Quick Navigation

Report Overview

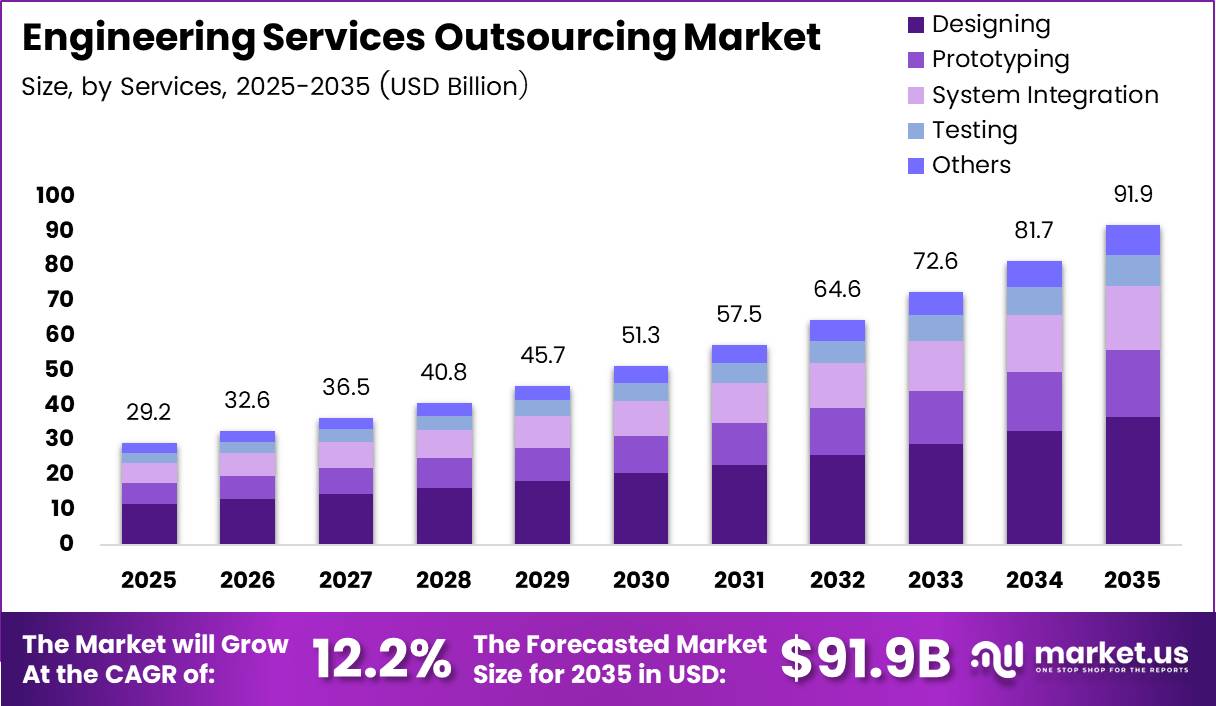

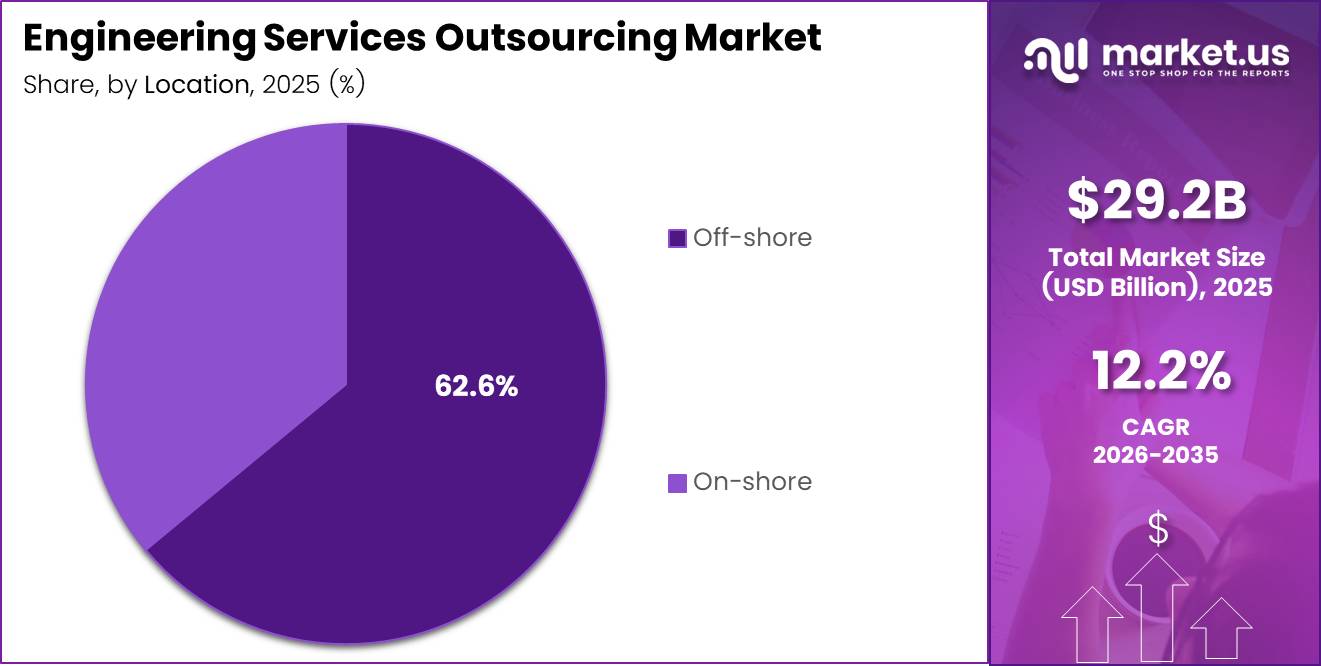

Global Engineering Services Outsourcing Market size is expected to be worth around USD 91.9 Billion by 2035 from USD 29.2 Billion in 2025, growing at a CAGR of 12.2% during the forecast period 2026 to 2035.

Engineering services outsourcing (ESO) covers the delegation of core technical functions including product design, system integration, testing, and prototyping to external specialist providers. Companies across automotive, aerospace, semiconductors, and healthcare sectors use ESO to access deep engineering expertise without building permanent in-house capacity. The market now spans onshore, nearshore, and offshore delivery models.

The 12.2% CAGR reflects something more structural than cyclical demand. Companies are not just cutting costs. They are accessing capabilities they cannot build internally fast enough. Digital engineering, autonomous systems, and embedded software require skill sets that most industrial firms cannot develop at the pace their product roadmaps demand.

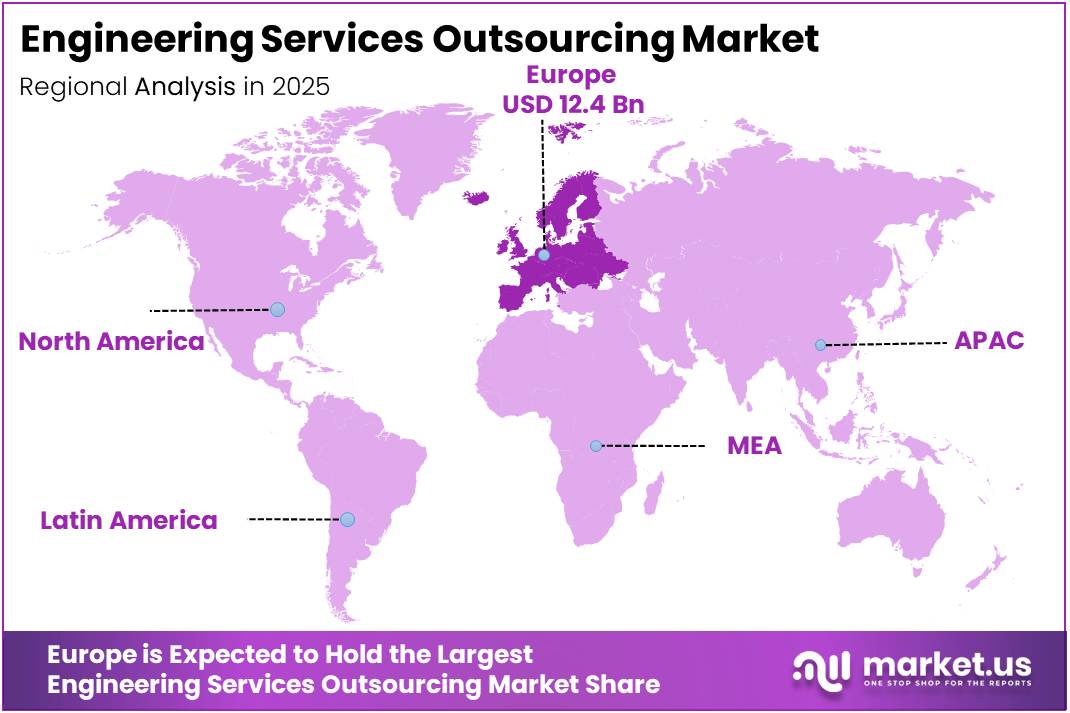

Europe holds the largest regional share at 42.70%, with a market value of USD 12.4 Billion in 2025. European manufacturers in automotive and aerospace have historically relied on external engineering partners for both design validation and systems integration work. This structural dependency reinforces Europe’s position as the highest-value ESO consumption region globally.

Government and regulatory frameworks in key markets are accelerating outsourced engineering adoption. Defense modernization programs, EV transition mandates, and digital infrastructure investments across North America, Europe, and Asia Pacific are generating multi-year engineering workloads. These cannot be absorbed by internal engineering teams alone, creating sustained demand for external delivery partners.

In August 2025, L&T Technology Services launched PLxAI, a proprietary Generative AI framework designed to accelerate the Product Development Life Cycle. This signals a broader industry shift where ESO providers are embedding AI tooling directly into engineering workflows, not just offering labor arbitrage. Providers that move fastest here will redefine their value proposition beyond cost savings.

According to NASSCOM, India-headquartered engineering R&D service providers generated around USD 19–20 Billion in revenue in FY2025. This figure represents a mature, scaled outsourcing base handling tens of billions of dollars in engineering work annually. It confirms that offshore ESO delivery has moved well beyond a niche or experimental model into a foundational component of global engineering supply chains.

As per NASSCOM, India’s ESO providers deliver approximately 50–65% cost savings compared with sourcing equivalent engineering work from Europe and Latin America, while maintaining comparable quality levels. For enterprise buyers weighing build-versus-buy decisions, this cost differential is not marginal. It is large enough to shift capital allocation strategies and accelerate outsourcing decisions across entire business units.

Key Takeaways

- The Global Engineering Services Outsourcing Market was valued at USD 29.2 Billion in 2025 and is forecast to reach USD 91.9 Billion by 2035.

- The market advances at a CAGR of 12.2% during the forecast period 2026 to 2035.

- By Services, Designing holds the dominant share at 36.3% in 2025.

- By Location, Offshore delivery leads with a 62.6% share of the market in 2025.

- By Application, Automotive accounts for the largest share at 19.5% in 2025.

- Europe dominates all regions with a 42.70% market share, valued at USD 12.4 Billion in 2025.

Services Analysis

Designing dominates with 36.3% due to upstream placement in every product cycle.

In 2025, Designing held a dominant market position in the By Services segment of the Engineering Services Outsourcing Market, with a 36.3% share. Design work sits at the front of every product development cycle. Outsourcing this function gives clients access to specialized CAD, simulation, and systems design expertise while compressing time-to-prototype. The value captured here flows through all downstream engineering stages.

Prototyping services translate design outputs into physical or virtual product models for testing and validation. Companies outsource prototyping to reduce internal lab investment and access rapid iteration capabilities. According to a Deloitte–NASSCOM study, over 80% of engineering organizations increased ER&D budgets to support technologies including advanced simulation, much of which is executed through outsourced providers. This directly sustains prototyping service demand.

System Integration covers the assembly and validation of multi-component engineering systems into cohesive functional products. In June 2024, Capgemini acquired D+I, an Australian product design and development consultancy, specifically to strengthen its product engineering and intelligent industry capabilities. This acquisition reflects how providers are vertically integrating to offer both design and integration services under one roof, improving stickiness with enterprise clients.

Testing services verify that engineered systems meet performance, safety, and regulatory standards before market release. The shift toward software-defined products in automotive and aerospace has expanded the testing surface area considerably. Outsourced testing now includes hardware-in-the-loop, cybersecurity validation, and functional safety assessments. Providers with certified testing labs and domain-specific accreditation command premium pricing in this sub-segment.

Others in the By Services segment includes documentation engineering, regulatory filing support, configuration management, and aftermarket engineering services. These functions are increasingly outsourced alongside core technical delivery as clients seek to hand off the full engineering service stack rather than managing fragmented supplier relationships across multiple vendors.

Location Analysis

Offshore dominates with 62.6% due to proven cost efficiency and talent scale advantages.

In 2025, Offshore delivery held a dominant market position in the By Location segment of the Engineering Services Outsourcing Market, with a 62.6% share. The offshore model captures the widest cost differential between buyer and provider geographies. India alone accounts for the bulk of offshore ESO volume, supported by a large pool of accredited engineers across mechanical, software, and systems disciplines. The scale and depth of this talent base are not easily replicated elsewhere.

Onshore delivery serves clients where regulatory compliance, security clearance requirements, or real-time collaboration needs make offshore execution impractical. Defense, nuclear, and classified government engineering programs predominantly use onshore models. While the cost premium is significant, onshore providers compete on speed of iteration, direct IP control, and accountability under domestic contract law. This segment grows as governments mandate local engineering content in critical infrastructure.

Application Analysis

Automotive dominates with 19.5% due to electrification and software-defined vehicle engineering demand.

In 2025, Automotive held a dominant market position in the By Application segment of the Engineering Services Outsourcing Market, with a 19.5% share. The transition from internal combustion engines to electric and software-defined vehicles has fundamentally expanded the engineering scope for every OEM. Battery management systems, ADAS validation, and over-the-air software update platforms require specializations that most OEMs cannot build fast enough internally. ESO providers fill that gap directly.

Aerospace engineering outsourcing covers airframe structural analysis, avionics integration, MRO engineering, and certification documentation. The return of commercial aviation demand post-2023 and the expansion of defense budgets across NATO members have created sustained workloads for aerospace ESO providers. Certification-grade engineering work demands domain-specific expertise and significant regulatory familiarity, which specialist providers hold as a competitive barrier.

Manufacturing outsourcing focuses on plant automation design, robotics integration, and industrial IoT engineering. As factories accelerate Industry 4.0 adoption, engineering requirements for retrofitting legacy systems alongside new automation infrastructure have created dual-track workloads. ESO providers with both OT and IT engineering competencies capture the highest-value contracts in this application area.

Consumer Electronics engineering outsourcing includes mechanical design, PCB layout, firmware development, and regulatory compliance engineering for devices from wearables to smart home systems. Short product cycles and intense cost pressure drive brands to outsource the majority of non-core hardware engineering. Speed-to-market and component-level cost reduction are the primary selection criteria buyers apply when choosing ESO partners in this segment.

Semiconductors engineering outsourcing covers chip architecture, RTL design, verification, physical design, and post-silicon validation. The global chip shortage cycle exposed how few companies retained sufficient in-house semiconductor engineering depth. This accelerated outsourcing decisions across fabless design houses and systems companies building custom silicon. Specialist semiconductor ESO providers with EDA tool proficiency and process-node experience command premium contract values.

Healthcare engineering outsourcing spans medical device design, embedded systems development, biocompatibility testing support, and regulatory submission engineering. FDA 510(k) and CE mark pathways require extensive documentation and validation engineering that most device startups and mid-tier manufacturers outsource entirely. Regulatory complexity creates high switching costs, making healthcare ESO relationships among the most durable in the market.

Telecom engineering outsourcing includes network architecture design, protocol stack development, 5G radio access engineering, and OSS/BSS system integration. Carriers and network equipment vendors use ESO to manage the engineering labor intensity of major technology upgrade cycles without permanently expanding their engineering headcount between buildout phases.

Energy and Utilities engineering outsourcing covers substation design, grid protection engineering, renewable generation system design, and digital twin development for utility assets. The global push toward grid decarbonization and renewable capacity expansion has created multi-year ESO workloads in this segment. Engineering providers with power systems domain credentials and grid simulation competency are positioned to capture sustained contract volumes.

Construction and Infrastructure engineering outsourcing addresses structural design, BIM modeling, MEP engineering, and project commissioning support. Large infrastructure programs in the Middle East, Southeast Asia, and North America generate outsourced engineering demand that domestic workforces cannot absorb alone. Cross-border engineering delivery for complex civil projects is normalizing as design collaboration tools improve and certification mutual recognition frameworks expand.

Others in the By Application segment includes defense systems engineering, rail and transportation engineering, and marine engineering. These verticals share a common characteristic: high regulatory complexity, long program durations, and specialized certification requirements that make outsourcing to pre-qualified specialist providers the most practical path to managing engineering capacity.

Key Market Segments

By Services

- Designing

- Prototyping

- System Integration

- Testing

- Others

By Location

- Offshore

- Onshore

By Application

- Automotive

- Aerospace

- Manufacturing

- Consumer Electronics

- Semiconductors

- Healthcare

- Telecom

- Energy & Utilities

- Construction & Infrastructure

- Others

Drivers

Automotive Electrification and Industry 4.0 Programs Are Compelling Enterprises to Outsource Complex Engineering Functions at Scale

The shift toward electric vehicles and software-defined mobility is generating engineering workloads that OEMs cannot absorb internally. Battery system design, ADAS validation, and connected platform integration each require deep technical specialization. In July 2024, Capgemini acquired Lösch & Partner, a German systems engineering specialist, to expand its automotive systems engineering and application lifecycle services for OEM clients. This signals where ESO buyers are directing spending.

Industry 4.0 transformation is creating parallel demand across manufacturing, energy, and process industries. Plant automation, digital thread implementation, and IIoT integration require multi-disciplinary engineering teams that most industrials do not maintain permanently. Outsourcing these programs to experienced ESO providers reduces ramp time and avoids the recruitment and retention costs associated with specialized engineering talent in competitive labor markets.

According to a NASSCOM–Deloitte study, more than 50% of surveyed companies expected their 2024 ER&D spending to be 10–20% higher than in 2021. This sustained budget commitment confirms that engineering outsourcing is a structural priority for enterprise buyers, not a discretionary cost measure. For ESO providers, it means multi-year contract pipelines across automotive, industrial, and technology sectors will remain active through the forecast period.

Restraints

Intellectual Property Risks and Performance Accountability Gaps Create Friction in Cross-Border Engineering Outsourcing Deals

IP protection is the most frequently cited barrier in cross-border engineering engagements. Design files, proprietary algorithms, and manufacturing process data transferred to offshore providers fall under jurisdictions with varying levels of trade secret enforcement. Buyers in aerospace, defense, and semiconductor sectors face contractual and regulatory constraints that limit which engineering functions can legally be outsourced across borders. This structurally caps addressable market volume in high-sensitivity verticals.

Shortages of specialized engineers in semiconductor design, digital twins, and functional safety validation compound the IP challenge. ESO providers cannot deliver what they cannot staff. When demand for niche competencies outstrips available talent, providers substitute with less experienced engineers or subcontract further, which introduces quality and security exposure. Buyers respond by narrowing scope or returning functions in-house, both of which reduce outsourcing contract values.

According to axaengineers, acceptable schedule variance for outsourced engineering deliverables is contractually set at within 5% of original timelines. This narrow tolerance band reflects how demanding buyers have become on delivery accountability. When providers miss this threshold, buyers face downstream program delays, regulatory re-filing costs, and contractual penalties. A single high-profile delivery failure can terminate a multi-year outsourcing relationship and prompt competitors to rebuild in-house engineering capacity.

Growth Factors

Renewable Energy, Medical Device Engineering, and Embedded Software Are Creating New Long-Cycle Outsourcing Revenue Streams

Renewable energy infrastructure buildout is generating sustained ESO demand across wind turbine structural engineering, solar farm electrical design, hydrogen system integration, and grid modernization projects. These programs run across multiple years and require multi-disciplinary engineering teams. In August 2025, Cyient announced plans to enter advanced chip design engineering targeting automotive, aerospace, defense, medical equipment, and data-center applications, signaling provider expansion into high-growth verticals.

Medical device engineering outsourcing benefits from regulatory complexity that most mid-tier device companies cannot manage internally. FDA and CE certification pathways require validation engineering, design history file management, and risk analysis documentation that specialist providers deliver faster and at lower cost than internal teams. This creates high-retention outsourcing relationships with recurring revenue characteristics, making healthcare ESO one of the highest-margin application segments.

According to microsourcing, engineering teams pursue offshoring when they can realize labor cost differentials of 40–70% compared with onshore rates. For renewable energy and medical device programs, where engineering labor constitutes a major share of project cost, this differential translates directly into project feasibility decisions. Programs that are borderline viable onshore become commercially attractive when offshore ESO delivery is factored into the cost model.

Emerging Trends

Generative AI Integration and Cloud-Based Engineering Platforms Are Redefining How Outsourced Engineering Work Is Delivered and Priced

Generative AI tools are now embedded into product design, testing, and engineering documentation workflows at leading ESO providers. AI-assisted code generation, design verification, and simulation acceleration are compressing delivery timelines while expanding the scope of work a given engineering team can execute. Providers that integrate these tools successfully into production workflows gain a structural speed and cost advantage over those still relying on manual engineering processes.

Cloud-based collaborative engineering environments and Product Lifecycle Management platforms are replacing legacy on-premises toolchains. This shift enables real-time collaboration between client engineering teams and offshore providers, reducing the coordination friction that historically limited the complexity of work that could be safely outsourced. Model-Based Systems Engineering adoption further supports this, standardizing how requirements, architecture, and verification evidence are shared across distributed teams.

According to ISG, HCM SaaS fees in outsourced environments are 28% lower over the last five years and 25% lower over the last three years to 2025. This pattern of compressing per-unit technology costs in mature outsourcing relationships is directly applicable to engineering services environments. Buyers who lock in long-term ESO partnerships now benefit from declining unit costs as provider productivity improves and AI tooling amortizes across growing delivery volumes.

Regional Analysis

Europe Dominates the Engineering Services Outsourcing Market with a Market Share of 42.70%, Valued at USD 12.4 Billion

Europe holds the largest share of the global ESO market at 42.70%, valued at USD 12.4 Billion in 2025. Germany’s automotive and mechanical engineering ecosystem, France’s aerospace cluster, and the UK’s defense and energy sectors generate persistent outsourcing demand that European providers and offshore delivery centers serve in parallel. Stringent product liability and safety regulations in these industries create complex engineering documentation requirements that specialist outsourcing partners manage on behalf of OEMs.

North America Engineering Services Outsourcing Market Trends

North America represents the second largest ESO consumption region, anchored by the US defense, semiconductor, and healthcare sectors. Federal investment in domestic chip manufacturing through the CHIPS Act and expanded defense procurement budgets are generating multi-year engineering program workloads. US buyers combine onshore providers for classified and compliance-sensitive work with offshore providers for non-sensitive design and validation tasks, creating hybrid delivery models that optimize cost and control simultaneously.

Asia Pacific Engineering Services Outsourcing Market Trends

Asia Pacific functions as both a major ESO consumption region and the world’s largest delivery base. India generates the majority of offshore ESO revenue, with a talent pool of accredited engineers across software, systems, and mechanical disciplines. China, South Korea, and Japan drive regional ESO demand through their consumer electronics, semiconductor, and automotive manufacturing ecosystems. Intra-regional outsourcing between high-cost Japanese and Korean manufacturers and lower-cost Indian and Southeast Asian providers is an accelerating structural pattern.

Latin America Engineering Services Outsourcing Market Trends

Latin America is growing as a nearshore ESO destination for North American buyers seeking time-zone alignment and Spanish-language capability alongside cost reduction. Brazil and Mexico host growing engineering delivery centers serving US automotive, industrial, and energy clients. Nearshore delivery reduces collaboration overhead compared with offshore models, making it attractive for programs requiring iterative design reviews and close client interaction throughout the engineering lifecycle.

Middle East and Africa Engineering Services Outsourcing Market Trends

The Middle East is generating new ESO demand through infrastructure megaprojects, energy transition programs, and defense modernization investments across Saudi Arabia, the UAE, and Qatar. GCC governments are funding large-scale engineering programs in smart cities, hydrogen infrastructure, and grid electrification. These programs require engineering specializations that local workforces cannot supply at scale, creating sustained import demand for offshore and nearshore ESO providers with relevant domain credentials.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AKKA Technologies positions itself as a pure-play engineering and technology services provider with deep roots in European automotive and aerospace accounts. The firm’s concentration in high-value design and validation work for German and French OEMs gives it a defensible revenue base tied to long product development programs. However, its European focus creates exposure to regional slowdowns in automotive capital investment, particularly as OEMs rationalize engineering spend during EV transition periods.

Alten Group operates a broad multi-vertical ESO model spanning automotive, aerospace, defense, and life sciences clients across Europe and internationally. Its geographic diversification reduces single-sector revenue concentration, but the firm competes in a fragmented talent market where retaining specialized engineers across multiple domains simultaneously is operationally demanding. Alten’s scale enables competitive pricing on volume contracts, but differentiation on technical depth remains a persistent challenge in commoditizing service lines.

Capgemini Engineering deploys the broadest market positioning among ESO providers, combining management consulting heritage with engineering delivery scale. In June 2024 and July 2024, Capgemini completed two targeted acquisitions in Australia and Germany to strengthen product engineering and automotive systems capabilities. This acquisition pace signals a deliberate strategy to close capability gaps through inorganic means, targeting verticals where organic talent development would take too long given client demand timelines.

Entelect focuses on software engineering and digital product development outsourcing, primarily serving technology-driven clients in financial services and retail. Its positioning in software-defined engineering differentiates it from hardware-centric ESO providers. As industrial and manufacturing clients increase software content in physical products, Entelect’s core competencies become increasingly relevant outside its traditional sector base. The firm’s ability to scale into embedded software and digital twin services will determine its addressable market expansion rate.

Key Players

- AKKA Technologies

- Alten Group

- Capgemini Engineering

- Entelect

- HCL Technologies Limited

- Emerson Electric Co

- Infosys Limited

- Tata Elxsi

- Tata Consultancy Services Limited

- Tech Mahindra Limited

- Wipro Limited

Recent Developments

- August 2025 – VVDN Technologies acquired GGS Engineering Services, adding mechanical design, simulation, virtual manufacturing, and engineering analysis capabilities across automotive, aerospace, and medical technology sectors.

- September 2025 – Wipro agreed to acquire Harman’s Digital Transformation Solutions business for USD 375 million, significantly expanding its Engineering R&D, device engineering, and digital engineering capabilities.

- March 2025 – Quest Global acquired Alpha-Numero Technology Solutions, a semiconductor and FPGA engineering specialist, strengthening mission-critical engineering, aerospace, and semiconductor design services.

- May 2026 – Cyient acquired Tao Digital Solutions for approximately USD 218 million, enhancing its AI-native data engineering, digital engineering, and lifecycle engineering service portfolio.

- May 2026 – L&T Technology Services opened an Engineering Intelligence Centre of Excellence in Munich, Germany, focused on AI-led product engineering and software-defined mobility solutions for global ESO customers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 29.2 Billion |

| Forecast Revenue (2035) | USD 91.9 Billion |

| CAGR (2026-2035) | 12.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Services (Designing, Prototyping, System Integration, Testing, Others), By Location (Offshore, Onshore), By Application (Automotive, Aerospace, Manufacturing, Consumer Electronics, Semiconductors, Healthcare, Telecom, Energy & Utilities, Construction & Infrastructure, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AKKA Technologies, Alten Group, Capgemini Engineering, Entelect, HCL Technologies Limited, Emerson Electric Co, Infosys Limited, Tata Elxsi, Tata Consultancy Services Limited, Tech Mahindra Limited, Wipro Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |