Quick Navigation

Report Overview

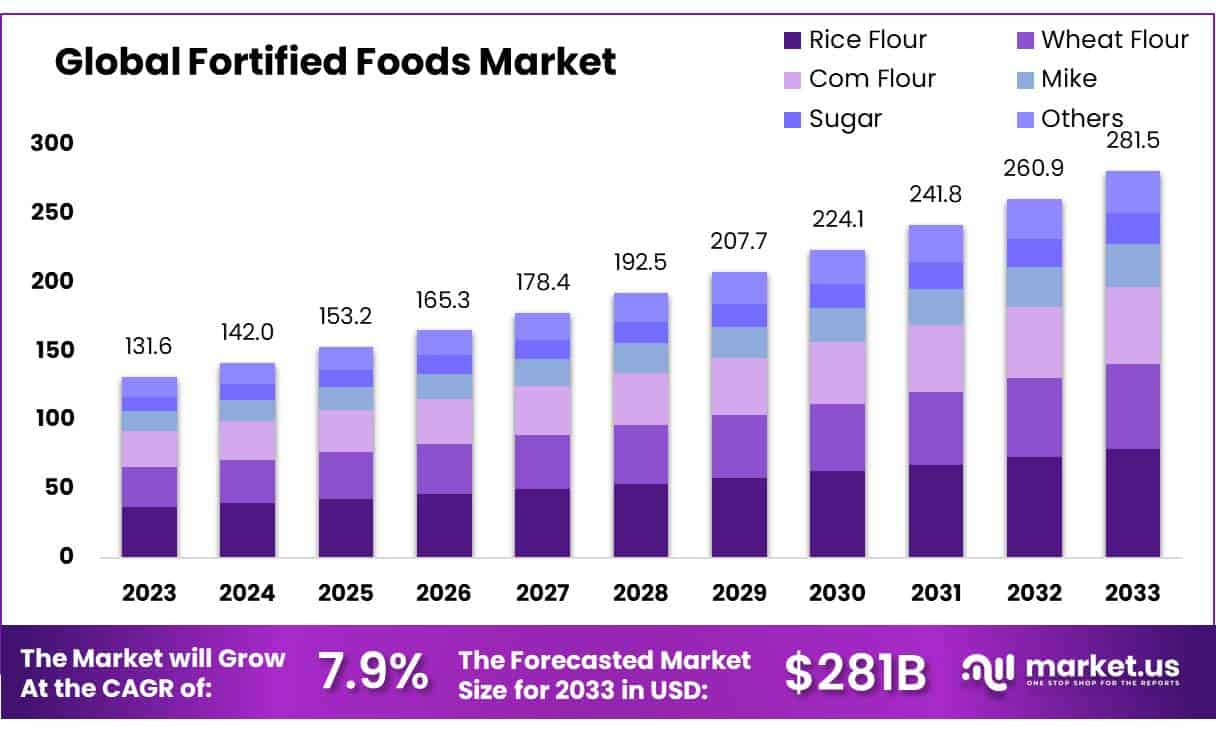

The Global Fortified Foods Market size is expected to be worth around USD 281.5 Bn by 2033, from USD 131.6 Bn in 2023, growing at a CAGR of 7.9% during the forecast period from 2024 to 2033.

Fortified foods are those that have added essential nutrients, such as vitamins and minerals, to prevent or address nutritional deficiencies. These nutrients, which may include vitamin D, calcium, iron, and folic acid, are often added during food processing.

The main goal of fortification is to improve public health by ensuring individuals receive the necessary nutrients, even if their regular diet is lacking in certain areas. This is particularly important in regions where diets may not naturally contain enough of these vital nutrients.

Government Regulations and Initiatives have been crucial in driving the adoption of fortified foods. Many countries have implemented mandatory fortification programs to combat micronutrient deficiencies. For example, in the United States, iodine was added to salt in the 1920s, helping eliminate iodine deficiency.

Globally, the World Health Organization (WHO) supports fortifying staple foods like rice and wheat flour with essential nutrients, especially in low- and middle-income countries. In India, the government launched a fortification initiative in 2021 to add iron, folic acid, and vitamin B12 to wheat flour and rice.

This initiative addresses iron deficiency anemia, a condition affecting over 50% of the Indian population, with an estimated 63 million women affected by inadequate iron intake, according to UNICEF.

Import-Export and Regional Growth trends also highlight the increasing demand for fortified foods. In 2023, Asia-Pacific accounted for over 35% of the global fortified foods market share, driven by rising awareness and expanding middle-class populations in countries like China, India, and Indonesia. China’s imports of fortified foods rose by 18%, while India’s imports of fortified oils and grains increased by 22%.

Private Sector Expansion and Partnerships have also contributed to market growth. Companies like Danone and General Mills are expanding their fortified food portfolios through acquisitions and partnerships.

Danone’s acquisition of WhiteWave Foods in 2020 for USD 12.5 billion allowed it to strengthen its presence in the health-focused food sector. In 2023, General Mills partnered with the Global Alliance for Improved Nutrition (GAIN) to increase the availability of fortified foods in sub-Saharan Africa, aiming to address regional malnutrition by fortifying products like rice and cereal.

Key Takeaways

- Fortified Foods Market size is expected to be worth around USD 281.5 Bn by 2033, from USD 131.6 Bn in 2023, growing at a CAGR of 7.9%.

- Rice Flour held a dominant market position, capturing more than a 27.2% share.

- Rice Dusting held a dominant market position, capturing more than a 62.2% share.

- Vitamins held a dominant market position, capturing more than a 48.3% share.

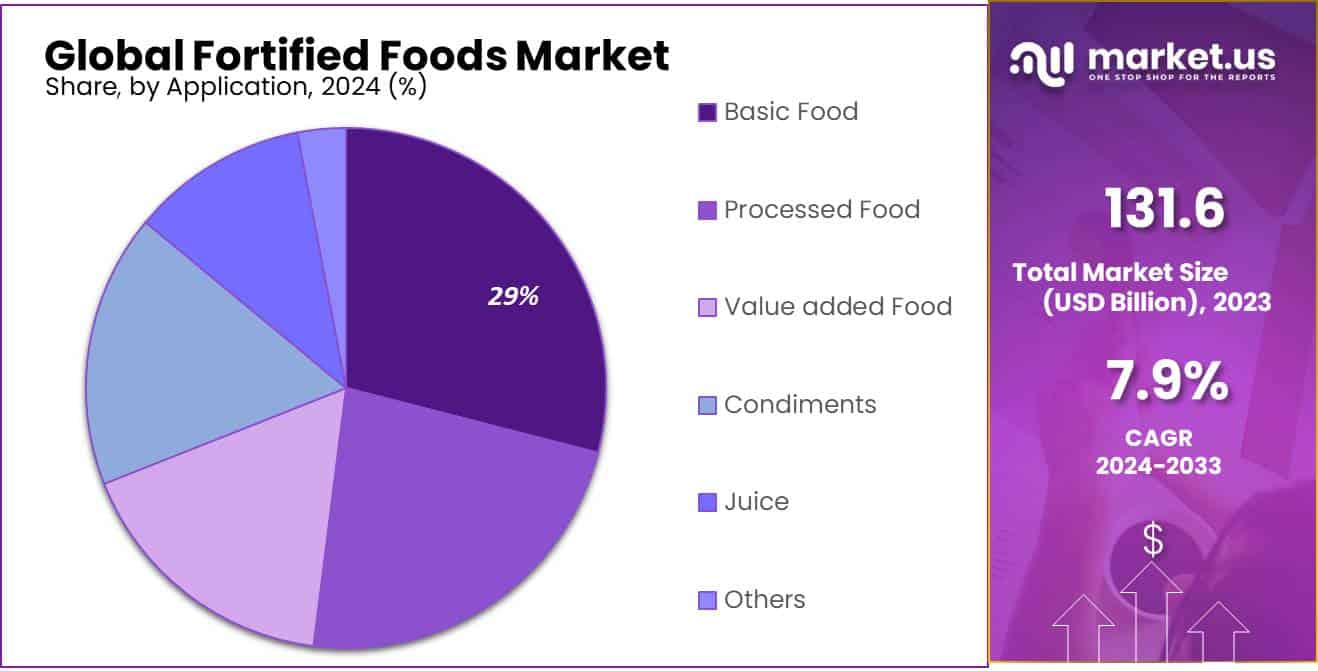

- Basic Food held a dominant market position, capturing more than a 29.1% share of the fortified foods market.

- Drying held a dominant market position, capturing more than a 39.1% share of the fortified foods market.

- Modern Trade held a dominant market position, capturing more than a 44.1% share of the fortified foods market.

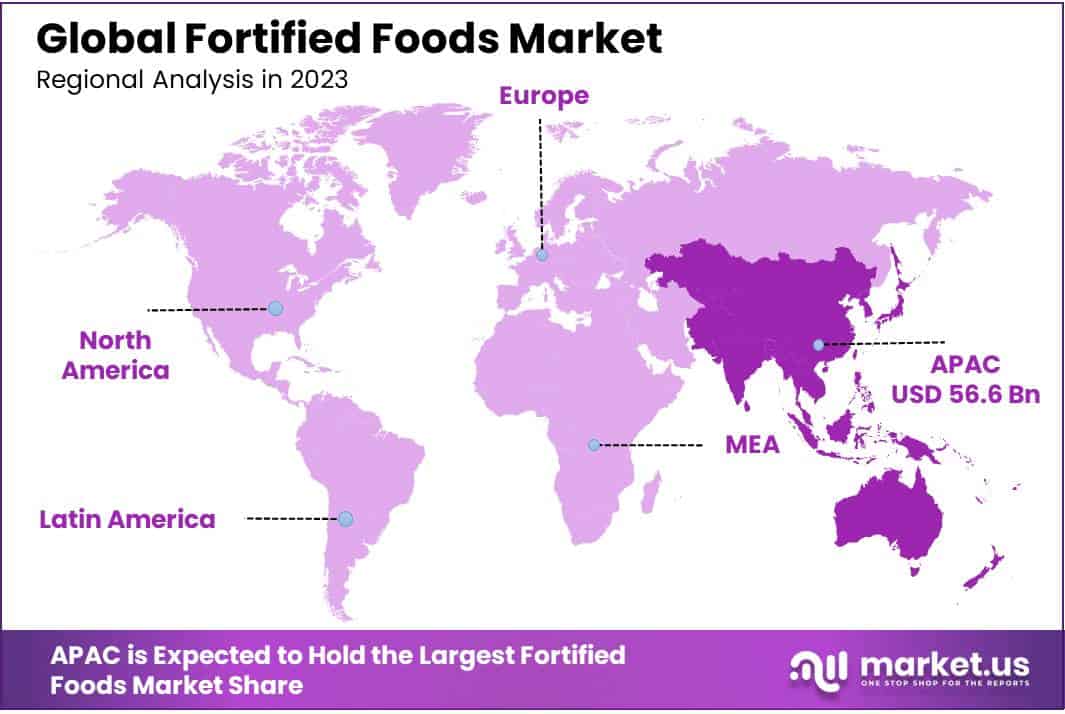

- Asia Pacific (APAC) region dominated the fortified foods market, capturing more than 43% of the global market share, valued at approximately USD 56.6 billion.

By Raw Material

In 2023, Rice Flour held a dominant market position, capturing more than a 27.2% share of the global fortified foods market. This growth can be attributed to rice’s widespread use as a staple food in many regions, especially in Asia-Pacific and Latin America.

The fortification of rice with essential nutrients such as iron, folic acid, and vitamins has been a key strategy for combating micronutrient deficiencies, particularly in countries like India and Vietnam, where rice is a major part of the diet. Government initiatives and public health programs are increasingly focusing on rice fortification to address iron-deficiency anemia and other nutritional deficiencies, driving the demand for fortified rice.

Wheat Flour followed as another significant raw material in the fortified foods market, accounting for a substantial market share in 2023. Wheat flour is widely used for producing bread, pasta, and other bakery products. Many countries have implemented mandatory wheat flour fortification programs to improve public health.

For instance, the United States and Mexico have mandatory fortification laws, which have greatly increased the availability of fortified wheat flour. Iron, folic acid, and vitamin B12 are commonly added to wheat flour, helping to reduce birth defects and improve overall nutrition.

Corn Flour also holds a considerable share, particularly in regions where corn is a primary staple, such as Sub-Saharan Africa and parts of Latin America. Corn flour is often fortified with vitamins and minerals to address deficiencies in rural populations. In regions like Central America, corn flour fortification is a government-driven initiative aimed at reducing micronutrient malnutrition.

By Process

In 2023, Rice Dusting held a dominant market position, capturing more than a 62.2% share of the fortified foods market. This process involves spraying powdered vitamins and minerals onto rice, which is then blended to ensure an even distribution of nutrients. Rice dusting is a cost-effective and efficient method of fortification, making it particularly popular in countries with large populations of rice consumers, such as India, China, and Indonesia.

The process allows for the fortification of staple foods in a way that is both scalable and accessible, reaching a broad consumer base. Government-led initiatives, particularly in Asia-Pacific, have increased the demand for fortified rice to combat nutrient deficiencies like iron deficiency anemia and vitamin A deficiency, which are prevalent in these regions.

Drum Drying, while not as dominant as rice dusting, is another key process used in the fortification of foods. This method is commonly applied to products like milk powder and instant cereals. In drum drying, liquid nutrients are applied to the surface of the food product and then dried to form a powdered version, preserving the stability and bioavailability of the nutrients.

This process is widely used for fortified milk and other dairy products, where vitamins such as vitamin D and vitamin A are added to enhance nutritional value. Drum drying is preferred in markets where dairy products are consumed regularly, including North America and Europe, to ensure that essential nutrients are added without affecting the product’s taste or texture.

By Micronutrients

In 2023, Vitamins held a dominant market position, capturing more than a 48.3% share of the fortified foods market. Vitamins are critical in addressing a wide range of nutritional deficiencies, and their inclusion in fortified foods has become a key strategy to improve public health globally. The most commonly fortified vitamins include vitamin D, vitamin A, vitamin B12, and folic acid, which are vital for immune function, bone health, vision, and the prevention of birth defects.

These vitamins are widely added to staple foods like rice, flour, and milk in regions where deficiencies are prevalent. For example, vitamin D fortification in dairy products has been a longstanding practice in North America, and vitamin A fortification in rice and flour is common in countries like India and Indonesia, where deficiencies are widespread.

Minerals follow closely as a significant micronutrient category in fortified foods, accounting for a substantial share of the market in 2023. Common minerals added to food products include iron, calcium, and zinc. Iron fortification is particularly prominent in countries with high rates of iron-deficiency anemia, such as India, China, and parts of Africa.

Fortifying staple foods like rice, flour, and salt with iron has been a highly effective strategy to reduce anemia rates. Calcium fortification is widely used in dairy products, and it plays a crucial role in bone health, especially in aging populations. The fortification of foods with minerals is especially prominent in Asia-Pacific and Africa, where mineral deficiencies are a major health concern.

By Application

In 2023, Basic Food held a dominant market position, capturing more than a 29.1% share of the fortified foods market. Basic foods, including rice, wheat, and corn flour, are staple ingredients in many diets worldwide. Fortifying these basic food products with essential nutrients like iron, folic acid, vitamin A, and vitamin D has proven to be an effective strategy to combat nutritional deficiencies, especially in developing countries.

In regions such as South Asia, Africa, and parts of Latin America, the fortification of rice and wheat flour is a government-driven initiative aimed at addressing micronutrient malnutrition. These basic food items often serve as the primary source of nutrients for large segments of the population, making fortification an essential tool in public health initiatives.

Processed Food follows as a significant application in the fortified foods market. The growing demand for convenience foods, including ready-to-eat meals, snacks, and instant products, has led to an increase in the fortification of processed food products. Consumers are looking for foods that offer not just convenience but also added nutritional value.

Fortifying processed foods with vitamins, minerals, and other essential nutrients helps meet the growing need for nutrient-dense options. For example, instant noodles, canned soups, and processed meat products are often fortified with iron, vitamins B12, and zinc to boost their nutritional content. The processed food segment continues to grow in North America and Europe, driven by busy lifestyles and increasing consumer awareness of the importance of nutrition.

Value-added Foods, including functional foods and beverages, are also gaining significant market share. These products are designed to provide health benefits beyond basic nutrition, such as improved digestion, heart health, or enhanced immunity. Fortified dairy products, energy bars, and fortified beverages are examples of value-added foods that are increasingly popular among health-conscious consumers.

The rise in plant-based diets and demand for nutrient-dense products has further fueled the growth of this segment. In particular, fortified plant-based milks, protein bars, and snack foods have become essential in the diets of individuals seeking healthier, more functional food options.

Condiments and Juices also represent key application areas for fortified foods. The fortification of condiments like salt with iodine, iron, and folic acid is widely used in regions where deficiencies in these nutrients are prevalent.

Fortified fruit juices, especially orange juice enriched with calcium and vitamin D, are growing in demand due to their convenience and health benefits. These products cater to consumers looking for easy ways to boost their nutrient intake without significantly altering their diets.

By Technology

In 2023, Drying held a dominant market position, capturing more than a 39.1% share of the fortified foods market. Drying is a widely used technology for fortifying staple foods like rice, flour, and grains. The process involves removing moisture from food products while preserving the nutrients added during fortification.

Drying helps extend the shelf life of fortified foods, making them more suitable for long-term storage and distribution. This is particularly important in regions with limited access to fresh food supplies, where fortified dried products can play a key role in addressing nutritional deficiencies.

For instance, fortified rice and instant noodles often undergo drying to ensure they retain the added vitamins and minerals while maintaining their convenience. The drying process is also energy-efficient and cost-effective, making it popular in large-scale fortification programs, especially in Asia-Pacific and Africa, where rice and wheat flour fortification is a government-driven initiative.

Extrusion technology follows as a significant method used in the fortification of processed food products. This technique is often applied to cereal-based snacks, ready-to-eat cereals, and protein bars. In extrusion, ingredients are mixed, heated, and forced through a machine that shapes them into various forms. Fortification occurs during the extrusion process, where essential nutrients such as vitamins, minerals, and fiber are added.

Extrusion helps retain the nutritional content of the added nutrients and enhances the texture and digestibility of the final product. This technology is widely used in the production of fortified breakfast cereals and snack foods that cater to health-conscious consumers. The demand for healthier snack options has been rising, particularly in North America and Europe, driving the growth of extrusion technology in the fortified foods sector.

Coating & Encapsulation technology is also increasingly used for fortifying foods. This method involves coating food particles with a thin layer of material, which helps protect the added nutrients from degradation during processing and storage. Encapsulation is especially effective for sensitive nutrients like omega-3 fatty acids and probiotics, which can lose their efficacy when exposed to heat or light.

By using coating or encapsulation, manufacturers can ensure that these nutrients remain stable and are released at the right time during digestion. This technology is widely applied in fortified dairy products, beverages, and functional foods. It is particularly useful in the production of fortified drinks, vitamin-enriched gummies, and energy bars, which have become popular as convenient, nutrient-rich options.

By Sales Channel

In 2023, Modern Trade held a dominant market position, capturing more than a 44.1% share of the fortified foods market. Modern trade refers to large, organized retail formats such as supermarkets, hypermarkets, and chain stores. These retail outlets are significant in the distribution of fortified food products because they offer consumers a wide range of options in one location.

The growth of modern trade has been particularly pronounced in developed markets like North America and Europe, where consumers prefer the convenience of one-stop shopping. Large retail chains also play an important role in the awareness and promotion of fortified foods, offering in-store promotions and discounts that attract health-conscious consumers.

Additionally, modern trade retailers often have strong relationships with manufacturers, enabling better shelf space and visibility for fortified products. As the demand for healthier and nutrient-dense food options grows, modern trade will continue to be a key channel for the distribution of fortified foods.

Online Sales is another rapidly growing sales channel for fortified foods. The increasing trend of online shopping has made it easier for consumers to purchase fortified products directly from the comfort of their homes. Online platforms like Amazon, Walmart, and specialty health-focused websites have become essential channels for the distribution of fortified foods.

In 2023, online sales accounted for a significant portion of the market, as consumers seek convenient access to fortified food products, especially those that may not be readily available in physical stores. This shift towards e-commerce is also driven by the rise of mobile commerce, with consumers increasingly purchasing fortified foods through smartphones and other mobile devices.

The Asia-Pacific region, in particular, has seen a surge in online food sales, with platforms like Alibaba and JD.com playing a significant role in expanding the reach of fortified food products.

Neighbourhood Stores, such as local grocery stores and independent shops, also contribute to the fortified foods market but hold a smaller share compared to modern trade and online sales. These stores provide convenience for consumers seeking everyday fortified products such as fortified rice, cereal, and dairy items.

While they offer a more localized shopping experience, neighbourhood stores often rely on strong community relationships to attract customers. In emerging markets, particularly in Latin America and Africa, neighbourhood stores remain vital in reaching underserved populations who may not have access to larger retail outlets or e-commerce platforms. These stores typically offer basic fortified food products at affordable prices, catering to lower-income households.

Key Market Segments

By Raw Material

- Rice Flour

- Wheat Flour

- Com Flour

- Mike

- Sugar

By Process

- Drum Dying

- Dusting

By Micronutrients

- Vitamins

- Minerals

- Ther Fortifying Nutrients

By Application

- Basic Food

- Processed Food

- Value added Food

- Condiments

- Juice

By Technology

- Drying

- Extrusion

- Coating & Encapsulation

- Others

By Sales Channel

- Modern Trade

- Online Sales

- Neighbourhood Stores

- Other

Drivers

Rising Consumer Awareness of Health and Nutrition

A key driving factor in the growth of the fortified foods market is the increasing consumer awareness of health and nutrition. Over the past few years, consumers have become more conscious about the nutritional value of the foods they consume, as well as their impact on overall health and well-being.

According to a report by the World Health Organization (WHO), approximately 40% of the global population is at risk of deficiencies in essential micronutrients, such as vitamins and minerals, which are often addressed through fortified foods. This has led to an increased demand for food products that offer additional nutritional benefits, especially those with added vitamins, minerals, and other micronutrients.

In 2023, the global fortified food market was valued at over USD 170 billion, with consumers increasingly seeking out functional foods that can support immunity, bone health, heart health, and overall wellness.

For example, fortified cereals and grains remain among the most popular fortified foods, with nearly 25% of global consumers opting for fortified versions of breakfast foods, according to a survey by the Food and Agriculture Organization (FAO). As more consumers embrace a healthier lifestyle, fortified foods, particularly those enriched with essential nutrients like vitamin D, iron, and folic acid, are becoming more prevalent on supermarket shelves.

Government Initiatives and Regulations

Government policies and initiatives play a pivotal role in driving the demand for fortified foods. Several governments around the world have implemented regulations mandating the fortification of staple foods to address widespread nutrient deficiencies. For example, in India, the government has launched the Fortification of Food Bill to fortify staples like rice, wheat, and salt with essential micronutrients, targeting over 1 billion people.

This initiative alone is expected to increase the fortified food market by approximately 15% in the coming years. Similarly, in the United States, the FDA has recommended fortifying foods such as flour and milk to combat deficiencies in vitamins B12, vitamin D, and folate, especially among vulnerable populations.

Governments across Africa, Asia, and Latin America have also supported the fortification of essential food items to reduce malnutrition and improve public health. According to the Global Alliance for Improved Nutrition (GAIN), over 80 countries have adopted national food fortification programs. These initiatives have encouraged both public and private investments in the production of fortified foods, further expanding market opportunities and improving access to essential nutrients.

Growing Health Consciousness and Dietary Shifts

The growing trend toward healthy eating habits and personalized nutrition is another significant driver for the fortified foods market. Consumers are increasingly shifting toward diets that prioritize functional benefits, which has led to the expansion of fortified foods beyond traditional categories like cereals and bread.

For instance, fortified beverages, snacks, and dairy products have seen a surge in popularity in recent years. In fact, the demand for functional beverages like fortified juices, teas, and plant-based drinks is expected to grow at a CAGR of 6.3% from 2023 to 2028.

This dietary shift is fueled by the rising incidence of chronic diseases such as obesity, cardiovascular diseases, and diabetes, which have prompted consumers to seek foods that not only provide energy but also offer added health benefits.

Fortified foods provide an easy and effective way to enhance one’s diet without significant changes in eating habits. As a result, many food manufacturers are investing heavily in the development of new fortified products, including those aimed at specific health concerns like immunity, gut health, and mental well-being.

Innovations in Fortified Food Products

Innovative products in the fortified foods market have further accelerated growth. Food companies are continually exploring new methods to enhance the nutritional profile of everyday food products. Fortified plant-based foods, such as fortified plant-based milks, vegan snacks, and meat substitutes, are gaining traction due to their growing popularity among health-conscious and environmentally-aware consumers.

The rise of plant-based diets, combined with a greater understanding of nutrition, is opening up new market opportunities for fortified food producers. According to data from the Plant Based Foods Association (PBFA), the market for plant-based foods in the U.S. alone grew by 27% in 2022, and the demand for fortified plant-based options is expected to keep increasing.

Restraints

High Production Costs of Fortified Foods

A significant restraining factor for the growth of the fortified foods market is the high production costs associated with the fortification process. Fortifying food with essential nutrients such as vitamins, minerals, and other micronutrients requires additional processing, specialized equipment, and higher-quality raw materials, which can increase the cost of production.

According to data from the Food and Agriculture Organization (FAO), the cost of fortifying staple foods like flour, rice, and salt can increase production costs by 5% to 15%, depending on the type of fortification and the scale of operation. These increased costs are often passed on to consumers in the form of higher retail prices, which can limit the affordability and accessibility of fortified products, especially in low-income regions.

Moreover, while fortified foods are essential for addressing malnutrition and micronutrient deficiencies, many consumers in developing markets may not perceive them as a priority over basic food items. The World Bank estimates that more than 3 billion people globally live on less than USD 2.50 per day, limiting their purchasing power for fortified foods.

Regulatory and Compliance Challenges

The fortification of foods is subject to stringent regulations and quality control standards, which can be complex and costly for manufacturers to navigate. In many countries, food fortification is heavily regulated by government bodies, such as the U.S. Food and Drug Administration (FDA), the European Food Safety Authority (EFSA), and the World Health Organization (WHO).

These agencies set specific guidelines regarding which nutrients can be added, in what quantities, and to which types of foods. Compliance with these regulations often requires significant investments in testing, certification, and reporting, which increases operational costs.

In some markets, the absence of clear and standardized regulations for fortification can also lead to inconsistent quality and consumer mistrust. For example, in India, although food fortification programs have been launched, there is still a lack of uniformity in nutrient levels across different brands and products.

Limited Consumer Awareness and Acceptance

According to the World Health Organization, a significant portion of the population in emerging markets still lacks knowledge about micronutrient deficiencies and the role of fortified foods in addressing these issues. In sub-Saharan Africa, for example, only 15% of the population is familiar with the concept of food fortification, which severely limits the potential market for fortified food products.

Limited Access and Distribution Challenges

While fortified foods are increasingly available in developed markets, distribution challenges persist in low-income and rural areas. A significant portion of the global population still lacks access to fortified foods, particularly in remote areas where infrastructure and logistics are underdeveloped.

According to the United Nations Food and Agriculture Organization (FAO), about 30% of the world’s population lives in rural areas with limited access to fortified foods, particularly in developing nations in Asia, Africa, and Latin America.

Opportunity

Government Initiatives in Food Fortification

A major growth opportunity for the fortified foods market lies in the expansion of government initiatives aimed at addressing malnutrition and micronutrient deficiencies globally. Governments around the world are increasingly recognizing the importance of food fortification as a sustainable solution to improving public health, especially in low- and middle-income countries. These initiatives create a conducive environment for the growth of fortified food markets, offering opportunities for manufacturers to align their products with national nutrition goals.

For example, the World Health Organization (WHO) and the United Nations (UN) have actively promoted food fortification as a key strategy to combat nutrient deficiencies, particularly iron, vitamin A, iodine, and folic acid. In 2020, the Global Alliance for Improved Nutrition (GAIN) reported that over 60 countries had implemented mandatory or voluntary food fortification programs, with India and Indonesia being prominent examples.

In India, for instance, the government has mandated the fortification of wheat and rice with iron, folic acid, and vitamin B12, targeting more than 1.3 billion people. By 2024, India’s wheat and rice fortification program is expected to cover 100 million households, reflecting significant market potential.

Additionally, the Indian government allocated USD 35 million for a pilot project to fortify 10 million metric tons of wheat and rice as part of its National Food Security Act. This initiative not only drives demand for fortified ingredients but also encourages private sector investments in food processing technologies and fortification expertise.

Increasing Consumer Awareness of Health Benefits

Consumer awareness about the health benefits of fortified foods presents another promising growth opportunity. As health-consciousness increases globally, more consumers are seeking ways to improve their nutritional intake, particularly in regions where micronutrient deficiencies are prevalent. The World Bank states that 2 billion people suffer from micronutrient deficiencies worldwide, which has led to growing demand for food products that can improve overall health and prevent nutritional gaps.

In developed regions like North America and Europe, fortified foods are increasingly seen as part of a holistic approach to preventive healthcare. For instance, the sales of fortified foods in the United States grew by 8% annually in 2023, driven by consumer preferences for products that support immune health, bone strength, and overall wellness.

In the European Union, fortification with vitamin D, calcium, and iron is becoming more common, especially in dairy, bread, and cereals. According to the European Food Safety Authority (EFSA), around 80% of European consumers are willing to pay a premium for fortified foods, particularly those with added functional ingredients that support immunity and digestive health.

Technological Advancements and Innovations

The adoption of advanced technologies in the food processing sector is creating new growth opportunities for the fortified foods market. Innovations in fortification techniques and ingredients have made it easier to incorporate essential nutrients into a wide range of food products without compromising their taste, texture, or shelf life. Emerging technologies, such as nanoencapsulation, extrusion, and microencapsulation, are making it possible to fortify foods with micronutrients in a more efficient and cost-effective manner.

For example, nanoencapsulation allows nutrients to be added to foods in tiny, bioavailable particles, enhancing their absorption in the body. According to the Institute of Food Technologists (IFT), innovations like this are expected to significantly expand the types of foods that can be fortified, including snacks, beverages, and confectionery products. This creates new market opportunities for manufacturers to target a broader consumer base, especially in the rapidly growing functional foods segment.

Trends

Increasing Demand for Plant-Based Fortified Foods

One of the major latest trends driving the fortified foods market is the growing consumer preference for plant-based fortified foods. This trend is largely driven by the rising adoption of vegan, vegetarian, and flexitarian diets across the globe. According to the Plant Based Foods Association (PBFA), the plant-based food market in the United States alone was valued at USD 7.4 billion in 2023, reflecting a 27% growth over the previous year.

In terms of specific products, plant-based milk alternatives such as soy, almond, and oat milk, are being increasingly fortified with essential nutrients like calcium, vitamin D, and vitamin B12. The International Food Information Council (IFIC) reported that the plant-based milk segment is projected to grow at a 10% compound annual growth rate (CAGR) through 2025.

Government Initiatives Supporting Plant-Based Fortification

Government initiatives are also playing a significant role in encouraging the fortification of plant-based foods. In India, for example, the National Food Security Act (NFSA) has expanded its fortification policies to include a wider range of food products, including plant-based alternatives.

As of 2023, the Indian government has been exploring the possibility of fortifying plant-based dairy products like plant milk with vitamin B12, iron, and vitamin D to address the rising deficiencies in these nutrients.

The Food Safety and Standards Authority of India (FSSAI) is working to introduce guidelines that would make fortification in these sectors more standardized and safe. Moreover, government policies in countries such as Canada and the United Kingdom are providing funding and grants to support the fortification of plant-based foods as a way to combat malnutrition and micronutrient deficiencies.

Consumer Demand for Functional Fortified Foods

Another trend that is accelerating the growth of fortified plant-based foods is the increasing demand for functional foods. Functional foods are those that provide health benefits beyond basic nutrition, and consumers are increasingly seeking such foods to support overall wellness.

This trend is particularly prominent among millennials and Generation Z consumers, who are highly focused on health and wellness, and are willing to pay a premium for foods that offer additional health benefits. The Functional Foods Market is projected to reach USD 275 billion by 2025, growing at a 7% CAGR, with a significant portion of that growth coming from fortified plant-based products.

Regional Analysis

In 2023, the Asia Pacific (APAC) region dominated the fortified foods market, capturing more than 43% of the global market share, valued at approximately USD 56.6 billion. This growth is primarily driven by the rising demand for fortified staple foods such as rice, wheat, and flour, particularly in countries like China and India, where malnutrition remains a key concern.

In India, government initiatives like the National Food Security Act (NFSA) are promoting the fortification of staple foods, thereby contributing to market growth. Additionally, the increasing health consciousness and a growing middle class in countries like China and Indonesia are expanding the consumer base for fortified food products.

North America holds the second-largest market share, accounting for 27% of the global market in 2023. The demand for fortified foods in the region is driven by health-conscious consumers seeking to prevent chronic diseases, particularly among older populations. The U.S. and Canada continue to lead the adoption of fortified foods, with fortified cereals and snacks being highly popular. In the U.S., fortified foods such as vitamin D and folic acid enriched products are integral to public health initiatives aimed at combating nutrient deficiencies.

In Europe, the fortified foods market was valued at USD 20.4 billion in 2023, with steady growth driven by consumer awareness around functional foods and nutrient fortification. European countries, particularly the UK and Germany, are increasingly adopting fortified products as part of their daily diets, especially in sectors like dairy, cereals, and beverages.

Latin America and the Middle East & Africa (MEA) show promising growth potential, but currently hold smaller shares, driven by increasing urbanization, shifting dietary preferences, and regional government initiatives targeting malnutrition.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The fortified foods market is characterized by the presence of several leading players across the global food and nutrition landscape. Aria Foods, BASF SE, Bühler AG, and Bunge Limited are some of the prominent companies involved in the development and supply of fortified ingredients, primarily focusing on vitamins, minerals, and other micronutrients.

These companies leverage their extensive research and development capabilities to cater to the growing consumer demand for healthier, fortified food options. Cargill, Danone, DSM Nutritional Products, and General Mills continue to be strong players in the market, offering a diverse range of fortified products such as dairy, cereals, and beverages, aligning with evolving consumer preferences for functional foods that provide additional health benefits.

Nestlé S.A., Mondelez International, and Kellogg Company also hold significant shares in the fortified foods market, particularly in the categories of breakfast cereals, snacks, and dairy products. These companies have focused on fortifying common foods with essential nutrients like vitamins D and B12, folic acid, and calcium.

Lonza Group AG, Tata Chemicals, and Unilever PLC are additionally active in the fortification sector, with innovations in both product formulations and manufacturing processes. SternVitamin GmbH & Co. KG and Watson, Inc. specialize in providing customized nutrient blends to food manufacturers, helping them create fortified products with a targeted approach to health benefits.

Through strategic partnerships, acquisitions, and product expansions, these key players have established a robust market presence. For example, BASF SE continues to invest heavily in micronutrient innovation, particularly in regions like Asia Pacific and Latin America, where the demand for fortified foods is on the rise due to public health initiatives aimed at combating malnutrition.

Additionally, companies like FMC Corporation and Tate & Lyle PLC are enhancing their fortified product portfolios with natural ingredients and solutions that cater to health-conscious consumers globally.

Top Key Players in the Market

- Aria Foods

- BASF SE

- Bühler AG

- Bunge Limited

- Cargill, Incorporated

- Corbion N.V.

- Danone

- Dr. Paul Lohmann GmbH KG

- DSM Nutritional Products

- Fabrik Wright Enrichment Inc.

- FMC Corporation

- Gastaldi Hermanos

- General Mills, Inc.

- Glanbia PLC

- Kellogg Company

- Koninklijke DSM NV

- Lonza Group AG

- Mondelez International

- Nestlé S.A.

- Nutritional Holdings (Pty) Limited

- Sinokrot Global

- SternVitamin GmbH & Co. KG

- Stern-Wywiol GmbH & Co.KG

- Tata Chemicals Limited

- Tate & Lyle PLC

- The Archer Daniels Midland Company

- Ufuk Kimya llac Sanayi Ve Ticaret Limited Sirketi

- Unilever PLC

- Watson, Inc.

Recent Developments

In 2023, Aria Foods reported a significant increase in revenue, with its fortified foods segment growing by 8% compared to the previous year.

In 2023, BASF’s Human Nutrition division reported a 7.2% increase in sales compared to 2022, driven by strong demand for its fortified food ingredients such as vitamins, minerals, and omega-3 fatty acids.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 131.6 Bn |

| Forecast Revenue (2033) | USD 281.5 Bn |

| CAGR (2024-2033) | 7.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Rice Flour, Wheat Flour, Com Flour, Mike, Sugar), By Process (Drum Dying, Dusting), By Micronutrients (Vitamins, Minerals, Ther Fortifying Nutrients), By Application (Basic Food, Processed Food, Value added Food, Condiments, Juice), By Technology (Drying, Extrusion, Coating Anda Encapsulation, Others), By Sales Channel (Modern Trade, Online Sales, Neighbourhood Stores, Other) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Aria Foods, BASF SE, Bühler AG, Bunge Limited, Cargill, Incorporated, Corbion N.V., Danone, Dr. Paul Lohmann GmbH KG, DSM Nutritional Products, Fabrik Wright Enrichment Inc., FMC Corporation, Gastaldi Hermanos, General Mills, Inc., Glanbia PLC, Kellogg Company, Koninklijke DSM NV, Lonza Group AG, Mondelez International, Nestlé S.A., Nutritional Holdings (Pty) Limited, Sinokrot Global, SternVitamin GmbH & Co. KG, Stern-Wywiol GmbH & Co.KG, Tata Chemicals Limited, Tate & Lyle PLC, The Archer Daniels Midland Company, Ufuk Kimya llac Sanayi Ve Ticaret Limited Sirketi, Unilever PLC, Watson, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |