over novelty means fabricators that demonstrate measurable throughput and yield improvements win contracts ahead of those offering technology without performance data. Buyers are selecting suppliers based on proven operational outcomes, not technology claims alone.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public works steel demand pull | +2.5% | North America core, India, GCC, EU corridors | Short term (≤ 2 years) |

| Factory-buildout fabrication intensity | +2.2% | North America, India, Southeast Asia | Medium term (2-4 years) |

| Automation boosts job-shop output | +1.8% | US Midwest, Germany, Italy, Japan, China | Short term (≤ 2 years) |

| Clean-energy localization programs | +2.0% | US, India, EU industrial hubs | Medium term (2-4 years) |

| Data-center enclosure and support demand | +1.7% | North America core, Nordics, GCC, APAC hubs | Medium term (2-4 years) |

| Higher mix of engineered assemblies | +1.6% | Global OEM corridors, export fabrication clusters | Long term (≥ 4 years) |

Restraints

Working-capital intensity is a significant restraint for fabrication companies because large projects require substantial upfront spending before customer payments are received. Firms must fund raw materials, labor, subcontracted processing, transportation, and compliance documentation during production. As projects become more engineered and compliance-driven, cash remains tied up longer in work-in-progress inventory, staged assemblies, and certification requirements.

This challenge is particularly acute for small and mid-sized fabricators serving infrastructure, utility, and EPC projects. Extended customer payment terms and holdbacks linked to inspection or performance milestones further delay cash recovery. This reduces financial flexibility and limits the number of projects companies can pursue simultaneously, directly restricting growth capacity even when shop-floor utilization remains high.

Data from the National Association of Manufacturers shows 45.23% of manufacturers indicated they would postpone hiring under a tax-policy deterioration scenario. This hiring hesitation directly constrains fabrication capacity expansion during a period of high project demand. Shops that cannot staff up fast enough lose contracts to better-resourced competitors with larger available workforces.

The National Association of Manufacturers indicates that 44.72% of manufacturers said they would delay expansion plans if tax provisions expired. Capital investment hesitation at this scale slows equipment upgrades, facility expansions, and new market entry. Fabricators that lock in expansion financing before policy uncertainty peaks will hold a structural cost and capacity advantage over delayed competitors.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance-grade sourcing barriers | -2.0% | North America clean-energy hubs, EU-certified exports | Medium term (2-4 years) |

| Tariff-driven procurement hesitation | -1.6% | US-India lanes, APAC sourcing corridors, exporters | Short term (≤ 2 years) |

| Fabricated price inflation pass-through | -1.5% | North America core, EU industrial buyers, GCC imports | Short term (≤ 2 years) |

| Working-capital lock in projects | -1.3% | Global EPC chains, SME fabricators, infrastructure suppliers | Medium term (2-4 years) |

| Specification-driven order exclusion | -1.2% | Energy, transport, defense-adjacent fabrication corridors | Medium term (2-4 years) |

| Small-batch economics ceiling | -1.1% | Regional job shops in India, ASEAN, Latin America | Long term (≥ 4 years) |

Challenges

Multi-site capacity imbalance is a growing operational challenge for fabrication companies managing multiple plants with different equipment, workforce capabilities, and customer portfolios. As lead-time expectations tighten, manufacturers increasingly need to balance laser cutting, forming, machining, welding, finishing, and assembly workloads across facilities. Many organizations still lack integrated scheduling systems and standardized production visibility between plants.

Rising adoption of industrial robotics and connected-factory technologies is increasing customer expectations for faster and more predictable delivery performance. This exposes inefficiencies tied to disconnected multi-plant operations and fragmented production planning. The result is higher levels of inter-facility material transfers, duplicated setup activities, and unnecessary freight costs that reduce overall equipment effectiveness.

According to the Manufacturing Skills Institute, over 80% of manufacturers reported that job candidates lack basic foundational workplace and technical skills. This skills gap directly limits the rate at which fabrication shops can onboard new workers and scale output. Companies that invest in structured apprenticeship and certification programs now will build a hiring pipeline that competitors without such programs cannot replicate quickly.

As reported by L2L’s 2025 research report, 67% of manufacturing professionals observed a growing skills gap in 2025. PMMI’s 2025 workforce-gap study engaged 136 manufacturing end users and OEMs, confirming this is a sector-wide structural issue rather than a firm-level problem. Fabricators that treat workforce development as a capital investment, not an overhead cost, will secure labor access advantages that compound over the forecast period.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Labor-skill depth mismatch | -1.5% | North America core, Europe, India, ASEAN | Long term (≥ 4 years) |

| Automation adoption asymmetry | -1.3% | US Midwest, Germany, Italy, India SME clusters | Medium term (2-4 years) |

| Quote-to-order margin erosion | -1.2% | Global OEM corridors, export job shops | Short term (≤ 2 years) |

| Traceability and compliance load | -1.1% | North America clean-energy hubs, EU, GCC | Medium term (2-4 years) |

| Project-mix demand swings | -1.4% | North America, China-linked export chains, India | Short term (≤ 2 years) |

| Multi-site capacity imbalance | -1.0% | APAC fabrication corridors, North America regional shops | Medium term (2-4 years) |

Opportunities

Domestic-content-compliant fabrication is emerging as a structural opportunity driven by policy-linked qualification requirements. Clean-energy projects can qualify for up to a 10% tax-credit bonus when domestic-content rules are met, increasing the economic value of compliant supply chains. The domestic share threshold rises from 40% in 2023 to 55% after 2026, increasing demand for verifiable U.S.-based fabrication capacity.

Fabricators that integrate compliance documentation, mill certification, and audit-ready workflows into bidding processes gain a competitive advantage over price-only competitors. EPC contractors increasingly prefer suppliers that can reliably meet domestic-content verification needs. This shift reduces price-only competition by adding regulatory qualification as a key differentiator, channeling higher-margin, compliance-driven project flows toward credentialed fabricators.

As per our research, Jindal Stainless achieved carbon-emission reductions of 187,341 tonnes of CO₂ during FY2025 through energy-substitution, renewable-energy procurement, and process-improvement initiatives. This scale of verified reduction signals that large fabricated steel producers are building measurable sustainability credentials. Fabricators that adopt similar emission-reduction programs position themselves to meet buyer qualification thresholds before these requirements become contractually mandatory.

A 2025 industrial study by PPG and ArcelorMittal found that greenhouse-gas emissions from steel used in vehicle manufacturing can be reduced by up to 30% through electric-arc-furnace steelmaking and advanced high-strength steel solutions. This creates a direct commercial opportunity for fabricators that source EAF-produced steel. Automotive and clean-energy buyers increasingly specify low-carbon material provenance, making EAF-aligned supply chains a near-term qualification requirement rather than a future preference.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Domestic-content project fabrication | +2.8% | North America core, IRA-linked corridors | Short term (≤ 2 years) |

| Precision tool-room outsourcing | +2.2% | India, Southeast Asia, Middle East exports | Medium term (2-4 years) |

| Fabrication-as-a-service platforms | +1.9% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Automation retrofit job shops | +1.8% | US Midwest, Germany, Italy, Japan | Short term (≤ 2 years) |

| Energy-transition balance-of-plant | +2.1% | US, India, GCC, EU industrial hubs | Medium term (2-4 years) |

| Container and modular builds | +1.7% | India, Southeast Asia, Africa logistics nodes | Long term (≥ 4 years) |

Regional Analysis

Asia Pacific Dominates the Metal Fabrication Services Market with a Market Share of 40.3%, Valued at USD 103.42 Billion

Asia Pacific holds the largest regional position in the Metal Fabrication Services Market at 40.3%, valued at USD 103.42 Billion in 2025. This dominance reflects the region’s concentration of steel production, low-cost fabrication labor, and deep integration with global automotive, electronics, and construction supply chains. China, Japan, South Korea, and India collectively anchor fabrication output capacity across the region.

North America represents a structurally significant fabrication market driven by factory-buildout spending, defense procurement, and clean-energy infrastructure investment. U.S. manufacturing construction spending reached USD 185.7 Billion annualized in April 2026, sustaining a dense pipeline of fabrication-intensive projects. Fabricators in this region that carry domestic-content compliance capabilities capture higher-margin, qualification-gated contract opportunities.

Europe maintains a technically advanced fabrication base anchored by Germany, Italy, and France, where precision manufacturing and engineered assembly demand remains high. EU industrial decarbonization policy is accelerating the shift toward lower-emission steel and fabricated components, creating compliance-driven demand. Fabricators that invest in certified low-carbon material sourcing align with buyer qualification requirements across energy and transport infrastructure projects.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Amada Co. Ltd holds a structural advantage in sheet-metal fabrication equipment through its integrated hardware and software platform connecting cutting, bending, and welding systems. This end-to-end approach reduces customer switching costs and generates recurring service revenue. However, heavy dependence on Asian manufacturing centers creates supply chain exposure if regional sourcing costs shift materially.

Lincoln Electric Holdings Inc leads the global welding consumables and automation segment, giving it direct exposure to every fabrication end-use vertical from construction to aerospace. In 2025, ArcelorMittal Europe Tubular Products, a major fabricated steel producer, achieved a 29% reduction in CO₂ intensity per tonne and a 56% absolute reduction in Scope 1 and 2 emissions versus the 2018 baseline. This trajectory signals that fabrication buyers are setting measurable sustainability thresholds that welding and process technology suppliers must align with to retain supplier status.

Key Players

- Amada Co Ltd

- Lincoln Electric Holdings Inc

- Mitsubishi Electric Corporation

- TRUMPF GmbH + Co. KG

- Omax Corporation

- Bend-Tech

- Accu-Fab

- ThyssenKrupp AG

- O’Neal Industries

- Sandvik AB

- Tata Steel Ltd.

- Allegheny Ludlum (part of ATI Inc.)

- Outokumpu Oyj

- Voestalpine AG

- Mueller Industries, Inc.

- Other Key Players

Recent Developments

- January 2026 – Sigma Advanced Systems announced plans to invest an additional approximately Rs 450 crore into the Nasmyth Group business following its acquisition, targeting accelerated manufacturing growth and expanded precision fabrication capability.

- March 2026 – Rosebank Industries raised USD 3.1 Billion to acquire MW Components, a manufacturer of precision metal components and fasteners, as part of its industrial manufacturing expansion strategy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 256.6 Billion |

| Forecast Revenue (2035) | USD 426.7 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Casting, Cutting, Die Casting, Drawing, Others), By Material (Steel, Aluminum, Stainless Steel, Copper, Others), By End Use Industry (Oil and Gas, Construction, Aerospace, Marine, Automotive, Military, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Amada Co Ltd, Lincoln Electric Holdings Inc, Mitsubishi Electric Corporation, TRUMPF GmbH + Co. KG, Omax Corporation, Bend-Tech, Accu-Fab, ThyssenKrupp AG, O’Neal Industries, Sandvik AB, Tata Steel Ltd., Allegheny Ludlum (part of ATI Inc.), Outokumpu Oyj, Voestalpine AG, Mueller Industries, Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |