Quick Navigation

Report Overview

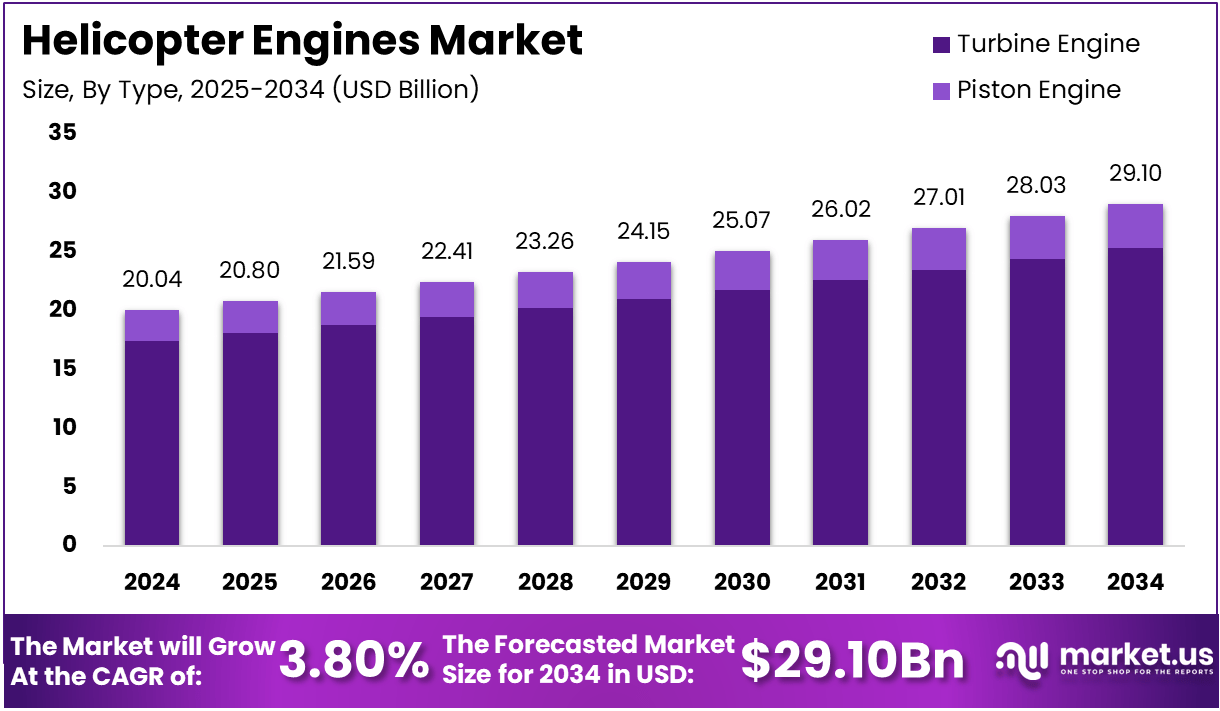

The Global Helicopter Engines Market size is expected to be worth around USD 48.36 Billion By 2034, from USD 20.04 Billion in 2024, growing at a CAGR of 3.80% during the forecast period from 2025 to 2034.

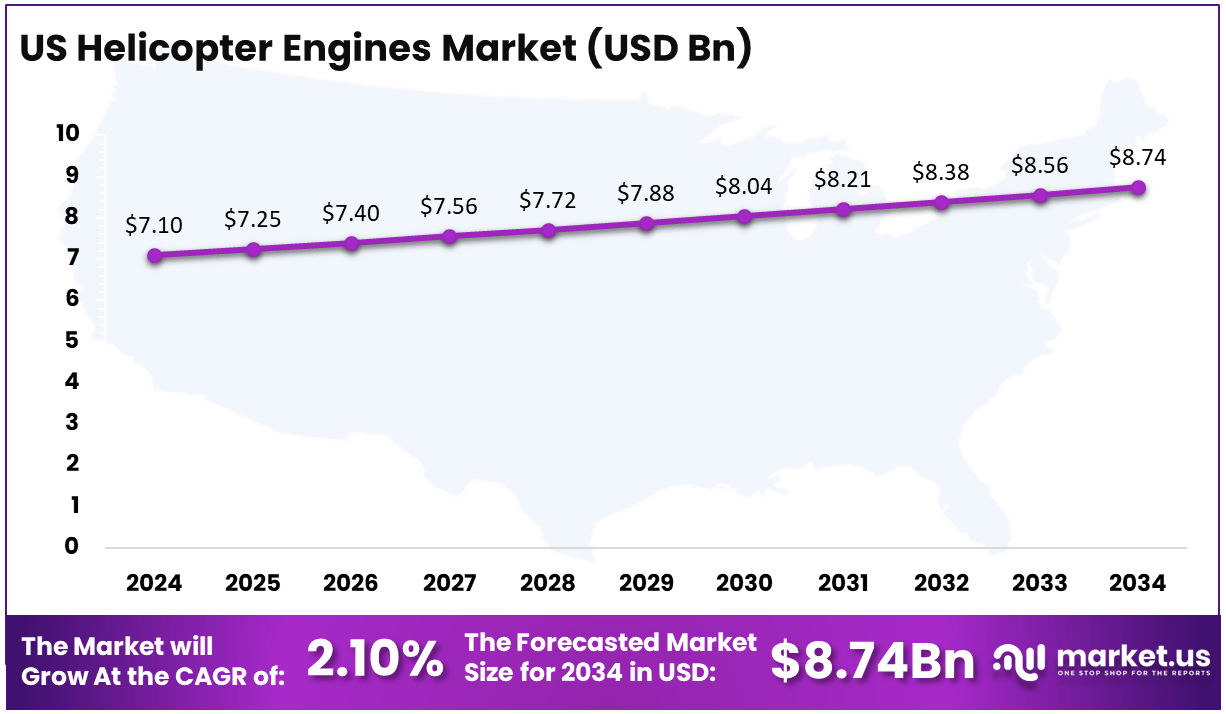

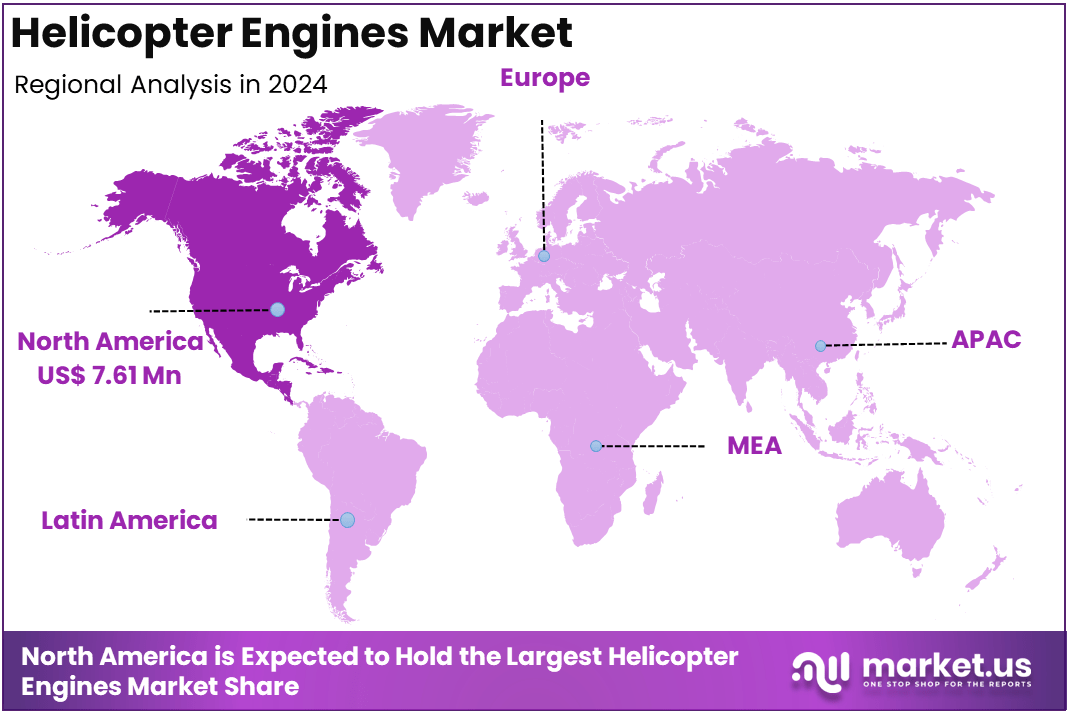

In 2024, North America held a dominant market position, capturing more than a 38% share, holding USD 7.61 Billion in revenue. Further, In North America, The United States dominates the market by USD 7.1 Billion, steadily holding a strong position with a CAGR of 2.1%.

Helicopter engines are the heart of rotary-wing aircraft, providing the necessary power for flight. Unlike fixed-wing aircraft engines, helicopter engines are designed to produce continuous, reliable thrust that allows helicopters to hover, take off, and land vertically.

These engines can be either turboshaft or piston engines, with the former being more common in modern helicopters due to their high efficiency and reliability at varying altitudes. Turboshaft engines convert the energy produced by burning fuel into mechanical power, which is then used to drive the helicopter’s main rotor.

On the other hand, piston engines are generally found in smaller helicopters and are simpler in design, often used for recreational or training purposes. The choice of engine depends on factors like the helicopter’s size, intended use, and performance requirements. Today’s helicopter engines are becoming more efficient, with advancements focused on improving fuel consumption, reducing emissions, and enhancing operational lifespan.

The helicopter engines market refers to the global industry that designs, manufactures, and services the engines that power helicopters. The market is growing steadily, driven by increasing demand for both military and civilian helicopters across sectors like emergency medical services (EMS), law enforcement, oil and gas, and tourism.

Additionally, the rise in military spending, particularly in regions such as North America, Asia-Pacific, and the Middle East, is fueling the demand for high-performance helicopter engines. The global market is also benefiting from the ongoing adoption of newer, more fuel-efficient engines, as well as the increasing need for lightweight, high-performance engines in various civilian applications.

The major driving factors behind the growth of the helicopter engine market include the expansion of the global helicopter fleet, military modernization programs, and increased demand for air mobility solutions. As various industries, including oil and gas, search and rescue, and tourism, rely heavily on helicopters, the demand for reliable and high-performance engines continues to rise.

Moreover, as defense budgets increase worldwide, particularly in regions like the Middle East and Asia-Pacific, the demand for military helicopters with advanced engines is also growing. The rise in urban air mobility (UAM) solutions, such as air taxis and drones, is another emerging factor pushing the demand for efficient and cost-effective helicopter engines. Additionally, advances in engine technology that focus on improving fuel efficiency, reducing emissions, and increasing the operational lifespan of engines are also contributing to the market’s expansion.

Key Statistics

Engine Types and Applications:

- Turboshaft engines dominated the market in 2023 due to their efficiency and performance in helicopter applications.

- Turbine-engine helicopters have surpassed piston engines in power-to-weight ratios.

- Engines with 1000-3000 HP are typically installed in larger helicopters for heavy-lift operations, search and rescue, military applications, and offshore transportation.

- Reciprocating engines are often used in smaller, practice helicopters because they are low-cost and simple to operate.

Helicopter Usage:

- As of December 2024, armed forces worldwide operated 947 Boeing CH-47 Chinook helicopters.

- As of December 2024, armed forces worldwide operated 117 Bell 407 helicopters.

- Light helicopters are used for aerial surveillance, law enforcement, emergency medical services (EMS), search and rescue missions, and private transportation.

- Heavy helicopters are commonly used for offshore oil rig support, heavy cargo transport, troop deployment, and firefighting operations.

Contracts and Procurement:

- In December 2023, Boeing secured a contract to produce 18 CH-47F Block I Chinooks for South Korea and one for Spain, valued at up to USD 793 million.

- Honeywell was awarded a four-year contract worth USD 476 million for new production and spare T55-GA-714A engines for the U.S. Army’s CH-47 Chinook helicopters.

Key Takeaways

- Market Size and Growth: The global helicopter engines market is valued at USD 20.04 billion in 2024 and is projected to reach USD 48.36 billion by 2034, growing at a CAGR of 3.80%.

- Market Segmentation by Type: The turbine engine segment holds a dominant share of 87%, reflecting its widespread use in modern helicopters due to its higher efficiency and reliability.

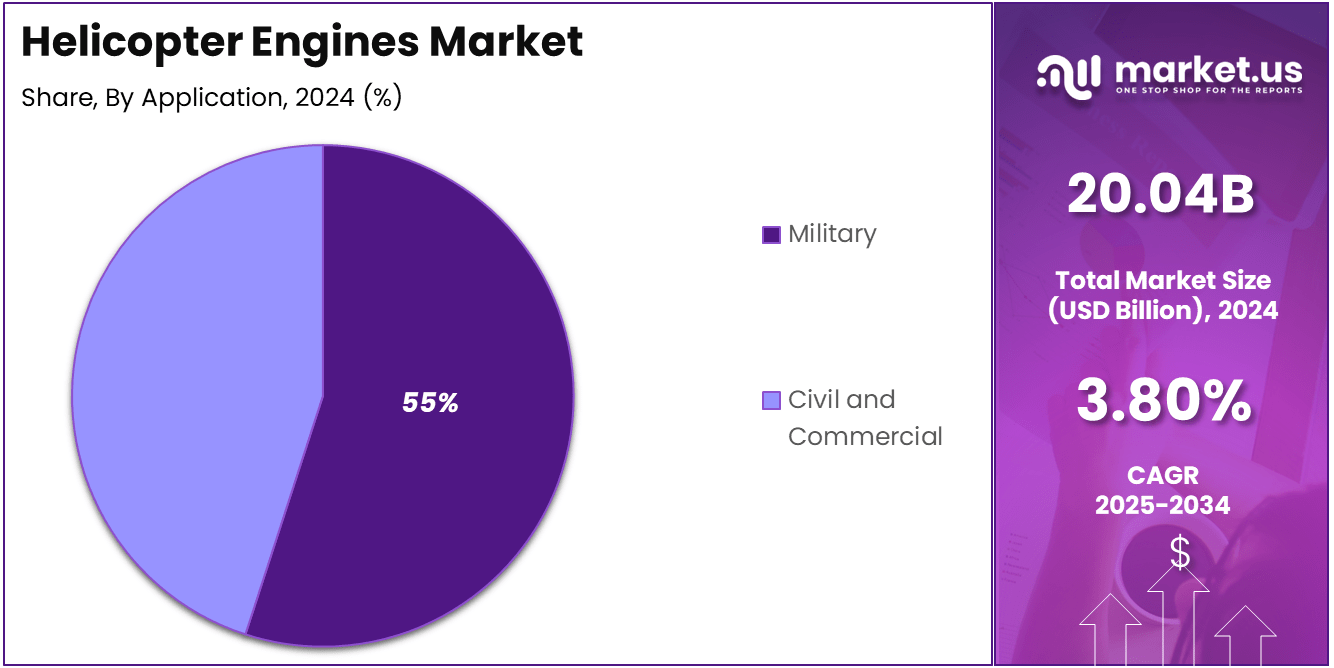

- Market Segmentation by Application: The military application segment leads with a share of 55%, driven by ongoing defense modernization and the growing need for advanced military rotorcraft worldwide.

- Market Segmentation by Sale: The OEM (Original Equipment Manufacturer) sales segment represents 68% of the market, indicating strong demand for new engines as helicopter fleets expand and modernize.

- Regional Analysis – North America: North America holds a significant share of 38%, with the US accounting for USD 7.1 billion of the market, growing at a CAGR of 2.1%. This is largely due to continued military investment, EMS demand, and commercial applications in the region.

- Long-Term Outlook: The helicopter engine market is poised for sustained growth, with technological advancements in fuel efficiency, hybrid-electric systems, and military upgrades driving demand across multiple sectors.

Regional Analysis

US Helicopter Engines Market Size

In 2024, North America holds a dominant share of the global helicopter engines market, accounting for 3.80% of the total market value. The region is primarily driven by the United States, which alone contributes USD 7.1 billion to the market. This dominance can be attributed to the continued investments in military modernization, the expansion of commercial helicopter fleets, and the growing demand for emergency medical services (EMS).

The United States has one of the largest helicopter fleets globally, serving a variety of sectors, including defense, law enforcement, search and rescue, and oil and gas. Moreover, the country is witnessing increasing demand for advanced helicopter engines that focus on fuel efficiency, reliability, and eco-friendly technologies.

The military sector in the U.S. plays a crucial role in shaping the demand for helicopter engines. As defense budgets remain strong, there is a steady need for high-performance engines in modern military helicopters, including those used for surveillance, troop transport, and combat operations.

Furthermore, with the rising focus on urban air mobility (UAM) and advancements in electric propulsion systems, the U.S. is positioning itself as a leader in developing new technologies for both civilian and military aviation. With a CAGR of 2.1%, the U.S. helicopter engine market is poised to continue growing steadily, supported by technological advancements and a strong industrial base.

North America Helicopter Engines Market Size

In 2024, North America held a dominant market position in the global helicopter engines market, capturing more than 3.80% of the total market share and generating USD 7.61 billion in revenue. This region’s leadership can be attributed to the significant military and commercial aviation sectors in countries like the United States and Canada.

North America’s robust defense budgets and large helicopter fleets, particularly in military, law enforcement, and emergency medical services (EMS), drive the demand for high-performance helicopter engines. The U.S. alone accounts for a major portion of this market, with a steady demand for advanced and fuel-efficient turbine engines used in military rotorcraft, commercial helicopters, and search and rescue operations.

The region also benefits from continuous investment in helicopter fleet modernization and the integration of next-generation technologies, such as smart engines and hybrid-electric systems. North American manufacturers are leaders in developing these advanced systems, which provide operational efficiencies and environmental benefits. Furthermore, the demand for urban air mobility (UAM) solutions, including air taxis and drones, is contributing to market growth, as new rotorcraft technologies require specialized, innovative engines.

Additionally, the U.S. government’s focus on upgrading its military infrastructure, particularly under initiatives like the Future Vertical Lift (FVL) program, ensures a sustained demand for military helicopters and their engines over the next decade. This, coupled with a well-established aerospace manufacturing base, gives North America a strong foothold in the global helicopter engines market.

Looking forward, North America is expected to maintain a steady growth trajectory, driven by ongoing technological advancements, particularly in fuel-efficient and environmentally friendly engines, alongside an expanding civilian helicopter fleet. As the region continues to invest in air mobility and rotorcraft advancements, its position as the market leader remains solid, further consolidating its dominance in the global helicopter engine market.

By Type

In 2024, the turbine engine segment held a dominant market position, capturing more than 87% of the total helicopter engine market. This significant share is driven by the superior performance and reliability of turbine engines, especially in commercial and military helicopters.

Turbine engines are known for their ability to produce higher power-to-weight ratios, making them ideal for modern helicopters that require both power and efficiency for a wide range of operations, from search and rescue missions to combat operations and transportation. Their ability to operate at high altitudes, fuel efficiency, and longer lifespan compared to piston engines make them the preferred choice in the helicopter industry.

Turbine engines are especially well-suited for military applications, where performance, durability, and efficiency are paramount. Additionally, the growth in the civil aviation sector, including emergency medical services (EMS) and oil and gas, has further contributed to the dominance of turbine engines, as they are capable of handling the heavy lifting and operational demands of larger commercial helicopters.

With advancements in turbine engine technologies, such as fuel efficiency improvements and low emissions designs, their market share is expected to continue growing, solidifying their leadership position in the global helicopter engines market.

By Application

In 2024, the military segment held a dominant market position in the helicopter engines market, capturing more than 55% of the total market share. This strong position is primarily driven by the ongoing demand for advanced helicopter engines in military applications, where performance, durability, and reliability are critical.

Modern military helicopters require engines that can support a wide range of operations, including combat missions, surveillance, transportation, and rescue operations in various environments and conditions. Military forces globally continue to prioritize the modernization of their rotorcraft fleets, which leads to a steady demand for high-performance engines, particularly turbine engines. These engines are favored for their ability to produce higher power output while maintaining fuel efficiency, making them ideal for the demanding needs of military helicopters.

Additionally, the military sector’s focus on next-generation technologies, such as stealth and vertical lift capabilities, further drives the need for more advanced engine systems. As defense budgets grow, particularly in regions like North America, Asia-Pacific, and the Middle East, the military segment will continue to be a key driver in the growth of the helicopter engines market.

By Sale

In 2024, the OEM (Original Equipment Manufacturer) segment held a dominant market position in the helicopter engines market, capturing more than 68% of the total market share. This strong market presence can be attributed to the continuous demand for new helicopters, particularly from the military, commercial, and civil aviation sectors.

OEM sales are driven by the need to equip new rotorcraft with cutting-edge, high-performance engines that meet modern operational requirements, including efficiency, reliability, and fuel economy. The growth in OEM sales is also fueled by helicopter fleet expansions and military modernization programs. As governments around the world invest in upgrading their defense and emergency services fleets, there is a steady demand for new engines that can support these more advanced rotorcraft models.

Additionally, the increasing focus on urban air mobility (UAM) and electric propulsion technologies further drives innovation and investment in OEM engine solutions. With helicopter manufacturers and engine suppliers working closely to design engines that cater to specific aircraft needs, the OEM segment is expected to maintain its dominant position in the market over the coming years.

Key Market Segments

By Type

- Piston Engine

- Turbine Engine

By Application

- Military

- Civil and Commercial

By Sale

- OEM

- Aftermarket

Driving Factors

Growing Demand for Military Helicopters

One of the key driving factors behind the growth of the helicopter engine market is the rising demand for military helicopters across the globe. Military forces worldwide continue to prioritize the modernization and expansion of their helicopter fleets, which require advanced and high-performance engines. These helicopters play a crucial role in various military operations, such as the transportation of troops and supplies, surveillance, combat missions, and search and rescue operations.

Military budgets are growing, especially in regions such as North America, Asia-Pacific, and the Middle East, where countries are enhancing their defense capabilities. For instance, programs like the Future Vertical Lift (FVL) in the U.S. are pushing the need for next-generation rotorcraft and engines that can provide higher efficiency, longer operational ranges, and better performance in diverse environments. The demand for turbine engines in military helicopters is particularly high due to their superior power-to-weight ratio, reliability, and efficiency.

In addition, military helicopter fleets are increasingly adopting advanced technologies that require specialized, high-performing engines. These technologies include vertical lift capabilities, stealth features, and hybrid-electric propulsion systems, all of which contribute to the demand for more innovative and efficient engine solutions. As defense spending continues to grow and military fleets expand, the helicopter engines market is poised for long-term growth.

Restraining Factor

High Maintenance Costs

One significant restraining factor for the helicopter engine market is the high maintenance and operational costs associated with these engines. Helicopter engines, especially turbine engines, require regular and often expensive maintenance to ensure optimal performance. Routine repairs, part replacements, and overhauls can significantly increase the total cost of ownership for both military and civilian operators.

For many organizations, especially in developing markets, the cost of maintaining and servicing these engines can be prohibitive. This is particularly true for smaller fleets or operators with limited budgets, such as those involved in EMS, law enforcement, or commercial applications.

Moreover, maintenance costs are compounded by the need for highly skilled personnel to carry out these complex services, further driving up expenses. While the demand for helicopters continues to grow, these high operating costs may deter smaller or less financially secure operators from investing in new helicopters or engines, limiting growth in certain market segments.

Growth Opportunities

Advancements in Hybrid and Electric Engines

A promising growth opportunity in the helicopter engines market is the development and adoption of hybrid and electric propulsion systems. With growing pressure to reduce carbon emissions and improve fuel efficiency in the aviation sector, hybrid-electric and fully electric engines are emerging as viable alternatives to traditional fuel-based turbine engines. This shift is particularly important in the civilian sector, where environmentally friendly solutions are becoming increasingly prioritized.

Hybrid engines, which combine traditional turbine engines with electric motors, offer significant advantages, including lower fuel consumption, reduced emissions, and improved operational efficiency. They are also expected to significantly reduce operating costs in the long run, making them appealing to commercial operators, especially in sectors like tourism and emergency services.

Additionally, electric helicopters are gaining traction in markets like urban air mobility (UAM) and small commuter aircraft. As technology continues to improve, fully electric helicopters may offer a clean and cost-effective alternative to traditional propulsion systems. Companies such as Vertical Aerospace and Joby Aviation are already making strides toward creating electric vertical take-off and landing (eVTOL) aircraft, which could revolutionize short-distance travel.

Challenging Factors

Stringent Regulatory Compliance

A major challenging factor for the helicopter engine market is the growing complexity and stringency of regulatory compliance across the globe. Helicopter engines must meet a wide range of safety, environmental, and performance standards, which vary by region.

Regulatory bodies such as the Federal Aviation Administration (FAA) in the U.S. and the European Union Aviation Safety Agency (EASA) impose strict guidelines on engine design, emissions, noise levels, and maintenance procedures.

As governments impose stricter environmental regulations, helicopter manufacturers are under increasing pressure to innovate and develop engines that comply with these requirements, especially in light of growing concerns about climate change and the aviation industry’s carbon footprint. Adapting to these new standards can be both costly and time-consuming, requiring significant investment in research and development.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Growth Factors

A significant growth factor for the helicopter engines market is the rising demand for both military and civilian helicopters worldwide. The global military helicopter fleet is expanding, driven by increasing defense budgets, particularly in regions like North America, Asia-Pacific, and the Middle East.

In 2024, military helicopters accounted for more than 55% of the total helicopter engine market share, with turbine engines being the preferred choice due to their high power-to-weight ratio and reliability in critical missions.

Emerging Trends

Hybrid and Electric Propulsion Systems

One of the most significant emerging trends in the helicopter engine market is the shift toward hybrid and electric propulsion systems. The growing need for more environmentally friendly and fuel-efficient alternatives is reshaping the market. Hybrid engines, which combine traditional turbine engines with electric motors, are gaining traction, especially in the civil aviation sector.

Electric helicopters, which are seen as a game-changer for urban air mobility (UAM), could redefine how people travel in densely populated areas. Companies like Joby Aviation and Vertical Aerospace are already making progress in developing electric vertical take-off and landing (eVTOL) aircraft, signaling a shift toward cleaner, greener aviation technologies.

Business Benefits

Cost Savings and Operational Efficiency

Adopting advanced helicopter engines, including hybrid and electric systems, brings significant business benefits. These new engine technologies are designed to be more fuel-efficient, cost-effective, and environmentally friendly. For instance, hybrid-electric propulsion can significantly reduce fuel consumption, cutting long-term operating costs by up to 30-40%.

This reduction in fuel costs is particularly beneficial for commercial operators who rely on helicopters for regular transportation, like in tourism and EMS services. Additionally, advancements in engine reliability and maintenance are contributing to reduced downtime and increased operational efficiency. These business benefits invest in new engine technologies highly appealing, positioning companies to thrive in an increasingly competitive and cost-conscious market.

Key Players Analysis

Airbus SE, a major player in the global helicopter engines market, has continued to strengthen its position through strategic acquisitions and product innovations. In recent years, Airbus has focused on expanding its helicopter portfolio, particularly with the launch of the H160 and H175 models, which are equipped with advanced turbine engines designed for both commercial and military applications.

Hindustan Aeronautics Ltd. (HAL) has been a key player in the Indian and global helicopter engines market, particularly in the defense sector. HAL has been working closely with the Indian Ministry of Defense to develop indigenous helicopter engines for military applications.

Through partnerships and collaborations, such as its agreement with GE Aviation for the development of turboshaft engines, HAL has significantly enhanced its engineering capabilities and its portfolio of advanced engine technologies.

Honeywell International Inc. remains one of the top global players in the helicopter engine market, primarily through its development of turbine engines for both military and civilian helicopters. Honeywell has recently introduced several new engines, including the HTS900 turboshaft engine, designed for light-utility helicopters, providing greater efficiency and lower operating costs. Honeywell’s innovative approach to engine technology, which emphasizes fuel efficiency and reduced emissions, positions it well for future growth in environmentally conscious markets.

Top Key Players in the Market

- Airbus SE

- Hindustan Aeronautics Ltd.

- Honeywell International Inc.

- ITP Aero

- JSC Klimov

- Kawasaki Heavy Industries Ltd.

- Mitsubishi Heavy Industries Ltd

- MTU Aero Engines AG

- Rolls Royce Holdings Plc

- Rostec

- Safran SA

- Textron Aviation Inc.

- Turkish Aerospace Industries Inc.

- ULPower Aero Engines

- Voronezh Mechanical Plant

- Bell Textron Inc.

- Pratt & Whitney (RTX Corporation)

- General Electric Company

- Avco Corporation

- IHI Corporation

- Other Key Players

Recent Developments

- In 2024, Honeywell International launched its highly anticipated HTS900 turboshaft engine, designed for light-utility helicopters.

- In 2024, Airbus SE made significant strides in the development of Urban Air Mobility (UAM) by advancing its electric vertical take-off and landing (eVTOL) technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 20.04 Billion |

| Forecast Revenue (2034) | USD 48.36 Billion |

| CAGR (2025-2034) | 3.80% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Piston Engine, Turbine Engine), By Application (Military, Civil and Commercial), By Sale (OEM, Aftermarket) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Airbus SE, Hindustan Aeronautics Ltd., Honeywell International Inc., ITP Aero, JSC Klimov, Kawasaki Heavy Industries Ltd., Mitsubishi Heavy Industries Ltd, MTU Aero Engines AG, Rolls Royce Holdings Plc, Rostec, Safran SA, Textron Aviation Inc., Turkish Aerospace Industries Inc., ULPower Aero Engines, Voronezh Mechanical Plant, Bell Textron Inc., Pratt & Whitney (RTX Corporation), General Electric Company, Avco Corporation, IHI Corporation, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |