Quick Navigation

Report Overview

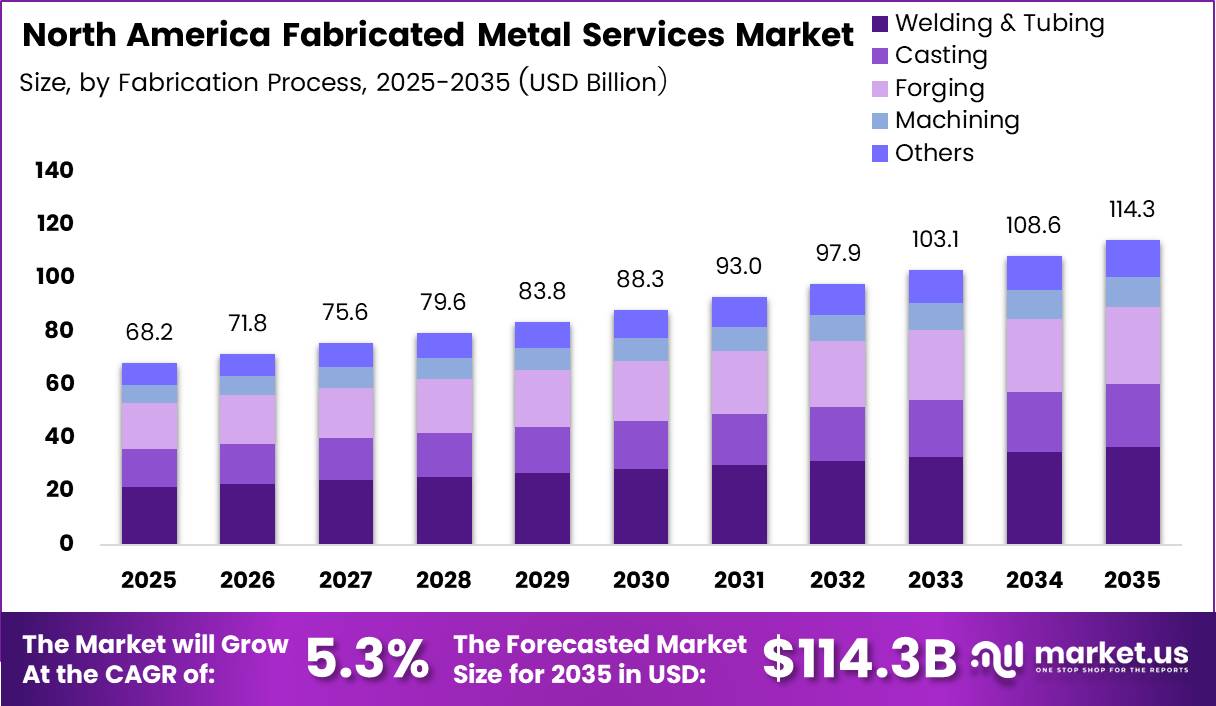

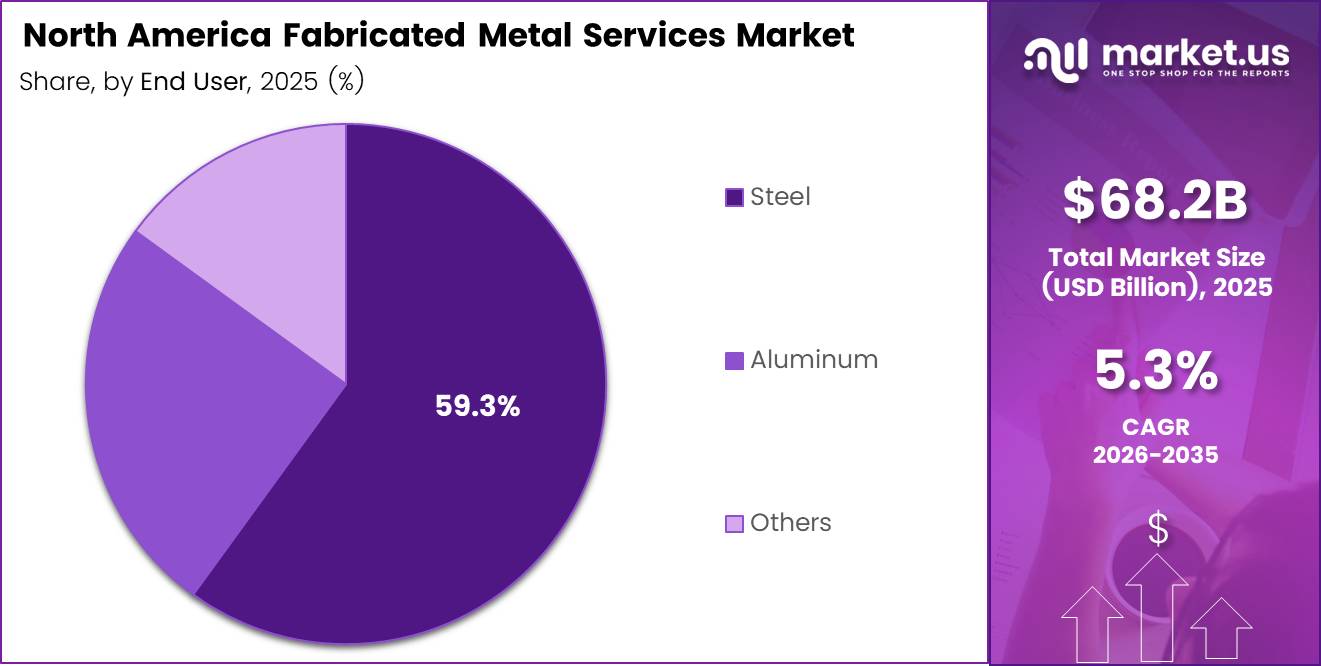

North America Fabricated Metal Services Market size is expected to be worth around USD 114.3 Billion by 2035 from USD 68.2 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The fabricated metal services market covers contract manufacturing operations that cut, bend, weld, cast, forge, and machine raw metal stock into finished components and assemblies. These services supply parts to manufacturing plants, power utilities, construction contractors, oil and gas operators, automotive assemblers, and aerospace producers. The market sits at the intersection of industrial supply chains and advanced manufacturing capacity.

North America’s fabricated metal sector operates through a dense network of independent job shops, regional contract manufacturers, and vertically integrated OEM suppliers. Steel accounts for the largest share of material inputs. Welding and tubing operations lead all fabrication processes. End-user diversity insulates the market against single-sector downturns and spreads revenue risk across industrial cycles.

Federal infrastructure spending programs have directed capital toward bridge rehabilitation, pipeline upgrades, power grid expansion, and industrial facility construction across the United States and Canada. Each of these programs requires precision fabricated metal components at scale. This government-driven pipeline creates predictable demand for fabricators with certified welding and structural steel capabilities.

Renewable energy project development has added a structural fabrication layer to utility-scale solar, wind, and transmission projects. Mounting frames, tower sections, substation enclosures, and cable management systems all require custom metal fabrication. This energy transition spending creates multi-year order visibility for fabricators serving the power and utilities end-user segment.

According to the U.S. Bureau of Labor Statistics, the fabricated metal product manufacturing industry contained 61,435 private establishments in Q4 2025. This density signals a fragmented supply base with high geographic coverage. Buyers can source locally, but consolidation among larger players is creating tiered competitive pressure on smaller job shops.

Data from the U.S. Bureau of Labor Statistics shows the number of fabricated metal manufacturing establishments increased from 61,158 in Q2 2025 to 61,435 in Q4 2025, adding 277 establishments in six months. This net growth confirms active market entry and reflects strong order backlogs that justify new shop formation. Investors tracking capacity expansion should monitor establishment counts as a leading indicator of sector health.

Key Takeaways

- The North America Fabricated Metal Services Market was valued at USD 68.2 Billion in 2025.

- The market is forecast to reach USD 114.3 Billion by 2035.

- The market grows at a CAGR of 5.3% during the forecast period 2026 to 2035.

- Steel dominates the Material Type segment with a 59.3% share.

- Welding & Tubing leads the Fabrication Process segment with a 31.2% share.

- Manufacturing is the largest end-user segment with a 23.4% share.

- North America is the primary regional market covered by this report.

- The industry contained 61,435 private establishments as of Q4 2025.

Material Type Analysis

Steel dominates with 59.3% due to structural strength and broad industrial applicability.

In 2025, Steel held a dominant market position in the By Material Type segment of the North America Fabricated Metal Services Market, with a 59.3% share. Steel’s structural performance, weldability, and cost efficiency make it the default material across construction, manufacturing, and energy infrastructure projects. Fabricators with certified steel processing capabilities command premium contracts from OEM buyers and government project managers seeking proven material traceability.

Aluminum serves fabrication applications where weight reduction and corrosion resistance outweigh the cost premium over steel. Aerospace, transportation, and enclosure fabrication buyers drive aluminum demand. Fabricators investing in aluminum-specific tooling and forming equipment position themselves to capture higher-margin contracts as lightweighting requirements tighten across transportation and logistics applications.

Other materials including copper alloys, titanium, and specialty steels serve niche fabrication needs in defense, power generation, and precision machining applications. These materials command higher per-unit margins but require dedicated equipment and workforce certification. Fabricators targeting this tier must demonstrate process qualification to access aerospace and defense supply chains.

Fabrication Process Analysis

Welding & Tubing dominates with 31.2% due to universal demand across all end-use industries.

In 2025, Welding & Tubing held a dominant market position in the By Fabrication Process segment of the North America Fabricated Metal Services Market, with a 31.2% share. Welded assemblies and tubing systems form the structural backbone of industrial equipment, piping networks, and vehicle frames. Fabricators with robotic welding capacity and certified welding procedures hold a competitive advantage in securing high-volume OEM supply contracts.

Casting produces near-net-shape metal parts for applications requiring complex internal geometries, such as pump housings, engine blocks, and valve bodies. Casting operations require significant capital investment in foundry equipment and process control systems. Buyers in oil and gas, power, and heavy equipment manufacturing rely on casting suppliers for components with strict dimensional and metallurgical tolerances.

Forging produces high-strength metal components by applying compressive force to heated metal stock. Automotive powertrain components, aerospace structural members, and construction equipment parts rely on forged metal for fatigue resistance. Forging suppliers serving aerospace and defense customers face stringent quality certification requirements that create strong entry barriers and stable long-term supply relationships.

Machining removes material from metal workpieces to achieve tight dimensional tolerances and surface finishes. Precision machining supports aerospace, medical device, and semiconductor equipment manufacturing. Fabricators combining machining with welding and forming operations deliver integrated assemblies that reduce buyer supply chain complexity and support outsourcing decisions by OEM procurement teams.

Other fabrication processes include laser cutting, waterjet cutting, stamping, and roll forming. These processes serve high-volume, thin-gauge metal part production for appliance, HVAC, and electronics enclosure applications. Stamping and laser cutting operations benefit from automation investments that reduce labor cost per part and improve throughput consistency across high-mix production schedules.

End-User Analysis

Manufacturing dominates with 23.4% due to continuous demand for custom metal subassemblies.

In 2025, Manufacturing held a dominant market position in the By End-user segment of the North America Fabricated Metal Services Market, with a 23.4% share. Industrial equipment makers, material handling system builders, and general machinery producers rely on contract fabricators for structural frames, machined components, and welded subassemblies. Outsourcing these operations lets OEM manufacturers focus capital on assembly and final testing rather than raw material processing.

Power & Utilities buyers require fabricated metal for transmission towers, substation enclosures, turbine support structures, and pipeline systems. Renewable energy project build-outs have extended this segment’s order horizon beyond traditional fossil fuel infrastructure. Fabricators with structural steel certification and experience in utility-grade weld procedures are best positioned to capture this segment’s project-based procurement cycles.

Construction & Infrastructure buyers source structural steel assemblies, rebar cages, curtain wall frames, and modular building components from metal fabricators. Federal infrastructure programs have expanded the construction pipeline across highways, bridges, water treatment facilities, and public transit. Fabricators with prefabrication and modular construction capabilities reduce on-site labor costs and accelerate project timelines for construction buyers.

Oil & Gas operators require fabricated metal for wellhead equipment, pressure vessels, heat exchangers, and pipeline fittings. Midstream infrastructure expansion and LNG export terminal construction support long-cycle fabrication contracts. Fabricators serving this segment must maintain ASME and API process certifications that create compliance-based barriers to entry and protect margin stability for qualified suppliers.

Other end-user segments include agriculture equipment, HVAC systems, marine, and consumer appliance manufacturing. These buyers typically source higher volumes of simpler formed and stamped components. Fabricators serving multiple end-user categories across this group benefit from demand diversification that buffers revenue during downturns in any single vertical.

Key Market Segments

By Material Type

- Steel

- Aluminum

- Others

By Fabrication Process

- Welding & Tubing

- Casting

- Forging

- Machining

- Others

By End-user

- Manufacturing

- Power & Utilities

- Construction & Infrastructure

- Oil & Gas

- Automotive

- Aerospace & Defense

- Others

Market Dynamics

Drivers – Infrastructure Investment and Expanding Industrial Backlogs Fuel Fabrication Services Demand

Federal and state infrastructure modernization programs are directing capital toward bridge rehabilitation, highway expansion, water system upgrades, and energy grid reinforcement. Each project demands precision fabricated metal components such as structural beams, connection plates, and custom assemblies. Fabricators with certified structural steel capacity and fast turnaround capabilities are winning larger share of this public-sector procurement pipeline.

According to PMA’s July 2025 Business Conditions Report, 36% of North American metalforming manufacturers expected incoming orders to increase over the next three months. This level of forward confidence signals that infrastructure and industrial project awards are translating into real fabrication backlogs. Investors and fabricators expanding capacity ahead of this cycle will capture more contract value than those who wait for orders to arrive before investing.

As reported by PMA’s July 2025 Business Conditions Report, 36% of surveyed companies were actively expanding their workforce in July 2025. Labor expansion at this rate reflects production ramp-ups tied to confirmed orders rather than speculative hiring. Fabricators building skilled trades pipelines through apprenticeship and certified welder programs gain a structural advantage over competitors constrained by workforce bottlenecks.

Restraints – Skilled Labor Shortages and Raw Material Price Volatility Constrain Growth

The fabricated metal services sector faces a persistent shortage of certified welders, machinists, and metalforming technicians across the United States and Canada. Trade school enrollment has not kept pace with workforce retirements among experienced fabrication personnel. This skills gap limits throughput capacity at existing facilities and delays new facility ramp-up timelines for fabricators holding confirmed order backlogs.

PMA’s July 2025 Business Conditions Report found that 46% of surveyed metalforming companies expected incoming orders to remain unchanged over the following three months. This flat-order outlook among nearly half the sector signals that workforce and capacity constraints are capping output growth. Fabricators unable to staff up cannot convert inquiry activity into revenue, which erodes market share toward better-staffed competitors.

Data from PMA’s July 2025 Business Conditions Report shows 18% of respondents expected incoming orders to decrease over the next three months. This contraction signal, even among a minority of firms, reflects the margin pressure created by volatile steel and aluminum prices. When input costs spike unpredictably, fixed-price contracts turn loss-making and buyers delay non-critical fabrication awards, compressing fabricator revenue across the sector.

Growth Factors – Manufacturing Outsourcing and Data Center Expansion Create New Revenue Opportunities

OEM manufacturers building smart factory ecosystems are outsourcing structural frame fabrication, enclosure assembly, and precision machined components to specialized contract fabricators. This outsourcing shift lets OEMs reduce fixed asset investment while accessing fabrication precision they cannot replicate in-house. Contract fabricators who invest in quality management systems and design engineering support win preferred supplier status in these long-cycle outsourcing relationships.

Figures from PMA’s July 2025 Business Conditions Report show 23% of metalforming companies reported increased shipping levels in July 2025 compared with the previous month. Rising shipment activity confirms that fabrication output is moving into active end-use projects rather than accumulating as inventory. This throughput signal validates investment in capacity expansion by fabricators already serving data center, logistics, and industrial automation buyers.

In December 2025, Manufacturing Corporation of America launched MetalPeak Fabrication, a joint venture creating one of the largest metal fabrication operations in the eastern United States. This scale-up demonstrates that the outsourcing opportunity is large enough to justify major capital commitments. Fabricators who build regional density through joint ventures or acquisitions before this outsourcing wave peaks will establish cost and delivery advantages that organic-growth competitors cannot match quickly.

Emerging Trends – AI-Powered Design and Automation Technologies Enhance Fabrication Efficiency

AI-driven design optimization tools are reducing engineering iteration cycles by generating and validating fabrication geometries faster than manual CAD workflows allow. Fabricators deploying these tools cut pre-production engineering time and reduce material waste from first-article failures. Early adopters gain bid-to-delivery speed advantages that allow them to compete for shorter-lead-time contracts that manual-process shops cannot fulfill profitably.

Based on PMA’s July 2025 Business Conditions Report data, 50% of metalforming companies reported no change in shipping levels in July 2025. This stability among the majority of firms shows that baseline production is holding while a subset captures accelerating demand. Fabricators adopting robotic welding and automated material handling are the subset driving output gains, while manual-process shops hold steady without volume upside.

Figures from PMA’s July 2025 Business Conditions Report show 18% of manufacturers reported increased customer lead times in July 2025. Extended lead times signal that demand is outpacing available production capacity at certain fabrication shops. Fabricators who deploy digital twin workflow management to identify and resolve bottlenecks before they extend lead times retain key accounts that would otherwise shift orders to faster competitors.

Key Company Insights

O’Neal Manufacturing Services operates ten ISO-certified facilities across North America, giving it multi-regional delivery reach that single-site competitors cannot match. This geographic distribution reduces buyer supply chain risk and supports just-in-time delivery contracts. Fabricators without this multi-site infrastructure face a structural disadvantage when competing for national OEM supply agreements requiring consistent lead times across regions.

Mayville Engineering Company strengthened its fabrication portfolio in May 2025 by announcing a definitive agreement to acquire Accu-Fab for approximately $140.5 million, adding sheet metal fabrication, engineering integration, and specialized finishing capabilities. This acquisition expanded MEC’s OEM service coverage and added engineering value that justifies premium contract pricing. Fabricators who bundle engineering services with production capacity are harder to displace than those offering only manufacturing throughput.

Valmont Industries operates at the intersection of infrastructure and industrial fabrication, producing utility poles, transmission structures, and agricultural equipment components. This end-user diversification insulates Valmont from single-sector procurement cycles. However, public infrastructure project timelines are subject to government budget allocation delays, which can compress quarterly revenue against fixed overhead costs at large fabrication facilities.

BTD Manufacturing focuses on metal stamping, fabrication, and assembly for agricultural, construction, and industrial OEM customers. Its strength in high-volume, close-tolerance stamped components serves buyers who require consistent part quality across large production runs. However, its concentration in stamping-dependent processes limits its ability to compete for complex welded assembly contracts where multi-process fabrication capability is a buyer qualification requirement.

Key Players

- O’Neal Manufacturing Services

- Mayville Engineering Company

- Valmont Industries

- BTD Manufacturing

- Kapco Metal Stamping

- Ironform Corporation

- Matcor-Matsu Group

- Ryerson Holding Corporation

- United Steel Inc.

- PMF Industries

- Monti Inc.

- Prince Manufacturing

Recent Developments

- July 2025 – Mayville Engineering Company (MEC) completed the acquisition of Accu-Fab, adding advanced metal fabrication, engineering, and finishing capabilities serving OEM customers across North America.

- August 2025 – FalconPoint Partners committed $500 million to acquire and expand SMS, a steel mill services and scrap-processing company, supporting growth investments across the North American metals and steel services sector.

- October 2025 – MASABA officially opened its new 147,500-square-foot steel and metal fabrication facility in Vermillion, South Dakota, significantly expanding fabrication capacity and steel processing operations.

- October 2025 – MASABA announced an investment of more than $15 million in advanced steel fabrication equipment at its new fabrication center, supporting automated and centralized steel processing operations.

- December 2025 – Manufacturing Corporation of America (MCA) launched MetalPeak Fabrication, a joint venture between MetalOne Fabrication and EHC Industries, creating one of the largest metal fabrication operations in the eastern United States.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 68.2 Billion |

| Forecast Revenue (2035) | USD 114.3 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Steel, Aluminum, Others); By Fabrication Process (Welding & Tubing, Casting, Forging, Machining, Others); By End-user (Manufacturing, Power & Utilities, Construction & Infrastructure, Oil & Gas, Automotive, Aerospace & Defense, Others) |

| Competitive Landscape | O’Neal Manufacturing Services, Mayville Engineering Company, Valmont Industries, BTD Manufacturing, Kapco Metal Stamping, Ironform Corporation, Matcor-Matsu Group, Ryerson Holding Corporation, United Steel Inc., PMF Industries, Monti Inc., Prince Manufacturing |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |