Quick Navigation

Report Overview

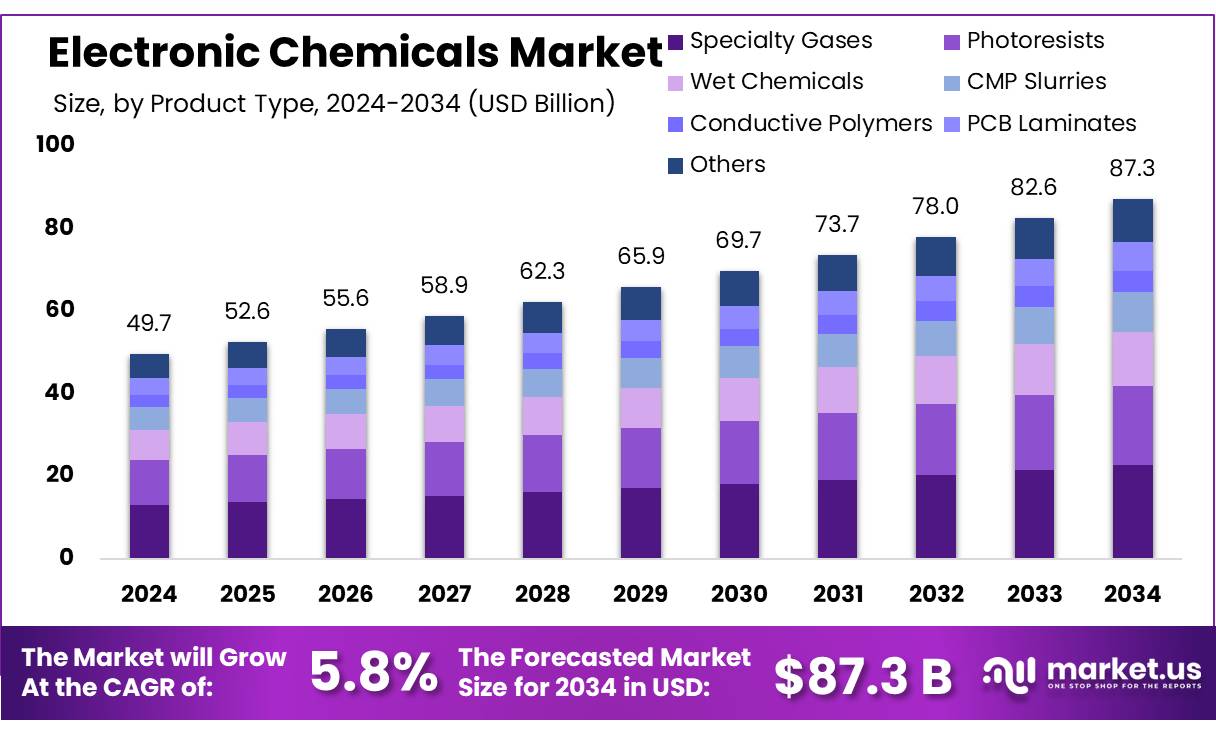

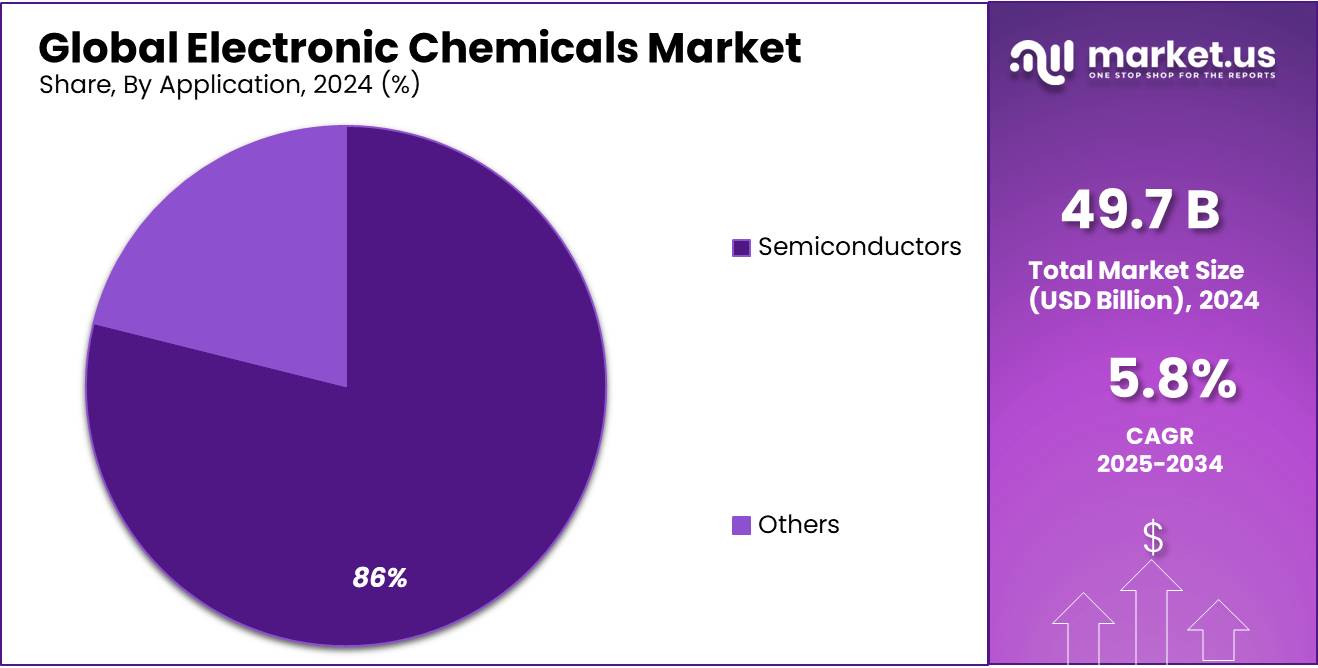

The Global Electronic Chemicals Market size is expected to be worth around USD 87.3 Bn by 2034, from USD 49.7 Bn in 2024, growing at a CAGR of 5.8% during the forecast period from 2025 to 2034.

Electronic chemicals are specialized materials used extensively in the manufacture of electronic components and devices such as semiconductors, integrated circuits, and printed circuit boards. These chemicals, including gases, photoresists, wet chemicals, and solvents, play a critical role in the etching, cleaning, and doping processes that are integral to the electronics manufacturing industry. As the demand for smaller, faster, and more efficient electronic devices continues to rise, the electronic chemicals market is positioned for significant expansion.

The global market for electronic chemicals is characterized by its close alignment with the electronics and semiconductor industries. Notably, a report from the U.S. Department of Commerce highlighted that the semiconductor industry alone accounted for approximately $3.5 trillion in sales globally, underlying the vast scale and impact of this sector on electronic chemicals.

Several factors drive the demand for electronic chemicals. The relentless advancement in consumer electronics, such as smartphones, wearables, and high-performance computing devices, necessitates the use of high-quality electronic chemicals. Additionally, the automotive sector’s shift towards electric vehicles (EVs) and autonomous driving technologies has created a robust demand for electronic components, thus fueling the electronic chemicals market. For example, the production of electric vehicles has surged by approximately 40% from 2021 to 2024, according to the International Energy Agency (IEA), necessitating advanced electronics for battery management systems and onboard diagnostics.

Governments worldwide are also playing a pivotal role in the growth of this sector through various incentives and regulatory support. For instance, the U.S. government announced a $500 million grant in 2024 to support semiconductor manufacturing which relies heavily on electronic chemicals. Similarly, the European Union has launched initiatives like the “Digital Europe” program, which allocates €7.5 billion towards the development of digital competencies, including the electronics sector, thereby indirectly supporting the electronic chemicals industry.

Key Takeaways

- Electronic Chemicals Market size is expected to be worth around USD 87.3 Bn by 2034, from USD 49.7 Bn in 2024, growing at a CAGR of 5.8%.

- Specialty Gases held a dominant market position, capturing more than a 26.50% share of the electronic chemicals market.

- Semiconductors held a dominant market position, capturing more than an 86.30% share of the electronic chemicals market.

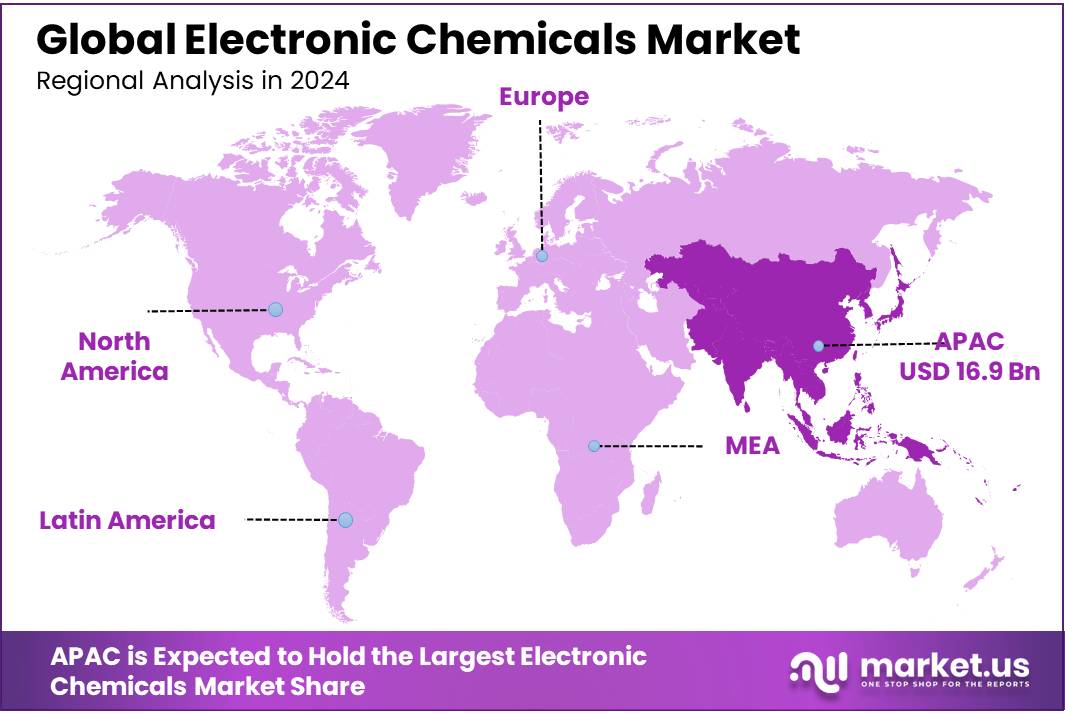

- Asia Pacific (APAC) region dominated the Electronic Chemicals Market, accounting for approximately 34.20% of the global market share, valued at around USD 16.9 billion.

By Product Type

Specialty Gases Lead with Over a Quarter of the Market Share

In 2024, Specialty Gases held a dominant market position, capturing more than a 26.50% share of the electronic chemicals market. This segment’s strong performance can be attributed to its critical role in various high-tech manufacturing processes, including semiconductors and flat panel displays.

The demand for ultra-high purity gases, which are essential for ensuring the quality and efficiency of electronic manufacturing, has driven the growth of this market segment. As industries continue to innovate and expand, specialty gases remain vital for the development of new electronic products, supporting their strong market position.

By Application

Semiconductors Dominate with 86.3% Market Share Due to Essential Role in Technology

In 2024, Semiconductors held a dominant market position, capturing more than an 86.30% share of the electronic chemicals market. This significant presence is primarily due to the essential role semiconductors play in the modern technology landscape. They are core components in virtually all electronic devices, from smartphones and computers to advanced medical equipment and automotive electronics.

The relentless advancement in technology and increasing demand for more powerful and efficient electronic devices have propelled the growth of semiconductors, cementing their substantial share in the market. As the backbone of the digital and electronic manufacturing industries, semiconductors continue to drive substantial demand for high-quality electronic chemicals.

Key Market Segments

By Product Type

- Specialty Gases

- Nitrogen Trifluoride (NF₃)

- Sulfur Hexafluoride (SF₆)

- Ammonia (NH₃)

- Others

- Photoresists

- Wet Chemicals

- CMP Slurries

- Conductive Polymers

- PCB Laminates

- Others

By Application

- Semiconductors

- Integrated Circuits (ICs)

- Printed Circuit Boards (PCBs)

- Others

Drivers

Rapid Technological Advancements Propel Electronic Chemicals Market

One major driving factor for the electronic chemicals market is the swift progression in semiconductor technology, spurred by rising demands for smaller, more powerful devices. Innovations in renewable energy systems also contribute significantly to this demand.

The drive to miniaturize devices and enhance their functionalities has led to a higher consumption of specialty gases, CMP slurries, and photoresists. These materials are crucial for various stages in semiconductor manufacturing, including cleaning, etching, and polishing, which are necessary for producing integrated circuits and printed circuit boards.

The expansion of renewable energy technologies, particularly solar energy, has increased the need for photovoltaic cells, further pushing the demand for high-purity electronic chemicals. Government initiatives across the globe support this growth by investing in domestic semiconductor production, fostering developments in 5G technologies, electric vehicles, and smart devices, thereby enhancing the overall market for electronic chemicals.

This surge is particularly evident in regions with strong technological ecosystems such as Asia Pacific, where countries like South Korea and China are leading in semiconductor production and the development of display technologies. The emphasis on green manufacturing and sustainability is also steering the market towards eco-friendly and high-purity materials, aligning with global environmental regulations.

Restraints

Environmental Regulations and Health Concerns: Major Restraints in the Electronic Chemicals Market

The growth of the electronic chemicals market is significantly restrained by stringent environmental and health regulations. Many chemicals used in the electronics industry are subject to rigorous regulatory scrutiny because of their potential environmental and health impacts. For instance, the use of hazardous substances in manufacturing processes has compelled companies to adhere strictly to various regulations, which directly affects their operational costs and limits the use of certain chemicals.

Environmental concerns about the sustainability and disposal of electronic chemicals lead to stricter regulations, pushing manufacturers towards adopting green chemistry principles. These principles aim to minimize waste, reduce the use of toxic substances, and save energy by developing processes that are environmentally benign right from the start. Moreover, the increasing emphasis on reducing the carbon footprint and enhancing the recyclability of electronic components further drives the need for compliance with environmental standards.

Additionally, health risks associated with certain chemicals used in the semiconductor manufacturing process, like crystalline silica, which can cause serious diseases such as silicosis and lung cancer, underline the need for safer working conditions and protective regulations. This not only impacts the materials that can be used but also how they are handled in the manufacturing process, adding another layer of operational complexity and cost.

Opportunity

Expanding Demand in Semiconductor Manufacturing: A Major Growth Opportunity for the Electronic Chemicals Market

The electronic chemicals market is poised for significant growth, largely driven by the expanding semiconductor industry. This surge is fueled by advancements in technologies such as artificial intelligence, 5G communications, and electric vehicles, which require increasingly sophisticated semiconductor components. The demand for high-purity liquid chemicals, crucial for the semiconductor manufacturing process, is set to rise dramatically as these sectors continue to evolve.

Government and industry investments are heavily concentrated on scaling up semiconductor fabrication facilities, which in turn boosts the need for various electronic chemicals like wet chemicals, ultra-pure solvents, and specialty gases. These investments are not just about expanding current capabilities but also about integrating greener and less toxic materials to meet stringent environmental standards.

Moreover, the global push towards digital transformation and smarter electronic solutions is expanding the market for electronic materials necessary for products like OLED and flexible displays. This demand extends beyond just the semiconductors to other electronic chemicals needed for etching, doping, and plasma-enhanced chemical vapor deposition processes.

The shift towards miniaturization of electronic components and the drive for more efficient manufacturing processes also create substantial opportunities for growth in the specialty gases market segment. As devices become smaller and more complex, the precision required in manufacturing processes becomes more critical, highlighting the need for high-purity gases and advanced chemical solutions.

Trends

Surge in Demand for High-Purity Electronic Chemicals Amid Technological Advances

A notable trend in the electronic chemicals market is the increasing demand for high-purity chemicals, driven by rapid advancements in semiconductor technology and the production of electronic devices. This trend is closely tied to the development and expansion of technologies such as artificial intelligence, 5G, and electric vehicles, which require sophisticated semiconductor components made with ultra-pure materials.

The emphasis on miniaturization and improving the performance of electronic devices has led to a greater need for high-quality silicon wafers and advanced photoresist chemicals. These materials are critical for the manufacturing of semiconductors used in a wide range of consumer electronics and automotive applications. Additionally, the push towards more environmentally friendly and less toxic chemical formulations is reshaping the market, reflecting the industry’s response to increasing environmental regulations and sustainability goals.

Furthermore, the integration of connected devices and smart technologies into everyday life is boosting the use of specialty gases like argon, nitrogen, and hydrogen in electronic manufacturing processes such as etching and doping. These gases play a crucial role in ensuring the accuracy and precision required in the increasingly complex semiconductor fabrication processes.

Regional Analysis

In 2024, the Asia Pacific (APAC) region dominated the Electronic Chemicals Market, accounting for approximately 34.20% of the global market share, valued at around USD 16.9 billion. This substantial market share is primarily driven by the extensive electronic manufacturing base in countries such as China, South Korea, Japan, and Taiwan, which are global leaders in semiconductor production and consumer electronics manufacturing.

The region’s prominence in the market is further bolstered by significant investments in high-tech manufacturing infrastructure, including the development of state-of-the-art semiconductor fabrication plants. Governments in the region have been instrumental in this growth through supportive policies and substantial financial incentives aimed at enhancing local manufacturing capabilities and reducing dependency on foreign electronic components.

Moreover, the APAC region benefits from a robust supply chain and skilled labor force, which have been pivotal in supporting the rapid expansion of electronic manufacturing services. The demand for electronic chemicals in the region is also driven by the burgeoning automotive industry, particularly with the shift towards electric vehicles, which require advanced electronics for batteries and management systems.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow is a prominent player in the Electronic Chemicals Market, known for its innovative materials science expertise. The company offers a range of electronic materials including photoresists, antifoams, and CMP slurries that are essential for semiconductor manufacturing. Dow’s commitment to sustainability and innovation enables it to meet the stringent requirements of the electronics industry, focusing on enhancing performance and environmental safety.

Covestro is recognized for its high-tech polymer materials which are critical components in the electronics sector. Their products are used in a wide array of applications, from IT devices to solar panels, emphasizing durability and efficiency. Covestro’s continuous innovation in material science significantly drives advancements in the production of electronic components, aligning with the industry’s shift towards more sustainable solutions.

BASF is a key supplier in the global electronic chemicals market, offering chemicals for wafer processing and chip manufacturing, among others. The company focuses on developing materials that improve the performance and reduce the environmental impact of electronic products. BASF’s approach to digitalization and sustainable operations positions it as a leader in the field, supporting the electronics industry’s evolving needs.

Top Key Players

- Dow Chemical Company

- Covestro AG

- BASF SE

- Solvay

- Honeywell International Inc.

- Linde plc

- Air Liquide

- JSR Corporation

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Fujifilm Electronic Materials

- RESONAC CORPORATION

- Tosoh Corporation

- Air Products and Chemicals, Inc.

- Others

Recent Developments

In 2024, Dow Chemical Company continued to play a significant role in the Electronic Chemicals Market, focusing on the production and supply of essential materials used in semiconductor manufacturing and other high-tech industries.

In 2024, Covestro AG continued to assert its position in the Electronic Chemicals Market, focusing on innovation and sustainability. The company navigated a challenging economic environment while achieving a notable EBITDA of between EUR 1.0 billion and EUR 1.25 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 49.7 Bn |

| Forecast Revenue (2034) | USD 87.3 Bn |

| CAGR (2025-2034) | 5.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Product Type (Specialty Gases, Photoresists, Wet Chemicals, CMP Slurries, Conductive Polymers, PCB Laminates, Others), By Application (Semiconductors, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Dow Chemical Company, Covestro AG, BASF SE, Solvay, Honeywell International Inc., Linde plc, Air Liquide, JSR Corporation, Shin-Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., Fujifilm Electronic Materials, RESONAC CORPORATION, Tosoh Corporation, Air Products and Chemicals, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |