Quick Navigation

Report Overview

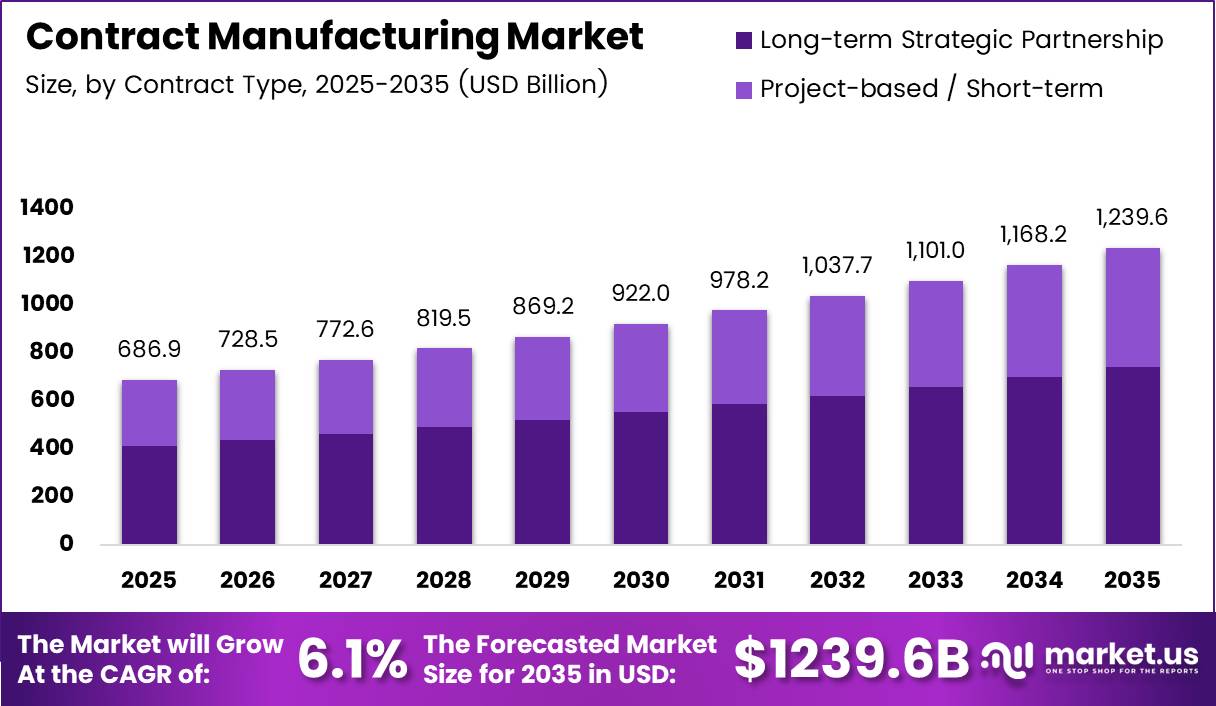

Global Contract Manufacturing Market size is expected to be worth around USD 1,239.6 Billion by 2035 from USD 686.9 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035. This trajectory reflects a structural shift in how global manufacturers allocate production responsibility across specialized third-party providers.

Contract manufacturing is the practice of outsourcing production to specialized third-party manufacturers. Brand owners and product developers retain design, marketing, and distribution control. The manufacturing partner handles equipment, labor, and process execution. This model spans electronics, pharmaceuticals, automotive, consumer goods, food and beverage, and industrial machinery sectors.

The market organizes around two core contract structures: long-term strategic partnerships and project-based short-term agreements. Long-term arrangements dominate because they support capacity planning and supply chain stability. Short-term contracts serve overflow production needs and product launch cycles. Both structures benefit from the same underlying trend toward asset-light operating models among global product companies.

Regulatory frameworks shape contract manufacturing activity across all verticals. Pharmaceutical manufacturing requires compliance with FDA, EMA, and national GMP standards. Electronics manufacturing must meet RoHS, REACH, and country-specific import regulations. Automotive supply chains operate under ISO/TS quality standards. These compliance requirements create barriers to entry that favor established providers with certified facilities and audit-ready operations.

Government investment in domestic manufacturing infrastructure is reshaping where contracts are placed. Industrial policy programs across the US, EU, and Asia Pacific are directing capital toward semiconductor fabrication, pharmaceutical production, and EV battery assembly. This policy activity creates a shift in contract allocation, moving volume toward regions with subsidy-backed cost structures and regulatory incentives for local sourcing.

According to the Qimtek Contract Manufacturing Index, 1,254 outsourced manufacturing projects were recorded from 427 buying companies during 2025. This scale of activity confirms that outsourcing decisions are widespread across company sizes and sectors, not concentrated in a single industry. Buyers who can offer competitive lead times and process flexibility hold a structural advantage in winning repeat project volumes.

Data from the Qimtek CMI shows contract manufacturing activity increased by 47% in 2025 compared with the 2024 average. This rise confirms that outsourcing volumes are accelerating across the manufacturing base. Providers who have invested in production flexibility and supplier coordination are best positioned to absorb this volume without margin compression.

Key Takeaways

- The global Contract Manufacturing Market was valued at USD 686.9 Billion in 2025 and is forecast to reach USD 1,239.6 Billion by 2035.

- The market will expand at a CAGR of 6.1% during the forecast period 2026 to 2035.

- By Contract Type, Long-term Strategic Partnership dominates with a 59.6% share in 2025.

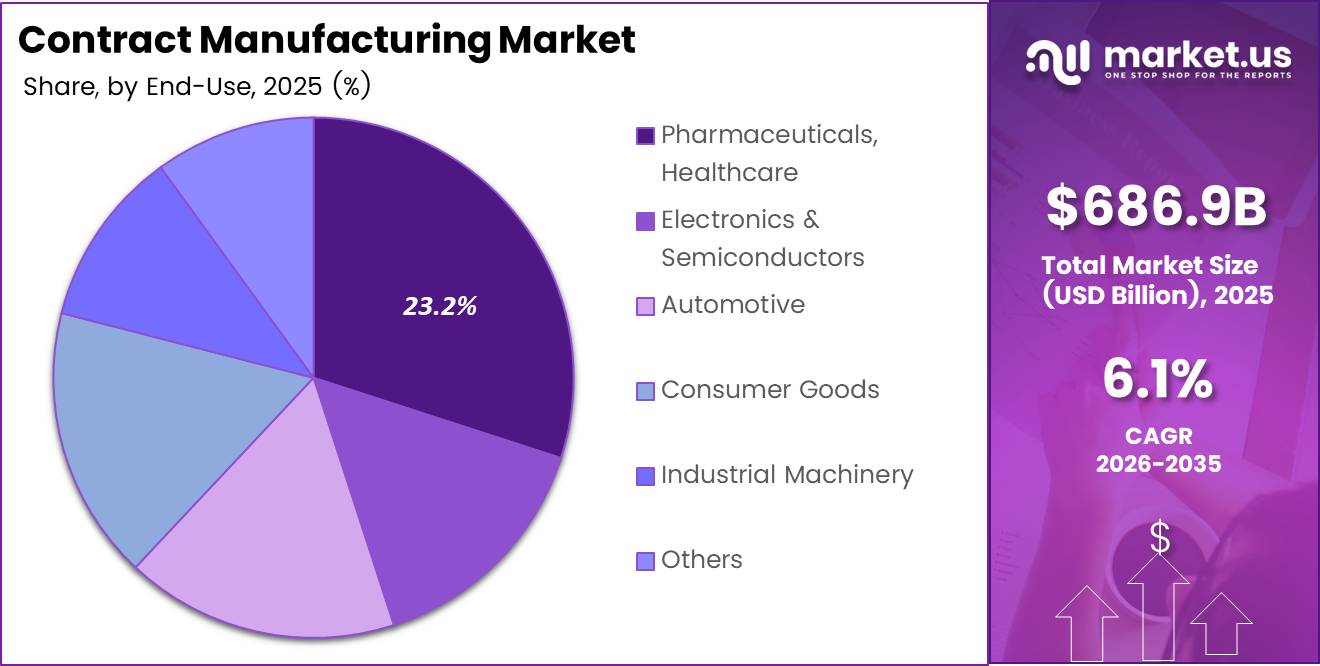

- By End-Use, Pharmaceuticals, Healthcare and Medical Devices leads with a 23.2% share.

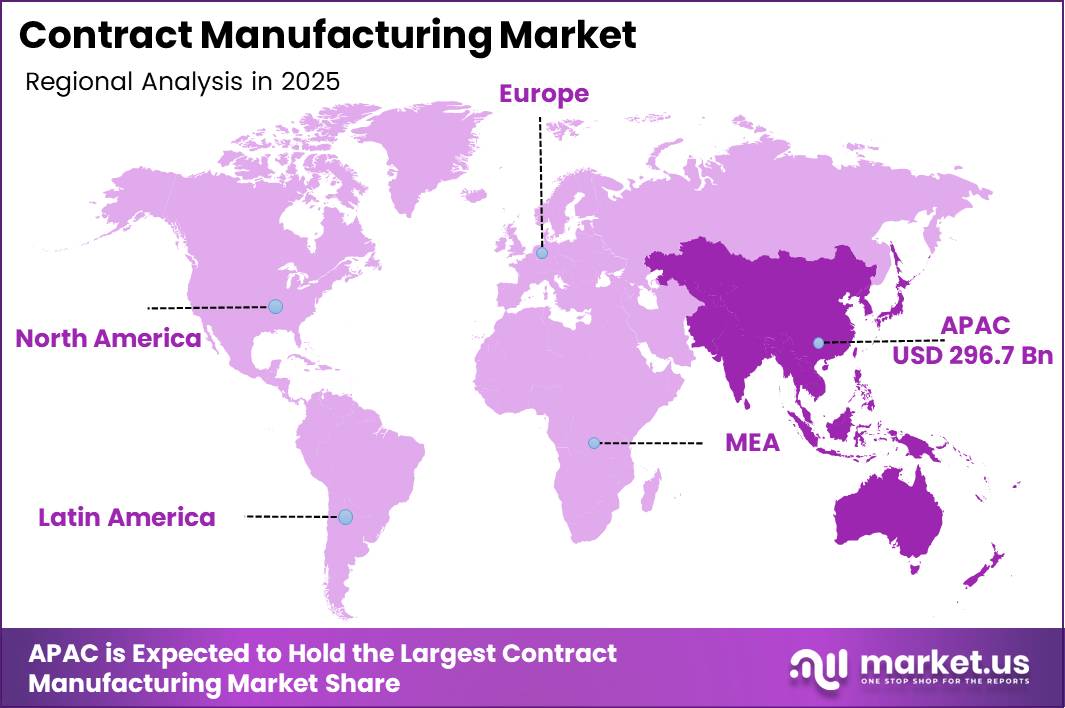

- Asia Pacific holds the dominant regional position with a 43.20% market share, valued at USD 296.7 Billion.

- Automotive companies accounted for 39% of all outsourced manufacturing projects in Q3 2025.

- Contract fabrication outsourcing activity increased by 60% in 2025 compared with 2024 levels.

- The Contract Manufacturing Index rose by 62% in Q2 2025 compared with Q1 2025.

- The value of outsourced fabrication projects reached £25.8 million in Q3 2025, an 18% increase from Q2 2025.

Contract Type Analysis

Long-term Strategic Partnership dominates with 59.6% due to stable capacity commitments and supply chain continuity.

In 2025, Long-term Strategic Partnership held a dominant market position in the By Contract Type segment of the Contract Manufacturing Market, with a 59.6% share. This dominance reflects buyer preference for supply chain stability over transactional flexibility. Buyers who lock in long-term agreements gain priority access to capacity, tighter quality control, and lower per-unit costs across multi-year production runs.

Project-based and short-term contracts serve a distinct operational role for manufacturers managing product launches, demand spikes, or capacity overflow. These agreements allow buyers to activate production without committing to long-term facility investments. As reported by the Qimtek CMI, Q2 2025 recorded 285 projects from 183 buyer companies, signaling that short-term outsourcing is an active and recurring procurement strategy across diverse product categories.

End-Use Analysis

Pharmaceuticals, Healthcare and Medical Devices dominates with 23.2% due to high compliance barriers and specialized production needs.

In 2025, Pharmaceuticals, Healthcare and Medical Devices held a dominant market position in the By End-Use segment of the Contract Manufacturing Market, with a 23.2% share. Regulatory requirements for GMP compliance, validated processes, and batch traceability make in-house manufacturing capital-intensive. Outsourcing to certified CDMOs reduces fixed investment while preserving quality standards, making this the most structurally embedded outsourcing relationship in the entire market.

Electronics and Semiconductors is the second-largest end-use segment, covering consumer electronics, industrial IoT devices, telecom equipment, computing infrastructure, and semiconductor assembly. This segment drives high outsourcing volumes because product cycles are short and capital investment in fabrication is prohibitive for most brand owners. Contract manufacturers in this segment compete on yield rates, component sourcing relationships, and time-to-production speed.

Key Market Segments

By Contract Type

- Long-term Strategic Partnership

- Project-based / Short-term

By End-Use

- Pharmaceuticals, Healthcare & Medical Devices

- API & FDF (Small-molecule)

- Biologics Manufacturing (Cell & Gene Therapy, mAbs)

- Nutraceuticals / OTC Drugs

- Medical Devices (diagnostics, surgical, etc.)

- Others

- Electronics & Semiconductors

- Consumer Electronics (smartphones, IoT devices, etc.)

- Industrial & IoT Electronics

- Telecommunication Equipment

- Computing & Data Infrastructure

- Semiconductor Assembly, Packaging & Testing (OSAT)

- Others

- Automotive

- Powertrain Components (ICE, Electric & Hybrid)

- EV Battery Packs

- Interior & Exterior Assemblies

- Embedded Electronics

- ADAS / Autonomous Modules

- Consumer Goods

- Home Appliances

- Personal Care & Wearables

- Others

- Industrial Machinery

- Textiles & Apparel

- Garment Manufacturing

- Others

- Textiles & Apparel

- Food & Beverage

- Food Processing

- Beverage Bottling

- Packaging & Labeling

- Others

- Personal Care & Cosmetics

- Others

Drivers

Contract manufacturing activity rises 47% as asset-light models spread across sectors

The Qimtek CMI found that contract manufacturing activity increased by 47% in 2025 compared with the 2024 average. This rise reflects a deliberate strategic choice by product companies to remove fixed manufacturing assets from their balance sheets. Buyers who outsource production gain capital flexibility and can redirect investment toward product development, brand building, and distribution expansion.

Scalable production capacity is a critical requirement for manufacturers operating across multiple industry verticals with unpredictable demand cycles. Contract manufacturers offer the ability to increase or decrease output without triggering fixed-cost penalties. This structural benefit makes outsourcing particularly attractive to companies launching new product lines, entering new markets, or managing seasonal demand variation without building permanent capacity.

In April 2025, PCI Pharma Services announced the acquisition of Ajinomoto Althea, expanding its injectable drug manufacturing, aseptic fill-finish, oligonucleotide, and peptide manufacturing capabilities. This transaction demonstrates how pharmaceutical contract manufacturers are investing in specialized capability expansion to meet outsourcing demand from drug developers who lack internal sterile manufacturing infrastructure. Providers with certified sterile manufacturing capacity command long-term contract premiums.

The Contract Manufacturing Index increased by 52% in Q1 2025 compared with Q4 2024, according to the Qimtek CMI. This sharp quarterly rise confirms that outsourcing demand is not seasonal. Manufacturers who built capacity and supplier relationships ahead of this demand wave secured volume at favorable terms, while late movers faced lead time pressure and reduced negotiating leverage.

Contract fabrication outsourcing activity increased by 60% in 2025 compared with 2024 levels, as reported by the Qimtek CMI. Fabrication covers metal forming, welding, and structural assembly operations that require capital equipment most product companies prefer not to own. This volume shift confirms that fabrication is one of the fastest-outsourcing sub-categories, creating durable demand for contract providers with certified fabrication capacity.

Restraints

IP transfer risks and supply disruptions slow contract placement decisions in 2025

Intellectual property protection remains a primary concern for product companies considering contract manufacturing partnerships. Brand owners risk exposing proprietary formulations, process parameters, and design specifications to third-party manufacturers. This risk is highest in sectors such as pharmaceuticals and electronics where competitive advantage is built on protected manufacturing processes. IP concerns slow contract finalization and increase legal and audit costs for both parties.

Granules India signed a definitive agreement in February 2025 to acquire Senn Chemicals AG, a Switzerland-based peptide CDMO. This transaction illustrates how pharmaceutical companies respond to IP risk by acquiring rather than outsourcing critical technology capabilities. Acquisition strategies reduce IP exposure but require substantial capital deployment and integration effort, limiting this approach to larger, well-capitalized companies.

Based on Qimtek CMI data, average supplier lead times decreased from 20 days in 2024 to 19 days in 2025, representing a 5% reduction. While this improvement signals operational progress, lead times remain a commercial constraint. Buyers managing tight production schedules require predictable delivery windows, and any disruption to supplier timelines translates directly into downstream production delays and customer service failures.

The value of outsourced fabrication projects reached £25.8 million in Q3 2025, an 18% increase from Q2 2025, as reported by the Qimtek CMI. This growth in fabrication value confirms that more complex and higher-value work is moving to contract providers. However, higher-value contracts carry greater disruption consequences, meaning supply chain failures in fabrication carry heavier financial penalties than in lower-value sub-categories.

Outsourced machining contracts reached £19.69 million in Q2 2025, based on Qimtek CMI data. The concentration of high-value machining work among contract providers creates single-point-of-failure risks for buyers relying on individual suppliers for precision components. Buyers who have not diversified their machining supply base face production vulnerability if a primary contract manufacturer experiences capacity disruption or financial difficulty.

Growth Factors

Nearshoring and end-to-end services expand contract scope beyond single-process production

Nearshoring strategies are redirecting contract manufacturing volume toward regional production hubs in Eastern Europe, Mexico, and Southeast Asia. Product companies are shortening supply chains to reduce transit risk and comply with local content requirements embedded in trade agreements. This structural shift creates contract manufacturing demand in regions that previously had limited outsourcing infrastructure, expanding the total addressable market for established providers.

Contract machining outsourcing activity increased by 27% in 2025 compared with 2024 levels, according to the Qimtek CMI. This growth confirms that precision machining is actively migrating from in-house to contract production. Providers who invested in CNC capacity, metrology equipment, and machining talent are positioned to capture a share of this expanding outsourcing volume without competing solely on unit price.

Q1 2025 contract manufacturing activity included 362 outsourced projects submitted by 217 companies, as reported by the Qimtek CMI. The breadth of buyer participation confirms that outsourcing adoption spans company size and sector. Contract manufacturers who develop structured onboarding processes and multi-sector capability certifications are better positioned to serve this diverse buyer base than providers optimized for a single vertical.

The value of outsourced machining work reached £19.2 million in Q3 2025, which was 68% higher than Q3 2024, based on Qimtek CMI data. This year-on-year increase confirms sustained structural growth in machining outsourcing rather than a single-quarter anomaly. Providers who can demonstrate certified quality systems and multi-material machining capability are winning a disproportionate share of this rising value pool.

Outsourced fabrication contracts reached £21.91 million in Q2 2025, according to the Qimtek CMI. The scale of fabrication contract value confirms that buyers are entrusting high-value structural work to contract providers. End-to-end providers who combine fabrication, machining, and assembly under one quality system can offer buyers consolidated supply chain accountability, reducing total procurement management cost and strengthening long-term contract retention.

Emerging Trends

Digital manufacturing platforms and predictive analytics reshape production visibility in 2025

Contract manufacturers are integrating digital manufacturing platforms to provide buyers with real-time production status, quality data, and inventory visibility. This capability addresses a core buyer concern: lack of operational transparency in outsourced production. Providers who offer live production dashboards and exception reporting create a stickier customer relationship, as switching to a provider without this capability represents a backward step in supply chain control.

Manufacturers requested quotations for 19.8 million parts through the Qimtek outsourcing platform during 2025, as reported by the Qimtek CMI. The volume of parts in active sourcing demonstrates that buyers are using digital procurement platforms to access contract capacity at scale. Contract manufacturers who maintain strong platform profiles and fast quotation response times capture disproportionate visibility among the buying population.

The Contract Manufacturing Index increased by 62% in Q2 2025 compared with Q1 2025, based on Qimtek CMI data. This acceleration confirms that outsourcing demand is not plateauing. Contract manufacturers who deploy predictive analytics for capacity planning and inventory optimization are better prepared to absorb demand spikes without delivery failure, giving them a competitive advantage in renewing and expanding buyer contracts.

Q3 2025 contract manufacturing activity increased by 10% compared with Q2 2025, according to the Qimtek CMI. This sequential growth confirms that demand is building across consecutive quarters. Contract manufacturers investing in flexible manufacturing systems and rapid product changeover capability are positioned to serve buyers whose product customization requirements are outpacing the capacity of traditional dedicated production lines.

Regional Analysis

Asia Pacific Dominates the Contract Manufacturing Market with a Market Share of 43.20%, Valued at USD 296.7 Billion

Asia Pacific holds a 43.20% share of the global Contract Manufacturing Market, valued at USD 296.7 Billion. This dominance reflects decades of investment in manufacturing infrastructure, a deep pool of skilled production labor, and established supply chain ecosystems in China, South Korea, Japan, India, and Southeast Asia. Government industrial policy across the region continues to direct capital toward advanced manufacturing capability, reinforcing the region’s position as the primary global production hub.

North America holds the second-largest regional position in the contract manufacturing market. Pharmaceutical and medical device contract manufacturing is concentrated in the US due to FDA facility proximity requirements and the depth of the domestic CDMO ecosystem. The nearshoring trend is also expanding contract manufacturing activity in Mexico, particularly in automotive and electronics assembly, as US buyers seek shorter supply chains with lower geopolitical risk than Asia-sourced production.

Europe is a significant contract manufacturing region anchored by pharmaceutical CDMOs in Switzerland, Germany, and Ireland, and by precision engineering and automotive component manufacturers in Germany, France, and Poland. European contract manufacturers compete on quality certification depth, regulatory compliance capability, and proximity to the EU market. Labor costs are higher than Asia Pacific, but total delivered cost calculations favor European providers for complex, low-volume, high-specification contracts.

Latin America is an emerging contract manufacturing destination driven by Mexico’s automotive supply chain integration with the US market and Brazil’s domestic consumer goods manufacturing base. The region benefits from favorable US trade agreements and growing investment in manufacturing capacity from both domestic and foreign buyers seeking supply chain diversification away from Asia.

The Middle East and Africa region is at an earlier stage of contract manufacturing development, with growth concentrated in pharmaceutical and food processing outsourcing in GCC markets and South Africa. Government-backed industrialization programs in Saudi Arabia and the UAE are directing investment toward domestic manufacturing capability. This policy activity is expanding the addressable contract manufacturing base in the region but from a smaller established foundation than other regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Hon Hai Precision operates as the world’s largest electronics contract manufacturer, with production scale spanning consumer electronics, computing infrastructure, and EV components. Its integrated supply chain model gives buyers a single provider capable of managing component sourcing, assembly, and logistics at volumes that smaller providers cannot match. This scale creates deep customer dependency but also exposes the company to concentrated revenue risk from a small number of hyperscale clients.

Flex Ltd positions itself as an end-to-end manufacturing solutions provider spanning design, engineering, supply chain management, and production across multiple sectors. This breadth allows Flex to compete for complex program wins that require more than pure production capacity. However, broad sector coverage also creates management complexity and can dilute specialization in verticals where deep process expertise is the primary competitive requirement.

Jabil Inc. serves electronics, healthcare, and packaging markets through a global network of manufacturing facilities with strong design and engineering support capabilities. Jabil’s investment in digitally connected manufacturing operations gives buyer-facing teams greater production visibility. Q3 2025 recorded 313 outsourced manufacturing projects from 216 companies, per Qimtek CMI data, reflecting the broad buyer base that providers like Jabil are positioned to serve through multi-sector capability and geographic distribution.

Celestica Inc. focuses on high-complexity electronics manufacturing for aerospace, defense, healthcare, and enterprise computing sectors. Its specialization in regulated and high-reliability markets creates a higher barrier for both entry by competitors and exit by customers. The “other processes” category reached £3.6 million in Q3 2025, a 45% increase from Q2, according to Qimtek CMI data, illustrating that specialty process outsourcing is actively expanding alongside mainstream fabrication and machining volumes.

Key Players

- Hon Hai Precision

- Flex Ltd

- Jabil Inc.

- Celestica Inc.

- Wistron Corp.

- Sanmina Corp.

- Benchmark Electronics Inc.

- Pegatron Corp.

- Plexus Corp.

- Universal Scientific Industrial Co. Ltd

- BYD Electronics

- Compal Electronics Inc.

- Shenzhen Kaifa Tech Co. Ltd

Recent Developments

- May 2025 – PCI Pharma Services completed the acquisition of Ajinomoto Althea, a US-based sterile fill-finish CDMO, strengthening its North American contract development and manufacturing footprint and adding large-scale sterile manufacturing capacity in California.

- April 2025 – Granules India completed the acquisition of Senn Chemicals AG for approximately CHF 20 million, expanding its global contract development and manufacturing capabilities in peptide-based therapeutics.

- June 2025 – Zydus Lifesciences announced plans to acquire two biologics manufacturing facilities from Agenus Inc. in California for up to US $125 million, marking its entry into the global biologics CDMO market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 686.9 Billion |

| Forecast Revenue (2035) | USD 1,239.6 Billion |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Contract Type (Long-term Strategic Partnership, Project-based / Short-term); By End-Use (Pharmaceuticals, Healthcare & Medical Devices [API & FDF, Biologics Manufacturing, Nutraceuticals / OTC Drugs, Medical Devices, Others], Electronics & Semiconductors [Consumer Electronics, Industrial & IoT Electronics, Telecommunication Equipment, Computing & Data Infrastructure, OSAT, Others], Automotive [Powertrain Components, EV Battery Packs, Interior & Exterior Assemblies, Embedded Electronics, ADAS / Autonomous Modules], Consumer Goods [Home Appliances, Personal Care & Wearables, Others], Industrial Machinery [Textiles & Apparel, Garment Manufacturing, Others], Food & Beverage [Food Processing, Beverage Bottling, Packaging & Labeling, Others], Personal Care & Cosmetics, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Hon Hai Precision, Flex Ltd, Jabil Inc., Celestica Inc., Wistron Corp., Sanmina Corp., Benchmark Electronics Inc., Pegatron Corp., Plexus Corp., Universal Scientific Industrial Co. Ltd, BYD Electronics, Compal Electronics Inc., Shenzhen Kaifa Tech Co. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |