Quick Navigation

Report Overview

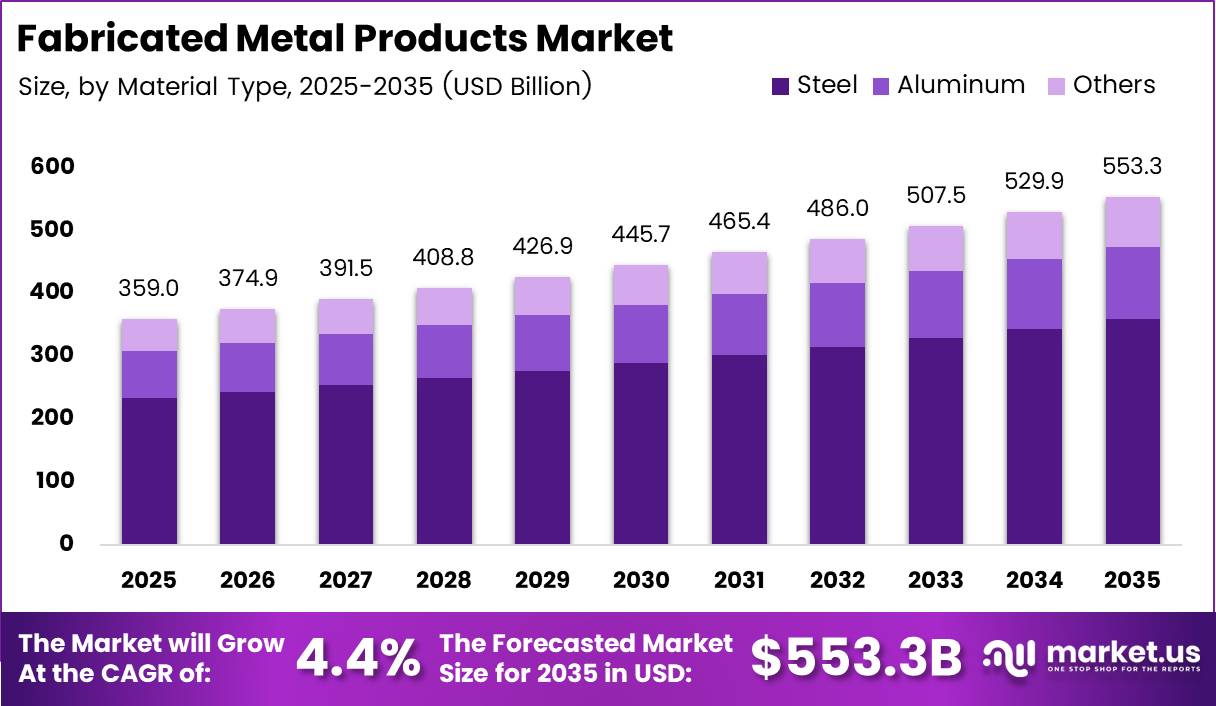

Global Fabricated Metal Products Market size is expected to be worth around USD 553.3 Billion by 2035 from USD 359.0 Billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

Fabricated metal products cover a broad range of manufactured goods produced by cutting, bending, forming, welding, and assembling raw metal stock into finished or semi-finished components. These products serve as critical inputs across construction, automotive, aerospace, power generation, and oil and gas sectors. The market spans both standard commodity outputs and high-precision engineered parts.

Infrastructure investment continues to anchor demand across every major economy. Governments in Asia, the Middle East, and North America are committing multi-year capital budgets to roads, bridges, energy grids, and industrial facilities. Each of these projects requires structural steel components, precision-machined parts, and custom fabricated assemblies. This consistent public-sector spending underpins baseline volume growth for fabricators across all process types.

The energy transition is creating a new and durable demand pool for fabricated metal producers. Solar mounting structures, wind turbine towers, transmission infrastructure, and battery storage enclosures all require metal fabrication at scale. Fabricators capable of producing structural and precision components for clean energy projects are accessing a faster-growing revenue stream than traditional heavy industry alone could provide.

Automation is restructuring the cost base across the fabrication industry. Laser cutting systems now achieve tolerances of ±0.01 mm at speeds up to 150 m/min, eliminating secondary finishing steps and reducing per-unit labor content. Fabricators investing in automated cell manufacturing are building structural cost advantages over competitors still relying on manual workflows. This performance gap will widen as technology adoption accelerates through 2026 and beyond.

Sustainability is shifting from a compliance issue to a commercial requirement. According to thechargestations.com, approximately 90% of metal products can be recycled, a figure fabricators are actively using to market circular economy credentials to procurement teams at major OEMs and construction firms. This recyclability advantage is becoming a differentiator in supplier selection, particularly in Europe and North America where sustainability mandates are embedded in procurement policy.

According to the World Economic Forum data cited in industry sources, approximately 70% of manufacturers are expected to adopt sustainable practices by 2026, including recycled metals, green technologies, and energy-efficient fabrication equipment. This signals a structural reorientation of the supply chain rather than a temporary trend. Fabricators that build green credentials now will hold preferred-supplier status as OEM customers face their own Scope 3 emissions reporting obligations.

Key Takeaways

- The Global Fabricated Metal Products Market was valued at USD 359.0 Billion in 2025.

- The market is forecast to reach USD 553.3 Billion by 2035, at a CAGR of 4.4%.

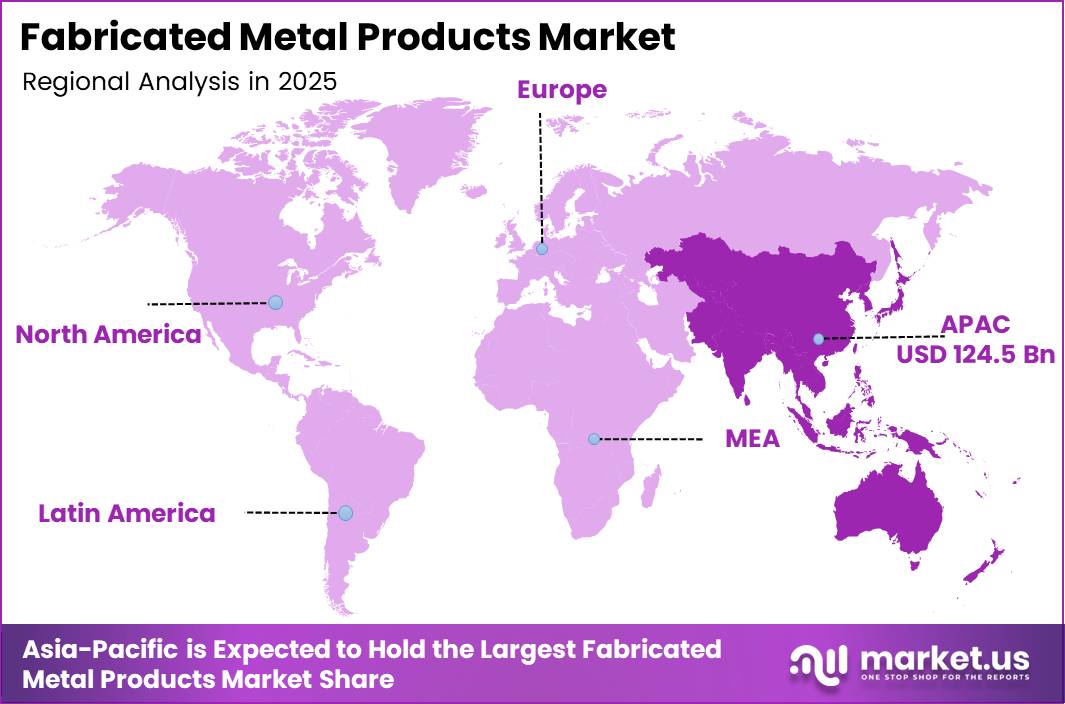

- Asia-Pacific leads all regions with a 34.70% market share, valued at USD 124.5 Billion.

- Steel dominates the By Material Type segment with a 64.9% share in 2025.

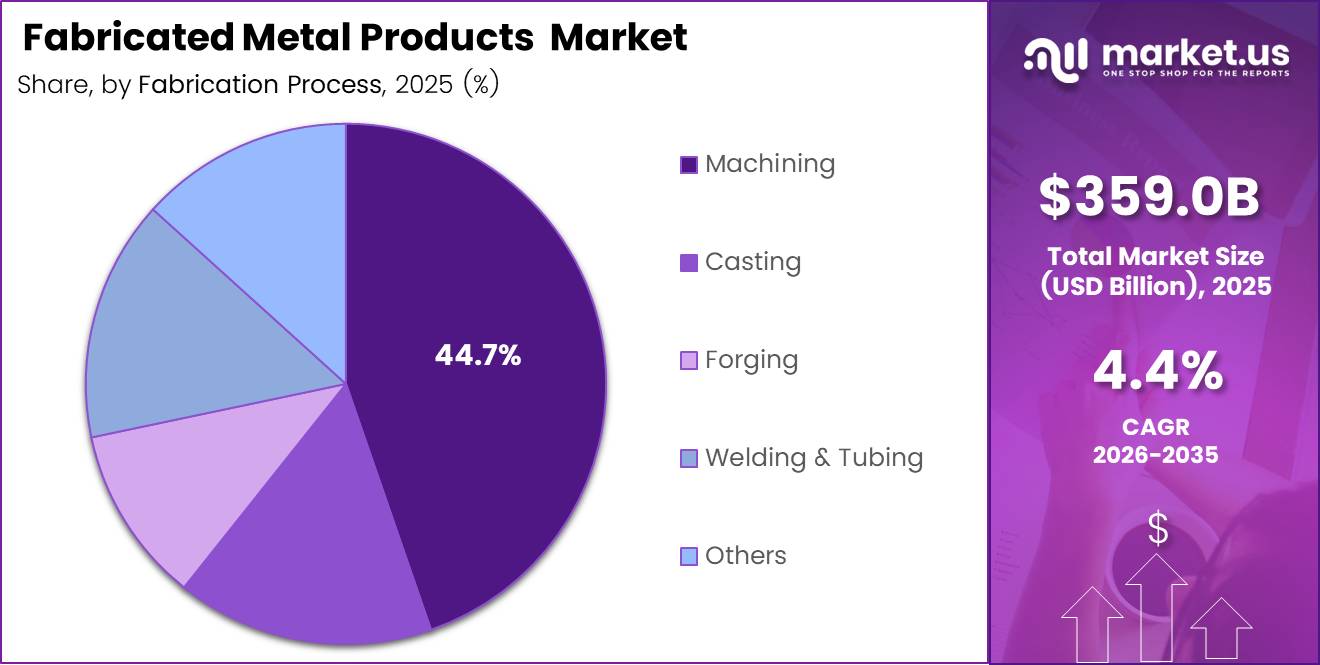

- Machining leads the By Fabrication Process segment with a 44.7% share in 2025.

- Construction & Infrastructure is the top end user segment, holding a 31.6% share in 2025.

- Automation and IoT adoption among fabricators is projected to reach 75% by 2026.

- Modular fabrication techniques can reduce assembly time by up to 80% compared to conventional methods.

Material Type Analysis

Steel dominates with 64.9% due to structural strength and cost availability.

In 2025, Steel held a dominant market position in the By Material Type segment of the Fabricated Metal Products Market, with a 64.9% share. Steel’s combination of tensile strength, weldability, and established supply chains makes it the default choice across construction, industrial equipment, and transportation applications. No other material matches its cost-per-unit performance at scale.

Aluminum serves fabricators targeting weight-sensitive applications in transportation, aerospace, and consumer electronics enclosures. Aluminum commands a price premium over steel, but its corrosion resistance and formability justify the cost differential in automotive body panels and aerospace structural components. Demand from electric vehicle manufacturers is creating a sustained pull for high-purity aluminum fabricated parts.

Others in the material segment include specialty alloys such as titanium, copper alloys, and nickel-based metals used in high-performance or corrosion-critical environments. These materials serve niche but high-margin applications in defense, medical devices, and chemical processing equipment. Volume is lower, but unit values and technical barriers to entry are significantly higher than commodity steel or aluminum.

Fabrication Process Analysis

Machining dominates with 44.7% due to precision tolerance requirements across industrial sectors.

In 2025, Machining held a dominant market position in the By Fabrication Process segment of the Fabricated Metal Products Market, with a 44.7% share. Machining delivers the dimensional accuracy required in aerospace, automotive, and medical device components. According to Vidir Solutions, a sheet metal storage upgrade in a fabrication facility saved over 34 labor hours per day and generated annualized savings of USD 228,000 per year, illustrating how operational efficiency improvements in machining environments directly translate into measurable bottom-line gains.

Casting enables fabricators to produce complex net-shape components in high volumes at lower per-unit tooling costs. It remains the preferred process for engine blocks, pump housings, and valve bodies where internal geometry complexity would be prohibitively expensive to machine from solid stock. Foundry operators supplying the oil and gas and power sectors maintain stable order books from long-term equipment supply contracts.

Forging produces components with superior grain structure and fatigue resistance compared to casting or machined billet. The process is dominant in safety-critical applications including aircraft landing gear, crankshafts, and heavy equipment drive components. In September 2024, Beacon acquired Chicago Metal Supply & Fabrication, enhancing its custom architectural sheet metal fabrication capabilities and signaling consolidation within the structural metal forming segment.

Welding & Tubing underpins structural and pressure-containing fabricated assemblies across construction, pipeline, and industrial plant applications. Welded tube and pipe fabrication supports energy infrastructure, HVAC systems, and fluid handling equipment. Automated welding cells are reducing labor content per joint while improving weld quality consistency, compressing the cost gap between high-wage and low-wage production markets.

Others in fabrication processes include stamping, roll forming, hydroforming, and press brake operations. These processes are central to high-volume automotive body panel production and white goods manufacturing. Sheet metal stamping remains one of the highest-throughput fabrication methods available, making it indispensable for consumer durables and appliance manufacturers operating at mass-production scale.

End User Analysis

Construction & Infrastructure dominates with 31.6% due to sustained global capital project pipelines.

In 2025, Construction & Infrastructure held a dominant market position in the By End User segment of the Fabricated Metal Products Market, with a 31.6% share. Government-backed infrastructure programs across Asia, North America, and the Middle East are generating multi-year demand for structural steel sections, fabricated connectors, and precision anchor systems. This end user segment provides fabricators with long-duration contracts and predictable order volumes.

Manufacturing buyers consume fabricated components as inputs to machinery, equipment, and industrial assemblies. This segment purchases across the full range of fabrication processes, from precision machining to heavy structural welding. Manufacturing sector growth in emerging economies is expanding the addressable market for regional fabricators supplying domestic equipment producers.

Power & Utilities buyers drive demand for pressure vessels, heat exchangers, structural supports, and electrical enclosures fabricated to strict dimensional and material certification standards. The ongoing buildout of renewable energy capacity is expanding this segment’s share of total fabricated metal consumption beyond traditional thermal and nuclear power plant requirements.

Oil & Gas fabrication requirements center on pressure-rated pipe systems, subsea structures, processing equipment, and wellhead components. This sector demands the highest material certification standards and traceability requirements of any end user group. Capital expenditure cycles in oil and gas create pronounced order peaks and troughs that fabricators serving this segment must manage through portfolio diversification.

Automotive buyers consume fabricated stampings, structural subassemblies, chassis components, and powertrain parts across passenger and commercial vehicle platforms. The shift toward battery electric vehicles is altering the mix of required components. Battery enclosures, thermal management structures, and motor housings are displacing some traditional internal combustion engine fabrications while creating new precision metal product categories.

Aerospace & Defense end users specify the tightest tolerances, the strictest material certifications, and the most demanding documentation requirements of any fabricated metals customer segment. Unit volumes are lower than automotive, but margins are substantially higher. Fabricators holding aerospace approvals such as AS9100 and Nadcap certifications operate in a structurally protected market with high barriers to new supplier qualification.

Others across end user categories include medical devices, marine, rail, and consumer electronics. These applications often require specialized alloys or surface treatment specifications. They represent smaller volume pools individually, but collectively provide fabricators with margin diversification opportunities outside the cyclicality of heavy industry and construction.

Key Market Segments

By Material Type

- Steel

- Aluminum

- Others

By Fabrication Process

- Machining

- Casting

- Forging

- Welding & Tubing

- Others

By End User

- Construction & Infrastructure

- Manufacturing

- Power & Utilities

- Oil & Gas

- Automotive

- Aerospace & Defense

- Others

Drivers

Infrastructure Spending and Industrial Manufacturing Demand Sustain Fabricated Metal Volume Growth

Global construction programs and industrial capital expenditure are generating sustained order flow for fabricated metal producers. Governments in Asia-Pacific, the Middle East, and North America are funding roads, bridges, energy grids, and manufacturing facilities that require structural steel sections, precision components, and custom assemblies. This public-sector demand provides fabricators with long-duration contract visibility unavailable in most other industrial supply chains.

Renewable energy project expansion is adding a structural layer of demand on top of traditional construction activity. Wind towers, solar mounting frames, and transmission infrastructure each require fabricated steel and aluminum at scale. Fabricators positioned in the clean energy supply chain are capturing a faster-growing revenue stream than legacy heavy industry alone delivers. In July 2025, Mayville Engineering Company completed the acquisition of Accu-Fab, a technology-driven sheet metal fabrication and finishing provider serving OEM customers, reflecting how leading fabricators are investing to capture this expanding demand pool.

According to thechargestations.com, automation and IoT adoption among fabricators is projected to reach 75% by 2026. This adoption rate signals that the industry is entering a phase where automated production becomes the baseline, not a competitive differentiator. Fabricators still operating predominantly manual workflows face a compounding cost disadvantage as peers lock in efficiency gains through robotic welding, automated cutting cells, and connected production monitoring systems.

Restraints

Raw Material Price Volatility and Skilled Labor Shortages Constrain Fabricator Margin Stability

Steel and aluminum price fluctuations create direct margin exposure for fabricators operating on fixed-price contracts. When input costs rise faster than contract escalation clauses allow, fabricators absorb the difference. This risk is most acute for smaller job shops without the purchasing scale to hedge commodity exposure or maintain strategic material inventory buffers. Margin protection requires either pricing power or volume scale, and most regional fabricators lack both.

Skilled labor shortages in welding, machining, and precision forming are limiting production capacity expansion across North American and European fabrication markets. Training cycles for certified welders and CNC machinists span multiple years, and the workforce pipeline is not keeping pace with retirement attrition. According to a peer-reviewed study published by ASTRJ, springback error rates in stainless steel sheet bending exceed 4% for 416-grade material. This dimensional error rate reflects the technical precision required from operators, and the cost of scrap and rework when that precision is not achieved.

The combination of volatile input costs and constrained skilled labor creates a structural margin squeeze for fabricators without automation investments already in place. Passing cost increases to customers requires contractual leverage that many tier-two and tier-three fabricators do not hold. For investors evaluating this market, margin sustainability is the central risk variable, not top-line growth. Fabricators with long-term supply agreements and automated production cells carry structurally lower exposure to both pressures.

Growth Factors

Advanced Fabrication Technology and Emerging Economy Industrialization Create New Revenue Streams

Laser cutting systems now achieve dimensional tolerances of ±0.01 mm at cutting speeds up to 150 m/min, often eliminating secondary finishing operations entirely. This performance level converts precision machining jobs into laser-cut parts, reducing cycle time and labor content simultaneously. Fabricators investing in fiber laser capacity are compressing per-part costs while expanding their addressable job scope into tighter-tolerance applications.

According to machitech.com, advanced modular fabrication techniques in 2026 can reduce assembly time by up to 80% through precision pre-cutting and fitting of components. This efficiency gain is not incremental. An 80% reduction in assembly time fundamentally changes the project economics of large structural fabrications, enabling faster site delivery, lower labor cost per structure, and higher throughput from the same facility footprint. Fabricators adopting modular methods for construction and industrial plant projects are rewriting the competitive cost model for structural metalwork.

Industrialization in emerging economies across Southeast Asia, Sub-Saharan Africa, and Latin America is creating new domestic demand for fabricated metal products that previously required importation. Local fabrication capacity is being established to serve construction, energy, and manufacturing sectors in these markets. In December 2024, Armstrong World Industries acquired A. Zahner Company, expanding its engineered and fabricated architectural metal solutions portfolio. This move reflects how established players are positioning to serve premium fabricated metal applications in high-growth construction markets.

Emerging Trends

Industry 4.0 Integration and Additive Manufacturing Are Redefining Fabrication Facility Operations

Smart factory adoption is changing how fabrication facilities manage quality, throughput, and maintenance. Digital twin systems create virtual replicas of fabrication cells, enabling engineers to simulate process changes before committing physical tooling or production time. Predictive maintenance applications analyze sensor data from CNC machines and welding systems to forecast component failures before they cause unplanned downtime. Facilities using these systems are reporting measurable reductions in unplanned stoppages.

According to thechargestations.com, additive manufacturing adoption in the fabricated metals sector is projected to reach 60% by 2026. This rate reflects a meaningful shift in how fabricators approach low-volume, high-complexity components. Metal 3D printing eliminates the tooling cost barrier for short-run precision parts, enabling fabricators to profitably serve prototype and specialty production runs that were previously uneconomical. Early adopters are using additive capability to move upmarket into aerospace and medical device supply chains.

Turnkey multi-machine automation in heavy fabrication aims to lift asset utilization from the current 50-65% range to 75-85%, tracking throughput by hours per week, touchpoints per part, rework rate, and overtime against established baselines. According to mac-tech.com, facilities achieving this utilization improvement generate a fundamentally different return on capital from the same installed equipment. For fabricators evaluating automation investment, this utilization uplift represents the clearest path to justifying capital expenditure without requiring top-line volume growth.

Regional Analysis

Asia-Pacific Dominates the Fabricated Metal Products Market with a Market Share of 34.70%, Valued at USD 124.5 Billion

Asia-Pacific commands the largest regional share of the Fabricated Metal Products Market at 34.70%, equivalent to USD 124.5 Billion in 2025. China’s manufacturing base, India’s infrastructure buildout, and Japan’s precision engineering sector collectively drive this dominance. Government capital programs across ASEAN economies continue to expand construction and industrial plant activity, sustaining regional fabrication order volumes through the forecast period.

North America holds a structurally strong position in fabricated metals on the basis of defense procurement, aerospace supply chain depth, and energy sector capital expenditure. The US market benefits from domestic reshoring of manufacturing capacity, with fabricators receiving increased order flow from OEMs reducing Asia-Pacific supply chain exposure. Infrastructure legislation is channeling federal investment into bridge, road, and utilities projects that require domestic fabricated steel content.

Europe’s fabricated metals market is shaped by automotive sector demand, precision engineering output from Germany and northern Italy, and a strong aerospace supply chain concentrated in France and the UK. Sustainability regulations are accelerating adoption of recycled input materials and energy-efficient fabrication equipment. European fabricators face cost pressure from energy prices but maintain a technology and quality premium in high-specification product categories.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Emerson Electric Co operates in fabricated metals through its automation and process control equipment divisions, where precision-fabricated enclosures, valves, and fluid control components are core outputs. Its strategic advantage lies in combining fabrication capability with embedded instrumentation and control technology. This integration allows Emerson to capture higher margin per assembly than commodity fabricators supplying equivalent structural metal components without electronic content.

Norsk Hydro ASA holds a vertically integrated position in aluminum fabrication, controlling bauxite mining, alumina refining, primary smelting, and downstream fabrication within a single corporate structure. This integration insulates Norsk Hydro from spot aluminum price volatility better than pure-play fabricators purchasing metal at market prices. Its focus on low-carbon aluminum is also creating premium pricing access as OEM customers embed carbon intensity targets into supplier qualification criteria.

Parker Hannifin Corporation positions its fabricated metal products within a broader motion and control technology portfolio, supplying precision hydraulic fittings, tube assemblies, and structural metal components to aerospace, industrial, and mobile equipment markets. Parker’s competitive strength comes from deep customer engineering integration rather than price competition on commodity fabrications. Its proprietary connector and fitting standards create switching costs that protect installed base revenue across multi-year equipment service cycles.

Eaton Corporation plc applies fabricated metal components across its electrical, hydraulic, and vehicle segments, where enclosures, bus bars, and structural assemblies serve high-reliability applications. In October 2025, OmniMax International acquired Nu-Ray Metal Products, strengthening its metal panel fabrication and roofing accessories manufacturing in the western United States. This acquisition reflects the broader market dynamic where larger platforms are absorbing regional fabricators to build geographic coverage and production scale simultaneously.

Key Players

- Emerson Electric Co

- Norsk Hydro ASA

- Parker Hannifin Corporation

- Eaton Corporation plc

- Alcoa Corporation

- Rusal plc

- Novelis Inc

- Siemens AG

- ABB Ltd

- Arconic Inc

Recent Developments

- January 2024 – Maysteel Industries acquired Star Precision Manufacturing, a sheet metal fabrication and precision machining company, expanding its fabrication capabilities and geographic presence in North America.

- April 2024 – Reliance, Inc. acquired Mid-West Materials, a flat-rolled steel service center serving metal fabrication and industrial manufacturing markets, strengthening its fabricated metals supply network.

- May 2025 – Lloyds Engineering Works acquired a 76% stake in Metalfab Hightech, increasing its heavy fabrication capacity and equipment manufacturing capabilities for infrastructure and industrial projects.

- February 2026 – Tube Investments of India announced the acquisition of an 87% stake in Orange Koi Pvt. Ltd., entering the metal injection molding and advanced precision metal components segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 359.0 Billion |

| Forecast Revenue (2035) | USD 553.3 Billion |

| CAGR (2026-2035) | 4.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Steel, Aluminum, Others), By Fabrication Process (Machining, Casting, Forging, Welding & Tubing, Others), By End User (Construction & Infrastructure, Manufacturing, Power & Utilities, Oil & Gas, Automotive, Aerospace & Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Emerson Electric Co, Norsk Hydro ASA, Parker Hannifin Corporation, Eaton Corporation plc, Alcoa Corporation, Rusal plc, Novelis Inc, Siemens AG, ABB Ltd, Arconic Inc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |