Quick Navigation

Report Overview

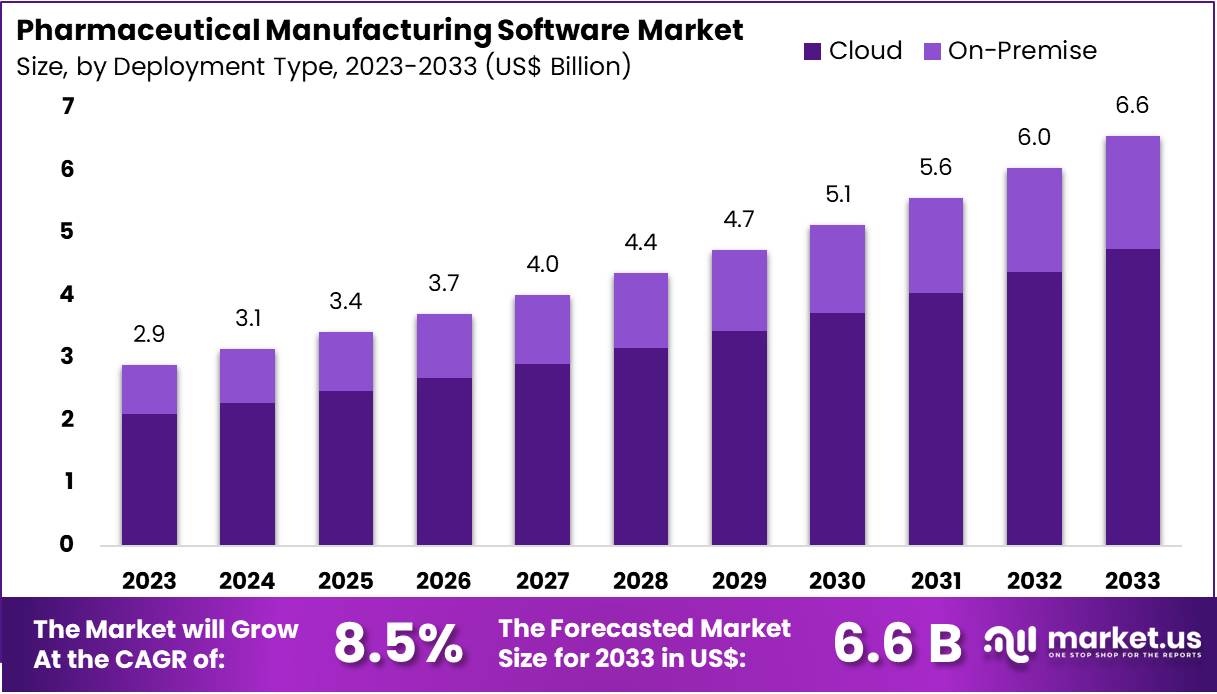

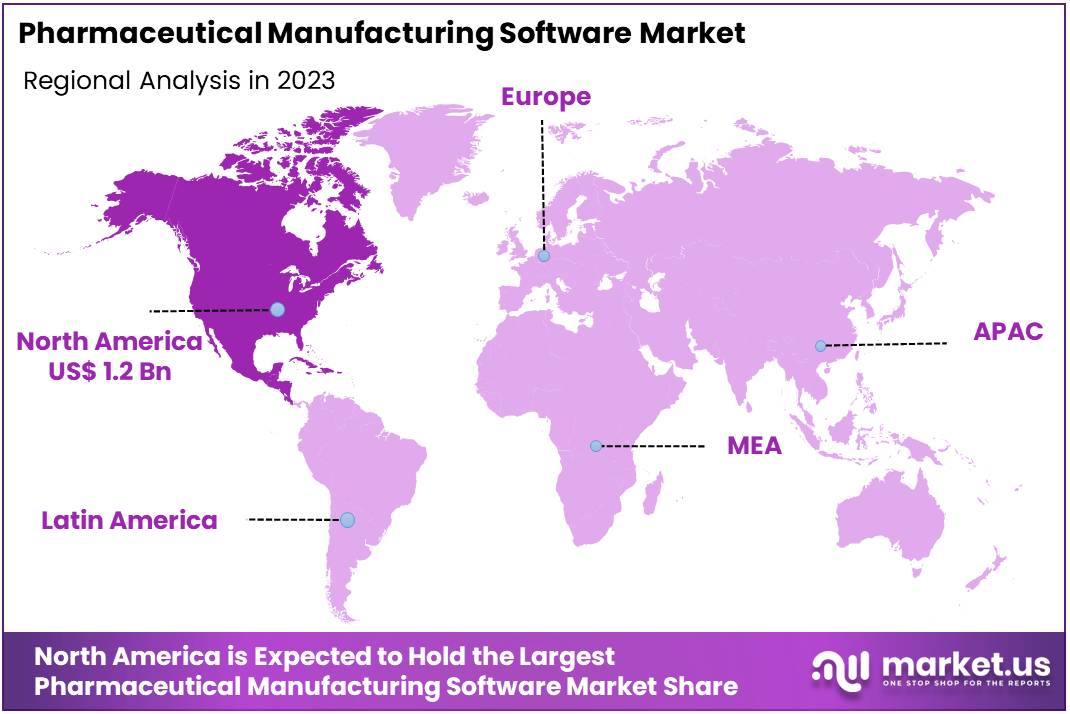

The Global Pharmaceutical Manufacturing Software Market size is expected to be worth around US$ 6.6 Billion by 2033, from US$ 2.9 Billion in 2023, growing at a CAGR of 8.5% during the forecast period from 2024 to 2033. North America held a dominant market position, capturing more than a 40.7% share and holds US$ 1.2 Billion market value for the year.

Growing demand for efficiency, regulatory compliance, and product quality in pharmaceutical manufacturing is driving the expansion of the pharmaceutical manufacturing software market. These software solutions are critical in optimizing production processes, ensuring strict adherence to regulatory standards, and improving operational efficiency across the pharmaceutical supply chain.

The increasing complexity of drug manufacturing, coupled with rising pressure to reduce costs, has spurred widespread adoption of advanced software platforms. Pharmaceutical manufacturers leverage these tools for tasks such as batch tracking, inventory management, production scheduling, and quality control, significantly reducing human error and enhancing traceability.

In March 2022, Aizon, a leader in enterprise AI software, partnered with Aggity, a company specializing in business digital transformation, to accelerate the digitalization of manufacturing operations for major pharmaceutical and biotech firms. This collaboration reflects a growing trend toward integrating artificial intelligence (AI) and machine learning (ML) technologies into pharmaceutical manufacturing software to enable real-time monitoring, predictive maintenance, and more precise quality assurance.

Additionally, cloud-based solutions are gaining traction, offering scalability, data security, and seamless integration with other enterprise systems. These trends highlight the increasing role of technology in transforming the pharmaceutical manufacturing process, presenting significant opportunities for market growth and innovation. As pharmaceutical companies strive for greater agility and faster time-to-market, the demand for advanced manufacturing software solutions will continue to rise.

Key Takeaways

- In 2023, the market for Pharmaceutical Manufacturing Software generated a revenue of US$ 2.9 billion, with a CAGR of 8.5%, and is expected to reach US$ 6.6 billion by the year 2033.

- The deployment type segment is divided into on-premise and cloud, with cloud taking the lead in 2023 with a market share of 72.5%.

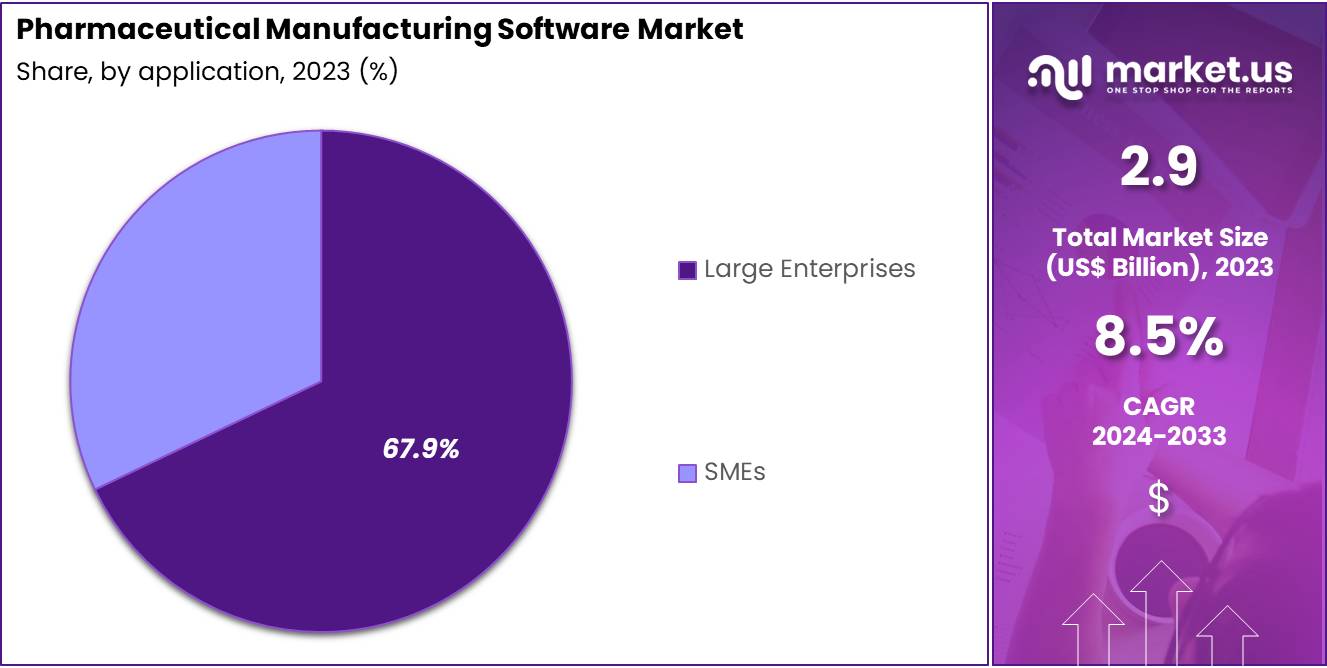

- Considering application, the market is divided into large enterprises and SMEs. Among these, large enterprises held a significant share of 67.9%.

- Furthermore, concerning the end-user segment, the biopharmaceutical companies sector stands out as the dominant player, holding the largest revenue share of 42.3% in the Pharmaceutical Manufacturing Software market.

- North America led the market by securing a market share of 40.7% in 2023.

Deployment Type Analysis

The cloud segment led in 2023, claiming a market share of 72.5% as more pharmaceutical companies embrace cloud-based solutions for enhanced scalability, flexibility, and cost-efficiency. Cloud-based deployment allows manufacturers to access real-time data, optimize production processes, and facilitate better collaboration across geographically dispersed teams.

The increasing adoption of digital transformation strategies, coupled with the demand for seamless integration with existing enterprise systems, is anticipated to drive the growth of cloud deployment. Cloud solutions also provide pharmaceutical companies with the ability to scale their operations quickly, enhance data security, and improve regulatory compliance, all of which are critical in the highly regulated pharmaceutical industry. As the industry shifts towards more agile and responsive operations, the cloud segment is likely to see widespread adoption across various pharmaceutical manufacturing segments.

Application Analysis

The large enterprises held a significant share of 67.9% due to the increasing complexity and scale of operations within large pharmaceutical companies. These organizations face significant challenges related to compliance, production efficiency, and data management, all of which are well-addressed by advanced pharmaceutical manufacturing software.

Large enterprises are expected to invest in integrated software systems that support the automation of key processes, from supply chain management to quality control. The demand for solutions that can handle high volumes of data, enhance traceability, and streamline manufacturing processes is anticipated to rise as pharmaceutical companies strive for greater operational efficiency and regulatory adherence. Additionally, large enterprises are more likely to adopt cutting-edge technologies like AI and IoT, further contributing to the growth of this segment.

End-user Analysis

The biopharmaceutical companies segment had a tremendous growth rate, with a revenue share of 42.3% owing to the increasing demand for biologics and the complex manufacturing processes involved in their production. Biopharmaceutical companies face unique challenges in ensuring the consistency, quality, and safety of their products, which pharmaceutical manufacturing software is designed to address.

These software solutions provide biopharmaceutical firms with tools to manage batch production, track raw materials, ensure regulatory compliance, and facilitate risk management. The growing focus on personalized medicine, the expansion of biologic therapies, and the increasing need for regulatory compliance in the production of biologics are expected to drive the adoption of pharmaceutical manufacturing software among biopharmaceutical companies. As the biopharma industry continues to evolve, software solutions will play a pivotal role in ensuring efficient and compliant manufacturing processes.

Key Market Segments

By Deployment Type

- On-premise

- cloud

By Application

- Large Enterprises

- SMEs

By End-User

- Medical Device Companies

- Biopharmaceutical Companies

- Academic Research Institutions

- Contract Research Organizations

- Others

Drivers

Rising Healthcare Expenditure Driving the Market

Rising healthcare expenditure plays a pivotal role in the growth of the pharmaceutical manufacturing solutions market. According to the World Health Organization (WHO), global healthcare spending reached US$ 8.5 trillion in 2022 and is projected to increase to 9.8% of global GDP by 2029. This rise in spending is largely attributed to investments in digital infrastructure, including advanced technologies within the pharmaceutical manufacturing sector.

As governments and private entities allocate more funds to modernize healthcare systems, pharmaceutical companies are expected to adopt innovative technologies to improve efficiency, ensure regulatory compliance, and enhance production capabilities. The need for streamlined operations and cost reduction in manufacturing processes is anticipated to boost the adoption of digital solutions. As healthcare expenditure continues to grow, the demand for automation and advanced manufacturing systems will likely drive further market expansion.

Restraints

High Treatment Costs Restraining the Market

High treatment costs present a significant challenge to the adoption of advanced manufacturing systems in the pharmaceutical industry. The capital-intensive nature of software deployment, including installation, training, and integration, can pose financial barriers, particularly for smaller companies and those in emerging markets.

Additionally, ongoing maintenance costs and the need for compliance with stringent regulatory standards further increase the financial burden on manufacturers. This high initial investment required for new solutions is expected to limit adoption in regions with constrained budgets. The combination of upfront costs and operational expenses hampers the widespread implementation of innovative technologies, which could slow market growth in certain segments and regions.

Opportunities

Surge in Launch of New and Advanced Solutions as an Opportunity

The rise in the launch of new, advanced solutions offers a considerable opportunity for the pharmaceutical manufacturing market. For example, Aizon introduced a new AI-driven asset tracking system in January 2022, designed specifically for the biotech and pharmaceutical sectors. This solution, which operates on Aizon’s SaaS platform and complies with GxP standards, allows real-time monitoring of equipment conditions, enabling predictive maintenance and optimization of asset performance.

Such innovations are expected to drive demand by enhancing operational efficiency, ensuring better regulatory compliance, and reducing costs. The growing focus on automation, quality control, and predictive analytics is likely to encourage more manufacturers to adopt these new technologies, spurring further market growth and creating new opportunities for software providers in the sector.

Impact of Macroeconomic / Geopolitical Factors

The pharmaceutical manufacturing software market is greatly influenced by macroeconomic and geopolitical factors, which pose both opportunities and challenges. Economic downturns or inflation may lead to reduced capital spending in the healthcare and pharmaceutical sectors. This reduction can delay investments in advanced software solutions that are crucial for enhancing operational efficiency.

On the other hand, during periods of economic stability and growth, companies often feel encouraged to adopt cutting-edge technologies. These technologies help streamline operations and boost manufacturing efficiency. Geopolitical issues like trade tensions, tariffs, and regulatory changes can disrupt global supply chains, affecting the availability of essential software components.

Despite these challenges, the demand for personalized medicine and a stronger focus on regulatory compliance continue to drive the adoption of pharmaceutical manufacturing solutions. The ongoing digital transformation in the healthcare sector and increasing regulatory demands create a positive environment for the market’s expansion in the long term. This trend suggests a resilient growth trajectory despite the potential hurdles.

Trends

Rising Surge in Collaborations and Partnerships Driving the Market

The increasing number of collaborations and partnerships in the pharmaceutical manufacturing software market is expected to significantly drive growth in the coming years. High levels of collaboration between software providers, pharmaceutical companies, and technology experts have fostered the development of more integrated and efficient manufacturing solutions.

In June 2023, Korber launched the PAS-X K.ME-IN partner program to enhance biometric authentication speeds in pharmaceutical manufacturing, providing a seamless, ready-to-use interface for Werum PAS-X MES customers. This move reflects the rising trend of collaborations aimed at advancing technological innovation and improving operational efficiency in pharmaceutical production.

Such partnerships are anticipated to accelerate the deployment of advanced software solutions, streamlining regulatory compliance, improving manufacturing processes, and enhancing overall production quality. The continued focus on such collaborations will likely contribute to the long-term growth of the market.

Regional Analysis

North America is leading the Pharmaceutical Manufacturing Software Market

North America dominated the market with the highest revenue share of 40.7% owing to advancements in technology and increasing demand for more efficient and streamlined drug production processes. The rise of digital transformation across the pharmaceutical sector has significantly contributed to this growth, as companies seek to optimize production, improve regulatory compliance, and reduce operational costs. One notable example of this trend is the partnership formed in December 2021 between Amazon Web Services (AWS) and Pfizer.

This collaboration aims to develop cloud-based solutions to revolutionize drug creation, production, and distribution, with a focus on enhancing clinical trial processes. The adoption of advanced pharmaceutical manufacturing software solutions, which integrate technologies such as artificial intelligence (AI), big data analytics, and automation, has become increasingly prevalent in the region.

These innovations enable pharmaceutical companies to streamline operations, ensure quality control, and accelerate time-to-market for new drugs. Additionally, the growing complexity of pharmaceutical supply chains, coupled with regulatory pressures, has further driven the demand for software solutions that improve visibility, traceability, and compliance across the manufacturing process.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific region is poised for rapid growth in the pharmaceutical manufacturing software market, driven by its expanding pharmaceutical industry and increased investments in digital technologies. Notably, China and India are leading this surge due to their burgeoning pharmaceutical sectors. These countries are actively adopting advanced manufacturing solutions to modernize their production facilities and boost efficiency, setting a robust pace for regional growth.

In March 2022, a significant collaboration was announced between Triastek, Inc. and Siemens Ltd. This partnership focuses on advancing digital technologies in pharmaceutical manufacturing. By combining Triastek’s expertise in 3D printing and digital pharmaceutical technologies with Siemens’ capabilities in automation and digitalization, they are setting new benchmarks for innovation in the industry.

This strategic alliance is reflective of a broader trend in the Asia Pacific region toward integrating cutting-edge technologies in drug development and production processes. The demand for software solutions that can optimize production, enhance drug quality, and comply with regulatory standards is increasing. Supported by government initiatives and a growing emphasis on digital healthcare transformation, the pharmaceutical manufacturing software market in Asia Pacific is expected to experience significant expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The pharmaceutical manufacturing software market is marked by a dynamic competition among key players, who are consistently innovating and integrating with emerging technologies. These companies prioritize continuous innovation to enhance their competitive edge. By investing in automation, data analytics, and cloud-based solutions, they aim to optimize manufacturing processes, bolster regulatory compliance, and guarantee product quality.

Strategic partnerships are vital for these companies. By collaborating with pharmaceutical firms and contract manufacturers, they expand their market reach and enhance their product offerings. These alliances are crucial for tapping into new opportunities and leveraging mutual strengths to foster growth in the sector.

Moreover, there is a significant focus on improving user interfaces and scalability of the software. This ensures it caters effectively to both large-scale producers and smaller pharmaceutical entities. Ensuring robust cybersecurity and data privacy is also a priority. These measures are essential to meet the stringent standards and regulations of the industry, securing both data integrity and customer trust.

One key player in the market is Dassault Systemes, a global leader in software solutions for various industries, including pharmaceutical manufacturing. Dassault’s growth strategy revolves around offering end-to-end solutions through its “BIOVIA” software suite, which integrates digital technologies like AI, cloud computing, and big data analytics to streamline drug development and manufacturing processes.

The company focuses on helping pharmaceutical companies improve operational efficiency, accelerate time-to-market, and ensure compliance with regulatory requirements. Dassault Systèmes also partners with pharmaceutical firms to co-develop tailored solutions, further driving adoption and expanding its market presence.

Top Key Players in the Pharmaceutical Manufacturing Software Market

- Wipro

- TATA

- Dassault Systemes

- IBM

- Honeywell

- Cognizant

- Capgemini

- Apple

- Accenture

Industrial Advantages and Opportunities For Market Players

Pharmaceutical manufacturing software offers critical advantages to industry leaders. One of the primary benefits is ensuring compliance with stringent regulatory standards, such as those from the FDA and GMP. This reduces the risk of costly legal issues and product recalls. Additionally, the software enhances productivity by automating complex processes, which minimizes manual labor and errors. This increase in efficiency is crucial for maintaining competitive advantage in the fast-paced pharmaceutical sector.

Another significant advantage is the improvement in quality control. The software supports rigorous quality assurance protocols and batch records management, leading to fewer deviations and inconsistencies. This results in higher product quality, which is essential for consumer trust and regulatory approval. Moreover, real-time data access provided by these systems enables timely decision-making and faster response to operational issues, further boosting production efficiency.

The software also optimizes the supply chain from raw material procurement to product distribution. This streamlining enhances inventory control and reduces lead times, which are vital for meeting market demands promptly. Additionally, operational costs are reduced through optimized resource utilization and minimized waste, thanks to more accurate demand forecasting and production planning.

Finally, pharmaceutical manufacturing software enhances security and supports scalability. It protects sensitive data with robust security features, crucial in an industry where intellectual property and patient data are paramount. Furthermore, it facilitates the scaling of production operations, allowing companies to expand into new markets or adjust to changing demands without compromising quality or compliance. These tools not only streamline processes but also contribute significantly to a company’s bottom line and market position.

Recent Developments

- In May 2021, Mankind Pharma embarked on a digital transformation by partnering with Accenture. They aimed to introduce a data-driven cloud platform, positioning Mankind Pharma to become an intelligent enterprise. This strategic move is intended to boost business agility, enhance operational efficiency, and improve overall performance.

- In September 2021, Honeywell completed the acquisition of Performix Inc., a company specializing in manufacturing execution system (MES) software for the pharmaceutical and biotech sectors. This acquisition is part of Honeywell’s strategy to develop a comprehensive software platform for life sciences companies, focusing on speeding up compliance and operational efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 2.9 billion |

| Forecast Revenue (2033) | US$ 6.6 billion |

| CAGR (2024-2033) | 8.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment Type (On-premise and cloud), By Application (Large Enterprises and SMEs), By End-user (Medical Device Companies, Biopharmaceutical Companies, Academic Research Institutions, Contract Research Organizations, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Wipro, TATA, Dassault Systemes, IBM, Honeywell, Cognizant, Capgemini, Apple, and Accenture |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |