Quick Navigation

Report Overview

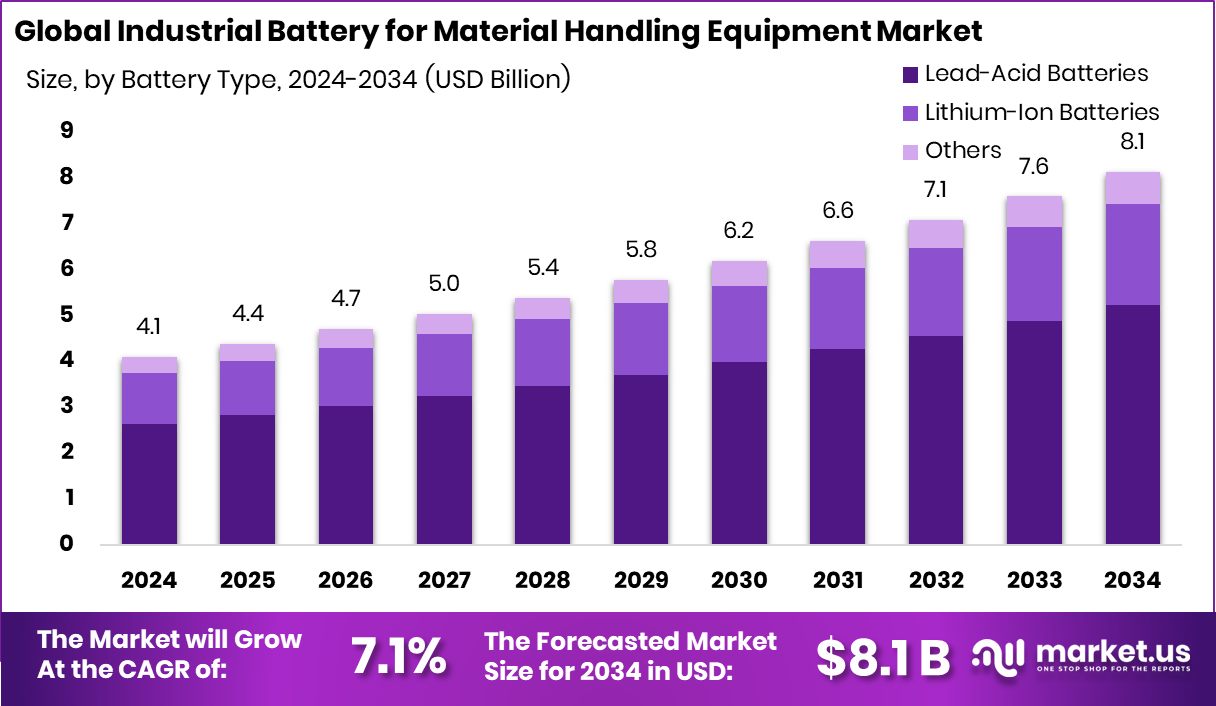

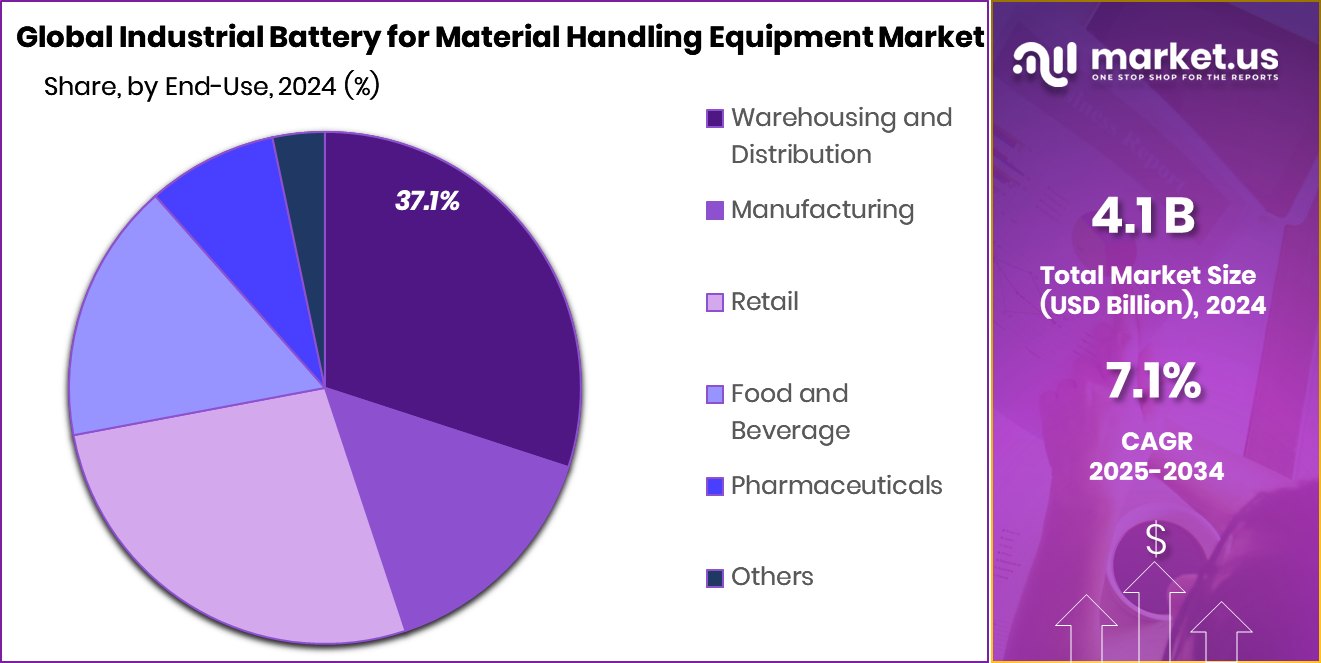

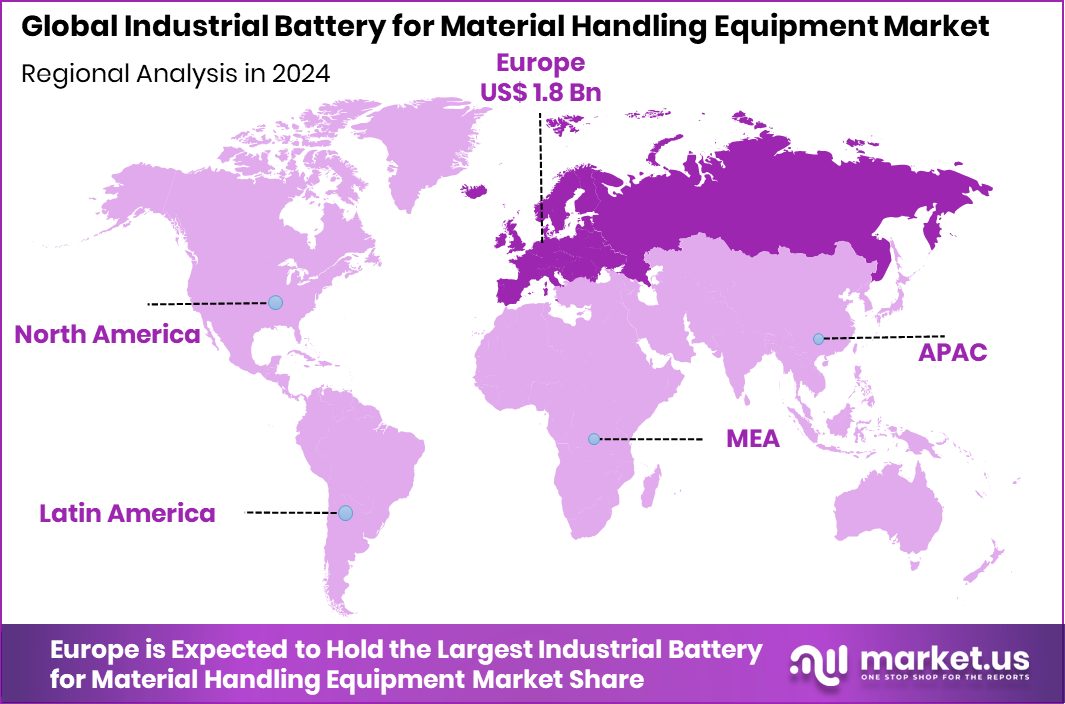

Global Industrial Battery for Material Handling Equipment Market is expected to be worth around USD 8.1 billion by 2034, up from USD 4.1 billion in 2024, and grow at a CAGR of 7.1% from 2025 to 2034. Industrial battery sales in Europe hit USD 1.8 Bn, holding 45.3% share.

An industrial battery for material handling equipment is a power source designed specifically for devices used in the movement, storage, control, and protection of materials, goods, and products throughout the process of manufacturing, distribution, consumption, and disposal.

These batteries are crucial in powering a wide range of equipment, including forklifts, electric pallet jacks, and automated guided vehicles (AGVs), among others. They are engineered to offer high durability and efficiency in industrial environments, ensuring reliable performance over long operational periods.

According to the Geological Survey of India (GSI) and mining officials, the lithium deposits in these reserves are large enough to supply nearly 80% of India’s overall demand. The cumulative demand for energy storage in India is projected to reach 903 GWh by 2030, distributed across technologies such as lithium-ion batteries, redox flow batteries, and solid-state batteries.

The lithium-ion battery market in India is expected to grow at a CAGR of 50%, increasing from 20 GWh in 2022 to 220 GWh by 2030. To support this growth, the government has invested around US$ 2.5 billion in an incentive scheme aimed at establishing a local manufacturing capacity of 50 GWh of Advanced Chemistry Cell (ACC) and 5 GWh of niche ACC capacity (planned).

The programme is designed to boost exports and create economies of scale, enabling large domestic and international manufacturers to build a competitive ACC battery production ecosystem in India.

The Indian government has launched several initiatives to bolster domestic battery manufacturing. The National Programme on Advanced Chemistry Cell (ACC) Battery Storage, approved in 2021 with a budgetary outlay of INR 18,100 crore, aims to establish giga-scale ACC and battery manufacturing facilities in India.

Additionally, the Union Budget for FY2025- 26 introduced customs duty exemptions on 35 capital goods used in EV battery manufacturing, aiming to reduce production costs and encourage local manufacturing.

Key Takeaways

- Global Industrial Battery for Material Handling Equipment Market is expected to be worth around USD 8.1 billion by 2034, up from USD 4.1 billion in 2024, and grow at a CAGR of 7.1% from 2025 to 2034.

- Lead-Acid Batteries dominate with a 64.3% share, preferred for their reliability and cost-effectiveness.

- Batteries ranging from 301 Ah to 800 Ah hold a 47.4% market share, supporting medium to high-capacity needs.

- Forklifts represent the largest application area, commanding a 52.8% market share due to widespread use.

- Warehousing and Distribution lead in end-use, with a 37.1% share, driven by the growth in e-commerce.

- Strong warehouse automation in Europe drives 45.3% market share, reaching USD 1.8 Bn.

By Battery Type Analysis

Lead-Acid Batteries dominate, holding 64.3% market share in robust applications.

In 2024, Lead-Acid Batteries held a dominant market position in the By Battery Type segment of the Industrial Battery for Material Handling Equipment Market, with a 64.3% share. These batteries remained a preferred choice due to their cost-effectiveness, wide availability, and reliable performance in heavy-duty industrial operations.

Their robust design and ability to handle deep discharge cycles make them ideal for forklifts and other handling equipment that operate in intense warehouse and logistics environments. The demand was notably strong in medium-to-large warehouses where cost control and durability are critical factors in equipment procurement.

While lithium-ion batteries are gaining traction, the adoption curve remains gradual due to higher upfront costs, especially across price-sensitive industrial setups. The dominance of lead-acid in 2024 underscores the market’s continued reliance on proven battery systems for operational consistency, despite rising interest in next-gen alternatives.

By Battery Capacity Analysis

Battery capacity between 301 Ah to 800 Ah captures 47.4% market share.

In the By Battery Capacity segment, batteries with a 301 Ah to 800 Ah rating captured a 47.4% market share, indicating a strong preference for medium-to-high-capacity batteries suited for longer operational cycles.

These capacities meet the power requirements of standard forklifts and pallet jacks, minimizing the need for frequent recharging and downtime. The segment saw strong demand from warehousing hubs handling high-throughput logistics, where uptime and energy stability are key performance metrics.

Such batteries also offer a balance between size, efficiency, and cost, making them a default selection for medium-duty equipment across retail, manufacturing, and freight distribution sectors.

By Application Analysis

Forklifts lead applications with a significant 52.8% of the market share.

In the By Application segment, Forklifts held a commanding 52.8% share, highlighting their widespread use in industrial facilities. These machines are fundamental for loading, unloading, and internal material transfers, and their operational efficiency heavily relies on battery performance.

Forklift batteries are engineered for sustained energy output and durability under repetitive use, and this application segment reflects the core demand driver for the entire market. Additionally, with the growing scale of e-commerce, warehouses increasingly depend on electric forklifts for round-the-clock operations, further solidifying this segment’s lead in 2024.

By End-Use Analysis

Warehousing and Distribution lead end-use, securing 37.1% of market participation.

Warehousing and Distribution led the by-end-use segment with a 37.1% share, emphasizing its crucial role in driving demand. These facilities rely on electric material handling equipment to streamline inventory movement, reduce operational delays, and ensure efficient logistics flow.

Batteries are central to this process, powering forklifts, stackers, and reach trucks used across multi-level racking systems and expansive distribution networks. This dominance is linked to ongoing warehousing expansion across logistics corridors and industrial parks, where battery-powered equipment is increasingly being adopted for sustainability and operational flexibility.

Key Market Segments

By Battery Type

- Lead-Acid Batteries

- Lithium-Ion Batteries

- Others

By Battery Capacity

- Up to 300 Ah

- 301 Ah to 800 Ah

- Above 800 Ah

By Application

- Forklifts

- Automated Guided Vehicles (AGVs)

- Reach Trucks

- Pallet Jacks

- Warehouse Management Systems

- Others

By End-Use

- Warehousing and Distribution

- Manufacturing

- Retail

- Food and Beverage

- Pharmaceuticals

- Others

Driving Factors

Growing E-Commerce Warehousing Demands Electric Battery Solutions

One of the biggest drivers of the Industrial Battery for Material Handling Equipment Market is the rapid growth of e-commerce. As online shopping increases, more warehouses and distribution centers are needed to store and move goods. These large facilities use electric forklifts and automated systems that depend on strong and reliable batteries.

Lead-acid and lithium-ion batteries are commonly used to power this equipment. Since e-commerce businesses operate around the clock, they need high-capacity, long-lasting battery systems to support their work.

As a result, battery-powered material handling solutions are becoming more popular than fuel-based systems, which are noisy and need more maintenance. This shift is boosting demand for industrial batteries across warehousing and logistics operations globally.

Restraining Factors

High Battery Replacement Costs Limit Market Adoption

One major challenge in the Industrial Battery for Material Handling Equipment Market is the high cost of battery replacement. Batteries used in forklifts, pallet jacks, and other handling equipment often have a limited life span, especially when used in tough, nonstop operations.

Replacing these industrial batteries can be expensive, especially for small and medium-sized businesses. In some cases, the cost of new batteries may make companies delay upgrades or avoid switching to electric handling systems.

This cost burden also includes regular maintenance and the need for trained staff to manage battery health. Because of these financial pressures, businesses may stick with older, fuel-based systems, even if electric options are more eco-friendly and efficient in the long run.

Growth Opportunity

Ultra-Fast Charging Batteries Revolutionize Warehouse Operations

A significant growth opportunity in the Industrial Battery for Material Handling Equipment Market lies in the development of ultra-fast charging battery technologies. Companies like Nyobolt are pioneering advancements that enable electric vehicles and warehouse robots to charge from 10% to 80% in under five minutes.

This rapid charging capability is particularly beneficial for autonomous warehouse robots and heavy-duty vehicles that operate around the clock, minimizing downtime and enhancing productivity. Nyobolt’s technology, which utilizes a graphite anode system, is designed to meet the high energy demands of continuous operations.

By licensing this technology to existing battery manufacturers, Nyobolt aims to accelerate the adoption of fast-charging solutions across various industries. As e-commerce and logistics sectors continue to expand, the demand for efficient, quick-charging battery systems is expected to grow, presenting a substantial opportunity for innovation and market growth in industrial battery applications.

Latest Trends

Shift Towards Lithium-Ion Batteries Accelerates Market Growth

A significant trend in the industrial battery market for material handling equipment is the increasing adoption of lithium-ion batteries. While lead-acid batteries have been the traditional choice, lithium-ion technology is gaining popularity due to its advantages.

These batteries offer longer lifespans, faster charging times, and require less maintenance, making them ideal for operations that run continuously. Despite their higher initial cost, many companies are transitioning to lithium-ion batteries to enhance efficiency and reduce downtime. This shift is particularly evident in sectors like e-commerce and logistics, where rapid and reliable operations are crucial.

Regional Analysis

Europe leads the Industrial Battery Market with a 45.3% share, worth USD 1.8 Bn.

In 2024, Europe held the dominant position in the Industrial Battery for Material Handling Equipment Market, accounting for 45.3% share valued at USD 1.8 billion. The region’s strong foothold is backed by advanced logistics infrastructure, widespread warehouse automation, and increased adoption of electric material handling equipment across Germany, France, and the UK.

North America followed closely, supported by high industrial activity and the expansion of e-commerce fulfillment centers using battery-powered forklifts and pallet trucks. In the Asia Pacific region, growing manufacturing hubs in China, India, and Southeast Asia are steadily increasing the demand for industrial batteries, especially in high-density logistics zones.

Meanwhile, the Middle East & Africa region is seeing gradual growth due to infrastructure investments and rising warehousing needs across the Gulf Cooperation Council (GCC) countries. Latin America, though smaller in share, is experiencing slow but steady adoption of battery-operated material handling systems in Brazil and Mexico.

Europe’s dominance is expected to continue due to its early shift towards electric mobility within industrial logistics, pushing demand for efficient battery solutions in the warehousing and distribution sectors. The regional spread highlights how developed economies are leading adoption, while emerging markets are steadily aligning with global electrification trends in industrial operations.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Trojan Battery continued to reinforce its position as a key player in the industrial battery segment, particularly for material handling equipment. Known for its deep-cycle lead-acid batteries, Trojan remains a preferred choice in warehouse forklifts and pallet trucks. The company focused on enhancing battery longevity and optimizing charge-discharge efficiency, targeting high-usage environments such as distribution centers and logistics hubs.

Valence Technology, with its core strength in lithium iron magnesium phosphate (LiFeMgPO4) chemistry, gained traction in high-performance applications where weight, fast charging, and low maintenance are priorities. In 2024, Valence expanded its footprint in Asia Pacific and Europe, offering modular battery systems for electric material handling vehicles. Its batteries provided longer cycle life, stable thermal performance, and integrated battery management systems (BMS), addressing increasing safety and efficiency demands in automated warehouse systems.

Exide, a long-established brand, remained a competitive force by offering both lead-acid and lithium battery technologies. The company’s strong service network and reliable battery solutions made it a favored partner for industrial fleet operators. In 2024, Exide emphasized sustainability by promoting recyclable battery products and advancing energy-efficient charging systems tailored for high-capacity forklifts.

Top Key Players in the Market

- Trojan Battery

- Valence Technology

- Exide

- Crown Battery

- EverExceed

- HOPPECKE

- MIDAC Batteries

- Navitas System

- BYD Company Limited

- East Penn Manufacturing Co., Inc.

- EnerSys

- GS Yuasa Corporation

- Johnson Controls International plc

- Panasonic Corporation

- Saft

Recent Developments

- In March 2025, Trojan introduced the Lithium OnePack™ XR, a 48V, 171Ah lithium-ion battery pack. Designed for golf carts and low-speed vehicles, it offers up to 75 miles on a single charge, enhancing range by approximately 30 miles compared to standard 105Ah batteries.

- In October 2024, Introduced the Solition battery, a lithium iron phosphate solution designed for forklifts and automated guided vehicles (AGVs). It offers over 98% charging efficiency and a lifespan of up to 4,000 cycles, enhancing reliability and reducing operational costs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.1 Billion |

| Forecast Revenue (2034) | USD 8.1 Billion |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery Type (Lead-Acid Batteries, Lithium-Ion Batteries, Others), By Battery Capacity (Up to 300 Ah, 301 Ah to 800 Ah, Above 800 Ah), By Application (Forklifts, Automated Guided Vehicles (AGVs), Reach Trucks, Pallet Jacks, Warehouse Management Systems, Others), By End-Use (Warehousing and Distribution, Manufacturing, Retail, Food and Beverage, Pharmaceuticals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Trojan Battery, Valence Technology, Exide, Crown Battery, EverExceed, HOPPECKE, MIDAC Batteries, Navitas System, BYD Company Limited, East Penn Manufacturing Co., Inc., EnerSys, GS Yuasa Corporation, Johnson Controls International plc, Panasonic Corporation, Saft |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |