Quick Navigation

Report Overview

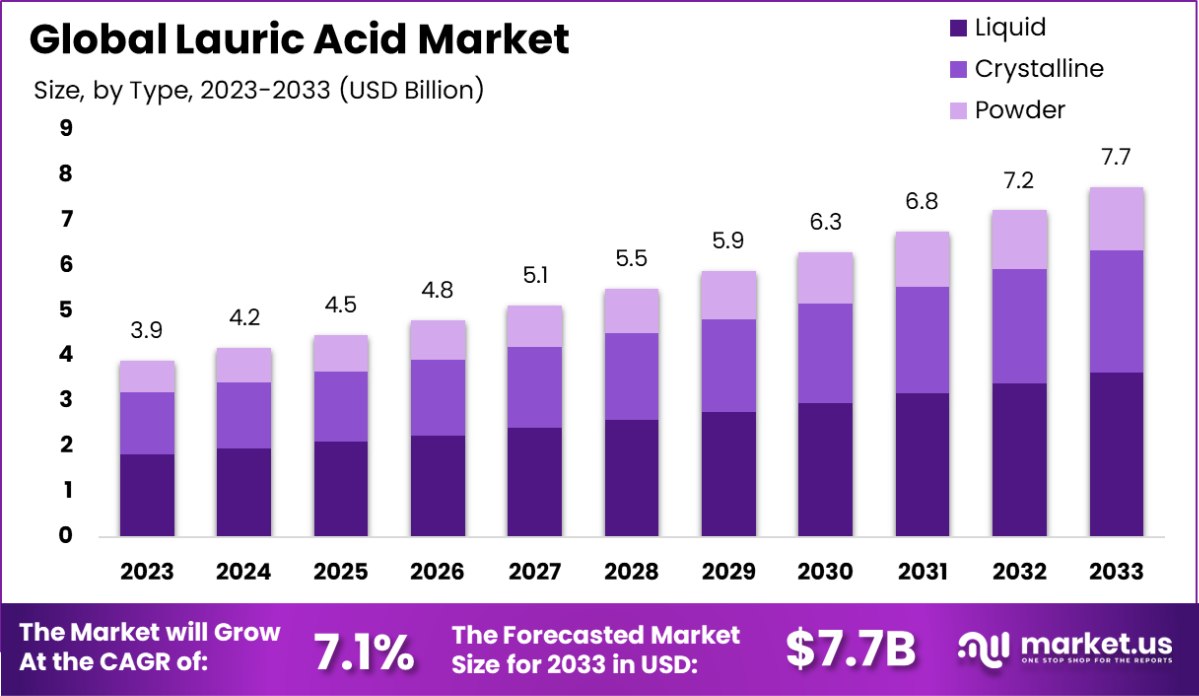

The Global Lauric Acid Market is expected to be worth around USD 7.7 Billion by 2033, up from USD 3.9 Billion in 2023, and grow at a CAGR of 7.1% from 2024 to 2033.

Lauric acid is a saturated fatty acid found predominantly in coconut oil, palm kernel oil, and certain dairy products. It is well-known for its antimicrobial properties, making it beneficial in the cosmetic, food, and pharmaceutical industries.

The Lauric Acid Market encompasses the production, distribution, and application of lauric acid across various industries. Growth in this market is primarily driven by the increasing demand for natural and organic personal care products, where lauric acid is utilized for its health-promoting benefits.

Growth factors for the Lauric Acid Market include the expansion of the personal care industry and the rising consumer preference for natural ingredients. Increased awareness of the health benefits associated with lauric acid boosts its demand for dietary supplements and healthy foods.

Opportunities in the Lauric Acid Market lie in technological advancements in extraction and processing methods. These innovations can reduce costs and improve the purity of lauric acid, making it more attractive for use in high-end cosmetic and pharmaceutical products.

The Lauric Acid Market is poised for significant growth, driven by evolving consumer preferences and technological advancements in production methods. As a key component in various industries, lauric acid’s applications are expanding, particularly in the personal care and health sectors. The shift towards more sustainable and environmentally friendly production practices marks a critical development in this market.

Recent innovations have led to a notable 8.9% reduction in greenhouse gas emissions in the production of lauric acid, compared to traditional methods that rely heavily on petroleum-based processes. This progress not only enhances the market’s appeal to environmentally conscious consumers but also aligns with global regulatory trends favoring greener manufacturing techniques.

Furthermore, the unique absorption characteristics of lauric acid, wherein only 25-30% is absorbed through the portal vein, as opposed to 95% of medium-chain triglycerides, underline its distinct metabolic processing.

This property can be leveraged in developing specialized dietary supplements and pharmaceuticals that require precise dosing and controlled release. As such, the market presents substantial opportunities for innovation in product formulation and health benefit positioning.

Looking ahead, the Lauric Acid Market is expected to continue expanding its footprint, supported by strong consumer demand for natural products and the industry’s drive towards more sustainable practices.

Companies are encouraged to invest in R&D to harness these opportunities, particularly in improving extraction and processing efficiencies, to cater to the growing market demands effectively. This approach will not only bolster market growth but also contribute to the broader goals of sustainability and health promotion.

Key Takeaways

- The Global Lauric Acid Market is expected to be worth around USD 7.7 Billion by 2033, up from USD 3.9 Billion in 2023, and grow at a CAGR of 7.1% from 2024 to 2033.

- The liquid form of lauric acid dominates the market, accounting for 47.4% of total consumption.

- High purity lauric acid, ranging from 85-98%, represents 47.5% of the market share.

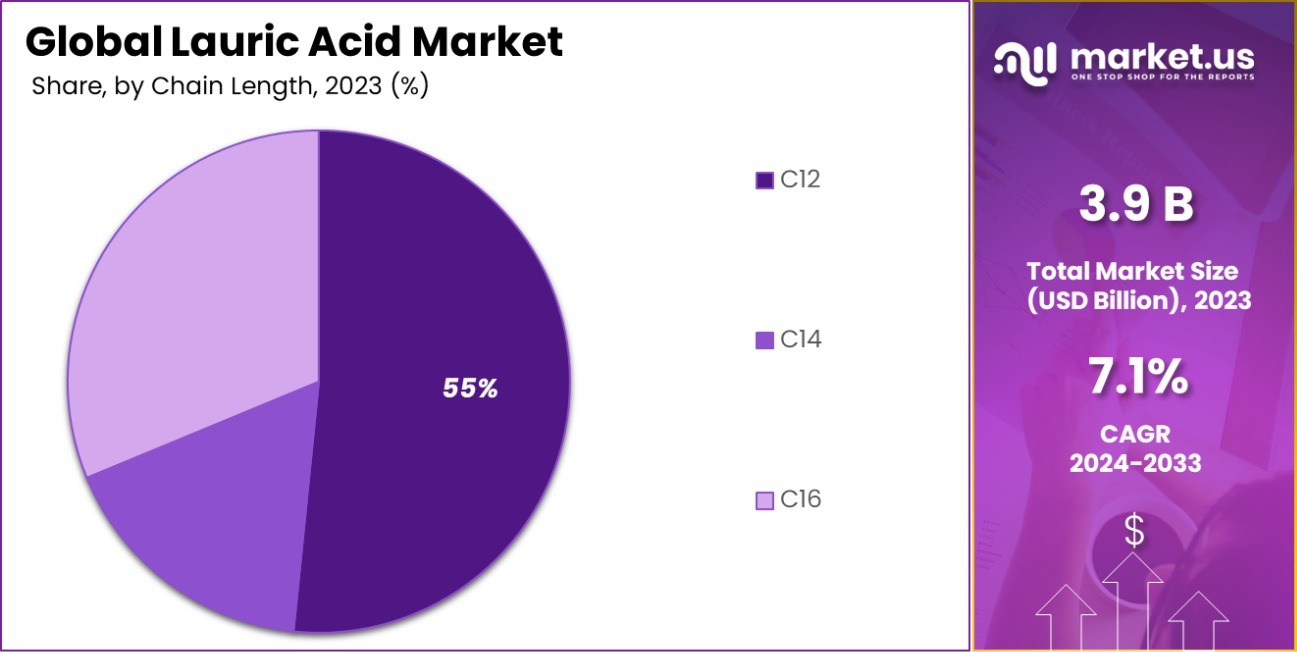

- C12 chain length lauric acid is the most prevalent, comprising 54.5% of the market.

- As an emulsifier, lauric acid holds a 26.5% share in various application sectors.

- The cosmetics and personal care sector is a major end-user, utilizing 29.5% of lauric acid.

- In 2023, the Lauric Acid Market in North America captured a 32.4% share, reaching a valuation of USD 1.2 billion.

By Form Analysis

The Lauric Acid Market sees 47.4% of its products supplied in liquid form, indicating predominant consumption preferences.

In 2023, the “By Form” segment of the Lauric Acid Market was distinctly categorized into three forms: Crystalline, Powder, and Liquid. Liquid held a dominant market position, accounting for 47.4% of the segment. This prominence can be attributed to the form’s versatility and efficiency in various industrial applications, including the production of soaps, detergents, and personal care products.

Crystalline form followed, capturing 32.1% of the market share. Its significant usage in the food industry, particularly as a preservative and fat source in baked goods, underpins its substantial market share. The Powder form held the smallest share at 20.5%, utilized primarily in the pharmaceutical and cosmetic sectors for its ease of solubility and mixture stability.

The distribution of market shares across these forms highlights distinct preferences and technological applications specific to each form. The Liquid form’s leadership is reinforced by its broad application spectrum and efficiency in production processes, making it a preferred choice for manufacturers seeking cost-effective and high-performance solutions in lauric acid-based products.

By Purity Analysis

In terms of purity, 47.5% of lauric acid produced falls within the high-purity range of 85-98%.

In 2023, the “By Purity” segment of the Lauric Acid Market was stratified into four categories: Low Purity (<70%), Medium Purity (70-85%), High Purity (85-98%), and Ultra High Purity (98-99%). High Purity (85-98%) held a dominant market position, capturing 47.5% of the segment. This segment’s leadership can be attributed to its optimal balance between cost and performance, making it highly sought after in both industrial and consumer product applications.

Medium Purity (70-85%) accounted for 26.2% of the market, preferred in applications where moderate lauric acid concentration is sufficient, such as in certain types of cleansers and industrial solvents. Low Purity (<70%) held a smaller share of 15.3%, utilized mainly in applications where high concentrations of lauric acid are unnecessary, such as in some low-grade industrial processes.

Lastly, Ultra High Purity (98-99%) made up 11.0% of the market, used predominantly in high-end cosmetics and pharmaceuticals, where exceptional purity is crucial for product efficacy and safety.

The distribution of these market shares underscores the varied demand across different applications, with High Purity lauric acid leading due to its extensive applicability and efficient performance in a broad range of products.

By Chain Length Analysis

A majority of the market, 54.5%, is dominated by the C12 chain length, highlighting its widespread industrial use.

In 2023, the “By Chain Length” segment of the Lauric Acid Market was distinctly categorized into three chain lengths: C12, C14, and C16. C12 held a dominant market position, accounting for 54.5% of the segment. This leadership can be attributed to its widespread use in the manufacture of surfactants and soaps due to its optimal balance of solubility and detergent properties.

Following C12, C14 captured 29.7% of the market share. This chain length is preferred in the production of medium-chain triglycerides (MCTs) used in nutritional supplements and specialty diets, reflecting its specific functional benefits in health and wellness applications.

C16, known for its stearic properties, held the smallest share at 15.8%. It is primarily utilized in the production of harder soaps and stearate derivatives, which are less in demand compared to products derived from C12 and C14.

The dominance of C12 in the market is reinforced by its versatility and efficacy in a broad range of industrial and consumer products, making it a fundamental component in numerous chemical formulations where performance and cost-efficiency are crucial. The distinct market preferences highlight the targeted applications and functional roles that different chain lengths play in the lauric acid industry.

By Application Analysis

As an emulsifier, lauric acid commands 26.5% of its market application, essential for food and cosmetic formulations.

In 2023, the “By Application” segment of the Lauric Acid Market was categorized into five key applications: Emulsifier, Additive, Chemical Intermediate, Lubricant, and Surfactant. Emulsifiers held a dominant market position, accounting for 26.5% of the segment. This prominence can be attributed to its critical role in food processing and cosmetics, where it facilitates the blending of ingredients that otherwise do not mix well, enhancing product stability and texture.

Surfactant followed closely, capturing 24.3% of the market share, driven by its widespread use in detergents and cleaners due to its effective grease-cutting and foaming properties. Chemical Intermediate was next, holding a 20.2% share, essential in synthesizing more complex chemical formulations used across various industries, including pharmaceuticals and plastics.

Additive accounted for 18.1% of the market, utilized for its properties that enhance the performance of products in food and industrial applications. Finally, Lubricants comprised 10.9% of the market, employed in the manufacturing and automotive sectors for their ability to reduce friction and wear in machinery.

The distribution of these shares highlights the diverse applications of lauric acid, with its use as an emulsifier leading due to its indispensable benefits in product formulation and quality enhancement across multiple industries.

By End Use Analysis

In the cosmetics and personal care sector, lauric acid is used in 29.5% of end-use applications, underscoring its versatility.

In 2023, the “By End Use” segment of the Lauric Acid Market was extensively categorized across six sectors: Plastics & Polymers, Food & Beverage, Textiles, Cosmetics & Personal Care, Soaps & Detergents, and Pharmaceuticals.

Cosmetics & Personal Care held a dominant market position, accounting for 29.5% of the segment. This sector’s leadership can be attributed to the extensive use of lauric acid as a surfactant and emulsifier in products such as moisturizers, shampoos, and other skincare items, where it enhances texture and stability.

Soaps & Detergents followed with a 23.7% share, owing to lauric acid’s effectiveness in soap-making processes where it contributes to lather quality and cleansing properties. Pharmaceuticals captured 18.6% of the market, leveraging lauric acid in medicinal formulations for its antimicrobial and anti-inflammatory properties.

Food & Beverage accounted for 14.2%, utilizing lauric acid as a food additive in confectionery and baked goods. Plastics & Polymers and Textiles sectors held smaller shares of 8.6% and 5.4%, respectively, where lauric acid is used to improve product durability and texture.

The prominence of the Cosmetics & Personal Care sector highlights lauric acid’s crucial role in enhancing product quality and consumer satisfaction in personal care formulations, underscoring its importance in daily consumer products.

Key Market Segments

By Form

- Crystalline

- Powder

- Liquid

By Purity

- Low Purity (<70%)

- Medium Purity (70-85%)

- High Purity (85-98%)

- Ultra High Purity (98-99%)

By Chain Length

- C12

- C14

- C16

By Application

- Emulsifier

- Additive

- Chemical Intermediate

- Lubricant

- Surfactant

- Others

By End Use

- Plastics & Polymers

- Food & Beverage

- Textiles

- Cosmetics & Personal Care

- Soaps & Detergents

- Pharmaceuticals

- Others

Driving Factors

Increasing Demand for Natural Cosmetics and Personal Care Products

The surge in consumer preference for natural and organic ingredients in cosmetics and personal care products is a major driving factor for the lauric acid market. Lauric acid, derived from natural sources like coconut oil, is favored for its moisturizing and antimicrobial properties.

This trend is bolstered by growing awareness about the benefits of using natural substances over synthetic chemicals, leading to increased demand in sectors such as skincare, haircare, and other personal care essentials.

Expansion of the Global Soap and Detergent Industry

The expansion of the global soap and detergent industry, fueled by rising hygiene awareness and higher standards of living worldwide, significantly drives the demand for lauric acid. As a key ingredient in soaps and detergents, lauric acid’s ability to create lather and remove oils and dirt makes it indispensable in household and industrial cleaning products. This ongoing expansion is expected to continue as emerging markets grow and sanitation practices improve globally.

Growth in Food Processing and Pharmaceutical Applications

Lauric acid’s role as an emulsifier and preservative in food processing, coupled with its antimicrobial properties in pharmaceuticals, contributes significantly to its market growth. In the food industry, it helps extend shelf life and maintain product consistency, while in pharmaceuticals, it is used in formulations for its health benefits, including combating bacteria and viruses. This versatility in high-value industries supports a steady demand trajectory for lauric acid.

Restraining Factors

Volatility in Raw Material Prices Affects Production Costs

The fluctuation in prices of raw materials such as coconut and palm kernel oil, primary sources of lauric acid, poses a significant challenge to the market. These price variations can lead to inconsistent production costs, affecting profitability for manufacturers.

Such economic unpredictability can deter investment in lauric acid production, restraining market growth as producers may seek more stable alternatives to manage costs effectively.

Stringent Environmental Regulations Limit Market Expansion

Tightening environmental regulations regarding the extraction and processing of natural oils for lauric acid production are restricting market growth. These regulations aim to reduce environmental impact but can increase production costs and operational complexity.

Compliance requires significant investment in cleaner technologies and practices, which can be a barrier for smaller producers or those in regions with less regulatory support, thus hindering market expansion.

Competition from Synthetic Alternatives in the Market

The availability of synthetic alternatives to lauric acid, which are often cheaper and more readily available, is a major restraining factor. These synthetic compounds can mimic or surpass the functionality of lauric acid in various applications, such as in soaps, detergents, and cosmetics.

The competitive pricing and stable supply of these alternatives make them attractive to manufacturers, potentially reducing the market share for natural lauric acid.

Growth Opportunity

Developing Markets Offer New Avenues for Market Expansion

Emerging economies present significant growth opportunities for the lauric acid market, driven by increasing industrialization and consumer spending power. As these markets develop, demand for consumer goods, including cosmetics, personal care products, and cleaning agents that contain lauric acid, is expected to rise.

Companies can capitalize on this trend by expanding their distribution networks and production facilities in these regions, thereby tapping into new consumer bases eager for quality products.

Technological Advancements in Lauric Acid Processing

Innovation in processing technologies offers a substantial growth opportunity for the lauric acid market. Advances in extraction and processing techniques can lead to more efficient and environmentally friendly methods of producing lauric acid.

This can reduce production costs and minimize environmental impacts, making lauric acid products more competitive against synthetic alternatives. Companies investing in these technologies can gain a significant advantage by meeting the increasing consumer demand for sustainable and cost-effective products.

Increasing Use in Health and Wellness Products

The health and wellness sector’s expansion provides a robust opportunity for growth in the lauric acid market. Lauric acid’s natural antimicrobial and anti-inflammatory properties make it an attractive ingredient in health-oriented products, including weight management supplements and functional foods.

As consumer focus shifts towards healthier lifestyles and natural products, the demand for lauric acid in this sector is expected to increase, offering lucrative prospects for producers and marketers in the industry.

Latest Trends

Rising Popularity of Sustainable and Eco-Friendly Products

The increasing consumer preference for sustainable and eco-friendly products is a prominent trend in the lauric acid market. As awareness about environmental issues grows, more consumers are choosing products made from natural, renewable resources, including lauric acid derived from coconut and palm kernel oil.

This trend is prompting manufacturers to highlight the natural origins and biodegradability of their products, enhancing their appeal to environmentally conscious consumers and potentially increasing market share in the green product segment.

Integration of Lauric Acid in Innovative Cosmetic Formulations

Lauric acid is becoming a key ingredient in innovative cosmetic formulations, a trend driven by its beneficial properties for skin care products, such as moisturizing and antimicrobial effects. Cosmetics manufacturers are incorporating lauric acid into a wider range of products, from anti-acne treatments to anti-aging creams, to leverage these benefits. This integration caters to the growing consumer demand for multifunctional and effective cosmetic solutions, expanding lauric acid’s applications and its market reach.

Expansion of Lauric Acid Applications in Food Preservation

The use of lauric acid in food preservation is a growing trend, as it offers natural antimicrobial properties that enhance food safety and extend shelf life without the use of synthetic preservatives. This trend is particularly relevant in the food and beverage industry, where there is a shift towards cleaner labels and healthier ingredients.

As consumers increasingly prefer foods with natural preservatives, the demand for lauric acid in this application is likely to see substantial growth, presenting new opportunities for producers in the food sector.

Regional Analysis

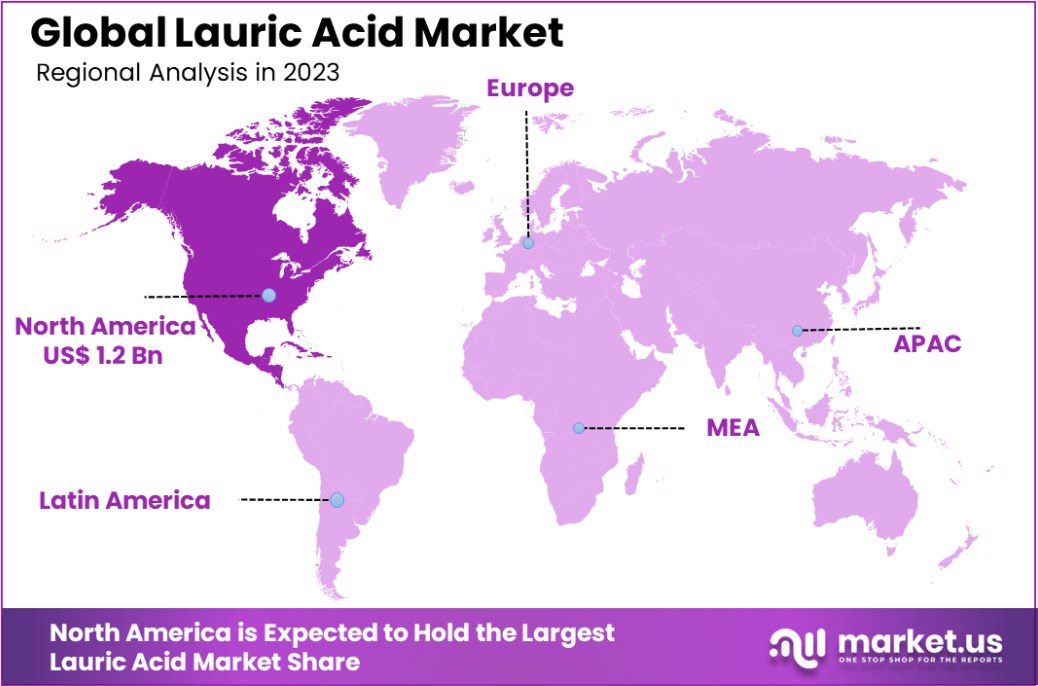

In 2023, North America’s Lauric Acid Market held a 32.4% share, valued at USD 1.2 billion.

The Lauric Acid Market demonstrates diverse dynamics across key regions, including North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. Each region reflects distinct market penetration and growth opportunities influenced by local industrial activities, consumer preferences, and regulatory landscapes.

North America emerges as the dominant region, commanding a 32.4% market share with a value of USD 1.2 billion. This robust performance is supported by the region’s advanced industrial base, particularly in cosmetics and personal care, as well as stringent regulatory standards promoting the use of sustainable and natural ingredients.

Europe follows closely, driven by a strong emphasis on environmentally friendly and bio-based products. The region’s market is bolstered by proactive government policies favoring green chemistry, making significant contributions to the overall market growth. European consumers’ high awareness and preference for natural personal care products further stimulate demand for lauric acid.

Asia Pacific is identified as a high-growth region, thanks to rapid industrialization and expanding manufacturing sectors in countries like China, India, and Southeast Asia. The region benefits from abundant raw material availability and the presence of key players in the lauric acid supply chain, which are pivotal in meeting both domestic and global demand.

The Middle East & Africa and Latin America are gradually catching up, with increasing investments in industrial sectors and rising consumer spending power. These regions exhibit potential for significant market expansion due to untapped market niches and increasing awareness of health and wellness products.

Overall, the global distribution of the Lauric Acid Market is shaped by regional trends in industrial applications, consumer behaviors, and regulatory frameworks, with North America taking the lead followed by Europe and rapidly growing contributions from Asia Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the competitive landscape of the global Lauric Acid Market was significantly shaped by the strategic activities of key players such as AAK AB, Acme-Hardesty, Bakrie Group, BASF SE, Cailà & Parés, Eastman Chemical Company, Emery Oleochemicals, Godrej Industries, International Ltd., WVF LLC, IOI Corporation Berhad, Kao Corporation, Kimia Farma Tbk, KLK OLEO, Kuala Lumpur Kepong Berhad, and Musim Mas Holdings Pte. Ltd.

These companies have been instrumental in driving the market forward through their robust production capabilities, extensive distribution networks, and strong focus on research and development.

AAK AB and BASF SE, for instance, have capitalized on their positions by investing in sustainable and high-purity lauric acid, aligning with global trends towards natural and environmentally friendly products. Similarly, Eastman Chemical Company and Emery Oleochemicals have focused on developing innovative applications of lauric acid in niche markets like pharmaceuticals and food preservatives, expanding their market reach.

Companies like KLK OLEO and Musim Mas Holdings Pte. Ltd. have leveraged their geographic advantage in Asia Pacific, a region abundant in raw materials like coconut and palm kernel oil, to enhance their production efficiency and cost-effectiveness. This strategic positioning allows them to dominate the supply chain in key growth markets.

Furthermore, entities such as Kao Corporation and Godrej Industries have been pivotal in integrating lauric acid into consumer products, particularly in the cosmetics and personal care sector, which continues to see expanding demand.

Overall, these key players are not only responding to current market demands but are also shaping future market dynamics by fostering advancements in lauric acid applications and sustainability practices. Their efforts are critical in maintaining the vitality and competitiveness of the global Lauric Acid Market

Top Key Players in the Market

- AAK AB

- Acme-Hardesty

- Bakrie Group

- BASF SE

- Cailà & Parés

- Eastman Chemical Company

- Emery Oleochemicals

- Godrej Industries

- International Ltd.

- WVF LLC

- IOI Corporation

- Berhad

- Kao Corporation

- Kimia Farma Tbk

- KLK OLEO

- Kuala Lumpur Kepong Berhad

- Musim Mas Holdings Pte. Ltd.

- Oleon NV

- Omya AG

- Pacific Oleochemicals

- Permata Hijau

- Procter Gamble

- PT. Cisadane Raya

- Stepan Company

- Timur OleoChemicals

- Unilever

- Vantage Group International

- Wilmar

- YASHO INDUSTRIES LTD

Recent Developments

- In 2023, Eastman Chemical Company navigated market challenges by implementing cost-cutting and operational efficiencies, generating a substantial $1.4 billion in cash flow and achieving $200 million in savings against inflation impacts.

- In 2023, BASF SE advanced sustainability in the lauric acid sector by launching innovative products like Lavergy® M Ace 100 L for stain removal in detergents and Sokalan® Ecopure C, a biodegradable polymer for dishwashers. These innovations reflect BASF’s strategy to meet consumer demands and boost environmental sustainability in product development.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.9 Billion |

| Forecast Revenue (2033) | USD 7.7 Billion |

| CAGR (2024-2033) | 7.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Crystalline, Powder, Liquid), By Purity (Low Purity (Less than 70%), Medium Purity (70-85%), High Purity (85-98%), Ultra High Purity (98-99%)), By Chain Length (C12, C14, C16), By Application (Emulsifier, Additive, Chemical Intermediate, Lubricant, Surfactant, Others), By End Use (Plastics and Polymers, Food and Beverage, Textiles, Cosmetics and Personal Care, Soaps and Detergents, Pharmaceuticals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | AAK AB, Acme-Hardesty, Bakrie Group, BASF SE, Cailà & Parés, Eastman Chemical Company, Emery Oleochemicals, Godrej Industries, International Ltd., WVF LLC, IOI Corporation, Berhad, Kao Corporation, Kimia Farma Tbk, KLK OLEO, Kuala Lumpur Kepong Berhad, Musim Mas Holdings Pte. Ltd., Oleon NV, Omya AG, Pacific Oleochemicals, Permata Hijau, Procter Gamble, PT. Cisadane Raya, Stepan Company, Timur OleoChemicals, Unilever, Vantage Group International, Wilmar, YASHO INDUSTRIES LTD |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |