Quick Navigation

Report Overview

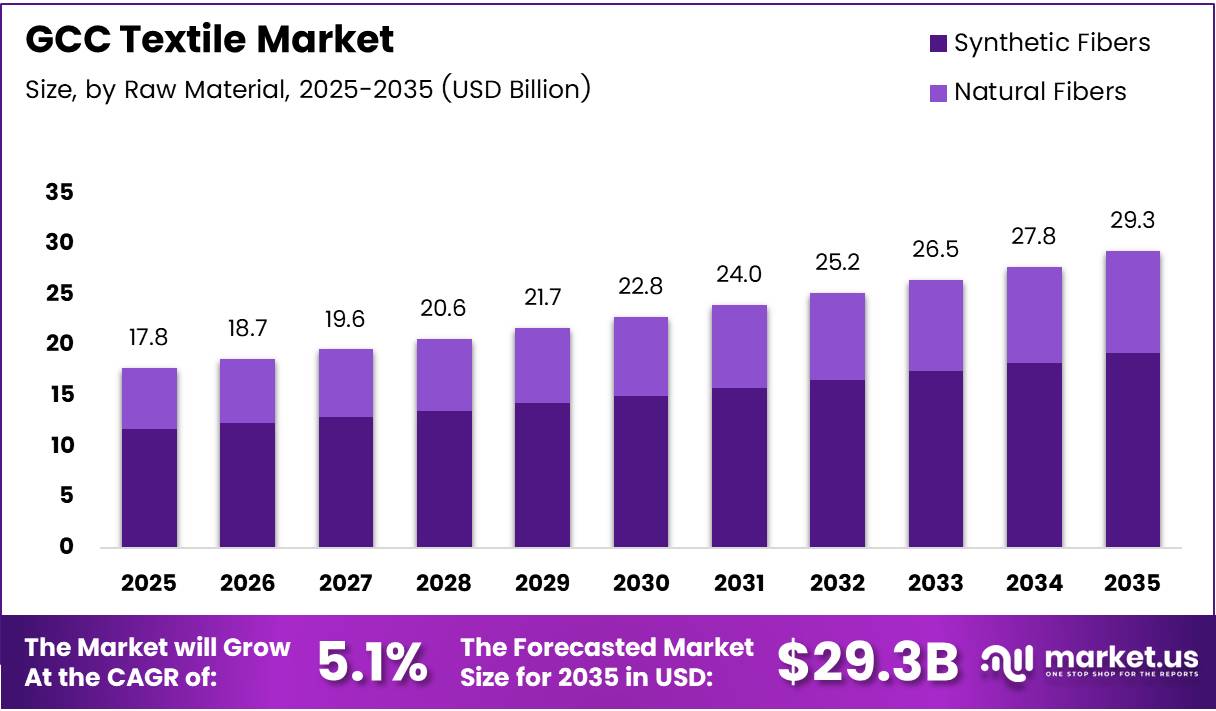

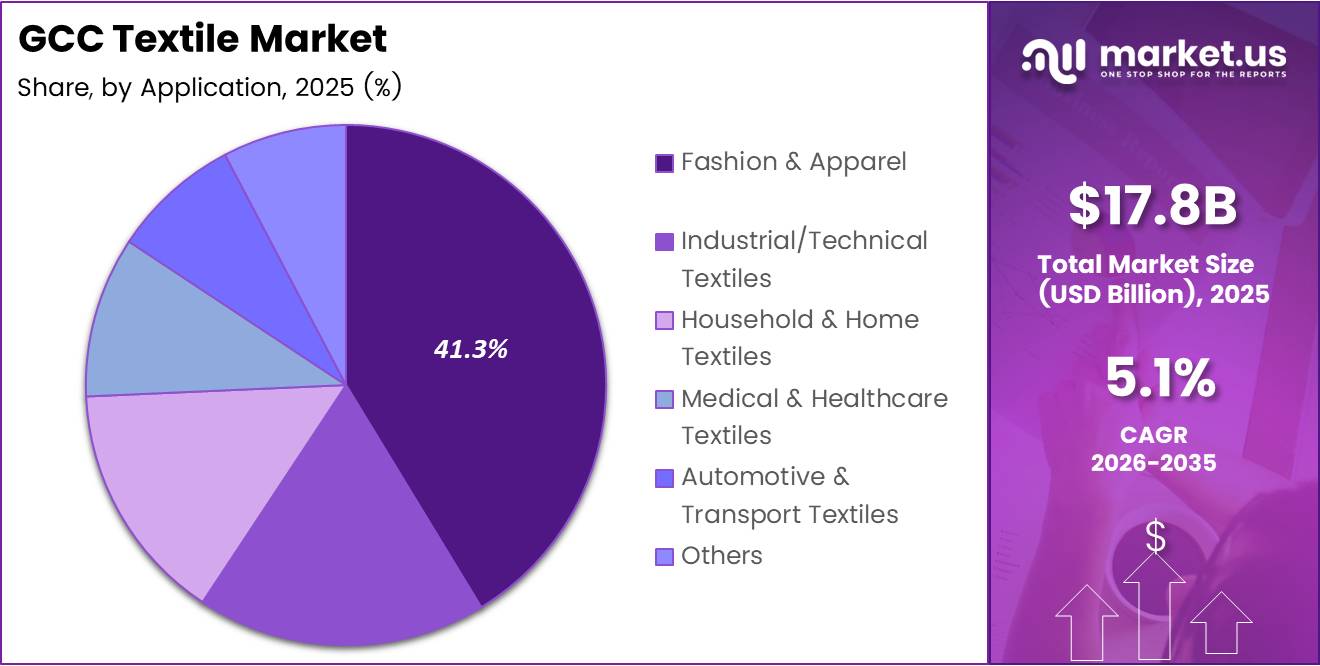

GCC Textile Market size is expected to be worth around USD 29.3 Billion by 2035 from USD 17.8 Billion in 2025, growing at a CAGR of 5.1% during the forecast period 2026 to 2035.

The GCC textile market covers the full production and trade ecosystem of fiber processing, fabric manufacturing, and finished textile goods across Saudi Arabia, the UAE, Qatar, Kuwait, Bahrain, and Oman. The market spans synthetic and natural fiber inputs, woven and nonwoven processes, and end-use categories from fashion apparel to industrial applications. This breadth makes it one of the most structurally diverse manufacturing sectors in the Gulf region.

Government-led economic diversification programs form the backbone of this market’s expansion trajectory. Saudi Vision 2030 and the UAE’s industrial development strategy both identify textile manufacturing as a priority sector for domestic value addition. Free-zone incentives across KIZAD, KAEC, and Jebel Ali attract foreign investors seeking cost-competitive access to GCC apparel buyers. This policy alignment directly accelerates capital deployment into local production capacity.

Synthetic fibers dominate the raw material base, holding a 65.8% share of GCC textile inputs. This reflects the region’s proximity to petrochemical infrastructure and its ability to produce polyester and nylon at competitive feedstock costs. Fashion and apparel applications lead end-use demand at 41.3%, signaling that the GCC consumer market itself drives significant domestic production requirements alongside export activity.

In December 2025, Welspun inaugurated a new terry towel manufacturing plant in Gujarat that became the world’s largest towel production facility, directly serving GCC home-textile importers. This investment signals that global suppliers are scaling up capacity specifically to service GCC procurement volumes — a structural confirmation that regional demand is attracting serious capital commitments from established manufacturers.

According to the Apparel Impact Institute and GEIDCO’s Low-Carbon Thermal Energy Roadmap, the textile and apparel sector contributes approximately 2% of global anthropogenic greenhouse-gas emissions. For GCC textile exporters targeting European and North American buyers, this figure is not abstract — it translates into compliance pressure, with sourcing brands applying scope-3 emission requirements that manufacturers must meet to retain contract eligibility.

According to the same roadmap, heat-pump-based heating systems deliver thermal energy at a lifetime cost below roughly 30–40 USD per MWh-thermal, compared to 60–80 USD per MWh-thermal for coal and gas boilers. For GCC plant operators, this cost differential reframes electrification not as an environmental obligation but as a margin improvement lever — particularly as carbon costs continue to be internalized into production economics.

The combination of policy support, synthetic fiber cost advantages, and rising sustainability requirements positions the GCC textile market at an inflection point. Manufacturers that invest now in process efficiency and material diversification will access preferential supply contracts from global fashion brands. Those that delay face both cost disadvantage and exclusion from sustainability-linked procurement frameworks.

Key Takeaways

- The GCC Textile Market is valued at USD 17.8 Billion in 2025 and is forecast to reach USD 29.3 Billion by 2035, at a CAGR of 5.1%.

- By Raw Material, Synthetic Fibers hold a dominant share of 65.8%, led by polyester, nylon, and recycled fiber variants.

- By Process/Technology, Woven leads with 37.5% share, reflecting established fabric manufacturing infrastructure across GCC industrial zones.

- By Application, Fashion & Apparel commands 41.3% share, making it the largest end-use segment in the GCC textile ecosystem.

- North America represents a key export destination, while Asia Pacific — particularly India — serves as a primary raw material and machinery supplier to GCC manufacturers.

- Key players operating in the GCC Textile Market include Alyaf Industrial Co. Ltd., SV Pittie Sohar Textiles, Takween Advanced Industries, and Aratex Group, among others.

Product Analysis

Synthetic Fibers dominates with 65.8% due to petrochemical feedstock cost advantage.

In 2025, Synthetic Fibers held a dominant market position in the By Raw Material segment of the GCC Textile Market, with a 65.8% share. GCC manufacturers benefit directly from proximity to refinery output, allowing polyester and nylon production at feedstock costs well below global averages. This structural cost advantage makes synthetic fiber dominance self-reinforcing — local producers can price competitively without sacrificing margin.

Natural Fibers serve a distinct and premium-positioned market within GCC textiles, supplying high-end fashion, luxury home textiles, and export-oriented product categories. The segment’s smaller share relative to synthetics reflects both raw material import dependence and higher processing costs. Nevertheless, natural fibers command price premiums that protect margin for manufacturers targeting luxury and mid-premium retail channels.

Process/Technology Analysis

Woven dominates with 37.5% due to broad application compatibility and established infrastructure.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the GCC Textile Market, with a 37.5% share. The woven process serves the widest range of end applications — from apparel and home textiles to industrial and technical fabrics — making it the most versatile and commercially entrenched production method in the region. In November 2025, the Saudi Stitch & Tex Expo showcased new product launches by GCC textile manufacturers, reflecting active capital investment in woven fabric production capabilities.

Knitted fabric manufacturing holds a structurally important position within GCC textile processing, particularly for sportswear, innerwear, and performance apparel categories. Knitting’s inherent stretch and comfort properties align with active lifestyle consumption patterns rising across GCC consumer demographics. Moreover, knitting machines offer faster production cycles than weaving for certain fabric constructions, allowing manufacturers to respond more efficiently to short-run fashion orders.

Non-woven processing is the highest-growth technology segment within GCC textiles, driven by medical, hygiene, construction, and filtration end-use demand. The GCC’s expanding healthcare infrastructure and hospitality sector consume nonwoven materials at a rate that outpaces traditional fabric categories. Therefore, manufacturers investing in nonwoven capacity are accessing a demand pool that is structurally less exposed to fashion cycle volatility.

3-D Weaving & Spacer Fabrics represent the most technically advanced production category within the GCC textile market. These processes produce engineered fabric structures used in aerospace components, medical implants, ballistic protection, and high-performance composites. GCC industrial free zones — particularly those aligned with aviation and defense supply chains — create a localized demand base for 3-D woven materials that few regional manufacturers currently serve, leaving a high-value capacity gap.

Application Analysis

Fashion & Apparel dominates with 41.3% due to large domestic consumer base and export orientation.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the GCC Textile Market, with a 41.3% share. The GCC’s young, brand-conscious population and high per-capita retail spending sustain strong domestic apparel demand. Additionally, Saudi and UAE manufacturers increasingly serve re-export markets, using free-zone infrastructure to supply African and South Asian retail buyers with finished garments and fabric.

Industrial/Technical Textiles carry the strongest structural growth trajectory among all GCC application segments. Construction, oil and gas, infrastructure, and defense sectors consume technical textiles for protective clothing, filtration systems, geotextiles, and composite reinforcements. As GCC governments accelerate megaproject delivery under Vision 2030 and related national plans, industrial textile consumption scales accordingly — making this the segment with the most policy-linked demand visibility.

Household & Home Textiles benefit from the GCC hospitality sector’s expansion, where hotel chains, resorts, and residential developers procure bedding, toweling, and decorative fabrics at institutional volumes. The GCC’s tourism infrastructure investment creates a procurement pipeline that is distinct from retail fashion cycles, giving home textile manufacturers relatively stable forward order visibility compared to apparel-focused counterparts.

Medical & Healthcare Textiles represent a high-margin, compliance-driven segment where GCC demand is growing in line with hospital infrastructure expansion and post-pandemic procurement standards. Nonwoven surgical drapes, isolation gowns, wound care materials, and sterilization wraps require certified manufacturing processes, which limits competition and supports pricing stability. Manufacturers entering this segment face high qualification barriers but benefit from long-term institutional supply contracts once approved.

Automotive & Transport Textiles serve a niche but strategically significant role within the GCC application landscape. Interior fabrics, acoustic insulation, seat covers, and technical composites for GCC-assembled vehicles and aviation interior refurbishment create specialized demand. The growth of GCC aviation MRO hubs and early-stage automotive assembly initiatives in Saudi Arabia signal that this segment’s procurement base will expand over the forecast period.

Key Market Segments

By Raw Material

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

- Natural Fibers

- Cotton

- Wool

- Silk

By Process/Technology

- Woven

- Knitted

- Non-woven

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

Government-Led Industrial Expansion and Sustainability Mandates Accelerate GCC Textile Investment

GCC governments have elevated domestic textile manufacturing as a strategic priority within their economic diversification agendas. Saudi Arabia’s Vision 2030, the UAE’s industrial strategy, and Oman’s Special Economic Zone programs allocate land, utilities, and capital incentives specifically to attract fiber processing and fabric manufacturing investors. This policy-backed cost structure removes a major barrier that historically made Gulf-based textile production uncompetitive against Asian alternatives.

In October 2025, a high-level Saudi delegation led by Vice Minister Khalil ibn Salamah engaged directly with India’s Ministry of Textiles to advance bilateral textile investments, with FY 2024–25 bilateral trade reaching USD 41.88 billion. This government-to-government coordination signals that Saudi Arabia treats textile sourcing and manufacturing investment as a diplomatic and economic priority — not simply a procurement decision. The scale of bilateral trade confirms the depth of supply chain integration being built.

According to a 2025 technical article sourced from Vu Phong Energy Group, switching from fossil-fuel boilers to electric heating systems paired with solar PV can reduce on-site CO₂ emissions by up to 50% compared with baseline fossil systems. For GCC manufacturers subject to international buyer sustainability requirements, this reduction is not aspirational — it is increasingly a contractual threshold. Manufacturers that achieve this reduction gain access to sustainability-linked sourcing agreements that competitors operating conventional plants cannot qualify for.

Restraints

Import Dependence and Input Cost Volatility Compress GCC Textile Manufacturer Margins

GCC textile manufacturers depend heavily on imported raw materials — including cotton, wool, silk, and specialized synthetic fiber grades — as well as imported machinery components for spinning, weaving, and finishing operations. This dual import exposure creates a structural cost vulnerability. When global cotton prices rise or container freight costs spike, GCC manufacturers absorb margin pressure that domestically integrated competitors in India, Bangladesh, or China can partially offset through vertical supply chains.

In February 2025, Vardhman Textiles unveiled an INR 2,350 crore expansion plan targeting GCC export markets, including INR 2,000 crore for spinning, weaving, and technical textiles and INR 350 crore for fabric processing. While this signals strong supplier commitment to the GCC market, it also illustrates the competitive pressure facing local GCC producers — Indian manufacturers are investing at scale specifically to capture supply contracts that GCC-based producers might otherwise develop domestically.

According to a 2025 WSEAS paper, implementing integrated energy-management systems and best-available technologies can yield electricity and fuel savings of 10–25% in textile mills, with payback periods under 5 years. This data point reframes the energy cost restraint: the technology to address it is available and financially viable, yet adoption remains uneven. GCC manufacturers that delay energy system upgrades are not just facing higher operating costs — they are forfeiting a documented margin improvement opportunity that more proactive competitors are already capturing.

Growth Factors

Smart Textile Capabilities, Digital Commerce Infrastructure, and Strategic Brand Partnerships Open New Revenue Streams

The development of smart textile and wearable fabric manufacturing within GCC industrial zones opens a product category with materially higher revenue per meter than conventional fabric. Smart textiles — incorporating conductive threads, embedded sensors, or responsive coatings — serve defense, healthcare, and sports performance buyers who pay specification-based prices rather than commodity rates. GCC manufacturers that build these capabilities early position themselves to supply categories where Asian mass producers have not yet established scale advantages.

According to a 2025 World Bank working document on textile sector decarbonization, deep efficiency measures and fuel-switching in textile manufacturing can deliver energy savings of 20–30% at the facility level. For GCC manufacturers, this is directly relevant: facilities that implement these measures reduce cost per unit while simultaneously qualifying for green procurement frameworks. In July 2025, Stride Ventures launched its ADGM Fund V with a USD 110 million pipeline targeting GCC expansion — including textile-adjacent logistics and climate-tech ventures — with plans to triple GCC assets under management to USD 500 million by 2026. Capital is actively flowing into the ecosystem.

The expansion of e-commerce fashion platforms across the GCC creates demand for shorter, more responsive local textile supply chains. International fashion platforms operating in Saudi Arabia and the UAE face delivery time pressures that favor sourcing from regional manufacturers over longer Asian supply routes. Additionally, strategic partnerships between GCC textile producers and global luxury brands — a trend accelerating as European houses seek Gulf-market proximity — create contract manufacturing opportunities at price points that justify investment in premium fabric capabilities.

Emerging Trends

AI-Driven Quality Systems, Circular Economy Practices, and High-Performance Nonwovens Redefine GCC Textile Operations

GCC textile manufacturers are deploying AI-driven quality inspection systems that identify fabric defects at production line speeds, reducing waste and rework costs that traditionally erode finishing-stage margins. These systems replace manual inspection — which is expensive, inconsistent, and difficult to scale — with machine vision tools that operate continuously and generate data for process improvement. Early adopters gain a dual advantage: lower defect rates and a documented quality management record that satisfies international buyer audit requirements.

Eco-friendly dyeing and waterless textile processing technologies are shifting from pilot-phase to commercial deployment across GCC finishing operations. Waterless dyeing methods — including supercritical CO₂ dyeing and digital inkjet printing — eliminate the effluent treatment costs and water consumption that conventional wet processing imposes. According to the Apparel Impact Institute and GEIDCO’s Low-Carbon Thermal Energy Roadmap, replacing conventional fossil-fuel boilers with steam-generating heat pumps can save approximately 48 GWh of thermal energy per plant per year. This scale of energy saving makes the technology commercially compelling, not just environmentally responsible.

High-performance nonwoven fabric investment represents the most commercially immediate trend in GCC technical textiles. Healthcare infrastructure expansion across the Gulf region generates institutional procurement for surgical nonwovens, filtration media, and wound care materials at volumes that justify dedicated manufacturing lines. The integration of circular economy practices — including fiber-to-fiber recycling programs and closed-loop dyehouse water systems — is also advancing from corporate commitment to operational reality, with manufacturers responding to brand partner requirements that now include end-of-life textile management standards.

Country Analysis

Saudi Arabia Dominates the GCC Textile Market with the Largest Market Share, Valued at the Core of the USD 17.8 Billion Regional Base

Saudi Arabia holds the commanding position within the GCC textile market, anchored by Vision 2030’s textile and apparel manufacturing targets, the King Abdullah Economic City industrial cluster, and the country’s scale as both the largest domestic consumer and leading regional exporter. Government procurement mandates for uniforms, healthcare textiles, and hospitality materials concentrate institutional demand within Saudi borders, creating a buyer base that supports local manufacturer scale-up independent of export market access.

UAE GCC Textile Market Trends

The UAE functions as the GCC’s textile trade and re-export hub, with Jebel Ali Free Zone and Dubai Textile City facilitating material flows between Asian suppliers and regional buyers. UAE-based manufacturers concentrate on value-added categories — technical textiles, luxury fabrics, and digitally printed materials — where free-zone infrastructure and logistics connectivity create competitive advantages that commodity fabric producers in other GCC markets cannot replicate.

Oman GCC Textile Market Trends

Oman’s Sohar Industrial Port hosts established textile manufacturing operations — including SV Pittie Sohar Textiles — that benefit from port-direct raw material access and preferential trade agreements with India and the broader Indian Ocean rim. The Omani government’s Special Economic Zone incentives attract spinning and weaving capacity specifically, positioning Oman as a production base for regional apparel manufacturers that need cost-competitive fabric supply within GCC customs boundaries.

Qatar GCC Textile Market Trends

Qatar’s textile market is shaped primarily by institutional and hospitality demand, driven by the country’s large expatriate workforce, FIFA World Cup legacy infrastructure, and ongoing hotel and residential development. Local manufacturing capacity remains limited compared to Saudi Arabia and Oman, making Qatar a net importer of both raw materials and finished textiles. However, the scale of Qatar’s hospitality procurement creates a predictable, volume-stable demand pool for regional suppliers with hotel-grade home textile certifications.

Kuwait and Bahrain GCC Textile Market Trends

Kuwait and Bahrain represent smaller but commercially viable textile markets within the GCC, driven by retail fashion consumption and institutional procurement for healthcare and hospitality. Both markets rely predominantly on imports from UAE trade channels and direct Asian suppliers. Nevertheless, their high per-capita spending and brand-conscious consumer base make them priority retail markets for GCC-manufactured premium apparel and home textile products targeting Gulf lifestyle buyers.

Key Company Insights

Alyaf Industrial Co. Ltd. holds a strategically anchored position within the GCC synthetic fiber supply chain, producing polyester staple fiber that feeds directly into regional spinning and weaving operations. Its integration within the Saudi petrochemical corridor gives it a feedstock cost structure that imported fiber suppliers cannot match on a landed-cost basis. This positions Alyaf as a default supplier for GCC mills prioritizing supply chain security over global price arbitrage.

SV Pittie Sohar Textiles leverages Oman’s Sohar Port infrastructure to operate as a cost-competitive spinning and yarn manufacturing base serving GCC and export markets simultaneously. Its Indian parent group’s textile expertise combined with Omani free-zone incentives creates a hybrid cost model that is difficult for pure GCC-domestic producers to replicate. In February 2025, Vardhman Textiles — a major peer in the Indian textile ecosystem — launched three new innovative yarn collections at Bharat Tex 2025 with Saudi companies participating as buyers, confirming that Indian-origin GCC manufacturers actively compete for regional premium yarn contracts.

Takween Advanced Industries differentiates through its focus on technical and specialty packaging-adjacent textile applications, serving a product range that straddles rigid packaging and flexible nonwoven materials. This positioning insulates Takween from direct fashion market volatility while connecting its revenue base to FMCG, food, and industrial sector procurement cycles. Its Saudi Industrial Development Fund relationships give it access to capital structures that smaller GCC textile manufacturers cannot secure independently.

Aratex Group operates across the GCC uniform and workwear segment, supplying corporate, hospitality, and industrial buyers with specification-grade garments that require consistent quality across large procurement volumes. The workwear segment provides Aratex with long-term institutional contracts that buffer against fashion retail seasonality. Its ability to manage large-volume, multi-location uniform programs for GCC hospitality and oil sector clients creates switching costs that protect its market position from lower-cost import substitution.

Key Players

- Alyaf Industrial Co. Ltd.

- SV Pittie Sohar Textiles

- Takween Advanced Industries

- Aratex Group

- Avgol Middle East

- Al Abdullatif Industrial Investment Company

- Threads Group LLC

- Unirab & Polvara Spinning, Weaving & Silk

- Al Ghurair Textile Mills

- Emirates Textile Industries LLC

Recent Developments

- February 2026 — Rieter completed the acquisition of the Barmag Division of OC Oerlikon, positioning itself as the world’s leading system provider for natural and synthetic fibre processing. This acquisition strengthens the machinery supply ecosystem serving GCC spinning operations that depend on Barmag-engineered filament winding and texturing systems.

- February 2026 — Lenzing announced the acquisition of a controlling majority stake in Swedish innovation company TreeToTextile AB, reinforcing its sustainable wood-based speciality fibre pipeline to Middle East markets. This move expands the range of certified sustainable fibre options available to GCC apparel manufacturers targeting eco-conscious retail buyers.

- February 2026 — Sparxell raised USD 5 million to scale plant-based dye manufacturing toward tonne-level production from 2026, targeting fashion brands sourcing from the GCC. This investment signals commercial readiness for bio-based colourant supply at volumes relevant to regional fabric finishers.

- December 2025 — Reliance Industries earmarked an INR 75,000 crore five-year investment to expand polyester, PTA, PET, PFY, and PSF capacities. As a major supplier to GCC apparel manufacturers, this capacity expansion improves forward supply security for regional producers dependent on Indian polyester feedstock.

- September 2025 — Indian textile companies led by EPCH participated in Saudi INDEX 2025, expanding GCC market entry partnerships and deepening the India-GCC textile trade corridor that supports both fabric imports and co-manufacturing arrangements.

- November 2024 — Berry Global completed the acquisition of a specialized European nonwovens manufacturer, adding 25,000 metric tons of annual capacity that directly supplies hygiene and medical textile segments in the GCC. This acquisition expands the availability of certified nonwoven materials for Gulf healthcare and personal care manufacturers.

- August 2024 — Toray Industries announced a strategic partnership with a leading aerospace OEM to co-develop next-generation carbon fiber composites. This collaboration advances a technical textile category with direct application in GCC aviation hubs, where composite material demand for MRO and new aircraft interiors continues to grow.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 17.8 Billion |

| Forecast Revenue (2035) | USD 29.3 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Synthetic Fibers, Natural Fibers), By Process/Technology (Woven, Knitted, Non-woven, 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Alyaf Industrial Co. Ltd., SV Pittie Sohar Textiles, Takween Advanced Industries, Aratex Group, Avgol Middle East, Al Abdullatif Industrial Investment Company, Threads Group LLC, Unirab & Polvara Spinning, Weaving & Silk, Al Ghurair Textile Mills, Emirates Textile Industries LLC |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |