Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Drug Development Analysis

- Formulation Analysis

- Route of Administration Analysis

- Therapy Area Analysis

- Age Group Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

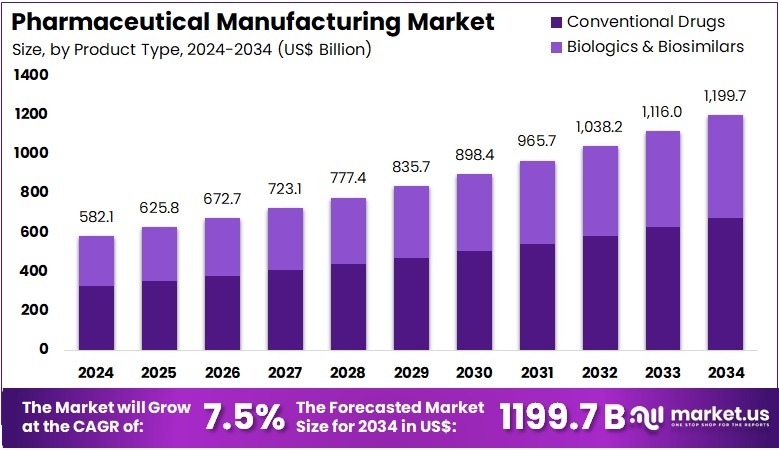

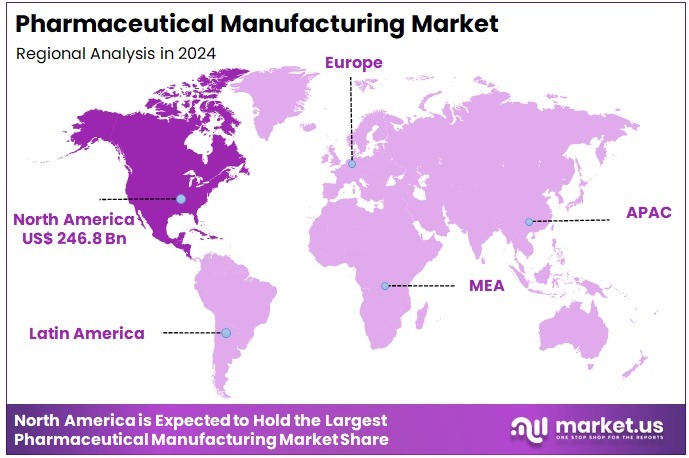

The Pharmaceutical Manufacturing Market Size is expected to be worth around US$ 1199.7 billion by 2034 from US$ 582.1 billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 42.4% share and holds US$ 246.8 Billion market value for the year.

Increasing demand for affordable and effective healthcare solutions is driving the growth of the pharmaceutical manufacturing market. The need for faster, more efficient production processes and cost-effective therapies has led to significant advancements in drug manufacturing technologies. Pharmaceutical companies are increasingly focusing on biologics, including biosimilars, to address the rising prevalence of chronic diseases such as cancer, diabetes, and autoimmune disorders.

These trends highlight the opportunities for innovation in manufacturing methods, including continuous manufacturing and automation, to improve efficiency and reduce production costs. In June 2023, Pfizer and Samsung Biologics formed a strategic partnership to enhance biosimilar production. This collaboration will expand Pfizer’s manufacturing capacity for biologics in immunology, oncology, and inflammation, addressing the growing global demand for affordable biologic treatments. The partnership demonstrates the industry’s commitment to increasing access to high-quality, cost-effective therapeutics, contributing to the ongoing evolution of pharmaceutical manufacturing.

Key Takeaways

- In 2024, the market for pharmaceutical manufacturing generated a revenue of US$ 582.1 billion, with a CAGR of 7.5%, and is expected to reach US$ 1199.7 billion by the year 2034.

- The product type segment is divided into biologics & biosimilars and conventional drugs, with conventional drugs taking the lead in 2024with a market share of 56.2%.

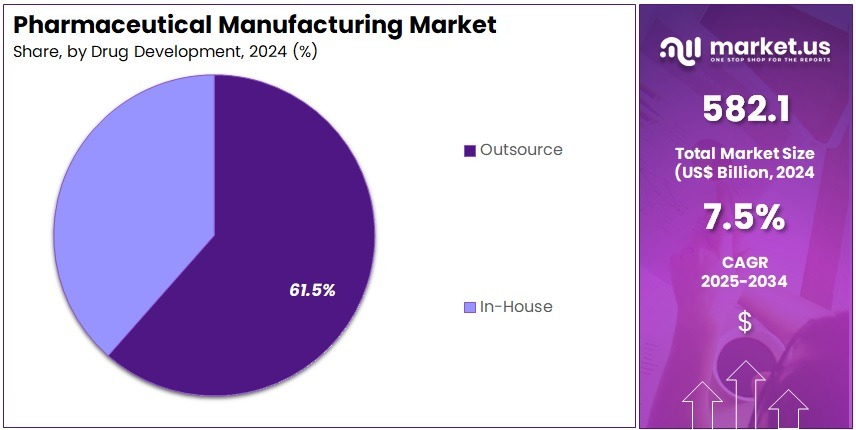

- Considering drug development, the market is divided into in-house and outsource. Among these, outsource held a significant share of 61.5%.

- Furthermore, concerning the formulation segment, the market is segregated into tablets, suspensions, sprays, powders, injectable, capsules, and others. The tablets sector stands out as the dominant player, holding the largest revenue share of 45.3% in the pharmaceutical manufacturing market.

- The route of administration segment is segregated into oral, topical, parenteral, inhalations, and others, with the oral segment leading the market, holding a revenue share of 57.5%.

- Furthermore, concerning the therapy area segment, the market is segregated into cardiovascular diseases, respiratory diseases, pain, diabetes, cancer, and other. The cardiovascular diseases sector stands out as the dominant player, holding the largest revenue share of 47.3% in the pharmaceutical manufacturing market.

- The age group segment is segregated into children & adolescents, adults, and geriatric, with the adults segment leading the market, holding a revenue share of 54.5%.

- North America led the market by securing a market share of 42.4% in 2024.

Product Type Analysis

The conventional drugs segment led in 2024, claiming a market share of 56.2% as the demand for cost-effective treatments remains strong. Conventional drugs, which are typically chemical-based, are anticipated to see continued use due to their lower production costs compared to biologics. As healthcare providers strive to manage budgets while delivering effective treatments, conventional drugs will likely remain a staple in many therapeutic areas.

Additionally, the increasing prevalence of chronic diseases, such as hypertension and diabetes, is expected to drive demand for affordable conventional treatments. The established infrastructure for producing these drugs and the ability to address a wide range of conditions will support the growth of this segment.

Drug Development Analysis

The outsource held a significant share of 61.5% as more companies turn to external partners for specialized services. Outsourcing allows pharmaceutical companies to reduce costs, speed up time-to-market, and leverage expertise in various aspects of drug development.

With the rising complexity of drug development processes and the growing demand for new therapies, more companies are expected to outsource clinical trials, manufacturing, and research activities to contract research organizations (CROs) and contract manufacturing organizations (CMOs). Outsourcing provides flexibility and efficiency, which will likely drive its growth in the pharmaceutical manufacturing market.

Formulation Analysis

The tablets segment had a tremendous growth rate, with a revenue share of 45.3% owing to the widespread use of tablets as an oral dosage form. Tablets remain one of the most preferred forms of medication because they are easy to administer, cost-effective to produce, and have long shelf-lives. The increasing demand for chronic disease management, especially for conditions like hypertension and diabetes, is expected to drive the growth of this segment.

Additionally, advances in tablet technology, such as controlled-release formulations, are likely to further boost demand in this segment, as patients and healthcare providers seek more efficient treatment options.

Route of Administration Analysis

The oral segment grew at a substantial rate, generating a revenue portion of 57.5% as more patients prefer non-invasive drug delivery methods. Oral administration remains the most popular route due to its ease of use and patient compliance. The rising prevalence of chronic diseases, such as diabetes and cardiovascular conditions, is likely to drive demand for oral medications, as they are convenient for long-term treatment regimens.

Furthermore, innovations in oral drug formulations, including improved bioavailability and extended-release properties, are anticipated to increase the attractiveness of oral medications, supporting the growth of this segment.

Therapy Area Analysis

The cardiovascular diseases segment had a tremendous growth rate, with a revenue share of 47.3% owing to the increasing global prevalence of heart-related conditions. As the world’s population ages and lifestyle diseases become more prevalent, the demand for cardiovascular drugs will continue to rise.

Advances in drug formulations and the development of new treatments targeting specific cardiovascular conditions, such as hypertension and heart failure, are likely to drive market growth. Additionally, the growing focus on preventative care and improved patient outcomes is expected to contribute to the demand for cardiovascular medications, supporting the expansion of this segment.

Age Group Analysis

The adults segment grew at a substantial rate, generating a revenue portion of 54.5% as the adult population worldwide increases, particularly in developed countries. The rising incidence of lifestyle-related diseases, such as diabetes, obesity, and hypertension, is expected to drive the demand for pharmaceutical products aimed at adults.

Additionally, as adults are the largest consumer group for chronic disease management medications, the demand for pharmaceutical products designed for this demographic is likely to rise. The aging adult population, with increasing healthcare needs, will further support the growth of this segment within the pharmaceutical manufacturing market.

Key Market Segments

By Product Type

- Biologics & Biosimilars

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapy

- Others

- Conventional Drugs

By Drug Development

- In-house

- Outsource

By Formulation

- Tablets

- Suspensions

- Sprays

- Powders

- Injectable

- Capsules

- Others

By Route of Administration

- Oral

- Topical

- Parenteral

- Inhalations

- Others

By Therapy Area

- Cardiovascular Diseases

- Respiratory Diseases

- Pain

- Diabetes

- Cancer

- Other

By Age Group

- Children & Adolescents

- Adults

- Geriatric

Drivers

Increasing Demand for Biologics is Driving the Market

The pharmaceutical industry continues to experience strong growth in biologic drug production, significantly driving the market. In 2023, the FDA approved 12 new biologic license applications, representing 40% of all novel drug approvals that year. This shift toward complex therapies, including monoclonal antibodies and gene therapies, requires specialized manufacturing infrastructure.

Major companies, such as Roche, reported their biologics portfolio generated US$49 billion in 2023, marking a 9% annual growth. To support this demand, companies are investing heavily in new bioprocessing facilities. The US government’s Biosimilar Action Plan further accelerates this expansion by promoting competition in the biologics market, which ultimately lowers costs and increases access. Additionally, biologics manufacturing jobs grew 15% faster than traditional pharmaceutical roles in 2023, reflecting the industry’s focus on this high-growth segment.

Restraints

Stringent Regulatory Requirements are Restraining the Market

The growing complexity of biologics has led to increased regulatory scrutiny, presenting a significant restraint for the market. Pharmaceutical manufacturers face mounting compliance burdens due to evolving quality standards and manufacturing regulations. In 2023, the FDA issued 72 warning letters to drug facilities, a 15% increase from the previous year, with 25% of these targeting mid-sized companies for manufacturing quality control violations.

These stringent regulatory requirements create substantial barriers to entry and slow the time-to-market for new therapies. The costs associated with upgrading facilities to meet current good manufacturing practices (CGMP) often exceed US$50 million, adding financial strain. Similarly, the European Medicines Agency (EMA) increased inspection activity by 20% in 2023, with 8% of applications rejected due to production concerns. These challenges highlight the operational difficulties faced by manufacturers striving to meet regulatory demands.

Opportunities

Emerging Markets Expansion is Creating Growth Opportunities

Developing economies present substantial growth opportunities for pharmaceutical manufacturers, driving expansion in the global market. For example, India’s pharmaceutical exports reached US$ 27 billion in 2023, and the country plans to develop new bulk drug manufacturing parks to support further growth. China’s domestic pharmaceutical market grew 7% in 2023, with local manufacturers supplying 80% of the country’s pharmaceutical needs, showing the potential for local production to meet domestic demand.

Additionally, the African Continental Free Trade Area agreement aims to boost regional drug production capacity by 60% before 2030. Multinational pharmaceutical companies are responding to these emerging market opportunities, with Pfizer investing US$ 500 million in a new manufacturing facility in Saudi Arabia in 2023. These investments demonstrate the growing importance of expanding manufacturing capabilities in emerging markets, where demand for pharmaceutical products continues to rise.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors have a significant impact on the pharmaceutical manufacturing market, influencing both production costs and global trade dynamics. Rising inflation has increased the cost of raw materials, particularly active pharmaceutical ingredients (APIs), with prices climbing 15-20% since 2022.

Geopolitical tensions, such as the ongoing trade disputes between the US and China, have disrupted supply chains, causing delays of 3-6 months for critical manufacturing equipment. However, government policies like the US CHIPS and Science Act are providing funding to strengthen domestic production capabilities, helping mitigate some of these challenges.

Additionally, new trade agreements are opening up export opportunities in fast-growing markets across Asia and Africa, further supporting market expansion. While currency fluctuations pose challenges for global operations, the essential nature of medicines ensures a stable long-term demand. Manufacturers are responding by investing in automation and advanced process technologies, which improve efficiency and reduce operational costs, ensuring that the pharmaceutical manufacturing sector remains resilient and continues to expand despite external challenges.

Latest Trends

Adoption of Continuous Manufacturing is a Recent Trend

A notable recent trend in the pharmaceutical industry is the rapid adoption of continuous manufacturing methods to improve efficiency and reduce costs. In 2023, the FDA approved five new drugs produced using continuous manufacturing, doubling the number from 2022. This shift is driven by the need for faster production times and cost reductions.

Johnson & Johnson reported a 30% reduction in production times and 20% cost savings at its continuous manufacturing sites. The growing adoption of continuous manufacturing is also reflected in equipment suppliers, who saw a 25% increase in sales of continuous processing systems in 2023. The FDA’s 2023 guidance encourages this transition, highlighting its potential to improve drug quality and supply chain resilience. Although continuous manufacturing still represents a minority of production, it is rapidly gaining acceptance across the industry due to its efficiency and cost-effectiveness.

Analysis

North America is leading the Pharmaceutical Manufacturing Market

North America dominated the market with the highest revenue share of 42.4% owing to regulatory approvals and strategic government investments. The US Food and Drug Administration (FDA) approved 55 novel drugs in 2023, representing a 15% increase from the previous year. According to the US Department of Health and Human Services, domestic pharmaceutical production facilities expanded their capacity by 12% during 2023. The US Department of Commerce reported a 9% increase in pharmaceutical exports in 2023 compared to 2022 levels.

Canada’s Patented Medicine Prices Review Board documented a 22% rise in domestic production of patented medicines in 2023. These developments were supported by the US government’s allocation of US$2 billion for advanced medicine manufacturing technologies through the CHIPS and Science Act. The growth was particularly notable in biologic drugs, with US manufacturing capacity for these therapies increasing by 18% between 2022 and 2023. These factors contributed to the overall growth of the pharmaceutical manufacturing sector in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow at the fastest CAGR due to government initiatives and expanding pharmaceutical capabilities. In 2023, China’s National Medical Products Administration approved 42% more new drug applications than in 2022. India’s pharmaceutical output rose by 17%, driven by trade incentives. Japan’s Ministry of Health recorded a 25% increase in biopharmaceutical facility registrations. South Korea saw a 38% rise in biologic product approvals. Australia’s Therapeutic Goods Administration expects a 30% surge in manufacturing site approvals in 2024.

These developments highlight strong growth potential in pharmaceutical production, especially in advanced therapies and vaccines. Governments are investing heavily to support this expansion. India alone allocated $3.2 billion for production incentives in 2023. These investments strengthen the region’s pharmaceutical manufacturing market. The rise in regulatory approvals, facility expansions, and government support positions Asia Pacific as a key player in global pharmaceutical production. The region is expected to witness continued growth in manufacturing and innovation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the pharmaceutical manufacturing market focus on technological innovation, cost optimization, and expanding production capacities to drive growth. They invest in advanced manufacturing techniques such as continuous manufacturing, automation, and 3D printing to increase efficiency and reduce costs. Companies also focus on regulatory compliance and ensuring high-quality standards to meet the growing global demand for pharmaceuticals.

Strategic partnerships with research institutions, contract manufacturers, and healthcare providers help them expand their market reach. Additionally, they target emerging markets with rising healthcare needs, offering more affordable and accessible pharmaceutical solutions. Pfizer Inc., headquartered in New York City, is one of the world’s leading biopharmaceutical companies.

Pfizer develops, manufactures, and distributes a wide range of medicines and vaccines across various therapeutic areas, including oncology, cardiology, and immunology. The company focuses on innovation by investing heavily in R&D and advanced manufacturing technologies to enhance production efficiency. Pfizer’s strategic partnerships with healthcare organizations and its global manufacturing capabilities strengthen its position in the pharmaceutical manufacturing market. With a strong presence in both developed and emerging markets, Pfizer continues to lead in global pharmaceutical production and distribution.

Top Key Players in the Pharmaceutical Manufacturing Market

- Sanofi SA

- Samsung Biologics

- Pfizer, Inc

- Novartis AG

- MilliporeSigma

- Johnson & Johnson

- Eli Lilly and Company

- AstraZeneca

Recent Developments

- In January 2024, Samsung Biologics unveiled its business plan for the year, outlining efforts to strengthen its biopharmaceutical production. The company is focusing on scaling up manufacturing capabilities to meet the increasing need for high-quality medicines worldwide.

- In May 2023, MilliporeSigma, a subsidiary of Merck KGaA, expanded its development and manufacturing operations in the US. This expansion will enhance its capacity to produce complex antibody-drug conjugates and highly potent ingredients, solidifying its position as a leader in pharmaceutical manufacturing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 582.1 billion |

| Forecast Revenue (2034) | US$ 1199.7 billion |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Biologics & Biosimilars (Monoclonal Antibodies, Vaccines, Cell & Gene Therapy, and Others), Conventional Drugs), By Drug Development (In-house and Outsource), By Formulation (Tablets, Suspensions, Sprays, Powders, Injectable, Capsules, and Others), By Route of Administration (Oral, Topical, Parenteral, Inhalations, and Others), By Therapy Area (Cardiovascular Diseases, Respiratory Diseases, Pain, Diabetes, Cancer, and Other), By Age Group (Children & Adolescents, Adults, and Geriatric) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Sanofi SA, Samsung Biologics, Pfizer, Inc, Novartis AG, MilliporeSigma, Johnson & Johnson, Eli Lilly and Company, and AstraZeneca. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |