Quick Navigation

Report Overview

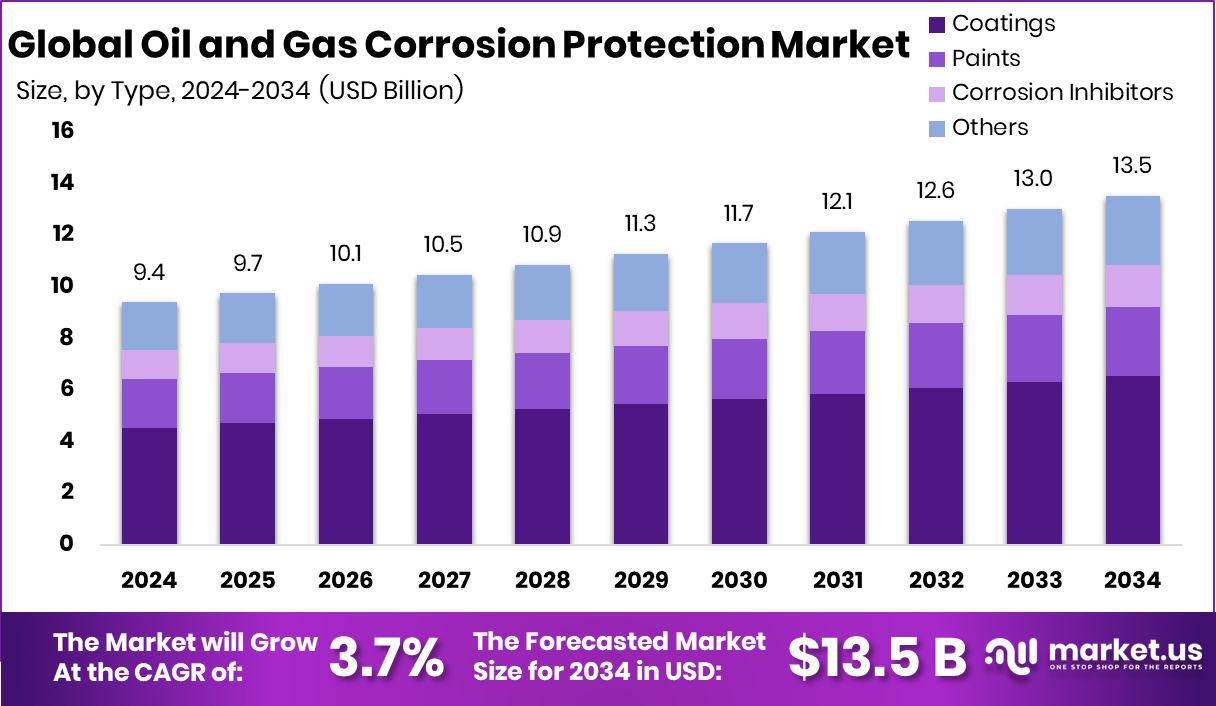

Global Oil and Gas Corrosion Protection Market is expected to be worth around USD 13.5 billion by 2034, up from USD 9.4 billion in 2024, and grow at a CAGR of 3.7% from 2025 to 2034. Middle East and Africa saw USD 3.2 Bn corrosion protection market expansion in 2024.

Oil and gas corrosion protection refers to the methods and technologies used to prevent or reduce the deterioration of metal and infrastructure due to chemical reactions, mostly involving water, oxygen, and other corrosive elements. This is critical in upstream, midstream, and downstream operations, where equipment such as pipelines, storage tanks, and rigs is exposed to harsh environments.

The oil and gas corrosion protection market includes products, technologies, and services to prevent corrosion across the industry. This includes coatings, inhibitors, cathodic protection systems, linings, and inspection tools. The market serves onshore and offshore applications, including pipelines, refineries, terminals, and drilling rigs.

The market continues to grow as companies focus on extending asset lifecycles, improving safety, and complying with stricter environmental and safety regulations. In 2023, crude oil was produced in 32 states and U.S. coastal waters, with six states contributing around 76% of the total output. Texas emerged as the leading oil producer, accounting for 42.61% of domestic production.

The market is growing due to aging oil infrastructure, especially in regions like North America and the Middle East. These older systems require extensive maintenance and protection to remain operational. Also, exploration in deepwater and harsh environments demands advanced corrosion protection. Rising awareness around cost savings from proactive maintenance further drives growth.

Key Takeaways

- Global Oil and Gas Corrosion Protection Market is expected to be worth around USD 13.5 billion by 2034, up from USD 9.4 billion in 2024, and grow at a CAGR of 3.7% from 2025 to 2034.

- In 2024, Coatings held a 48.3% share by type in the Oil and Gas Corrosion Protection Market.

- Offshore installations dominated with 67.7% market share by location in corrosion protection applications for oil and gas.

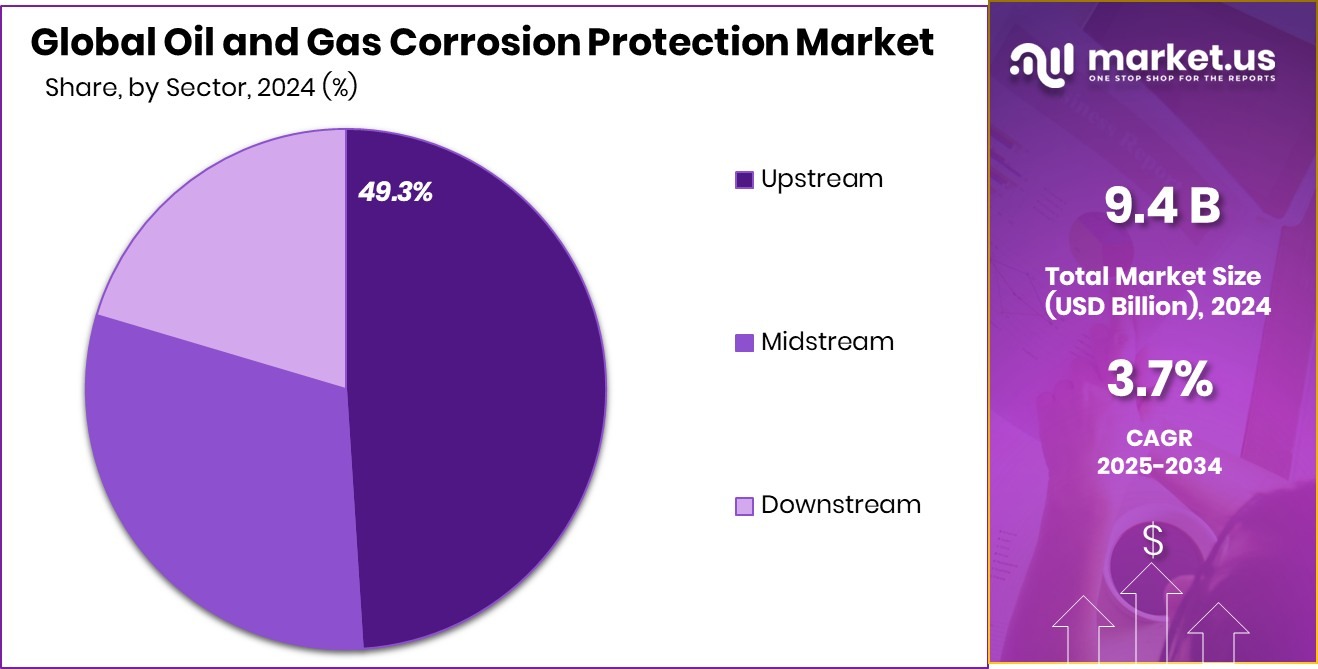

- The upstream sector accounted for a 49.3% share, leading demand in Oil and Gas Corrosion Protection solutions.

- Corrosion protection demand in the Middle East and Africa captured a 34.7% market value.

By Type Analysis

In the Oil and Gas Corrosion Protection Market, coatings held a 48.3% share by type in 2024.

In 2024, Coatings held a dominant market position in the By Type segment of the Oil and Gas Corrosion Protection Market, with a 48.3% share. This significant market presence reflects the continued reliance on protective coatings to prevent equipment and infrastructure deterioration across the sector.

Coatings play a crucial role in mitigating corrosion-related damage, particularly in high-risk operational environments exposed to moisture, salinity, and extreme temperatures. Their use spans pipelines, tanks, valves, and offshore structures, where durability and long-term performance are essential.

The preference for coatings as a corrosion protection method is supported by their cost-effectiveness and wide applicability across various oil and gas assets. Given the demanding operational conditions in the upstream and offshore segments, protective coatings remain a preferred choice due to ease of application, versatility, and compatibility with both metallic and non-metallic surfaces.

By Location Analysis

Offshore installations dominated the Oil and Gas Corrosion Protection Market, accounting for 67.7% share by location globally.

In 2024, Offshore held a dominant market position in the By Location segment of the Oil and Gas Corrosion Protection Market, with a 67.7% share. This high share reflects the intense need for corrosion protection solutions in offshore environments, where infrastructure is continuously exposed to harsh marine conditions.

Saltwater, high humidity, and fluctuating temperatures accelerate metal degradation, making corrosion control a critical operational priority. Platforms, risers, subsea pipelines, and floating production systems require robust corrosion prevention measures to ensure safety, operational efficiency, and equipment longevity.

The 67.7% market share underlines the strategic importance of corrosion protection technologies in safeguarding offshore assets, which are expensive to build and maintain. Offshore installations operate in remote locations where repair and replacement are costly and logistically challenging.

As a result, investment in protective solutions such as coatings, cathodic protection, and corrosion-resistant materials is essential to minimize downtime and prevent structural failures. The dominance of the offshore segment highlights the sector’s reliance on durable protection methods to cope with aggressive environmental exposure.

By Sector Analysis

The upstream sector led the Oil and Gas Corrosion Protection Market with a 49.3% share by sector worldwide.

In 2024, Upstream held a dominant market position in the By Sector segment of the Oil and Gas Corrosion Protection Market, with a 49.3% share. This leading position underscores the critical role of corrosion protection technologies in exploration and production activities, where equipment and infrastructure face continuous exposure to corrosive substances such as hydrogen sulfide, carbon dioxide, and brine.

The 49.3% market share emphasizes the sector’s dependency on reliable corrosion mitigation strategies to prevent equipment failure and production losses. Corrosion-related issues in upstream operations can result in well integrity problems and unplanned downtime, leading to significant financial and operational consequences.

As such, upstream companies prioritize investment in protective coatings, inhibitors, and advanced materials that can withstand high pressures, temperatures, and chemically aggressive environments. The dominance of this segment also reflects the widespread scale of upstream infrastructure globally, particularly in offshore and remote locations where asset protection is a major operational concern.

Key Market Segments

By Type

- Coatings

- Paints

- Corrosion Inhibitors

- Others

By Location

- Offshore

- Onshore

By Sector

- Upstream

- Midstream

- Downstream

Driving Factors

Harsh Offshore Conditions Drive Corrosion Protection Demand

One of the biggest reasons for the growth of the oil and gas corrosion protection market is the harsh conditions found in offshore environments. Offshore oil platforms, pipelines, and equipment are always in contact with salty seawater, high humidity, and extreme temperatures.

These conditions cause metal parts to rust and break down faster. To prevent this, companies invest heavily in protective coatings and technologies that stop corrosion before it starts. Since offshore operations are very expensive and are located in remote areas, regular maintenance is difficult.

Restraining Factors

High Installation Costs Limit Market Growth Potential

One major factor holding back the oil and gas corrosion protection market is the high cost of advanced solutions. Applying protective coatings, cathodic systems, or other technologies often requires skilled labor, special equipment, and long downtimes—especially in offshore or deep-sea operations. This makes it very expensive for companies, particularly smaller operators, to implement full-scale corrosion protection.

In some cases, the upfront cost is so high that firms choose to delay or reduce the use of these systems, risking future damage. Even though these solutions save money in the long term by preventing repairs, the high initial investment remains a barrier. This slows down the adoption rate, especially in cost-sensitive or low-profit drilling environments.

Growth Opportunity

Aging Infrastructure Spurs Corrosion Protection Demand

A significant growth opportunity in the oil and gas corrosion protection market arises from the aging infrastructure within the industry. Many pipelines, refineries, and offshore platforms have been operational for decades, making them more susceptible to corrosion-related failures. As these assets age, the risk of leaks, environmental hazards, and operational downtimes increases, necessitating effective corrosion protection solutions.

Implementing advanced protective measures, such as coatings, cathodic protection, and corrosion inhibitors, becomes essential to extend the lifespan of these structures and ensure safety. The pressing need to maintain and upgrade existing facilities presents a substantial opportunity for companies offering innovative corrosion protection technologies.

By focusing on solutions tailored to rehabilitate and preserve aging infrastructure, businesses can address a critical demand in the market, contributing to the overall growth of the oil and gas corrosion protection sector.

Latest Trends

Smart Coatings Revolutionize Corrosion Protection Strategies

A notable trend in the oil and gas corrosion protection market is the adoption of smart coatings. These advanced materials can detect and respond to environmental changes, such as pH shifts or the presence of corrosive agents, by releasing inhibitors or altering their properties to prevent corrosion. This self-healing capability reduces maintenance needs and extends the lifespan of infrastructure.

The integration of nanotechnology and responsive polymers in coatings enhances their effectiveness, making them suitable for harsh environments like offshore platforms and deep-sea pipelines.

Regional Analysis

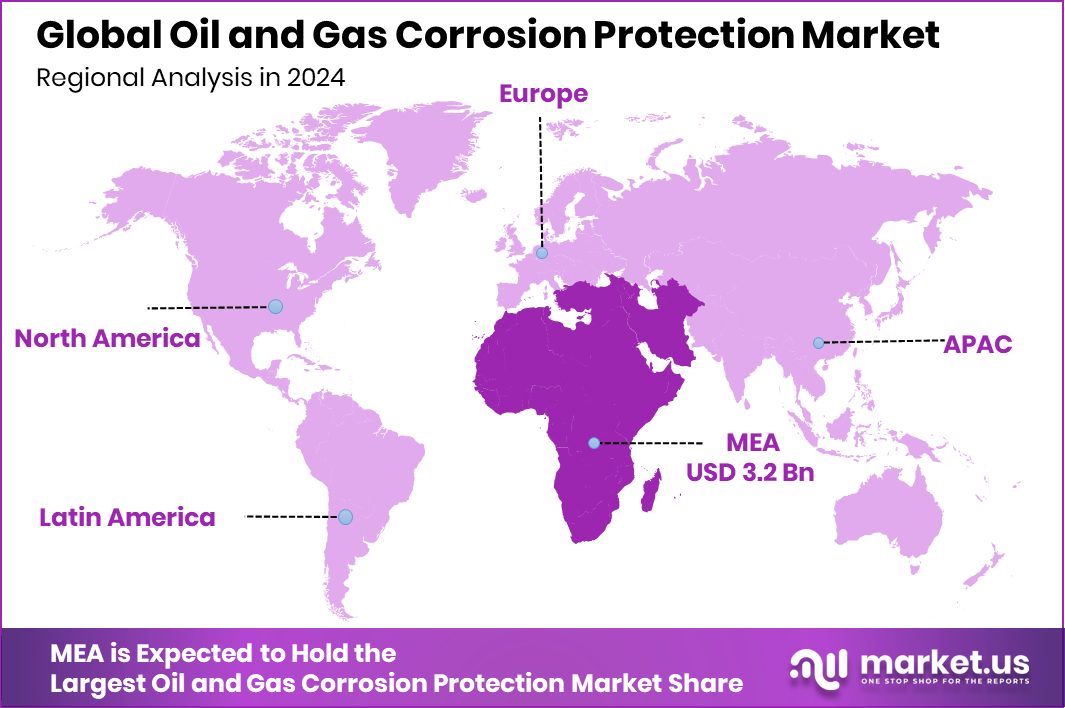

In the Middle East and Africa, the market reached USD 3.2 Bn with a 34.7% share.

In 2024, the Oil and Gas Corrosion Protection Market showed notable regional variations in demand, driven by infrastructure exposure and production activities. The Middle East and Africa emerged as the dominant regional market, accounting for 34.7% of the global share with a value of USD 3.2 billion. This leadership is attributed to the region’s extensive oil production infrastructure, particularly in countries like Saudi Arabia and the UAE, where offshore and onshore corrosion control remains a critical focus.

North America continued to register steady demand due to mature upstream operations and ongoing maintenance of aging assets, while Europe’s corrosion protection activities are supported by stringent safety and asset integrity regulations. Asia Pacific saw rising adoption across expanding refinery networks and offshore platforms, driven by energy demands in emerging economies.

Meanwhile, Latin America contributed modestly, with corrosion protection initiatives largely concentrated in offshore Brazilian oil fields. The overall market dynamics remain influenced by regional exposure to harsh environments, operational scale, and long-term maintenance priorities.

The Middle East and Africa’s dominance highlights the region’s high concentration of oilfield infrastructure, much of which operates under aggressive environmental conditions that necessitate advanced corrosion protection technologies to ensure equipment longevity and minimize production disruptions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Chase Corporation continued to provide a diverse range of corrosion protection solutions, including technologically advanced coatings and materials. Their offerings, such as adhesives, sealants, tapes, and membranes, are designed to protect infrastructure investments across various industries, including oil and gas. By leveraging a spectrum of chemistries like epoxies, urethanes, acrylics, silicones, and elastomers, Chase has developed a comprehensive line of products with proven track records in demanding anti-corrosion applications.

Cortec Corporation maintained its focus on innovative corrosion solutions through its patented Vapor phase Corrosion Inhibitor (VpCI®) technology. In 2024, Cortec participated in the Two Days Corrosion Conference in Santiago, Chile, underscoring its commitment to industry collaboration and the promotion of proactive corrosion prevention strategies.

Hempel A/S experienced growth in its Energy & Infrastructure segment, driven by the oil and gas sector, particularly in the Middle East. The company introduced a new Avantguard solution for infrastructure assets requiring long-term protection in highly corrosivity environments. This innovation contributed to Hempel delivering its best EBITDA result to date in 2024.

Top Key Players in the Market

- 3M Company

- Akzo Nobel N.V

- Ashland Global Specialty Chemicals Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Chase Corporation

- Cortec Corporation

- Hempel A/S

- Hexigone Inhibitors Ltd.

- Imperial Oilfield Chemicals Pvt. Ltd.

- Jotun A/S

- Maxwell Additives Pvt. Ltd.

- Metal Coatings Corp.

- RPM International Inc.

- SLB (Schlumberger Limited)

- Teknos (Teknos Group)

- The Sherwin-Williams Company

Recent Developments

- In November 2024, AkzoNobel introduced Chartek ONE, a 100% solids, boron-free, two-component coating designed for offshore oil and gas facilities. This product offers combined protection against corrosion, cryogenic conditions, and hydrocarbon fires, providing up to three hours of jet and pool fire resistance. Its single-coat, mesh-free application simplifies installation and can reduce workshop hours by up to 59%.

- In November 2024, Cortec introduced the VpCI®-329 D in an easy-to-use spray format. This oil-based rust preventative offers long-term protection for metals exposed to harsh environments, making it suitable for oil and gas applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 9.4 Billion |

| Forecast Revenue (2034) | USD 13.5 Billion |

| CAGR (2025-2034) | 3.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Coatings, Paints, Corrosion Inhibitors, Others), By Location (Offshore, Onshore), By Sector (Upstream, Midstream, Downstream) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M Company, Akzo Nobel N.V., Ashland Global Specialty Chemicals Inc., Axalta Coating Systems Ltd., BASF SE, Chase Corporation, Cortec Corporation, Hempel A/S, Hexigone Inhibitors Ltd., Imperial Oilfield Chemicals Pvt. Ltd., Jotun A/S, Maxwell Additives Pvt. Ltd., Metal Coatings Corp., RPM International Inc., SLB (Schlumberger Limited), Teknos (Teknos Group), The Sherwin-Williams Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |