Quick Navigation

Report Overview

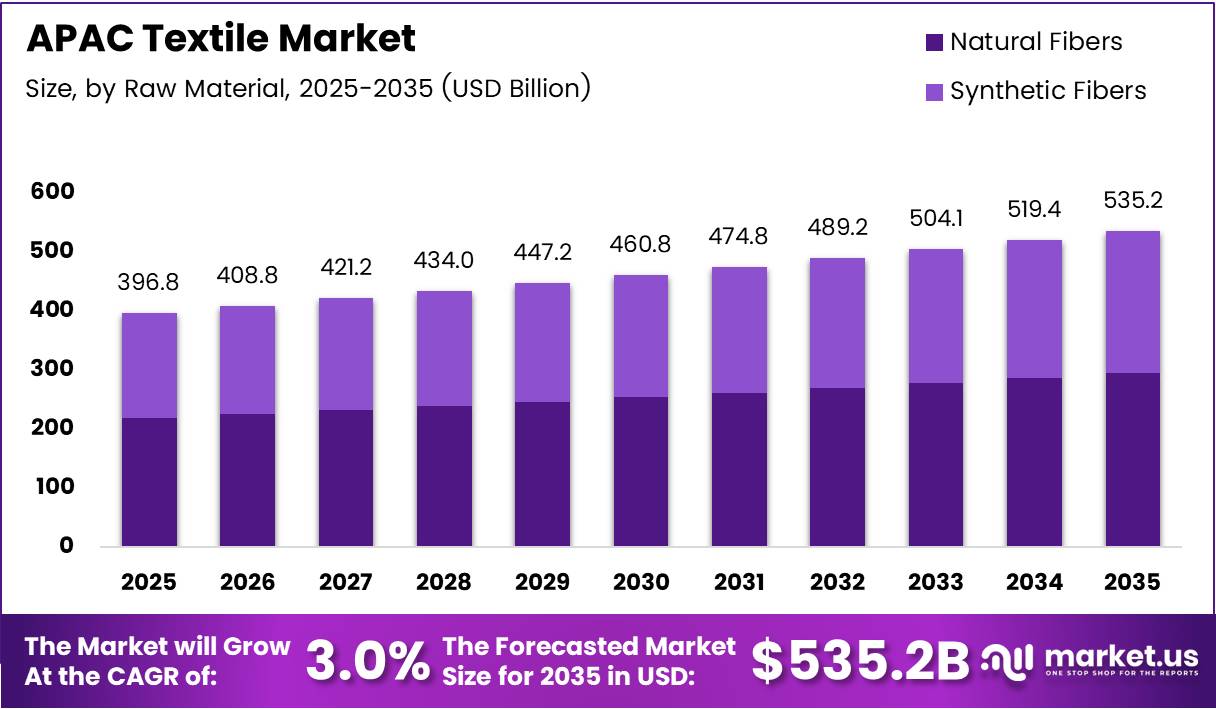

APAC Textile Market size is expected to be worth around USD 535.2 Billion by 2035 from USD 396.8 Billion in 2025, growing at a CAGR of 3.0% during the forecast period 2026 to 2035.

The Asia Pacific textile market spans the full production chain — from raw fiber processing and yarn spinning to fabric manufacturing, finishing, and garment assembly. The region holds a structural cost and scale advantage that no other geography can currently replicate. This keeps global sourcing concentrated in APAC despite rising labor costs in leading hubs.

Natural fibers and synthetic blends both find strong commercial footing here. Cotton-based production dominates volume in South Asia, while polyester and recycled fiber output concentrates in East Asia. This dual-material base gives APAC manufacturers flexibility to serve both premium fashion buyers and high-volume fast fashion retailers simultaneously.

Fashion and apparel commands the largest share of end-use demand, but industrial and technical textiles are reshaping revenue quality. Defense, automotive, and medical procurement increasingly requires performance-certified fabrics — a segment where APAC manufacturers are investing heavily to move up the value chain and reduce dependence on commodity volume.

Sustainability mandates from Western retail brands are restructuring procurement decisions throughout the region. Brands now impose supplier-level emissions and water targets, and manufacturers that cannot demonstrate compliance risk losing contracts. This shifts sustainability from a corporate reporting exercise into a hard commercial requirement for APAC textile producers.

According to Global Efficiency Intel, coal represented 81% of fuel use in India’s textile wet processing sector, contributing approximately 49 million tons of CO2e emissions. This concentration of fossil fuel dependency creates both a regulatory liability and a capital expenditure imperative — mills that delay electrification face carbon cost exposure as India tightens industrial emissions frameworks.

According to a SWITCH-Asia case study, circular textile pilot facilities in Indonesia achieved 52% energy savings and a 50% reduction in Scope 1 and 2 emissions. These figures signal that circular manufacturing models are not aspirational — they deliver measurable operating cost reductions, making the business case for adoption increasingly difficult to ignore.

Across the forecast period, the market’s trajectory reflects a structural upgrade rather than simple volume expansion. Manufacturers that combine efficiency investment with compliance capability will capture disproportionate share as global brands consolidate their APAC supplier bases around fewer, more capable partners.

Key Takeaways

- The APAC Textile Market was valued at USD 396.8 Billion in 2025 and is forecast to reach USD 535.2 Billion by 2035.

- The market grows at a CAGR of 3.0% during the forecast period 2026 to 2035.

- By Raw Material, Natural Fibers lead with a 54.2% share, driven by cotton-dominant production across South Asian manufacturing hubs.

- By Process/Technology, Woven fabrics hold the dominant position with a 45.4% segment share.

- By Application, Fashion & Apparel captures the largest share at 49.5%, reflecting APAC’s position as the world’s primary garment export base.

- North America and Europe remain key demand destinations, while APAC countries drive both production and a fast-expanding domestic consumption base.

- Key players include Shenzhou International Group, Weiqiao Textile, Toray Industries, Arvind Ltd, and Vardhman Textiles Ltd, among others.

Product Analysis

Natural Fibers dominates with 54.2% due to cotton volume and South Asian supply depth.

In 2025, Natural Fibers held a dominant market position in the By Raw Material segment of the APAC Textile Market, with a 54.2% share. Cotton production concentrated in India, Bangladesh, and Pakistan underpins this lead. Buyers source natural fibers for both performance and certification compliance, making this segment structurally resistant to full synthetic substitution.

Synthetic Fibers serve as the primary raw material for technical textiles, activewear, and non-woven applications. Polyester dominates synthetic output by volume, with China leading global polyester filament production. Synthetic fibers enable performance characteristics — stretch, moisture management, durability — that natural fibers cannot replicate, keeping demand structurally anchored in performance end-uses.

Process/Technology Analysis

Woven dominates with 45.4% due to broad apparel and technical textile applicability.

In 2025, Woven fabrics held a dominant market position in the By Process/Technology segment of the APAC Textile Market, with a 45.4% share. Woven construction serves apparel, home textiles, and technical fabric applications with equal effectiveness. This cross-category versatility sustains woven’s lead even as non-woven volumes grow in medical and hygiene segments.

Knitted fabrics serve the sportswear, casualwear, and intimate apparel segments where stretch and comfort drive buying decisions. Circular knitting capacity in Bangladesh, Sri Lanka, and China aligns directly with global activewear brand sourcing demands. Knitted construction’s ability to reduce material waste versus cut-and-sew wovens also attracts sustainability-focused buyers seeking lower input-to-output ratios.

Non-woven fabrics cover the highest-growth application set within the process segment, serving medical, hygiene, filtration, and geotextile markets. According to Global Efficiency Intel, electrification of industrial heating in Indian textile facilities demonstrated energy savings of approximately 17 GWh per year — a 26% reduction — signaling that non-woven producers adopting electrified processing gain both cost and emissions compliance advantages over conventionally powered competitors.

Spunlaid (Spunbond/Melt-blown) dominates non-woven sub-processes by volume, particularly in hygiene and filtration applications. COVID-19 demand accelerated APAC spunbond and melt-blown investment; that capacity now serves growing domestic demand for hygiene products across Southeast Asia and India’s expanding consumer health sector.

3-D Weaving & Spacer Fabrics represent the technical frontier of APAC textile manufacturing. These structures serve aerospace composites, protective apparel, and medical implant textiles where three-dimensional fiber architecture delivers performance unavailable in conventional flat fabrics. APAC producers in Japan, South Korea, and China lead development here, competing directly with European advanced textile manufacturers for defense and aerospace supply contracts.

Application Analysis

Fashion & Apparel dominates with 49.5% due to APAC’s global garment export infrastructure.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the APAC Textile Market, with a 49.5% share. The region’s integrated supply chain — from fiber to finished garment — gives APAC apparel manufacturers a turnaround speed and cost structure that sustains this lead across all price tiers of global retail.

Industrial/Technical Textiles represent the highest-margin opportunity within the APAC application landscape. Defense procurement, automotive OEM specifications, and infrastructure construction all generate non-cyclical demand for performance-certified fabrics. Manufacturers pivoting from commodity apparel to technical textiles access longer contracts and less price competition — a structural upgrade that APAC mill operators are actively pursuing.

Household & Home Textiles benefit from APAC’s own rising middle class as the primary demand engine, alongside export volumes to the US and European retail markets. China dominates home textile exports, while India holds strong positions in bedding and toweling. Domestic consumption growth across Southeast Asia reduces dependence on Western retail demand cycles.

Medical & Healthcare Textiles occupy a fast-expanding niche driven by hospital infrastructure investment across India, China, and Southeast Asia. Single-use surgical drapes, wound care materials, and hygiene nonwovens all require APAC-manufactured inputs. Regulatory quality certification requirements create a barrier that protects margin for compliant APAC producers against lower-standard competition.

Automotive & Transport Textiles track vehicle production volumes across APAC’s dominant auto manufacturing hubs — China, Japan, South Korea, and India. Interior fabrics, seat covers, acoustic insulation, and tire cord all require specialized textile inputs. EV platform growth introduces new technical textile requirements for battery thermal management and lightweight composite applications.

Key Market Segments

By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Brand-Mandated Supplier Decarbonization Reshapes APAC Textile Procurement

Global retail brands now impose binding emissions and energy targets directly on their APAC supplier factories. According to H&M Group’s 2025 energy report, coal use across its supplier base fell from 118 factories in 2022 to just 10 by Q3 2025. This pace of change proves that brand procurement power — not government regulation alone — drives decarbonization timelines in APAC textile supply chains.

Supplier factories unable to demonstrate compliance with buyer energy standards risk contract cancellation in favor of verified clean-energy producers. This dynamic creates a two-tier supplier landscape: manufacturers that invest in grid renewables, electrified heat systems, and certified energy procurement gain contract security; those that delay face accelerating commercial exposure regardless of their cost position.

Additionally, improved energy traceability across H&M’s supply chain reduced unknown energy reporting from 27% in 2024 to 16% in 2025. This closing transparency gap means APAC manufacturers can no longer rely on data opacity to avoid scrutiny. Buyers now have the visibility tools to enforce standards at Tier 1, 2, and 3 supplier levels — fundamentally changing the compliance calculus for the entire APAC textile production base.

Restraints

High Carbon Dependency and Water Intensity Create Compliance Cost Pressure Across APAC Mills

APAC textile manufacturing carries structural environmental liabilities that translate directly into capital expenditure obligations. According to Elevate Textiles’ 2025 Sustainability Report, the company achieved a 25% reduction in absolute water consumption — but reaching that benchmark required sustained facility-level investment over multiple years. Smaller mills without equivalent capital access face the same compliance targets with a fraction of the investment capacity.

India’s coal-intensive wet processing infrastructure illustrates the sector-wide challenge. Replacing fossil fuel heating with electrified alternatives requires upfront equipment investment that most mid-tier mill operators cannot self-fund. Consequently, the decarbonization timeline creates a capability gap between large integrated manufacturers and the fragmented SME base that accounts for the majority of APAC production capacity by unit count.

Moreover, wastewater treatment costs add another layer of operating burden. Effluent standards are tightening across India, Bangladesh, Vietnam, and Indonesia as regulators respond to environmental degradation from textile discharge. Mills that must retrofit treatment systems while simultaneously managing energy transition costs face compressed margins — slowing production modernization and, in some cases, forcing factory closures that reduce available manufacturing capacity.

Growth Factors

Circular Manufacturing and Water Reuse Technology Open New Competitive Tiers for APAC Producers

Circular textile manufacturing is transitioning from a brand marketing claim into a cost reduction mechanism. According to a SMEP Textiles Wastewater Management pilot in Bangladesh, a reverse osmosis system treated up to 2,400 cubic meters of water per day and recovered 50% of treated wastewater for direct reuse. Facilities deploying this technology reduce both freshwater procurement costs and effluent disposal fees simultaneously — a double-sided financial benefit.

The same Bangladesh pilot demonstrated that each cubic meter of wastewater treated with reverse osmosis avoided 17 to 30 kg of CO2e emissions compared to conventional discharge methods. For APAC manufacturers operating under Scope 3 reporting requirements from global brand clients, this emissions avoidance translates into verifiable ESG performance data — a commercial asset in contract negotiations with sustainability-committed buyers.

Therefore, manufacturers that invest in wastewater reuse and circular processing infrastructure gain on multiple fronts: lower operating costs, reduced regulatory exposure, and stronger buyer certification eligibility. This convergence of financial and compliance incentives creates a clear growth pathway for APAC mills willing to treat environmental infrastructure as a revenue-protecting asset rather than a compliance cost center.

Emerging Trends

AI-Driven Fabric R&D and Energy Efficiency Practices Signal the Next APAC Competitive Divide

Artificial intelligence is entering APAC textile manufacturing through fabric design, quality control, and process optimization. In April 2026, textile tech startup STCH raised USD 5.5 million in pre-Series A funding for AI-driven fabric R&D and sustainable textile manufacturing. This early-stage capital flow confirms that investors see AI-enabled textile design as a commercially viable differentiation strategy — not a distant research concept.

Energy efficiency at the facility level is becoming a documented competitive variable. According to the Asia Clean Energy Forum, Tay Ninh province in Vietnam achieved electricity savings of 537.2 million kWh through energy efficiency deployment, reducing sector emissions by 25.3%. Manufacturers achieving these efficiency gains lower their per-unit production cost while simultaneously improving their carbon footprint metrics for brand audit purposes.

Consequently, the convergence of AI-enabled design, energy efficiency monitoring, and emissions measurement tools is creating a new capability tier within APAC textile manufacturing. Early movers that integrate these systems gain production cost advantages and buyer certification eligibility that compound over time. Manufacturers that treat these as optional upgrades rather than strategic investments risk displacement as brand sourcing criteria evolve toward verified performance standards.

Key Company Insights

Shenzhou International Group holds a structurally advantaged position as one of the world’s largest vertically integrated knitwear manufacturers. Its end-to-end control — from yarn to finished garment — enables consistent quality at scale while compressing per-unit costs below standalone cut-and-sew competitors. This integration model attracts global sportswear brands seeking reliable high-volume partners with full supply chain accountability.

Weiqiao Textile positions itself as a dominant cotton yarn and fabric producer concentrated in China’s domestic and export markets. Its scale in cotton spinning gives it significant raw material procurement leverage and price stability advantages over smaller regional mills. However, Weiqiao’s concentration in conventional cotton processing creates exposure to sustainability mandates pushing brands toward recycled and certified fiber sourcing.

Toray Industries differentiates through advanced synthetic fiber and technical textile capabilities that commodity weavers cannot replicate. Its carbon fiber, high-performance nylon, and functional polyester products serve automotive, aerospace, and sportswear clients who prioritize material performance over price. This positions Toray at the high-value end of the APAC textile market where margin pressure is structurally lower than in commodity apparel.

Arvind Ltd combines its established denim and apparel fabric business with an aggressive technical textile expansion strategy. In May 2026, its subsidiary Arvind Advanced Materials acquired a 61% stake in US-based Dalco-GFT for approximately USD 136 million, targeting the needle-punched non-woven segment. This acquisition signals Arvind’s intent to compete in specialized technical fabric markets beyond its traditional apparel fabric base.

Key Players

- Shenzhou International Group

- Weiqiao Textile

- Toray Industries

- Arvind Ltd

- Vardhman Textiles Ltd

- Hyosung TNC

- Bombay Rayon Fashions

- Luthai Textile

- Nisshinbo Holdings

- Raymond Ltd

- Fabindia Overseas

- Teijin Ltd

Recent Developments

- February 2026 — Gurugram-based Jain Cord Industries secured ₹200 crore in its first institutional funding round, led by the Lohia Family Office (Indorama Capital), valuing the company at approximately ₹829 crore (USD 94.75 million) post-money. The capital targets modernization of weaving facilities, debt repayment, and market expansion across India.

- 2025 — H&M Group’s energy traceability initiative reduced unknown energy reporting across its Tier 1, 2, and 3 textile producers from 27% in 2024 to 16% in 2025, improving supply chain emissions visibility and strengthening its ability to enforce supplier-level clean energy standards across APAC manufacturing hubs.

- 2025 — A SMEP Textiles pilot in Bangladesh demonstrated a reverse osmosis wastewater system capable of treating 2,400 cubic meters per day and recovering 50% of processed water for reuse, while avoiding 17 to 30 kg of CO2e emissions per cubic meter compared to conventional discharge methods.

- 2024–2025 — Tay Ninh province in Vietnam documented electricity savings of 537.2 million kWh through textile and garment sector energy efficiency programs, achieving a 25.3% reduction in total sector emissions and establishing one of the most documented provincial clean energy performance records in APAC textile manufacturing.

- 2024–2025 — Under a SWITCH-Asia circular textile policy pilot in Indonesia, participating facilities achieved 18% water savings, 52% energy savings, and a 50% reduction in combined Scope 1 and 2 emissions — demonstrating that circular manufacturing delivers operational cost reductions alongside environmental compliance outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 396.8 Billion |

| Forecast Revenue (2035) | USD 535.2 Billion |

| CAGR (2026-2035) | 3.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Natural Fibers (Cotton, Wool, Silk), Synthetic Fibers (Polyester, Nylon, Rayon/Viscose, Acrylic, Polypropylene, Recycled Fibers, Others)), By Process/Technology (Woven, Knitted, Non-woven (Spunlaid, Dry-laid Hydro-entangled, Wet-Laid, Needle-punched, 3-D Weaving & Spacer Fabrics)), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Shenzhou International Group, Weiqiao Textile, Toray Industries, Arvind Ltd, Vardhman Textiles Ltd, Hyosung TNC, Bombay Rayon Fashions, Luthai Textile, Nisshinbo Holdings, Raymond Ltd, Fabindia Overseas, Teijin Ltd |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |