Quick Navigation

Report Overview

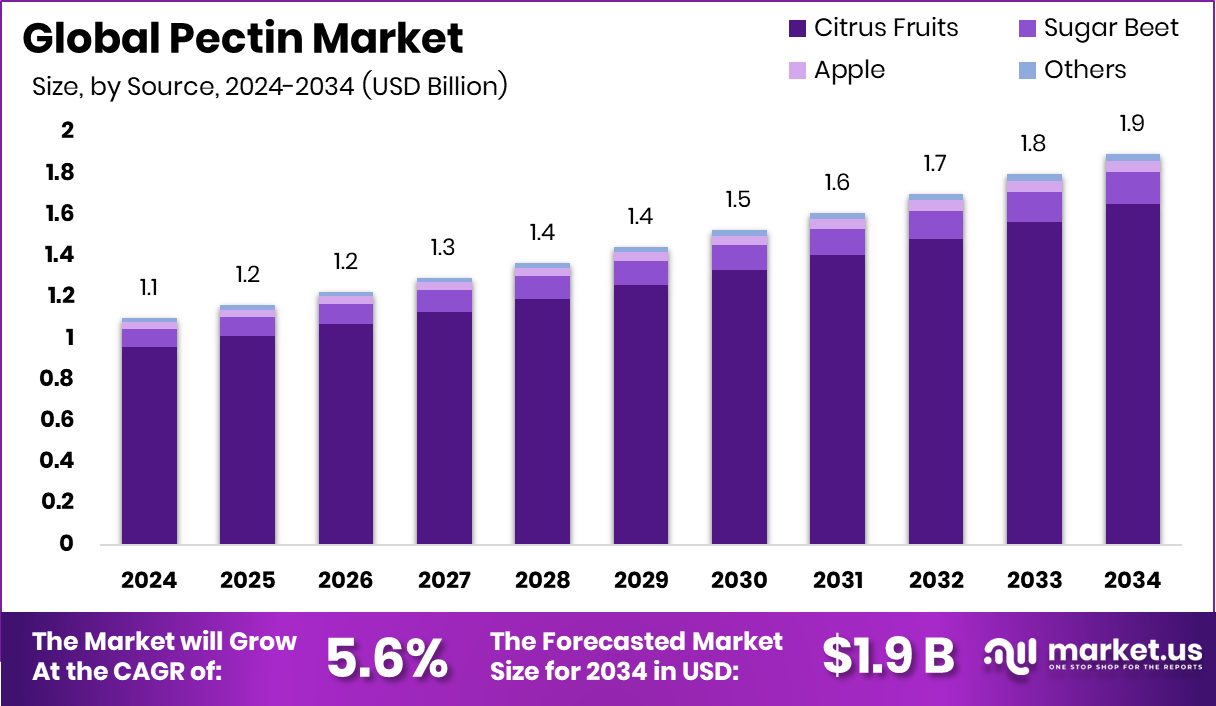

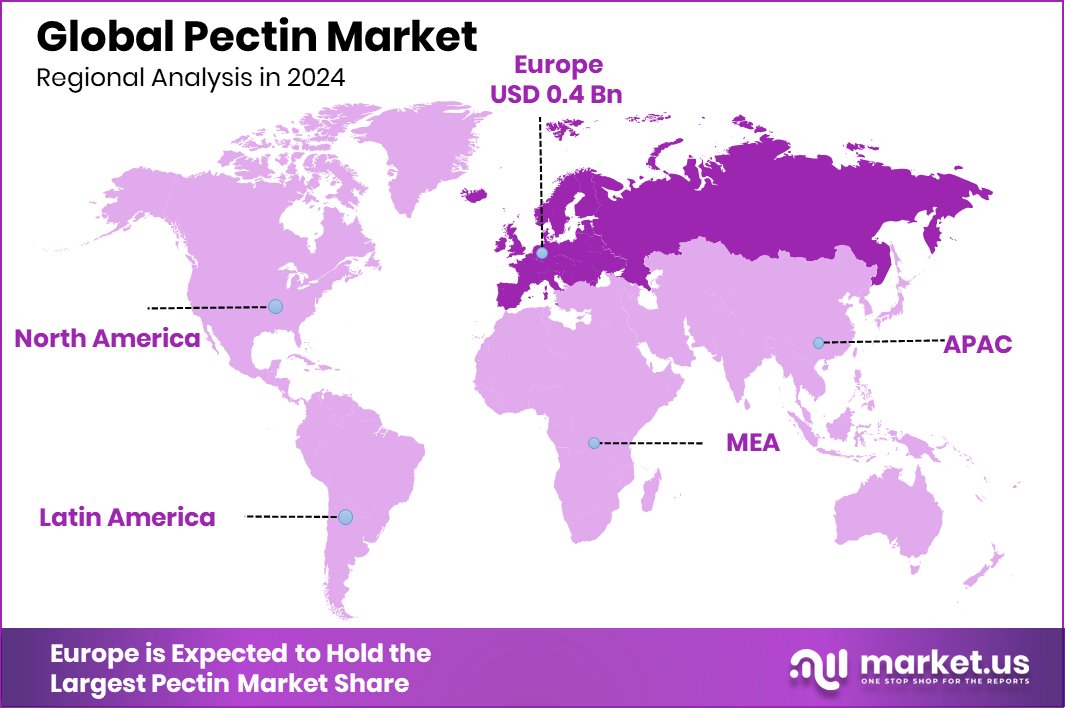

Global Pectin Market is expected to be worth around USD 1.9 billion by 2034, up from USD 1.1 billion in 2024, and grow at a CAGR of 5.6% from 2025 to 2034. The European Pectin Market holds a 43.9% share, generating USD 0.4 billion in revenue.

Pectin is a naturally occurring polysaccharide found in the cell walls of fruits and vegetables, primarily apples and citrus fruits. It is widely used as a gelling agent, stabilizer, and thickener in food products such as jams, jellies, dairy products, and confectionery. Pectin also finds applications in the pharmaceutical and cosmetic industries due to its functional properties, including its ability to form gels and its prebiotic effects on gut health.

The pectin market has been experiencing steady growth driven by rising demand for natural and clean-label food ingredients. Consumers increasingly seek plant-based, allergen-free, and organic food products, propelling the use of pectin as a natural additive in various food and beverage applications. Moreover, the shift towards healthier lifestyles has fueled demand for low-sugar and sugar-free products, further boosting pectin’s role as a gelling and thickening agent in reduced-sugar formulations.

Demand for pectin is also fueled by the increasing use of functional foods and dietary supplements. Pectin is recognized for its prebiotic properties, aiding in gut health and digestive wellness. The growing awareness about the health benefits of dietary fibers and plant-based ingredients is propelling the adoption of pectin in nutraceuticals, beverages, and fortified foods.

Commercial pectins are derived from apple and citrus fruits, with apple pomace containing 10–15% pectin and citrus peel holding 20–30% pectin by dry mass. India ranks as the world’s second-largest fruit producer, generating approximately 25-30% waste during fruit processing.

Key Takeaways

- Global Pectin Market is expected to be worth around USD 1.9 billion by 2034, up from USD 1.1 billion in 2024, and grow at a CAGR of 5.6% from 2025 to 2034.

- In the Pectin Market, citrus fruits remain the dominant source, accounting for 87.2% share.

- High methoxyl pectin leads the type segment, capturing a significant 67.4% of market demand.

- As a gelling agent, pectin holds a strong position, contributing to 37.9% of market usage.

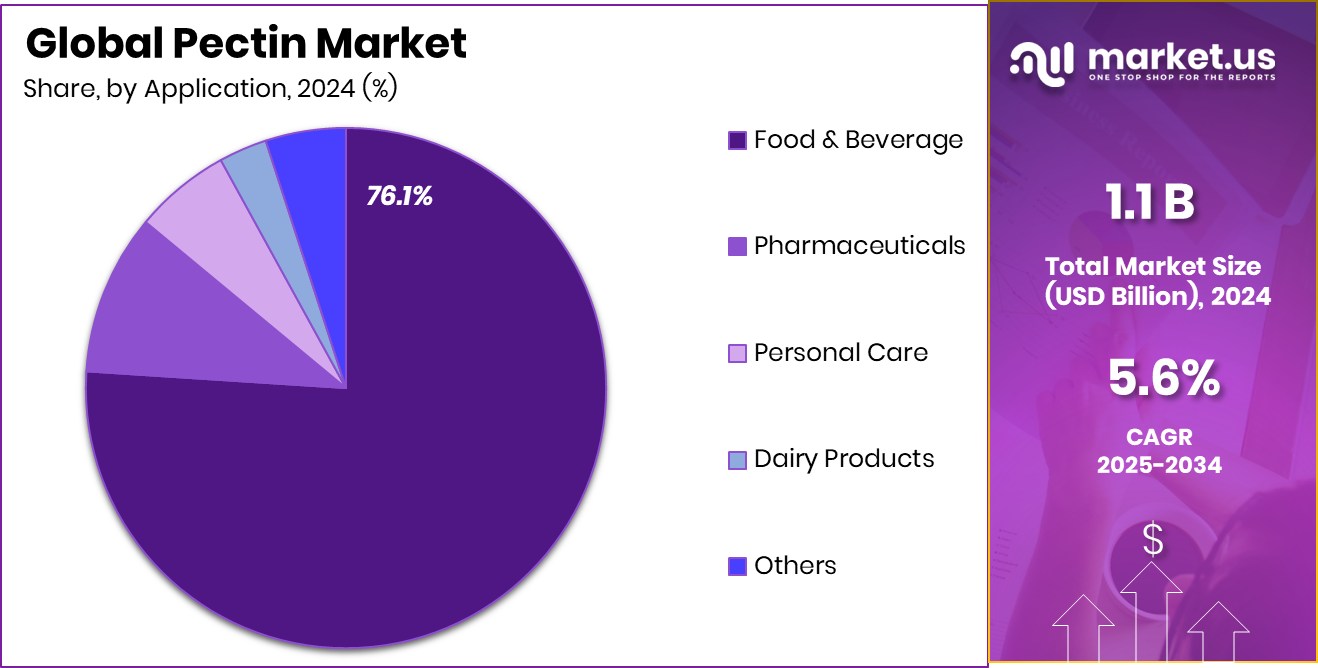

- Food and beverage applications dominate the pectin market, with a commanding 76.1% market share globally.

- USD 0.4 billion in Europe, representing 43.9% of the global Pectin Market.

By Source Analysis

Citrus fruits dominate the pectin market, accounting for 87.2% of the source.

In 2024, Citrus Fruits held a dominant market position in the By Source segment of the Pectin Market, with an 87.2% share. This dominance is attributed to the widespread use of citrus-based pectin in various food and beverage applications, particularly as a gelling and stabilizing agent.

The substantial share underscores the rising preference for natural and plant-based ingredients, with citrus fruits being a primary source of pectin extraction. The high pectin content in citrus peels has positioned them as a cost-effective and abundant raw material, further strengthening their market hold.

Additionally, the increasing adoption of citrus-derived pectin in dairy products, confectioneries, and pharmaceuticals continues to drive its demand, consolidating its leadership position in the source segment.

Ву Туре Analysis

High Methoxyl Pectin leads the pectin market, capturing a 67.4% share.

In 2024, High Methoxyl Pectin held a dominant market position in the By Type segment of the Pectin Market, with a 67.4% share. This substantial share is driven by its widespread use in food products requiring high sugar content and acidic conditions, such as jams, jellies, and fruit preserves.

High Methoxyl Pectin is favored for its ability to form strong gels at lower pH levels, making it a preferred choice for traditional fruit-based spreads and confectioneries. The segment’s dominance is further reinforced by the increasing consumer demand for natural and clean-label products, as High Methoxyl Pectin is derived from plant-based sources like citrus peels and apple pomace.

Its functional properties, such as stabilizing, thickening, and gelling, make it indispensable in the production of premium fruit fillings and yogurt products. This dominance in the By Type segment underscores its pivotal role in maintaining the texture and consistency of processed foods while catering to evolving consumer preferences for plant-based, natural ingredients.

By Function Analysis

Gelling agents hold a 37.9% share, driving pectin’s functional applications globally.

In 2024, Gelling Agent held a dominant market position in the By Function segment of the Pectin Market, with a 37.9% share. This significant share is primarily driven by the extensive use of pectin as a gelling agent in various food and beverage applications, including jams, jellies, and fruit preserves.

Pectin’s unique ability to form gels in the presence of sugar and acid makes it a preferred ingredient for creating desired textures and consistency in processed foods. The growing demand for natural and plant-based food additives has further propelled the adoption of pectin as a gelling agent, particularly in confectioneries and bakery products.

Additionally, the increasing popularity of low-calorie and reduced-sugar formulations has boosted the demand for pectin-based gelling agents, which provide texture and stability without compromising taste. This segment’s strong position highlights the expanding utilization of pectin in functional foods and beverages, as manufacturers aim to enhance product quality while meeting consumer preferences for natural and clean-label ingredients.

By Application Analysis

Food and Beverage sector commands 76.1% of the pectin market application share.

In 2024, Food and Beverage held a dominant market position in the By Application segment of the Pectin Market, with a 76.1% share. This significant share underscores the widespread utilization of pectin as a stabilizing, thickening, and gelling agent in various food products such as jams, jellies, confectioneries, and dairy desserts. The increasing demand for natural and plant-based ingredients in processed foods has propelled the adoption of pectin, particularly in fruit-based spreads and low-sugar beverages.

Additionally, the rising preference for clean-label and minimally processed food products has further driven the application of pectin in bakery and confectionery segments, where it serves as a critical ingredient in maintaining texture and consistency.

The dominance of the Food and Beverage segment also reflects the growing consumer inclination towards healthier and low-calorie formulations, leading manufacturers to leverage pectin as a functional additive to enhance product stability and shelf life. This robust share in the application segment highlights pectin’s expanding role in food processing, driven by its versatile functional properties and alignment with evolving dietary trends.

Key Market Segments

By Source

- Citrus Fruits

- Sugar Beet

- Apple

- Others

Ву Туре

- High Methoxyl Pectin

- Low Methoxyl Pectin

By Function

- Thickener

- Stabilizer

- Gelling Agent

- Fat Replacer

- Others

By Application

- Food and Beverage

- Jam, Jelly, and Preserve

- Baked Goods

- Dairy Products

- Others

- Pharmaceuticals

- Personal Care

- Dairy Products

- Others

Driving Factors

Rising Demand for Natural Ingredients in Food Products

The increasing consumer preference for natural and plant-based ingredients is significantly driving the pectin market. Pectin, derived primarily from citrus fruits and apples, is gaining traction as a natural stabilizer and gelling agent in food and beverage products. As health-conscious consumers seek cleaner labels and minimally processed foods, manufacturers are increasingly incorporating pectin to enhance product texture and shelf life.

Additionally, the surge in demand for low-sugar and reduced-fat products has further elevated pectin’s importance, particularly in jams, jellies, and dairy desserts. This growing inclination towards natural additives positions pectin as a vital component in the evolving food processing landscape, boosting its market demand.

Restraining Factors

High Production Costs Limit Market Expansion Potential

The pectin market faces challenges due to the high cost of raw materials and extraction processes. Sourcing quality citrus peels and apple pomace, the primary pectin sources, involves substantial expenses, particularly with fluctuating fruit prices. Additionally, the extraction process requires advanced technology and significant energy consumption, further increasing production costs.

These factors contribute to the high pricing of pectin, making it less accessible for small-scale manufacturers. As a result, some producers seek synthetic or less costly alternatives, impacting pectin’s market penetration. Addressing these cost-related challenges is crucial for maintaining competitiveness and ensuring broader adoption across various food and beverage applications.

Growth Opportunity

Expanding Applications in Plant-Based Food Products

The growing popularity of plant-based diets presents a significant growth opportunity for the pectin market. As more consumers shift towards vegan and vegetarian lifestyles, demand for plant-based food products has surged, increasing the need for natural stabilizers like pectin.

Pectin’s ability to provide texture and gelling properties without animal-derived ingredients makes it a preferred choice in dairy alternatives, plant-based desserts, and meat substitutes.

Moreover, as food manufacturers seek clean-label solutions, pectin’s natural origin and functional versatility align well with evolving consumer preferences. This trend is expected to drive the expansion of pectin applications beyond traditional jams and jellies, boosting market demand.

Latest Trends

Consumer Demand for Clean Label Pectin Products Rises

Consumers are increasingly seeking natural and clean label products, driving the demand for pectin derived from organic sources. Pectin manufacturers are focusing on producing pectin without synthetic additives or chemical modifications, aligning with the clean label trend. This shift is evident in the food and beverage sector, where clean label pectin is gaining traction as a gelling agent in jams, jellies, and dairy products.

Additionally, the surge in plant-based and vegan products is boosting the demand for pectin as a natural alternative to gelatin. As more consumers prioritize health and transparency, the market for clean-label pectin is expected to witness significant growth in the coming years.

Regional Analysis

Europe leads the Pectin Market with 43.9% share, valued at USD 0.4 billion.

In 2024, Europe held a dominant position in the Pectin Market, capturing 43.9% of the market share and generating USD 0.4 billion in revenue. This stronghold is attributed to the extensive use of pectin in the food and beverage industry, particularly in bakery and confectionery products, jams, and dairy applications.

North America follows closely, with increasing demand for pectin in plant-based and vegan products, driven by rising health-conscious consumer trends. The Asia Pacific region is witnessing steady growth due to the expanding food processing sector and the incorporation of pectin as a natural thickening agent in beverages and snacks.

Meanwhile, the Middle East & Africa and Latin America showcase moderate demand, with pectin applications growing in the confectionery and bakery sectors as manufacturers explore cost-effective natural ingredients.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Cargill, Inc. maintained a significant presence in the global pectin market, leveraging its established network and expertise in food ingredients. The company emphasized expanding its pectin product portfolio to cater to the growing demand for clean-label and plant-based products, aligning with consumer preferences for natural ingredients. Cargill’s strategic focus on sustainable sourcing and advanced extraction techniques further strengthened its market position, enhancing product quality and meeting regulatory standards.

CEAMSA continued to solidify its standing as a leading pectin supplier, particularly in Europe, where it capitalized on the rising demand for fruit-derived pectin in confectionery and bakery applications. The company’s commitment to expanding its production capacity and refining extraction processes positioned it well to address the increasing need for high-performance pectin in functional food products.

CP Kelco USA, Inc., a prominent player in the U.S. market, focused on innovation and product diversification to meet the evolving requirements of food manufacturers. Its emphasis on low-sugar and vegan formulations contributed to expanding its customer base, particularly in the beverage and dairy sectors. Additionally, CP Kelco’s investment in research and development enabled the company to introduce new pectin variants tailored for specific applications, reinforcing its competitive edge in the global market.

Top Key Players in the Market

- Cargill, Inc.

- CEAMSA

- CP Kelco USA, Inc.

- DuPont Inc.

- Herbstreith & Fox Corporate Group

- Ingredion Incorporated

- Koninklijke DSM N.V.

- Lucid Colloids Ltd

- Naturex Group

- Quadra Chemicals

- Silvateam S.p.A

- Tate & Lyle PLC

- Yantai Andre Pectin Co. Ltd.

Recent Developments

- In February 2025, Ingredion Incorporated, Ingredion revealed plans for a $48.5 million expansion of its Cedar Rapids facility. The project includes updating starch flash dryer technology and constructing new industrial buildings, which will significantly increase efficiency and capacity for starch product delivery.

- In December 2024, Tate & Lyle announced a partnership with BioHarvest Sciences to develop the next generation of plant-based ingredients using BioHarvest’s Botanical Synthesis technology. This collaboration aims to produce non-GMO, plant-derived ingredients in a more sustainable and economically viable way, potentially impacting the development of future pectin products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.1 Billion |

| Forecast Revenue (2034) | USD 1.9 Billion |

| CAGR (2025-2034) | 5.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Citrus Fruits, Sugar Beet, Apple, Others), Ву Туре (High Methoxyl Pectin, Low Methoxyl Pectin), By Function (Thickener, Stabilizer, Gelling Agent, Fat Replacer, Others), By Application (Food and Beverage (Jam, Jelly, and Preserve, Baked Goods, Dairy Products, Others), Pharmaceuticals, Personal Care, Dairy Products, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Cargill, Inc., CEAMSA, CP Kelco USA, Inc., DuPont Inc., Herbstreith & Fox Corporate Group, Ingredion Incorporated, Koninklijke DSM N.V., Lucid Colloids Ltd, Naturex Group, Quadra Chemicals, Silvateam S.p.A, Tate & Lyle PLC, Yantai Andre Pectin Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |