Quick Navigation

Report Overview

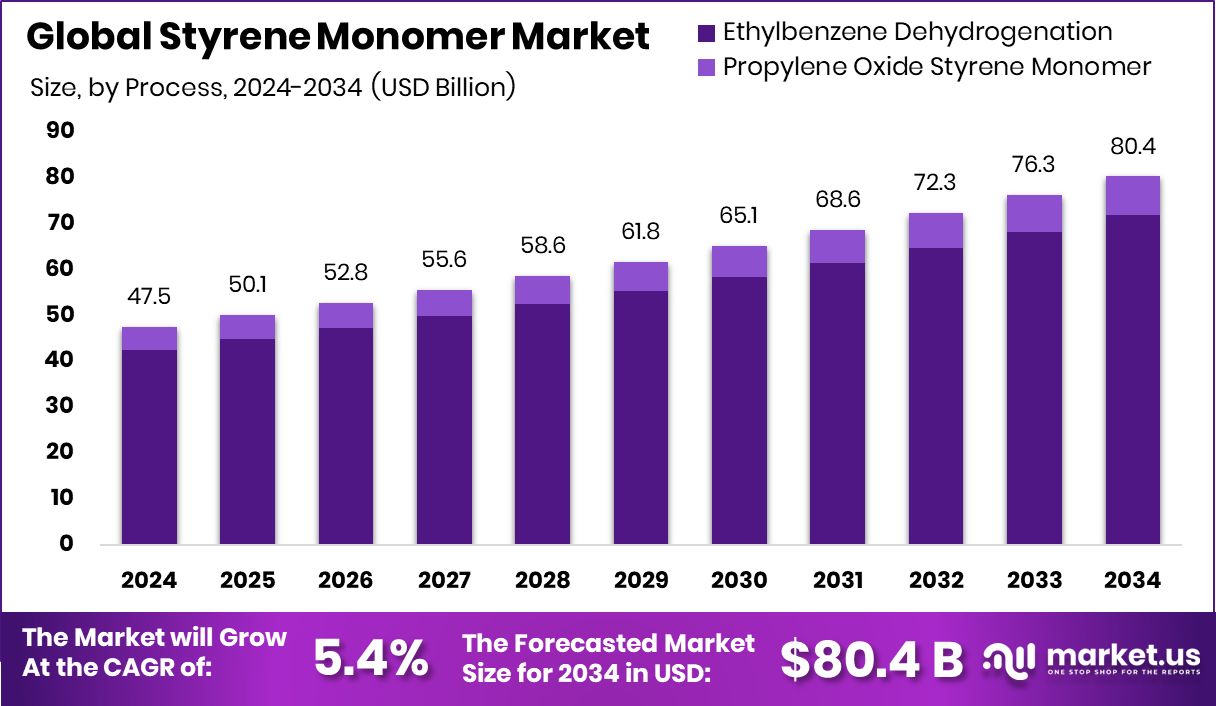

Global Styrene Monomer Market is expected to be worth around USD 80.4 billion by 2034, up from USD 47.5 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034. Strong manufacturing and packaging demand boosted Asia-Pacific’s 47.5% Styrene Monomer Market share.

Styrene monomer is a colorless, oily liquid derived mainly from petroleum-based sources. It is primarily used as a building block for various plastic and rubber products. Through polymerization, styrene is converted into polystyrene and other copolymers, which are found in packaging materials, insulation, automotive parts, consumer electronics, and construction products.

The styrene monomer market refers to the global trade and production landscape of this chemical compound. The market is influenced by demand from end-use sectors such as packaging, automotive, electronics, and construction. Demand patterns often reflect industrial trends, infrastructure development, and consumer preferences for lightweight and durable materials.

Urbanization and rising infrastructure development continue to boost the demand for insulation and construction materials, many of which are made from styrene-based polymers. Additionally, rising consumption of household appliances and electronics contributes to consistent growth. Innovations in polymer blends have also expanded styrene’s use in engineered plastics.

To address this, Indian Oil Corporation Limited (IOCL) has initiated the establishment of India’s first SM production facility at its Panipat refinery, with an annual capacity of 387 thousand tonnes. This project, aligned with the government’s “Atmanirbhar Bharat” initiative, involves an investment of approximately INR 4,495 crore and is expected to be operational by 2026-27.

The Indian styrene market is driven by robust demand from downstream sectors. The packaging industry, in particular, is a significant consumer, utilizing polystyrene for its lightweight and insulating properties. Additionally, the automotive and construction industries contribute to the demand through the use of ABS and SBR in various applications.

The Chemicals and Petrochemicals Association of India (CPAI) projects a 15% increase in styrene demand for FY2025- 26, reaching approximately 1.40 million tonnes, up from an estimated 1.22 million tonnes in FY2024- 25.

Key Takeaways

- Global Styrene Monomer Market is expected to be worth around USD 80.4 billion by 2034, up from USD 47.5 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034.

- Ethylbenzene dehydrogenation leads with an 89.6% share, dominating the styrene monomer production process globally.

- Polystyrene holds a 42.9% share, making it the primary application of styrene monomer worldwide.

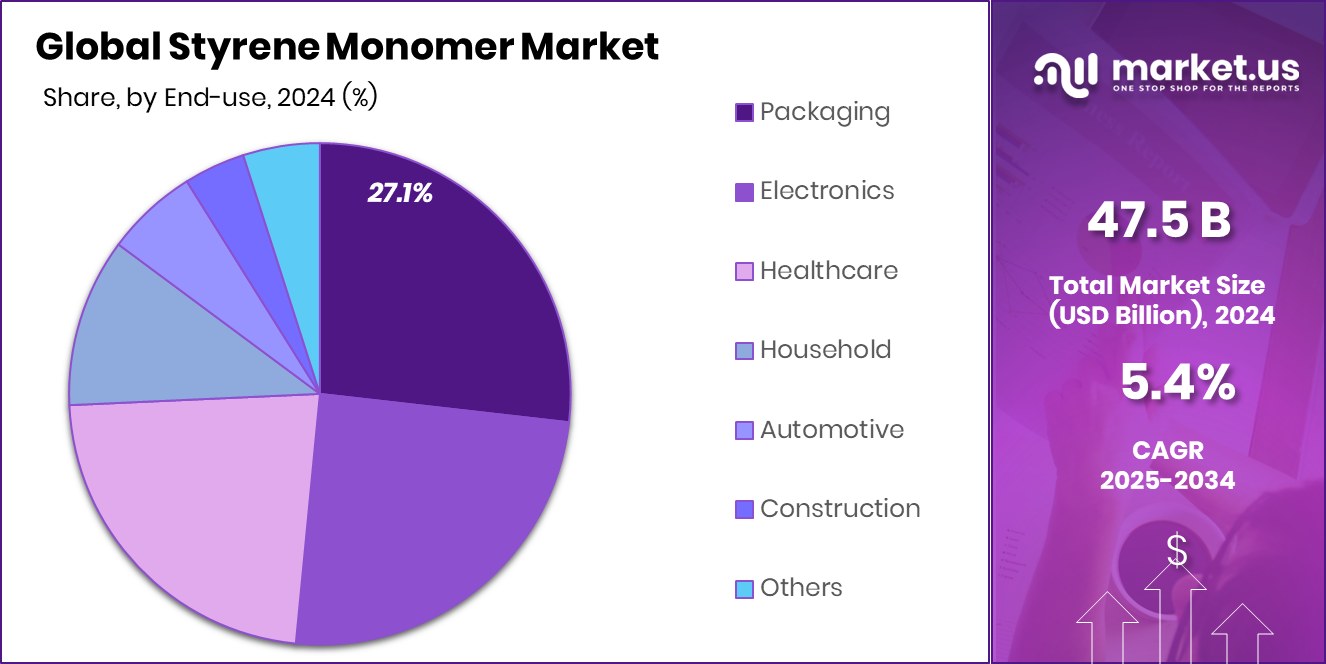

- Packaging represents 27.1% of end-use demand, marking it as the largest consumer of styrene monomer.

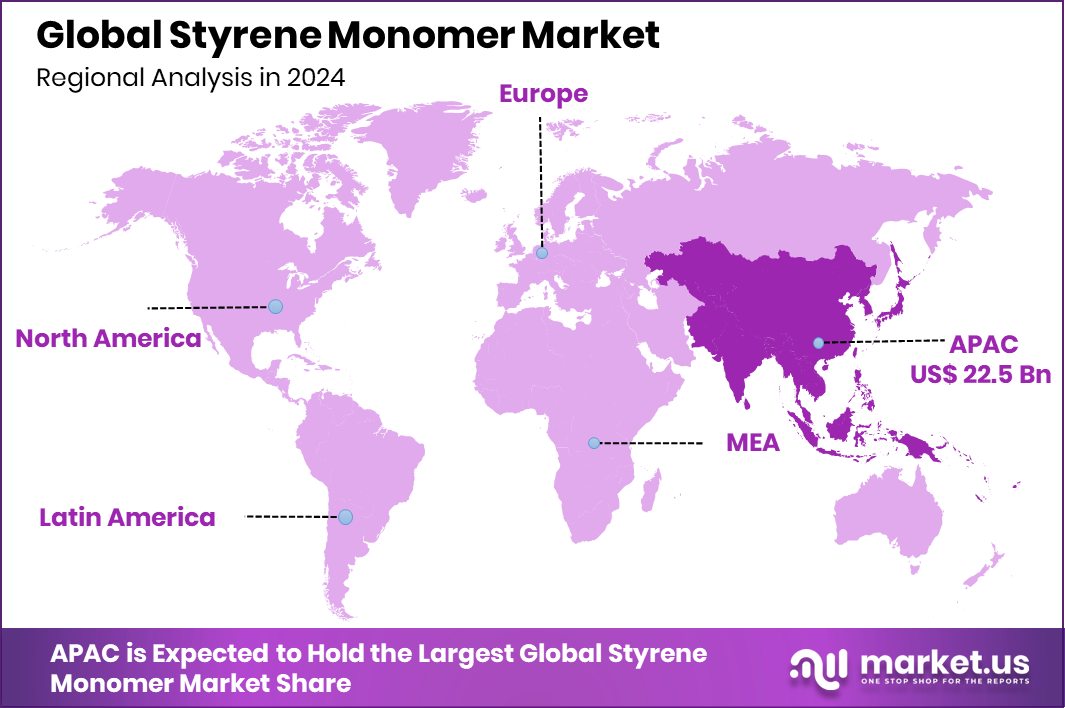

- The Asia-Pacific Styrene Monomer Market reached a value of USD 22.5 billion.

By Process Analysis

Ethylbenzene dehydrogenation dominates with an 89.6% share in the production process category.

In 2024, Ethylbenzene Dehydrogenation held a dominant market position in the By Process segment of the Styrene Monomer Market, with an 89.6% share. This overwhelming dominance highlights the continued reliance of global styrene production on the conventional dehydrogenation of ethylbenzene due to its cost-efficiency, scalability, and established infrastructure.

The process remains the backbone of industrial styrene synthesis, driven by its compatibility with large-scale petrochemical operations and integration with existing ethylbenzene feedstock availability. Ethylbenzene Dehydrogenation also benefits from lower per-unit production costs and high output volumes, making it ideal for meeting the growing demand for downstream applications like polystyrene, acrylonitrile butadiene styrene (ABS), and styrene-butadiene rubber.

The method’s dominance is further supported by process optimizations and catalytic advancements that enhance conversion efficiency while minimizing by-products. Despite emerging alternative technologies aiming for lower emissions or renewable feedstock integration, Ethylbenzene Dehydrogenation continues to maintain a competitive edge in terms of production economics and market familiarity.

By Application Analysis

Polystyrene accounts for 42.9% of the total styrene monomer application share globally.

In 2024, Polystyrene (PS) held a dominant market position in the By Application segment of the Styrene Monomer Market, with a 42.9% share. This dominance reflects the widespread use of polystyrene across packaging, consumer goods, electronics, and insulation materials. Its lightweight, durable, and cost-effective properties make PS an ideal choice for single-use packaging products, especially in the food and beverage sector.

Additionally, the construction industry continues to demand expanded polystyrene (EPS) for thermal insulation and structural applications. The automotive sector also contributes to PS demand through components requiring impact resistance and molding flexibility.

With manufacturers favoring PS for its ease of processing and recyclability, the segment maintained strong momentum in 2024. The 42.9% market share underscores its central role in driving styrene monomer consumption, particularly in high-volume production geographies.

Moreover, steady demand from developing regions for affordable and versatile plastic solutions supported the application’s continued growth. As sustainability initiatives gather pace, innovations in biodegradable and recycled polystyrene solutions are expected to emerge, yet conventional PS still retains its stronghold in 2024 due to its price-performance balance.

By End-use Analysis

Packaging is the largest end-use sector, holding 27.1% market share currently.

In 2024, Packaging held a dominant market position in the end-use segment of the Styrene Monomer Market, with a 27.1% share. This leadership position was primarily driven by the rising global demand for lightweight, cost-effective, and durable packaging solutions across the food, beverage, and consumer goods industries.

Styrene-based materials like polystyrene and expanded polystyrene (EPS) continue to be widely used in packaging applications due to their excellent insulation, moisture resistance, and protective properties. The segment’s 27.1% share reflects the high volume of styrene monomer consumed in manufacturing foam trays, disposable containers, and protective packaging materials. The food delivery and e-commerce boom further reinforced the segment’s growth, especially in urban and developing markets.

Additionally, the medical and pharmaceutical sectors increasingly rely on styrene-based packaging for sterile and lightweight product containment. Despite growing environmental scrutiny, the packaging segment retained its dominance due to its functionality and low production costs. Some brands also explored recycled or biodegradable polystyrene options to address sustainability concerns without compromising on performance.

Key Market Segments

By Process

- Ethylbenzene Dehydrogenation

- Propylene Oxide Styrene Monomer

By Application

- Polystyrene (PS)

- Acrylonitrile Butadiene Styrene (ABS)

- Acrylonitrile Styrene Acrylate (ASA)

- Styrene-acrylonitrile (SAN)

- Styrene Butadiene Rubber (SBR)

- Others

By End-use

- Packaging

- Electronics

- Healthcare

- Household

- Automotive

- Construction

- Others

Driving Factors

Growing Packaging Industry Driving Styrene Monomer Demand Worldwide

One of the main driving forces behind the styrene monomer market is the growing global packaging industry. Styrene is widely used to produce polystyrene, a popular plastic material for packaging containers, trays, and insulation. As online shopping and food delivery services increase, the demand for strong and lightweight packaging also grows.

Many companies prefer polystyrene packaging due to its affordability and protective qualities. Moreover, developing countries are seeing rapid growth in packaged food consumption, directly boosting the need for styrene-based products. The construction and electronics sectors also support this trend by using styrene in insulation and casings.

Restraining Factors

Health and Environmental Concerns Limit Market Growth

A major restraining factor for the styrene monomer market is the growing concern over health and environmental safety. Styrene is classified as a possible human carcinogen, and long-term exposure can cause serious health issues such as nervous system problems and respiratory irritation.

Due to these risks, many countries are implementing strict regulations on styrene use, handling, and emissions. Environmental activists and organizations are also pushing for safer alternatives, especially in food packaging.

This pressure has led several companies to explore biodegradable or less harmful materials. As regulations become tighter and awareness grows, the demand for styrene-based products may slow down, especially in markets where sustainable and non-toxic options are being strongly encouraged or even mandated.

Growth Opportunity

Expanding Automotive Sector Fuels Styrene Monomer Growth

The global automotive industry’s rapid expansion presents a significant opportunity for the styrene monomer market. Styrene monomer is a key component in producing materials like acrylonitrile butadiene styrene (ABS), which are extensively used in manufacturing automotive parts due to their lightweight, durability, and cost-effectiveness.

As the demand for fuel-efficient vehicles increases, manufacturers are seeking materials that reduce vehicle weight without compromising safety or performance. Styrene-based plastics meet these requirements, making them ideal for components such as dashboards, bumpers, and interior trims.

Additionally, the rise of electric vehicles (EVs) further amplifies this demand, as EV manufacturers prioritize lightweight materials to enhance battery efficiency and overall vehicle range. This trend indicates a promising growth trajectory for styrene monomer applications in the automotive sector.

Latest Trends

Shift Towards Eco-friendly Styrene Monomer Alternatives

A key trend in the styrene monomer market is the increasing shift towards eco-friendly and sustainable alternatives. With rising environmental concerns and stricter regulations, there is a growing demand for styrene-based products that have a smaller environmental footprint. Manufacturers are exploring bio-based styrene monomers derived from renewable resources, such as plant-based materials, to replace traditional petroleum-based styrene.

This transition is driven by the need to reduce greenhouse gas emissions and dependency on fossil fuels. Additionally, the rise in consumer preference for eco-friendly products is encouraging companies to innovate and adopt greener production processes. This trend is expected to gain momentum as more industries, especially in packaging and automotive, adopt sustainable materials to meet environmental standards and customer expectations.

Regional Analysis

In 2024, Asia-Pacific dominated the Styrene Monomer Market with a 47.5% regional share.

In 2024, the Asia-Pacific region held a dominant position in the global Styrene Monomer Market, accounting for 47.5% of the total market share, with a valuation of USD 22.5 billion. This leadership is primarily attributed to the region’s strong demand from the packaging, automotive, and construction sectors, particularly in emerging economies like China and India. Rapid industrialization and the growth of downstream industries further support the high consumption of styrene monomer in this region.

North America and Europe followed as significant markets, supported by the presence of key end-use industries and steady adoption of styrene-based polymers. Meanwhile, the Middle East & Africa and Latin America regions showed moderate growth, driven by expanding infrastructure and consumer goods sectors. However, these regions still trail behind in comparison to Asia-Pacific in terms of market value and share.

The demand in these regions remains promising but comparatively smaller in scale. Overall, the global styrene monomer market is seeing a clear regional skew, with Asia-Pacific emerging as the primary driver of growth due to its industrial expansion and increasing production capabilities.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, SABIC maintained a prominent role in the global Styrene Monomer Market through its extensive petrochemical operations and integrated production capabilities. With its strategic presence across Asia and the Middle East, SABIC leveraged strong supply chain infrastructure to meet the rising regional demand, particularly in the packaging and construction sectors. The company’s focus on innovation and operational efficiency helped it maintain cost leadership while complying with sustainability goals across its product portfolio.

INEOS continued to play a critical role in the market, supported by its vast production capacity in Europe and North America. The company capitalized on its robust downstream network and raw material integration, allowing it to respond swiftly to regional demand surges. INEOS also emphasized product consistency and reliability, which positioned it as a trusted supplier for polystyrene and ABS manufacturers.

Shell plc remained a key global supplier, benefiting from its global refining and chemical operations. In 2024, Shell optimized its operations in the U.S. and Asia to meet both domestic and export needs. The company maintained competitive performance by leveraging its feedstock flexibility and strategic joint ventures. Shell’s emphasis on decarbonization and technological advancement positioned it well to cater to future demand for sustainable monomers.

Top Key Players in the Market

- SABIC

- INEOS

- Shell plc

- KR Chemicals

- Qingdao Haiwan Group Co.,Ltd

- Denka Company Limited

- Chevron Phillips Chemical Company LLC

- KH Chemicals

- LOTTE Chemical CORPORATION

- Repsol

- Hanwha TotalEnergies Petrochemical Co Ltd

- Americas Styrenics LLC

- Westlake Corporation

- Equate Petrochemical Company

- The Kuwait Styrene Company

- Other Key Players

Recent Developments

- In March 2025, CPChem’s joint venture, Americas Styrenics (AmSty), began selling PolyRenew® styrene monomer made from recycled materials. This supports the eco-friendly production of items like tires and packaging.

- In March 2024, Denka commenced operations at a chemical recycling plant in Chiba, Japan. This facility recovers styrene monomer from used polystyrene through depolymerization, aligning with Denka’s “Mission 2030” goal to promote a circular economy for styrene-based packaging materials.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 47.5 Billion |

| Forecast Revenue (2034) | USD 80.4 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Ethylbenzene Dehydrogenation, Propylene Oxide Styrene Monomer), By Application (Polystyrene (PS), Acrylonitrile Butadiene Styrene (ABS), Acrylonitrile Styrene Acrylate (ASA), Styrene-acrylonitrile (SAN), Styrene Butadiene Rubber (SBR), Others), By End-use (Packaging, Electronics, Healthcare, Household, Automotive, Construction , Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | SABIC, INEOS, Shell plc, KR Chemicals, Qingdao Haiwan Group Co.,Ltd, Denka Company Limited, Chevron Phillips Chemical Company LLC, KH Chemicals, LOTTE Chemical CORPORATION, Repsol, Hanwha TotalEnergies Petrochemical Co Ltd, Americas Styrenics LLC, Westlake Corporation, Equate Petrochemical Company, The Kuwait Styrene Company, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |