Quick Navigation

Report Overview

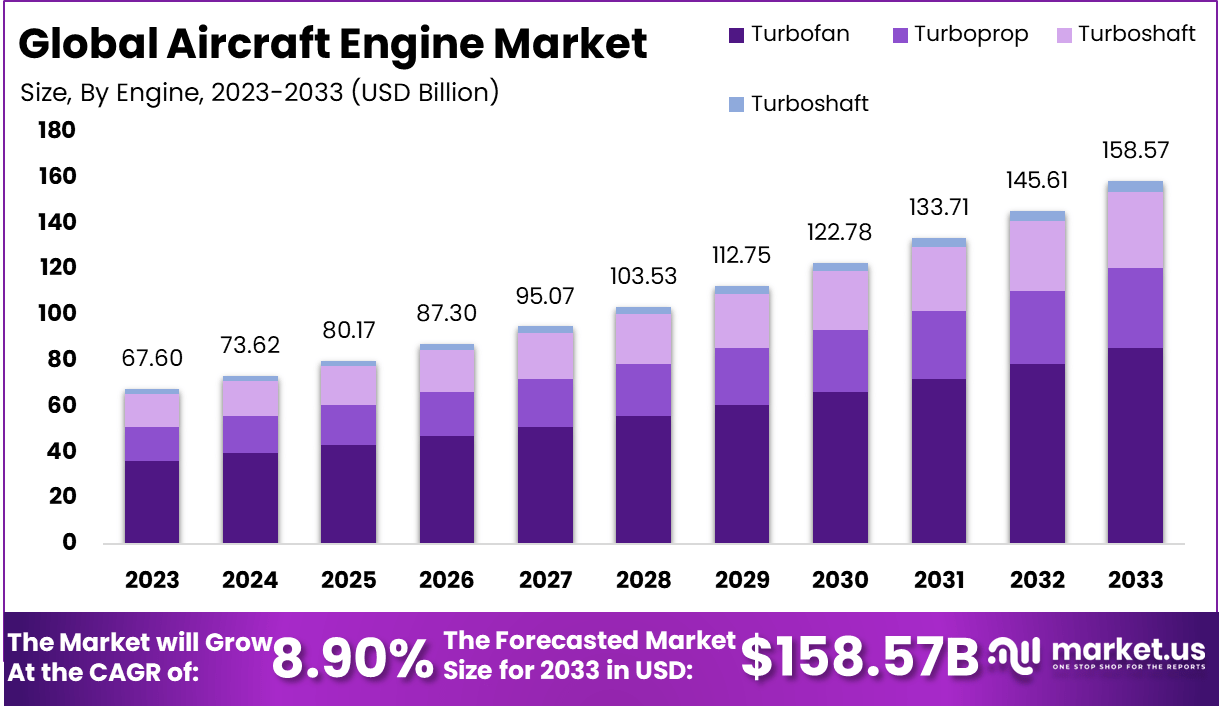

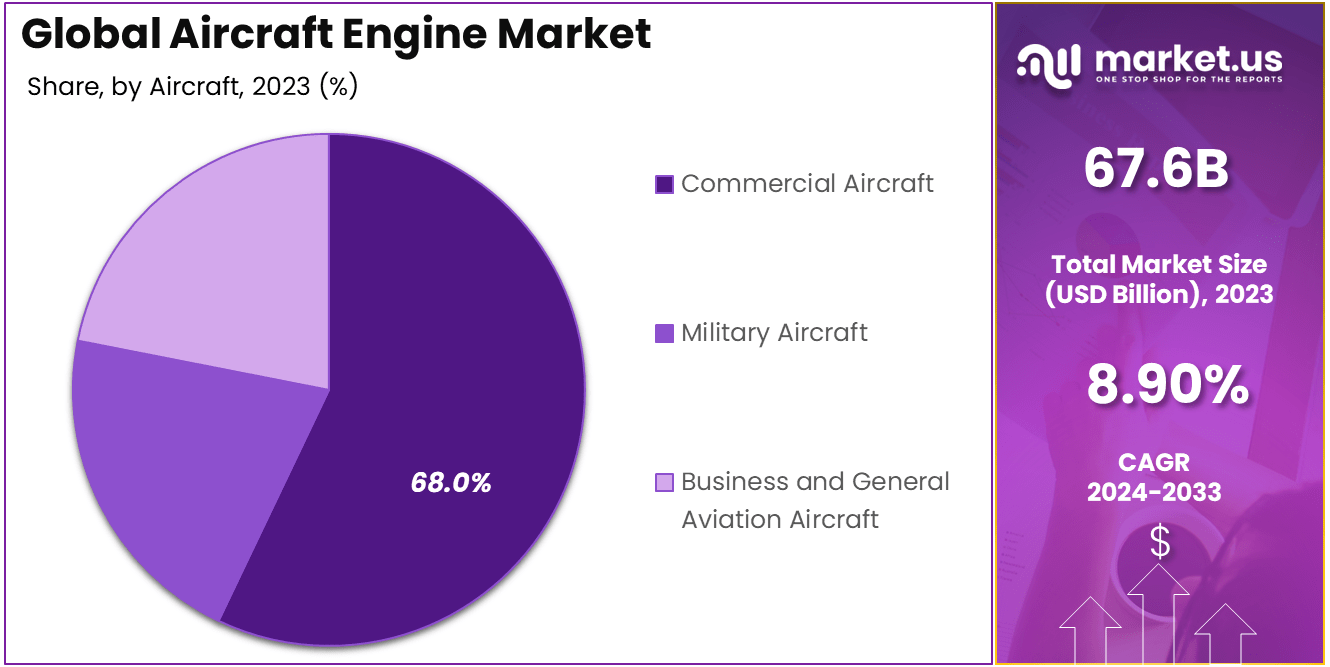

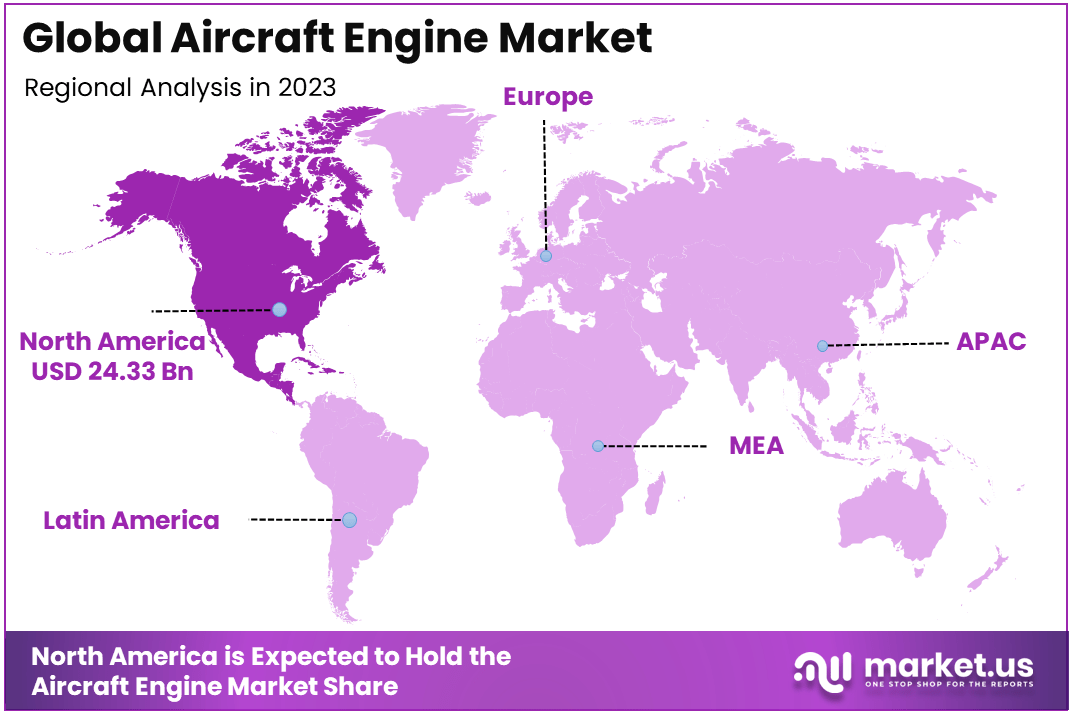

The Global Aircraft Engine Market size is expected to be worth around USD 158.57 Billion By 2033, from USD 67.6 Billion in 2023, growing at a CAGR of 8.90% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 36% share, holding USD 24.33 Billion in revenue.

An aircraft engine is a complex mechanical system designed to power an aircraft by generating thrust or propulsion. These engines are typically categorized into types such as jet engines, turboprops, and piston engines, depending on the specific requirements of the aircraft.

Jet engines, including turbofan and turbojet models, are most common in commercial and military aviation due to their high speed and efficiency. Aircraft engines are designed with advanced materials and precision engineering to ensure safety, reliability, and performance under varying conditions.

The aircraft engine market focuses on the production, development, and sales of engines for commercial, military, and general aviation aircraft. In 2023, the market was valued at approximately USD 67.6 billion, driven by increasing global air travel demand and the replacement of older fleets with fuel-efficient engines.

This market also includes related services such as maintenance, repair, and overhaul (MRO). Key players like General Electric, Rolls-Royce, and Pratt & Whitney are actively innovating to meet the evolving needs of airlines and defense sectors worldwide.

The growing demand for air travel, both domestically and internationally, significantly drives the aircraft engine market. According to IATA, global passenger traffic grew by 35% in 2023, highlighting a recovery post-pandemic. Airlines are focusing on acquiring modern, fuel-efficient engines to reduce operational costs and carbon emissions.

Additionally, governments are increasing investments in military aviation, further fueling demand for advanced jet engines. For instance, the U.S. defense budget allocated over USD 13 billion in 2023 for new military aircraft programs, including next-generation engines.

The market demand is fueled by the replacement of aging aircraft fleets and the increasing adoption of narrow-body aircraft for short-haul routes. As of 2023, airlines like Delta and Emirates have announced orders for over 300 new aircraft, each equipped with cutting-edge engines.

The growing popularity of private aviation also boosts demand for smaller piston and turboprop engines. Furthermore, emerging economies in Asia-Pacific are witnessing a surge in low-cost carriers, which require reliable and efficient engine technology.

Opportunities in the aircraft engine market include the growing demand for sustainable aviation fuels (SAF)-compatible engines and hybrid-electric propulsion systems. Companies are heavily investing in R&D to develop engines with lower carbon footprints.

For example, Rolls-Royce is testing a new hydrogen-powered jet engine expected to revolutionize sustainable air travel. Moreover, advancements in additive manufacturing and AI-driven design processes offer cost-effective and customizable solutions for engine production, opening doors for innovation.

Technological advancements are reshaping the aircraft engine industry, focusing on improving fuel efficiency, reducing emissions, and enhancing engine durability. Developments in materials like ceramic matrix composites (CMC) allow engines to operate at higher temperatures, increasing efficiency by up to 15%.

Digital twins and predictive maintenance technologies are also transforming the MRO segment, reducing downtime and costs. Additionally, hybrid-electric and fully electric propulsion systems are gaining traction, aligning with the industry’s sustainability goals.

Aircraft engines are sophisticated propulsion systems that generate thrust for various types of aircraft, with distinct specifications and performance metrics. Turbofan engines, commonly used in commercial aviation, produce thrust ranging from 44.6 kN at cruise to 169 kN at take-off with reheat, featuring a specific fuel consumption of approximately 33.71 mg/Ns and a pressure ratio of around 11.3 during cruise.

These engines typically consist of 7 low-pressure and 7 high-pressure compressor stages, along with one low-pressure and one high-pressure turbine stage, weighing about 3,386 kg. Turbojet engines, often found in military applications, vary in power output from 1,343 kW to 5,222 kW and have air mass flow rates between 9 kg/s to 29.5 kg/s.

Usually incorporating up to 13 axial compressor stages and 2 to 3 turbine stages. Turboprop engines, designed for regional and commuter aircraft, deliver power outputs ranging from around 2,000 kW to over 5,000 kW with specific fuel consumption between 0.40 kg/kWh and 0.52 kg/kWh, achieving compressor pressure ratios from about 5.6 to 6.35.

Additionally, advanced engines can reach turbine entry temperatures of up to 1,270 K and utilize various combustion system configurations, such as annular or can-type burners. These specifications highlight the diversity of aircraft engines tailored for specific operational requirements like speed, efficiency, and altitude capabilities across different aviation sectors.

Key Takeaways

- Market Growth: The global aircraft engine market was valued at USD 67.6 billion in 2023 and is projected to reach USD 158.57 billion by 2033, growing at a robust CAGR of 8.90% over the forecast period.

- Dominant Engine Type: The Turbofan segment held a dominant market share of 54% in 2023, driven by its widespread use in commercial and military jet applications due to superior fuel efficiency and thrust capabilities.

- Leading Aircraft Type: The Commercial Aircraft segment accounted for 68% of the market in 2023, supported by increasing global air travel demand and fleet modernization programs by major airlines.

- Point of Sale: The Aftermarket segment captured a significant 61% share in 2023, fueled by rising demand for maintenance, repair, and overhaul (MRO) services to ensure operational efficiency and regulatory compliance.

- Regional Insights: North America led the market with a 36% share in 2023, attributed to the presence of key aircraft engine manufacturers, high air travel demand, and substantial defense spending in the region.

By Engine

In 2023, the Turbofan segment held a dominant position in the aircraft engine market, capturing more than 54% of the total market share. This leading position is primarily attributed to the extensive use of turbofan engines in commercial aviation and military jets.

Turbofan engines are widely preferred for their superior fuel efficiency, high thrust-to-weight ratio, and reduced noise levels, making them an ideal choice for long-haul flights and high-capacity aircraft. The growth of the Turbofan segment is also driven by the increasing global air travel demand and fleet expansion by major airlines.

With rising passenger traffic, particularly in regions like Asia-Pacific and North America, airlines are investing in advanced aircraft equipped with turbofan engines to meet operational efficiency and emission regulations. Additionally, the rise of low-cost carriers (LCCs) has further boosted demand for narrow-body aircraft, which primarily utilize turbofan engines, contributing to the segment’s dominance.

Technological advancements in turbofan engines have further strengthened their market leadership. Innovations such as geared turbofans (GTF) and ultra-high bypass ratio engines have significantly improved fuel consumption and reduced carbon emissions.

Aligning with the aviation industry’s push toward sustainability. For instance, Pratt & Whitney’s GTF engines have been adopted by leading aircraft manufacturers like Airbus for their A320neo series, emphasizing the growing preference for turbofan technology.

By Aircraft

In 2023, the Commercial Aircraft segment held a dominant market position, capturing more than 68% of the total market share. This leadership is primarily driven by the rapid expansion of global air travel and the increasing demand for passenger and cargo transportation.

As economies recover from the pandemic and international borders reopen, airlines worldwide are witnessing a surge in passenger traffic, especially in regions like Asia-Pacific and North America, where tourism and business travel are rebounding strongly.

The dominance of the Commercial Aircraft segment is also fueled by fleet modernization and expansion programs undertaken by major airlines. With airlines striving to enhance fuel efficiency and reduce operating costs, there has been a significant shift toward acquiring next-generation aircraft equipped with advanced engines.

For instance, aircraft like the Airbus A320neo and Boeing 737 MAX, powered by fuel-efficient turbofan engines, have gained considerable traction in the market, further driving the growth of the commercial aviation segment. Another factor contributing to this segment’s dominance is the rise of low-cost carriers (LCCs), which have significantly expanded their operations, particularly in emerging economies.

LCCs prioritize narrow-body aircraft for short and medium-haul routes, creating robust demand for engines tailored for commercial aviation. Additionally, growing e-commerce activities have spurred the need for freighter aircraft, adding further momentum to the commercial aircraft market.

By Point of Sale

In 2023, the Aftermarket segment held a dominant market position, capturing more than 61% of the total market share. This leadership is attributed to the high demand for maintenance, repair, and overhaul (MRO) services for aircraft engines, driven by the increasing global airline fleet size and the aging of aircraft already in service.

With airlines focused on maintaining operational efficiency and ensuring passenger safety, the reliance on aftermarket services for routine engine maintenance and part replacements remains critical. One of the key factors contributing to the Aftermarket segment’s dominance is the rising number of older aircraft that require frequent engine inspections and replacements to meet operational and regulatory standards.

As airlines work to extend the lifecycle of their fleets, they continue to depend on aftermarket service providers for engine upgrades, spare parts, and repairs. Furthermore, the surge in air travel post-pandemic has resulted in higher aircraft utilization rates, leading to greater wear and tear on engines and, consequently, an increased demand for MRO services.

Another driving force for the Aftermarket segment is the complex and high-cost nature of aircraft engines, which makes repair and replacement services a significant expense for airlines. Leading engine manufacturers and independent MRO service providers play a pivotal role in offering cost-effective aftermarket solutions, including component repair, performance upgrades, and spare parts supply.

For instance, companies like GE Aviation and Rolls-Royce have developed specialized service agreements, such as power-by-the-hour contracts, ensuring airlines receive continuous support throughout the engine lifecycle.

Key Market Segments

By Engine

- Turboprop

- Turbofan

- Turboshaft

- Piston Engine

By Aircraft

- Commercial Aircraft

- Military Aircraft

- Business and General Aviation Aircraft

By Point of Sale

- OEM

- Aftermarket

Driving Factors

Growing Demand for Air Travel and Fleet Expansion

The increasing global demand for air travel is a significant driver for the aircraft engine market. In 2023, global air passenger traffic grew by nearly 9% year-on-year, recovering strongly post-pandemic. This growth, as reported by the International Air Transport Association (IATA), has resulted in airlines expanding their fleets to meet rising passenger demand.

Fleet expansion not only necessitates the procurement of new aircraft but also drives the demand for advanced and fuel-efficient engines. Fuel efficiency is a critical factor for airlines striving to reduce operational costs and meet stringent environmental regulations.

Modern engines, such as the Pratt & Whitney GTF and GE Aviation LEAP, offer up to 15% more fuel efficiency than their predecessors, making them attractive to airline operators. Furthermore, the boom in the low-cost carrier (LCC) segment has accelerated the adoption of single-aisle, narrow-body aircraft powered by turbofan engines, which are widely regarded for their cost-effectiveness and reliability.

Additionally, the surge in e-commerce and cargo services has led to a heightened demand for freighter aircraft, further boosting engine sales. Major players, such as Airbus and Boeing, have reported record backlogs for aircraft deliveries, translating into sustained demand for aircraft engines. For instance, as of mid-2024, Boeing’s commercial aircraft backlog exceeded 5,000 units, showcasing the long-term growth potential of the engine market.

Restraining Factors

High Development and Maintenance Costs

Despite strong growth prospects, the aircraft engine market faces challenges due to the high costs associated with engine development, manufacturing, and maintenance. Developing a new-generation engine involves significant research and testing costs, often amounting to billions of dollars. For example, Rolls-Royce invested approximately £1.4 billion in R&D in 2023, a figure that significantly impacts the financial dynamics of engine manufacturers.

Moreover, the maintenance, repair, and overhaul (MRO) of aircraft engines are capital-intensive due to the complexity of engine components and the need for specialized expertise. Airlines spend an estimated 40% of total maintenance costs on engines alone, which can be a significant financial burden, particularly for smaller operators. The unpredictability of engine failures and the high cost of spare parts exacerbate this issue, making it a critical concern for both manufacturers and users.

Additionally, the prolonged timeframes required for engine certification and compliance with regulatory standards delay the introduction of new technologies into the market, further restraining growth. For instance, stricter FAA and EASA emission standards require extensive testing, which adds to the cost and complexity of engine development.

Growth Opportunities

Advancements in Sustainable Aviation Technology

The shift toward sustainable aviation presents a transformative opportunity for the aircraft engine market. With aviation accounting for nearly 2.5% of global CO2 emissions, the focus on developing greener engines and reducing the environmental footprint has intensified. Governments and regulatory bodies worldwide are enforcing stringent emission norms, driving engine manufacturers to invest heavily in alternative technologies.

Hybrid-electric and fully electric engines are emerging as promising solutions for short-haul aircraft. Companies like Rolls-Royce, GE Aviation, and Safran are actively developing electric propulsion systems that could revolutionize the industry. For example, Rolls-Royce’s ACCEL program, which tested a fully electric plane in 2023, demonstrated a significant reduction in emissions and noise pollution.

Another key opportunity lies in the adoption of sustainable aviation fuels (SAFs), which can reduce CO2 emissions by up to 80%. Engine manufacturers are increasingly modifying existing engine designs to accommodate SAFs, ensuring long-term compatibility with cleaner fuels. As governments incentivize the production and adoption of SAFs, the demand for compatible engines is expected to surge.

Challenging Factors

Supply Chain Disruptions and Raw Material Shortages

One of the primary challenges in the aircraft engine market is the disruption in the global supply chain, exacerbated by geopolitical tensions and the lingering effects of the COVID-19 pandemic. The aerospace sector relies heavily on a global network of suppliers for critical materials, such as titanium, nickel alloys, and composites. However, disruptions in the supply chain have resulted in delays in engine production and increased costs.

For example, the Russia-Ukraine conflict in 2022 significantly impacted the supply of titanium, a vital component in aircraft engines. Russia is one of the largest suppliers of aerospace-grade titanium, and the imposition of sanctions disrupted the supply chain, leading to price surges. As of 2024, the price of titanium had risen by 15-20%, placing additional financial strain on engine manufacturers.

Moreover, shortages of skilled labor in the aerospace industry compound the challenge, particularly in the MRO segment. Engine maintenance requires highly specialized expertise, and the lack of trained personnel has led to bottlenecks in servicing and repairs. Additionally, the high dependence on just-in-time manufacturing strategies has made the industry vulnerable to unexpected disruptions, further complicating the production timelines.

Growth Factors

The aircraft engine market is experiencing significant growth, fueled by increasing global air travel demand and the expansion of airline fleets. Post-pandemic recovery in passenger traffic has been robust, with the International Air Transport Association (IATA) reporting a nearly 9% year-on-year increase in air passenger traffic in 2023.

Airlines are heavily investing in new, fuel-efficient aircraft to cater to this growing demand. Furthermore, the boom in e-commerce and logistics has led to higher demand for cargo aircraft, boosting the market for advanced aircraft engines. Rising environmental concerns have also pushed engine manufacturers to develop fuel-efficient and low-emission engines, a critical growth driver in this market.

Emerging Trends

Technological advancements are shaping the future of the aircraft engine market. Hybrid-electric propulsion systems and sustainable aviation fuels (SAFs) are key trends aimed at reducing the aviation sector’s environmental footprint. Companies like Rolls-Royce and Safran are leading the charge in developing hybrid-electric engines that promise reduced fuel consumption and lower emissions.

Another emerging trend is the use of digital twin technology, enabling predictive maintenance and real-time monitoring of engine performance, significantly reducing downtime and operational costs. These trends are transforming the industry, emphasizing sustainability and efficiency.

Business Benefits

The adoption of next-generation aircraft engines provides airlines with substantial business benefits. Fuel-efficient engines, such as Pratt & Whitney’s GTF and GE Aviation’s LEAP, offer up to 15% fuel savings, translating to lower operational costs for airlines. Improved engine designs also enhance reliability, reducing maintenance-related disruptions and ensuring higher fleet availability.

Furthermore, the integration of advanced analytics and digital solutions allows airlines to monitor engine health in real time, enabling predictive maintenance and minimizing costly repairs. These advancements not only enhance profitability but also help airlines meet regulatory requirements and environmental goals, solidifying their competitive advantage in the global aviation market.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 36% share of the global aircraft engine market, with revenue reaching USD 24.33 billion. The region’s leadership can be attributed to its robust aerospace industry, home to some of the largest aircraft and engine manufacturers such as General Electric (GE) Aviation, Pratt & Whitney, and Honeywell International Inc.

These companies are at the forefront of developing advanced aircraft engine technologies, including fuel-efficient and sustainable solutions, which continue to shape the global market. One of the key drivers for North America’s dominance is the significant investments in defense aviation.

The U.S. government allocates substantial budgets toward modernizing its military fleet, fostering demand for advanced engines used in fighter jets and other military aircraft. For instance, the U.S. Department of Defense’s budget for 2023 included allocations for the procurement of cutting-edge turbofan engines, which are pivotal for maintaining aerial superiority.

Furthermore, the commercial aviation sector in North America has rebounded strongly post-pandemic, with increasing passenger traffic and growing fleet expansions. According to the Federal Aviation Administration (FAA), the U.S. recorded a 14% year-on-year increase in domestic air travel in 2023, driving demand for new-generation aircraft powered by efficient engines.

The strong presence of low-cost carriers and rising cargo operations have further accelerated market growth in the region. North America also leads in the adoption of sustainable aviation fuels (SAFs) and hybrid-electric propulsion technologies. Regulatory bodies like the FAA and Environment Canada are actively promoting the use of eco-friendly engine solutions, pushing manufacturers to innovate.

Additionally, initiatives to integrate digital twin technologies and real-time engine monitoring systems are being rapidly adopted in the region, ensuring higher efficiency and lower operational costs. This focus on sustainability and technological advancements positions North America as a critical hub for aircraft engine innovation and manufacturing globally.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

General Electric Aviation made headlines with its focus on sustainability and innovation. The company successfully tested a new generation of turbofan engines designed to run on 100% Sustainable Aviation Fuel (SAF). This development aligns with the global push toward reducing aviation’s carbon footprint.

GE Aviation also collaborated with Boeing to integrate its next-gen engine technology into Boeing’s upcoming aircraft models, ensuring improved fuel efficiency and lower emissions. Additionally, GE has invested in partnerships with advanced materials firms to further enhance the durability and efficiency of its engine components.

Safran, a global leader in aircraft propulsion systems, has been expanding its footprint through strategic partnerships. In 2024, Safran announced a joint venture with MTU Aero Engines to develop cleaner, more efficient hybrid-electric propulsion systems. The partnership aims to redefine regional aviation by delivering quieter and eco-friendly engines by 2030.

Moreover, Safran introduced its latest LEAP engines, known for their advanced fuel efficiency, used in Airbus A320neo and Boeing 737 MAX fleets. The company also expanded its aftermarket services portfolio, signing long-term maintenance agreements with leading airlines such as Air France-KLM and Emirates.

Rolls-Royce continues to lead innovation in the aircraft engine market. In 2024, the company launched its much-anticipated UltraFan engine, which offers a 25% improvement in fuel efficiency compared to earlier models. This advanced turbofan engine, featuring lightweight composite materials and a unique gearbox design, supports both commercial and cargo aircraft.

Rolls-Royce also secured a major contract with Airbus for powering their next-generation long-haul aircraft, ensuring a strong market presence. Additionally, Rolls-Royce has been actively involved in hybrid-electric propulsion research, with several ongoing projects aimed at revolutionizing regional air travel.

Top Key Players in the Market

- General Electric Company

- Safran SA

- Rolls-Royce plc

- RTX Corporation

- Honeywell International Inc.

- Rostec

- MTU Aero Engines AG

- IHI Corporation

- Textron Inc.

- Mitsubishi Heavy Industries Aero Engines, Ltd.

- Other Key Players

Recent Developments

- In 2024: General Electric (GE) Aviation announced the successful testing of its next-generation turbofan engine designed to run on 100% Sustainable Aviation Fuel (SAF). This breakthrough aims to significantly reduce carbon emissions in commercial aviation while maintaining high efficiency and performance.

- In 2024: Rolls-Royce launched its UltraFan engine, a highly fuel-efficient and scalable turbofan engine platform, targeting both commercial and cargo aircraft markets. The UltraFan engine boasts a 25% improvement in fuel efficiency compared to its predecessors, thanks to its advanced composite materials and innovative gearbox technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 67.6 Bn |

| Forecast Revenue (2033) | USD 158.57 Bn |

| CAGR (2024-2033) | 8.90% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Engine (Turboprop, Turbofan, Turboshaft, Piston Engine), By Aircraft (Commercial Aircraft, Military Aircraft, Business and General Aviation Aircraft), By Point of Sale (OEM, Aftermarket) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | General Electric Company, Safran SA, Rolls-Royce plc, RTX Corporation, Honeywell International Inc., Rostec, MTU Aero Engines AG, IHI Corporation, Textron Inc., Mitsubishi Heavy Industries Aero Engines, Ltd., Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |