Quick Navigation

Report Overview

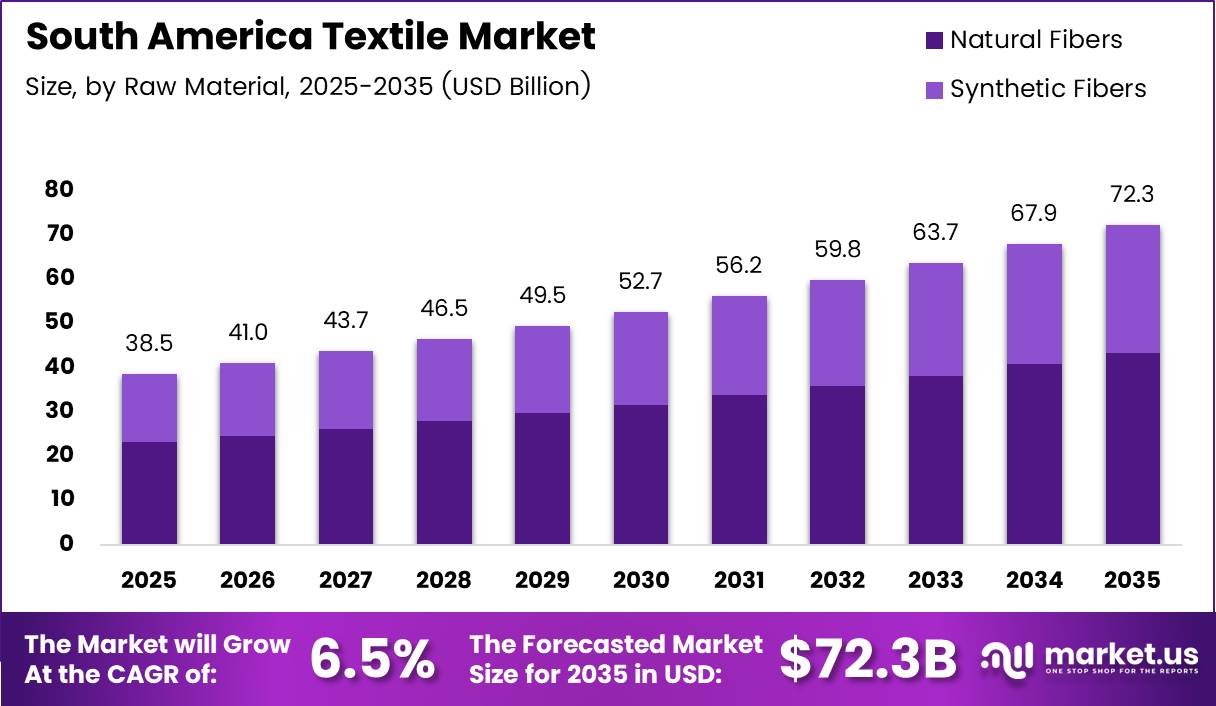

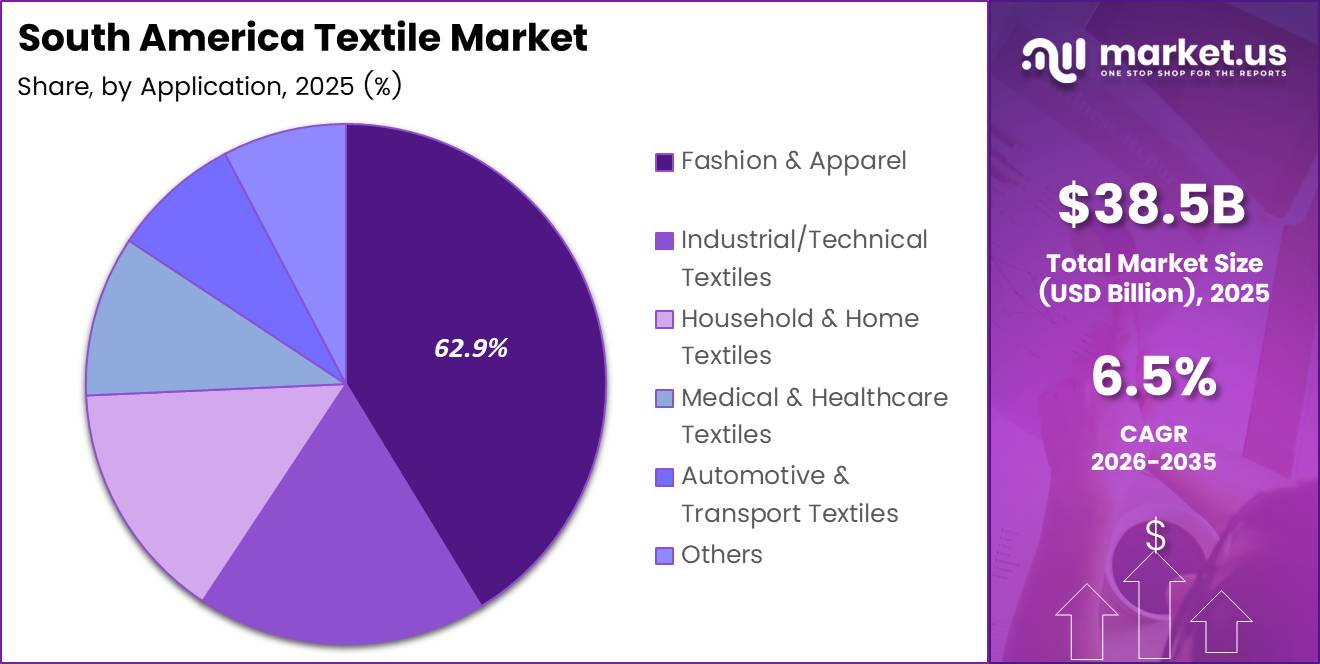

South America Textile Market size is expected to be worth around USD 72.3 Billion by 2035 from USD 38.5 Billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

South America’s textile sector spans the full production chain — from raw fiber cultivation and processing to finished apparel and technical fabrics. The market covers synthetic and natural fiber manufacturing, weaving and knitting operations, and end-use applications from fashion to industrial filtration. Brazil anchors regional output, supported by Argentina, Colombia, and Peru.

Synthetic fibers command 56.3% of raw material supply, reflecting a structural shift away from exclusively natural-fiber dependency. This shift lowers input cost volatility and allows manufacturers to respond faster to global fashion cycles. Consequently, facilities producing polyester and recycled variants hold a structural cost advantage over natural-fiber-only operations.

Fashion and apparel absorbs 62.9% of total textile output, confirming that consumer-facing demand remains the primary revenue engine. However, industrial and technical textiles represent the higher-margin growth segment, as infrastructure investment and mining activity across the region creates durable demand for filtration and geotextile products.

Brazil’s regulatory posture directly shapes market economics. The country launched its National Circular Economy Strategy in 2024, mandating textile manufacturers to promote material reuse and reduce production waste. This positions Brazilian producers favorably with global buyers who apply sustainability criteria to sourcing decisions — a competitive signal that extends beyond domestic compliance.

According to ITMF’s Global Textile Industry Survey of January 2026, South America’s business confidence balance reached +9 percentage points — the highest among all surveyed regions globally. This outperformance signals that regional manufacturers perceive forward order books and production conditions more positively than peers in South-East Asia, which posted −2 percentage points in the same survey.

According to ITMF’s May 2025 survey, South America had already posted a business confidence balance of +6 percentage points, ranking second globally after Africa. The consistent upward trajectory across two consecutive survey periods — from +6 to +9 points — indicates that regional sentiment is not a one-period anomaly but a directional trend supported by operational and trade fundamentals.

Trade policy shifts reinforce the market’s structural repositioning. U.S. tariff exemptions introduced in 2025 for recycled textile inputs directly benefit South American exporters with closed-loop manufacturing capabilities. Moreover, countries demonstrating supply chain sustainability receive fast-tracked customs clearance, creating a measurable trade cost advantage for compliant regional producers.

Key Takeaways

- The South America Textile Market was valued at USD 38.5 Billion in 2025 and is forecast to reach USD 72.3 Billion by 2035.

- The market grows at a CAGR of 6.5% over the forecast period 2026 to 2035.

- By Raw Material, Synthetic Fibers lead with a 56.3% share in 2025.

- By Process/Technology, Woven holds the dominant position with a 51.6% share.

- By Application, Fashion and Apparel commands 62.9% of market output in 2025.

- Brazil anchors the regional market, supported by its National Circular Economy Strategy launched in 2024.

- South America posted the highest business confidence balance of +9 percentage points among all global textile regions in January 2026, per ITMF.

- U.S. tariff exemptions on recycled textile inputs, introduced in 2025, create a direct export advantage for compliant South American producers.

Product Analysis

Synthetic Fibers dominate with 56.3% due to cost stability and production scalability.

In 2025, Synthetic Fibers held a dominant market position in the By Raw Material segment of the South America Textile Market, with a 56.3% share. Their dominance reflects manufacturers’ preference for inputs that decouple production costs from agricultural cycles. Synthetic fibers allow consistent quality output at volume, which natural fibers cannot match during harvest disruptions or price spikes.

Natural Fibers retain a structurally important role despite lower overall share. Premium positioning, organic certification markets, and export demand from European brands committed to natural-fiber sourcing sustain this segment. Moreover, cotton in particular anchors domestic apparel supply chains across Brazil, Peru, and Argentina.

Process/Technology Analysis

Woven dominates with 51.6% due to structural versatility across apparel and technical applications.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the South America Textile Market, with a 51.6% share. Woven fabric’s tensile strength and dimensional stability make it the default process for denim, workwear, home textiles, and industrial fabric. Its suitability across both fashion and technical end-uses gives it a breadth advantage no single alternative process matches.

Knitted fabric commands the fastest-growing process share within established textile technologies. Its stretch properties and comfort characteristics drive adoption in activewear, casual apparel, and medical compression garments — categories where South American manufacturers compete effectively on cost against Asian suppliers. Additionally, Magalu’s June 2024 partnership with AliExpress, which saw share price rise 12%, signals that cross-border fashion demand will reward knitted product suppliers with broader distribution reach.

Non-woven technology anchors the industrial and medical textile segments. Its ability to produce functional fabrics without weaving or knitting infrastructure reduces capital requirements and enables rapid product customization for filtration, hygiene, and packaging applications.

Spunlaid (Spunbond/Melt-blown) technology targets hygiene, medical, and filtration end-uses requiring consistent fiber distribution at high output speeds. South American healthcare sector growth and infrastructure investment in water filtration sustain demand for spunlaid nonwovens, making this sub-process a high-growth pocket within the non-woven category.

3-D Weaving and Spacer Fabrics represent the technology frontier within South America’s textile processing landscape. These advanced structures serve aerospace, protective equipment, and medical implant applications, where no conventional 2-D fabric can meet specification requirements. Regional investment in technical textile capabilities positions early adopters to capture premium contracts as local demand matures.

Application Analysis

Fashion and Apparel dominates with 62.9% due to consumer market depth and manufacturing concentration.

In 2025, Fashion and Apparel held a dominant market position in the By Application segment of the South America Textile Market, with a 62.9% share. Brazil, Colombia, and Peru host large-scale garment manufacturing industries that supply both domestic consumption and international fast-fashion and private-label buyers. This concentration makes apparel the volume anchor of regional textile demand.

Industrial and Technical Textiles carry the highest margin potential within the South America application mix. Mining, infrastructure, chemical processing, and filtration industries require specialized fabrics that command prices multiples above commodity apparel fabric. Valmet’s March 2026 inauguration of a dedicated filter-fabric factory in Minas Gerais, Brazil, confirms that international suppliers are investing directly in local technical textile supply capacity.

Household and Home Textiles serve a large domestic consumer base across Brazil and Argentina. Bedding, toweling, and furnishing fabrics benefit from urbanization trends and an expanding middle-income population. However, this segment faces import competition, particularly from Asian low-cost producers, which pressures domestic manufacturers on price.

Medical and Healthcare Textiles represent a structurally defensive segment with above-average margin characteristics. Surgical drapes, wound care materials, and hospital linen generate recurring institutional demand that does not follow fashion cycles. Consequently, manufacturers who qualify for medical-grade certification gain revenue stability unavailable in consumer-facing segments.

Automotive and Transport Textiles benefit from vehicle production activity concentrated in Brazil and Argentina. Seat covers, carpeting, insulation, and filtration media generate steady demand tied to automotive output volumes. Moreover, lightweighting trends in vehicle design open new technical specification requirements that advanced textile producers can fulfill.

Key Market Segments

By Raw Material

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

- Natural Fibers

- Cotton

- Wool

- Silk

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Operational Efficiency Gains and Trade Policy Shifts Accelerate South American Textile Competitiveness

South American textile manufacturers have implemented lean manufacturing across dyeing operations with measurable results. According to research published in 2025 (IJRES), lean manufacturing implementation in textile dyeing reduced machine stoppages by 52%. This directly translates to lower per-unit production cost and higher throughput — conditions that make regional producers more price-competitive against Asian suppliers on lead time-sensitive orders.

Trade policy changes in 2025 created a direct export incentive for manufacturers with recycled content capabilities. U.S. tariff exemptions now apply to fabric made from post-consumer or post-industrial recycled content, qualifying South American exporters for partial or full tariff reductions. Manufacturers who invested in recycled fiber integration now face a structural cost advantage in the U.S. market that competitors without these capabilities cannot replicate quickly.

Additionally, U.S. customs policy now grants fast-tracked clearance to countries demonstrating textile supply chain sustainability, including low water usage and closed-loop manufacturing. Brazil’s National Circular Economy mandate aligns domestic manufacturers with exactly these criteria. Therefore, regulatory compliance in Brazil is no longer just a domestic obligation — it has become a direct driver of export market access and cost advantage.

Restraints

U.S. Tariff Reclassification and Input Cost Pressures Constrain South American Export Margins

As of Q1 2025, U.S. tariffs on leather accessories and non-athletic footwear from Brazil were reclassified under higher duty codes. This reclassification directly raises landed costs for Brazilian exporters in affected product categories, narrowing margins and reducing price competitiveness against producers in lower-tariff countries. Exporters in these categories must absorb cost increases or reduce profitability to maintain volume.

Production lead times remain a structural constraint for South American manufacturers competing for fast-fashion and private-label orders. Private label clothing production lead times in 2025 range from 8 to 24 weeks depending on location, order size, and factory availability. The 16-week spread between best and worst-case scenarios creates uncertainty for buyers who require reliable delivery windows, limiting South America’s competitiveness for time-sensitive programs.

The investment required to meet evolving sustainability and efficiency benchmarks is another friction point. Italy’s Transizione 5.0 program, referenced as a benchmark by South American manufacturers, requires documented energy reduction of at least 3% at site level or 5% for specific processes to qualify for support. Smaller regional manufacturers who lack capital to fund efficiency upgrades or verification systems face a widening competitive gap against better-capitalized peers.

Growth Factors

Brazil’s Circular Economy Mandate and Regional Supply Chain Repositioning Open New Revenue Channels

Brazil’s National Circular Economy Strategy, launched in 2024, mandates textile producers to promote material reuse and reduce production waste. This regulatory push does more than enforce compliance — it creates a certified production profile that European and North American buyers actively seek. Manufacturers who build closed-loop fiber systems now access a premium buyer segment that rewards sustainability credentials with longer-term sourcing contracts.

South American sourcing reduces transit times relative to Asian supply chains, and this speed advantage directly benefits manufacturers competing for private-label programs. Private label production lead times in 2025 range from 8 to 24 weeks, with South American proximity to U.S. and European buyers delivering lower transit time. For brands managing inventory risk, shorter total lead times reduce working capital requirements — a buyer benefit that supports sourcing reallocation toward regional suppliers.

An integrated lean and machine learning approach to optimize textile and apparel production processes in Latin America was published in 2025, addressing a documented research gap in data-driven manufacturing optimization for the region. The development of locally relevant production models gives regional manufacturers access to optimization methodologies previously unavailable in systematic form, directly supporting productivity and margin improvement without requiring imported process frameworks.

Emerging Trends

Data-Driven Manufacturing and Sustainability-Linked Trade Access Reshape South American Textile Operations

A 2025 IEEE Latin America Transactions case study applied quantitative methodology to textile manufacturing and produced measurable improvements in operational metrics. This signals a shift from intuition-based to data-driven production management in the region. Manufacturers who adopt machine learning-supported process optimization gain compounding efficiency advantages over time — a structural differentiation that commodity producers relying on manual oversight cannot close easily.

According to ITMF’s January 2026 Global Textile Industry Survey, South America posted the highest business confidence balance of +9 percentage points among all surveyed regions. This reading, up from +6 points in May 2025, indicates that manufacturers perceive forward demand conditions and order pipelines positively. For suppliers and investors evaluating regional allocation, sustained confidence outperformance relative to South-East Asia’s −2 points represents a directional signal, not an outlier.

Sustainability-linked trade access is reshaping the competitive calculus for regional exporters. The combination of Brazil’s circular economy mandate and U.S. tariff exemptions for recycled-content textiles creates a policy-reinforced pathway where environmental investment generates direct commercial return. Manufacturers who treat sustainability as a compliance cost miss the trade advantage it now unlocks — this is a strategic reframing with real margin consequences.

Key Company Insights

Vicunha Têxtil positions itself as the dominant integrated denim and cotton fabric producer in South America. Its vertical integration — from spinning through weaving and finishing — reduces external supplier dependency and gives it pricing control across the value chain. This integration advantage is particularly powerful during input cost volatility, allowing Vicunha to protect margins when raw material prices fluctuate.

Coteminas S.A. operates one of the broadest product portfolios in the Brazilian textile sector, spanning home textiles, apparel fabrics, and yarn. Its scale allows cross-segment cost absorption and reduces dependence on any single end-use category. However, portfolio breadth also creates complexity risk, requiring disciplined operational management to prevent margin dilution across less-profitable product lines.

Santana Textiles Group focuses on denim fabric manufacturing, supplying both domestic Brazilian apparel producers and international fashion brands. Its specialization creates depth of product development capability and buyer relationships that generalist producers cannot replicate. Additionally, Valmet’s March 2024 investment decision to build a filter-fabric facility in Minas Gerais signals that specialized technical textile producers are expanding regional infrastructure — a competitive signal relevant to all segment-focused players.

Buddemeyer S.A. concentrates on premium home textiles, particularly toweling and bedding for hospitality and retail channels. Its positioning in higher-specification products insulates it from commoditized price competition. Moreover, hospitality sector recovery and hotel infrastructure investment across South America provide a durable demand base that sustains Buddemeyer’s premium channel positioning.

Key Players

- Vicunha Têxtil

- Coteminas S.A.

- Santana Textiles Group

- Buddemeyer S.A.

- Springs Global

- Lenzing AG

- Freudenberg Performance Materials

- Indorama Ventures (PET Brazil)

- Ahlstrom-Munksjö

- Beaulieu Technical Textiles

- HUESKER Synthetic GmbH

- TWE Group

Recent Developments

- March 2026 — Valmet officially inaugurated its South America filter-fabric factory in Vespasiano, Minas Gerais, a 12,000 m² facility dedicated to producing filter fabrics for industrial clients across Latin America. The inauguration expands local availability of high-specification textile-based filtration media, reducing regional buyers’ dependence on imported technical textile products.

- June 2024 — Brazilian retailer Magazine Luiza (Magalu) announced a strategic partnership with AliExpress, enabling each company to sell complementary products on the other’s marketplace, including fashion and apparel categories. The agreement extends the distribution reach of South American textile and apparel products into AliExpress’s international buyer base.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 38.5 Billion |

| Forecast Revenue (2035) | USD 72.3 Billion |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Synthetic Fibers: Polyester, Nylon, Rayon/Viscose, Acrylic, Polypropylene, Recycled Fibers, Others; Natural Fibers: Cotton, Wool, Silk), By Process/Technology (Woven, Knitted, Non-woven: Spunlaid, Dry-laid Hydro-entangled, Wet-Laid, Needle-punched; 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Vicunha Têxtil, Coteminas S.A., Santana Textiles Group, Buddemeyer S.A., Springs Global, Lenzing AG, Freudenberg Performance Materials, Indorama Ventures (PET Brazil), Ahlstrom-Munksjö, Beaulieu Technical Textiles, HUESKER Synthetic GmbH, TWE Group |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |