Quick Navigation

Report Overview

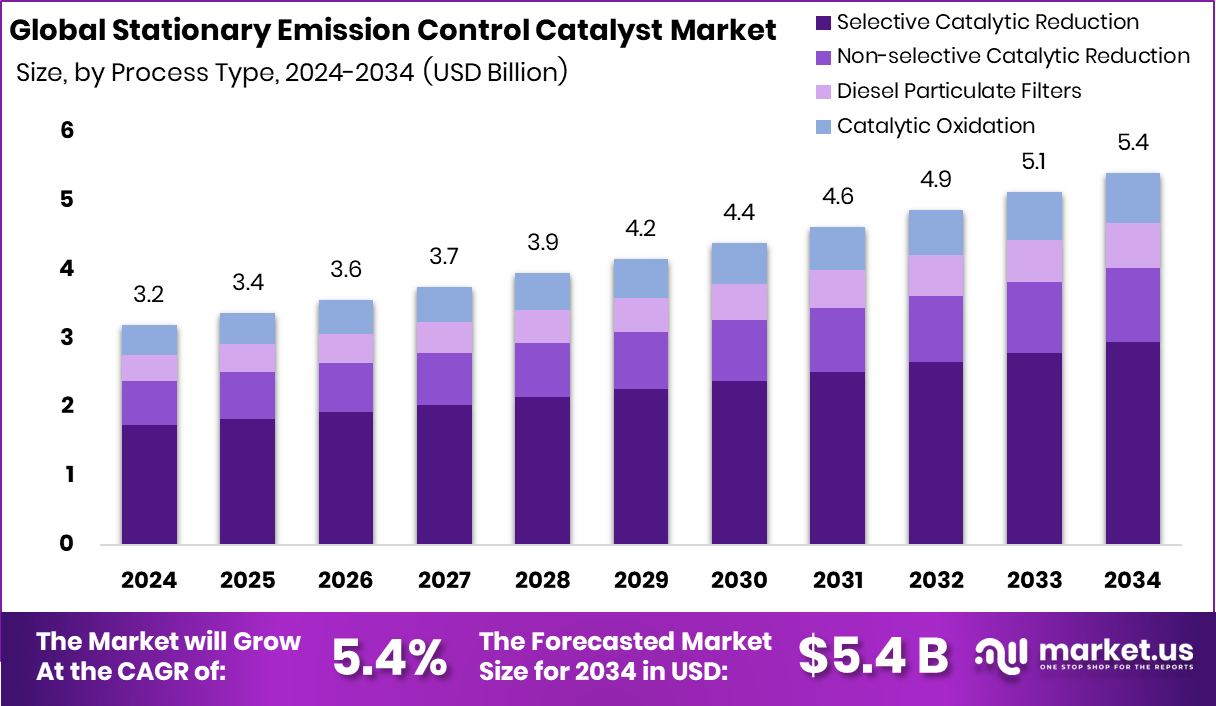

Global Stationary Emission Control Catalyst Market is expected to be worth around USD 5.4 billion by 2034, up from USD 3.2 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034. High industrial emissions in North America 47.8% are driving demand for advanced catalyst systems.

A stationary emission control catalyst is a substance used primarily in industrial and power generation settings to reduce harmful emissions released into the air. These catalysts facilitate chemical reactions that convert noxious gases like nitrogen oxides (NOx), sulfur dioxide (SO2), and carbon monoxide (CO) into less harmful substances such as nitrogen, water vapor, and carbon dioxide.

The stationary emission control catalyst market comprises the sales and distribution of catalysts designed for reducing emissions from stationary sources. This market caters to industries such as manufacturing, power generation, and waste incineration, where strict environmental regulations mandate the reduction of air pollutants.

The primary growth driver for the stationary emission control catalyst market is the tightening of global air quality standards. As governments worldwide impose stricter regulations to combat air pollution, industries are compelled to adopt advanced emission control technologies, bolstering the demand for effective catalysts.

Demand in this market is fueled by the ongoing industrial expansion, especially in emerging economies where industrial activities are intensifying. Additionally, the retrofitting of old plants with modern emission control systems to comply with new standards is a significant factor driving demand.

There’s a notable opportunity in developing and implementing next-generation catalysts that offer higher efficiency and longer operational lifespans. Innovations that can handle a broader range of temperatures and chemical inputs are up-and-coming as they can be adapted to various industrial processes and newer forms of energy production, like biomass and waste-to-energy plants.

Key Takeaways

- Global Stationary Emission Control Catalyst Market is expected to be worth around USD 5.4 billion by 2034, up from USD 3.2 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034.

- Selective Catalytic Reduction leads the process segment, capturing 54.4% of the Stationary Emission Control Catalyst market.

- Platinum Group Metals hold a dominant 43.7% share in catalyst type due to superior catalytic properties.

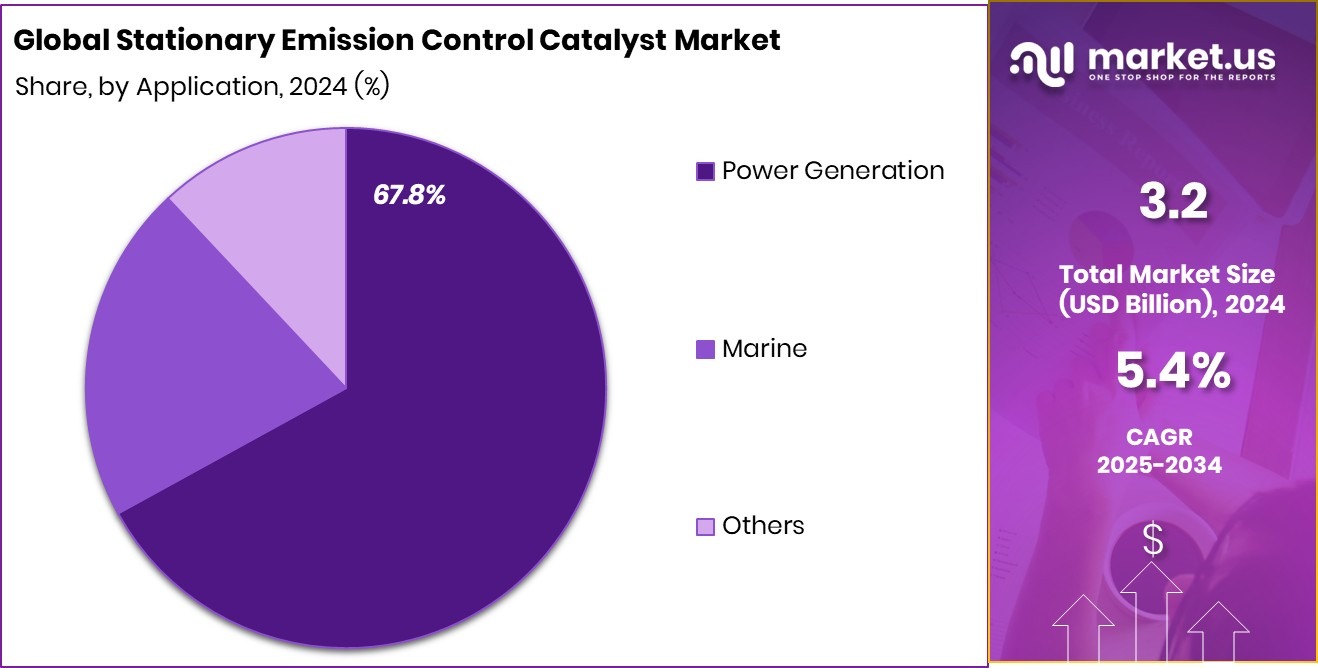

- Power Generation is the major application, accounting for 67.8% share in the Stationary Emission Control Catalyst Market.

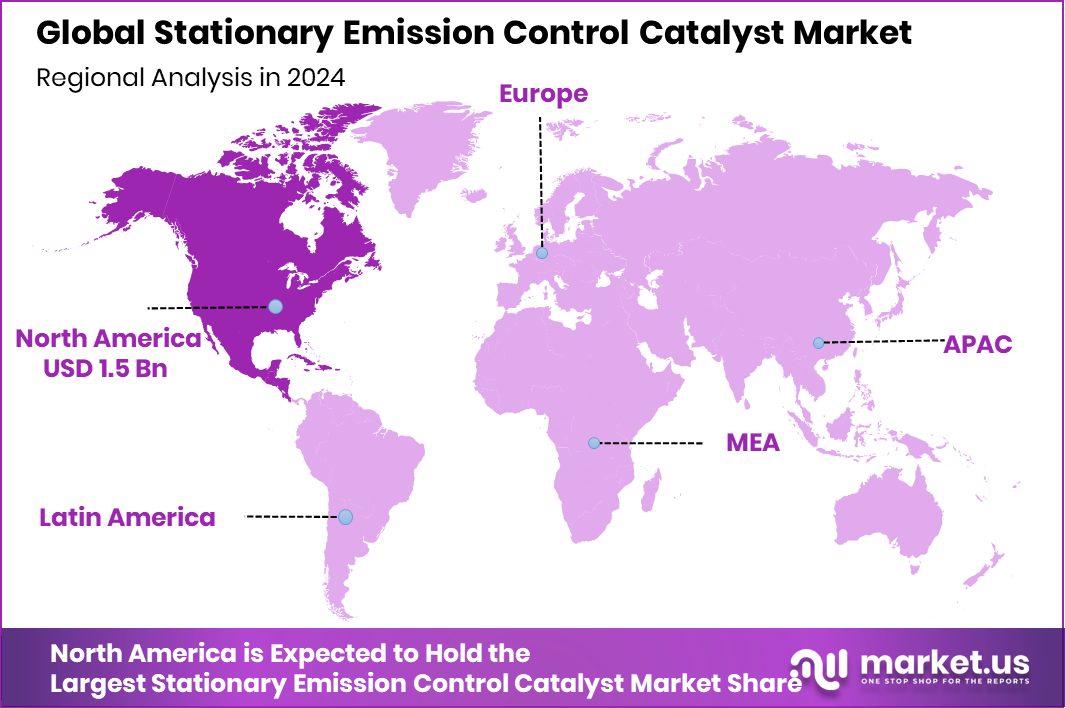

- The North America accounted for USD 1.5 billion, showing strong environmental policy influence.

By Process Type Analysis

Selective Catalytic Reduction 54.4% dominates the process type in the Stationary Emission Control Catalyst Market.

In 2024, Selective Catalytic Reduction held a dominant market position in By Process Type segment of Stationary Emission Control Catalyst Market, with a 54.4% share. This process was widely adopted due to its efficiency in reducing nitrogen oxide emissions across industrial setups.

Its proven performance in power plants, refineries, and chemical processing units contributed to its strong market hold. The high adoption rate was also linked to stricter emission regulations and increased focus on environmental compliance in the stationary industrial sector.

By Catalyst Type Analysis

Platinum Group Metals lead catalyst type with 43.7% market share globally.

In 2024, Platinum Group Metals held a dominant market position in By Catalyst Type segment of the Stationary Emission Control Catalyst Market, with a 43.7% share. The dominance was primarily driven by the superior catalytic efficiency and high thermal stability of platinum group metals in emission control systems. These catalysts are widely used in power plants, industrial boilers, and gas turbines to minimize harmful pollutants such as NOx, CO, and hydrocarbons, ensuring compliance with environmental norms.

The 43.7% share reflects the preference for platinum, palladium, and rhodium-based catalysts across stationary installations requiring consistent performance under harsh operational conditions. Their effectiveness in reducing long-term emissions while maintaining operational reliability has supported their demand. Additionally, the recyclability and long lifecycle of these materials add value in cost-sensitive industrial environments.

By Application Analysis

Power Generation drives major demand, contributing 67.8% in overall market applications.

In the By Application segment, Power Generation accounted for the highest share at 67.8% in 2024. This dominance stemmed from the substantial emissions produced by thermal power plants, requiring continuous deployment of emission control technologies.

The segment saw increased investments in emission-reduction infrastructure to align with national and international air quality goals. Overall, stationary emission control catalysts continued to be crucial in managing industrial pollution, with power generation remaining the primary application area.

Key Market Segments

By Process Type

- Selective Catalytic Reduction

- Non-selective Catalytic Reduction

- Diesel Particulate Filters

- Catalytic Oxidation

By Catalyst Type

- Platinum Group Metals

- Base Metals

- Non-Metallic Catalysts

By Application

- Power Generation

- Marine

- Others

Driving Factors

Growing Industrialization Increasing Air Pollution Levels Globally

The key factor driving the Stationary Emission Control Catalyst Market is the rapid growth of industrialization. As factories, power plants, and manufacturing units expand across countries, they release more harmful gases into the air. This pollution contributes to global warming and health problems.

Governments are now enforcing strict air quality regulations, pushing industries to install emission control technologies. Stationary emission control catalysts help reduce nitrogen oxides, carbon monoxide, and hydrocarbons from exhaust gases.

This rising awareness about clean air and the need to follow environmental rules is increasing the demand for these systems. With industrial hubs growing, especially in developing regions, the market is expected to grow significantly to support cleaner and greener industrial operations.

Restraining Factors

High Installation and Maintenance Cost Limits Adoption

One major factor restraining the growth of the Stationary Emission Control Catalyst Market is its high cost. Setting up emission control systems involves expensive catalysts and advanced technologies.

In addition, regular maintenance and replacement of components add to the overall expense. Many small and medium-sized industries find it difficult to afford these systems, especially in developing countries where budgets are tight.

Also, operating these systems requires skilled labor and technical knowledge, increasing operational costs. Due to these cost-related challenges, industries may delay or avoid installing emission control systems. This slows down the adoption rate and limits market growth, even though environmental regulations are getting stricter across the world.

Growth Opportunity

Adoption of Green Hydrogen and Cleaner Energy Solutions

A significant growth opportunity in the Stationary Emission Control Catalyst Market is the increasing adoption of green hydrogen and cleaner energy technologies. As industries and governments strive to reduce carbon emissions, there’s a growing shift toward sustainable energy sources. Green hydrogen, produced using renewable energy, is gaining traction as a clean fuel alternative.

This transition necessitates advanced emission control systems to manage and minimize pollutants during production and utilization processes. Stationary emission control catalysts play a crucial role in ensuring that these new energy solutions remain environmentally friendly by effectively reducing harmful emissions.

Latest Trends

Advancements in Catalyst Technology Enhancing Efficiency

A prominent trend in the Stationary Emission Control Catalyst Market is the continuous advancement in catalyst technologies aimed at enhancing efficiency and durability. Researchers and manufacturers are focusing on developing catalysts that can withstand higher temperatures and harsh industrial environments, thereby extending their operational lifespan and reducing maintenance costs.

Innovations include the use of advanced materials such as nanoparticle-based catalysts and hybrid composites, which offer improved surface area and reactivity, leading to more effective emission reductions. Additionally, there’s a growing emphasis on designing catalysts that are more selective, targeting specific pollutants like nitrogen oxides (NOx) and volatile organic compounds (VOCs) with greater precision.

Regional Analysis

North America dominated with a 47.8% share in the Stationary Emission Control Catalyst Market.

In 2024, North America held a dominant position in the Stationary Emission Control Catalyst Market, accounting for a 47.8% share, valued at USD 1.5 billion. This leadership is primarily driven by strict air quality regulations and the presence of numerous industrial and power generation facilities across the region. The enforcement of EPA standards has pushed the adoption of advanced emission control technologies in the manufacturing and energy sectors.

Europe followed with consistent adoption, supported by EU directives targeting industrial emissions and decarbonization goals. Asia Pacific showed notable growth, fueled by rapid urbanization and industrial expansion in emerging economies, although detailed values were not specified.

The Middle East & Africa region reflected moderate growth, primarily led by investments in power infrastructure and oil-based industries adapting to environmental norms. Latin America showed emerging demand, backed by increasing awareness and early policy movements toward emission control compliance.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the Stationary Emission Control Catalyst Market, BASF SE, Cataler Corporation, and CDTi Advanced Materials Inc. are pivotal players, each contributing uniquely to the industry landscape in 2024.

BASF SE leverages its extensive expertise in chemical solutions to enhance the efficacy and sustainability of emission control technologies. Their focus on developing high-performance catalysts that meet stringent environmental standards positions them as a leader in the market. BASF’s approach to innovation, coupled with its global reach, allows it to effectively respond to the evolving needs of industries seeking to reduce emissions.

Cataler Corporation, a specialist in catalyst technology, continues to make significant strides in the market by offering advanced solutions that cater to a wide range of applications, from industrial processes to power generation. Cataler’s commitment to R&D has enabled it to maintain a competitive edge, providing highly efficient catalysts that support the reduction of nitrogen oxides, particulate matter, and other pollutants.

CDTi Advanced Materials Inc. stands out for its unique proprietary technologies that target the reduction of emissions through advanced materials science. The company’s focus on cost-effective solutions that do not compromise on performance makes it a valuable player in the market. Their products are designed to meet the rigorous demands of stationary emission control, helping industries comply with environmental regulations while enhancing operational efficiency.

Top Key Players in the Market

- BASF SE

- Cataler Corporation

- CDTi Advanced Materials Inc.

- Clariant

- CORMETECH

- Corning Incorporated

- DCL International Inc.

- Honeywell International Inc.

- JGC C&C

- Johnson Matthey

- Umicore

- Topsoe

Recent Developments

- In April 2024, Clariant’s catalysts helped customers avoid 40 million tons of CO₂e in 2023, with significant reductions from N₂O abatement in nitric acid and low-carbon steel production.

- In April 2024, JGC Holdings completed a technical study on reducing methane and other greenhouse gas emissions at offshore natural gas sites in Malaysia, aiming to provide effective emission control solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.2 Billion |

| Forecast Revenue (2034) | USD 5.4 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process Type(Selective Catalytic Reduction, Non-selective Catalytic Reduction, Diesel Particulate Filters, Catalytic Oxidation), By Catalyst Type(Platinum Group Metals, Base Metals, Non-Metallic Catalysts), By Application(Power Generation, Marine, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Cataler Corporation, CDTi Advanced Materials Inc., Clariant, CORMETECH, Corning Incorporated, DCL International Inc., Honeywell International Inc., JGC C&C, Johnson Matthey, Umicore, Topsoe |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |