Quick Navigation

Report Overview

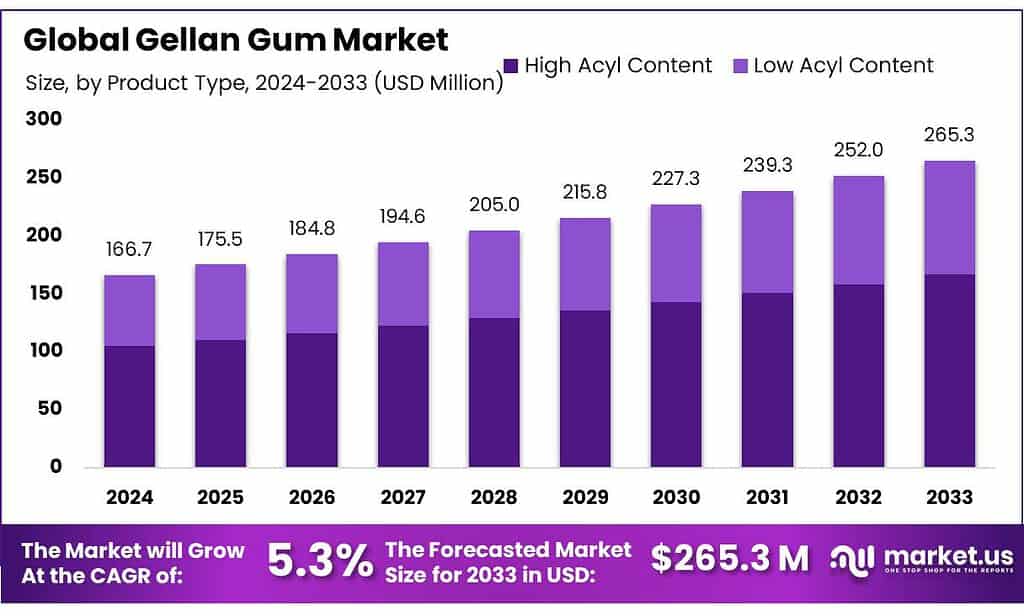

The Global Gellan Gum Market size is expected to be worth around USD 265.3 Mn by 2033, from USD 166.7 Mn in 2023, growing at a CAGR of 5.3% during the forecast period from 2024 to 2033.

Gellan gum is a water-soluble polysaccharide produced by fermentation by the bacterium Sphingomonas elodea. Originally discovered as a bacterial product, it has been commercially manufactured and used primarily as a gelling agent or thickener in the food industry. Gellan gum is valued for its high gel strength and ability to form gels at low concentrations, which makes it effective in small amounts.

Gellan gum, a versatile gelling agent, is utilized across various industries, each reflecting significant growth and demand. In the food and beverage industry, gellan gum’s role is crucial, particularly in vegan and health-oriented products which are part of a market expected to grow by 10% annually.

Regulatory environments in major markets such as the EU and the USA have approved gellan gum for use, with the EU specifying under Regulation (EU) No 231/2012 and the FDA in the USA approving its use with certain limits.

The global dynamics of gellan gum are influenced by major export activities from China, which sends about 40% of its production to North America and Europe, while the EU imports over 5,000 tons annually to support its food and pharmaceutical sectors.

The sector has seen robust investment activities; EU-funded biopolymer research projects received around €10 million over the past five years, and private investments in bio-based polymer production, including gellan gum, exceeded $100 million globally in 2022.

The market is ripe with innovation; recent acquisitions include a notable $500 million purchase by a leading food ingredient company to diversify its gellan gum portfolio. Partnerships are also shaping the market, such as the $30 million joint venture between two chemical companies to enhance production efficiency.

Technological advancements in fermentation have improved gellan gum yields by 20% since 2021. The introduction of a new low-acyl gellan gum variant in 2023, designed for high-clarity gel applications, marks a significant product development.

Production capacity is also set to expand, with a $20 million investment projected to increase production by 25% by 2025, further emphasizing the critical and expanding role of gellan gum in global markets.

Key Takeaways

- Gellan Gum Market size is expected to be worth around USD 265.3 Mn by 2033, from USD 166.7 Mn in 2023, growing at a CAGR of 5.3%.

- High Acyl Content held a dominant market position, capturing more than a 63.3% share.

- Thickener held a dominant market position in the gellan gum industry, capturing more than a 34.4% share.

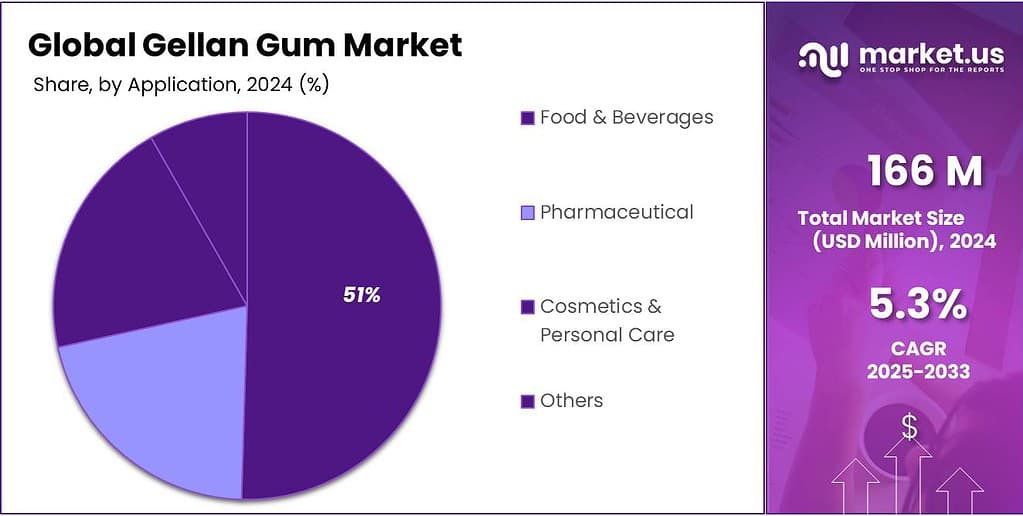

- Food & Beverages sector held a dominant market position in the gellan gum industry, capturing more than a 51.4% share.

- Supermarkets/Hypermarkets held a dominant market position in the distribution of gellan gum, capturing more than a 37.4% share.

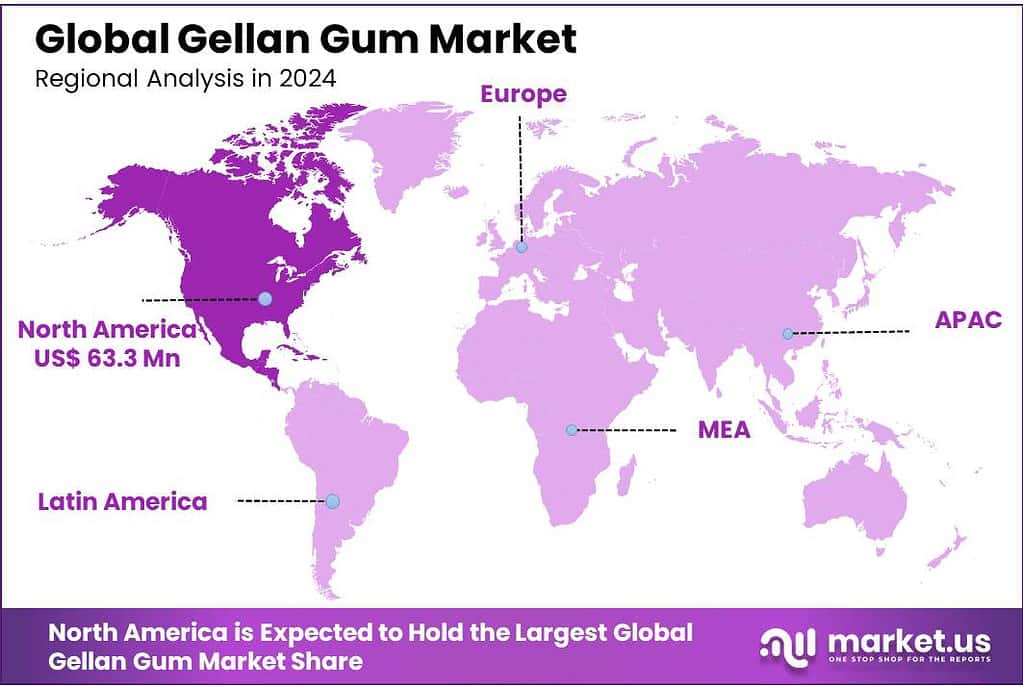

- North America emerges as the leading region, holding a significant 38% market share with a valuation of approximately USD 63.3 million.

By Product Type

In 2023, High Acyl Content held a dominant market position, capturing more than a 63.3% share. This segment is particularly favored for its ability to produce soft, elastic gels, making it suitable for a variety of food applications that require a flexible texture.

High Acyl Gellan Gum is extensively used in products such as dairy alternatives, desserts, and certain beverages where a smooth and pleasing mouthfeel is essential. Its popularity is supported by the rising consumer preference for clean-label products, which are perceived as healthier and more natural.

Low Acyl Content Gellan Gum, while holding a smaller market share, is highly valued for its ability to form firm, brittle gels. This type is indispensable in applications requiring precise gelling properties, such as in jellies, fillings, and some confectionery items.

Its firm texture makes it an ideal choice for structured yet edible products. Despite its lower market share, the demand for Low Acyl Gellan Gum remains robust, driven by its unique functional properties that are irreplaceable in specific culinary and industrial applications.

By Application

In 2023, Thickener held a dominant market position in the gellan gum industry, capturing more than a 34.4% share. This application is highly favored due to gellan gum’s effectiveness in providing the desired viscosity and consistency in products such as sauces, dressings, and some dairy goods. Its ability to create a smooth texture without altering flavor makes it indispensable in culinary applications.

Stabilizer and Emulsifier applications also play critical roles, utilizing gellan gum to maintain uniformity and stability in products like beverages and creams. As a stabilizer, gellan gum prevents ingredients from separating, thus ensuring consistent quality and texture. As an emulsifier, it helps in blending ingredients that typically do not mix well, such as oil and water.

The Gelling application of gellan gum is fundamental in products requiring gel formation, such as jellies and chewable gummies. Gellan gum is chosen for its precision in gel strength and its ability to form clear, aesthetic gels that are appealing in food presentation.

Coating applications involve gellan gum for its film-forming ability, which is beneficial in various food coatings to lock in freshness and enhance texture. Meanwhile, Texturizing is crucial for modifying the mouthfeel and texture of food products, an attribute that manufacturers prioritize to meet consumer preferences for specific tactile experiences.

By End Use

In 2023, the Food & Beverages sector held a dominant market position in the gellan gum industry, capturing more than a 51.4% share. This sector primarily utilizes gellan gum for its superior gelling, thickening, and stabilizing properties, making it a key ingredient in a variety of products such as plant-based milks, jellies, and sauces. Its functionality enhances texture and consistency, crucial for consumer satisfaction and product differentiation in the highly competitive food market.

The Pharmaceutical sector also significantly incorporates gellan gum, particularly in applications requiring controlled-release mechanisms in capsules and tablets, as well as in suspensions. Its unique properties help in stabilizing formulations and improving the delivery of active pharmaceutical ingredients.

In Cosmetics & Personal Care, gellan gum is valued for its ability to create gel-like textures and stabilize emulsions in products such as lotions, creams, and serums. The demand in this sector is driven by the growing consumer preference for products with natural ingredients.

By Distribution Channel

In 2023, Supermarkets/Hypermarkets held a dominant market position in the distribution of gellan gum, capturing more than a 37.4% share. This channel’s prominence is attributed to its widespread accessibility and convenience, offering consumers a variety of gellan gum-based products under one roof. The extensive reach and established logistics of supermarkets and hypermarkets ensure that they remain a preferred choice for the bulk purchase of both food and non-food items containing gellan gum.

Online Stores are rapidly gaining market share, driven by the shift in consumer shopping behaviors towards digital platforms. These stores offer the convenience of home delivery, a broader range of product selections, and often, competitive pricing, which appeals to a tech-savvy demographic.

Specialty Stores also play a crucial role in the gellan gum market, especially for consumers looking for specific, high-quality gellan gum applications such as in premium cosmetics or specialized health food products. These stores often provide expert advice and higher customer service.

Direct Sales are significant in the B2B sector, where gellan gum manufacturers sell directly to food and beverage producers, pharmaceutical companies, and other industrial users. This channel helps in maintaining strong relationships between manufacturers and large-volume customers.

Key Market Segments

By Product Type

- High Acyl Content

- Low Acyl Content

By Application

- Thickener

- Stabilizer

- Emulsifier

- Gelling

- Coating

- Texturizing

By End Use

- Food & Beverages

- Pharmaceutical

- Cosmetics & Personal Care

- Others

By Distribution Channel

- Online Stores

- Supermarkets/Hypermarkets

- Specialty Stores

- Direct Sales

- Others

Driving Factors

Growing Demand for Plant-Based and Clean-Label Products

A key driver for the gellan gum market is the surging consumer preference for plant-based and clean-label products. As consumers increasingly seek food products made with natural ingredients and minimal processing, gellan gum is becoming a popular choice due to its natural, plant-derived composition. This trend is particularly pronounced in the food and beverage industry, where gellan gum’s functionality as a stabilizer and thickener aligns with the demand for healthier, more sustainable consumption options.

Expansion in Food and Beverage Applications

The food and beverage sector continues to dominate the use of gellan gum, leveraging its superior properties as a gelling agent, stabilizer, and emulsifier. The versatility of gellan gum makes it ideal for a wide array of applications, including dairy products, confectionery, and beverages. Its ability to improve texture and stability in these products helps manufacturers meet the evolving tastes and dietary preferences of consumers, further driving market growth.

Technological Advancements in Production

Advancements in production technologies are also pivotal in driving the gellan gum market. Innovations in fermentation and processing have enhanced the efficiency and quality of gellan gum production, making it more cost-effective and accessible for wider industrial applications. These technological improvements not only support scale-up initiatives but also enable the development of new gellan gum formulations that meet specific industry needs.

Restraining Factors

High Production Costs and Limited Raw Material Availability

One of the most significant challenges facing the gellan gum market is the high cost associated with its production. Gellan gum is produced through a fermentation process, which requires precise control and specific conditions, leading to higher operational costs. Additionally, the raw materials needed for its production are not abundantly available, which can lead to supply chain issues and further increase costs.

Competition from Alternative Products

Gellan gum faces considerable competition from other hydrocolloids that offer similar functional properties. Products like xanthan gum, carrageenan, and agar-agar are often available at lower costs and are used widely across industries, including food and pharmaceuticals. This competition can limit the potential market share for gellan gum, as manufacturers may opt for more cost-effective alternatives that fulfill the same roles.

Regulatory and Compliance Challenges

Navigating the regulatory landscape can also pose a significant barrier to the growth of the gellan gum market. Each region has its own set of regulations regarding food additives, which can vary widely. Complying with these regulations incurs additional costs and requires extensive documentation and testing to ensure product safety and efficacy, which can delay product launches and restrict market entry in certain regions.

Growth Opportunity

Rising Consumer Demand for Functional and Fortified Foods: The gellan gum market is well-positioned to capitalize on the increasing consumer interest in functional foods—those offering health benefits beyond basic nutrition. This trend is particularly strong in the food and beverage sector, where gellan gum’s properties as a stabilizer, gelling agent, and emulsifier enable the production of fortified and functional beverages and foods. These products often contain added vitamins, minerals, and other health-promoting ingredients, with gellan gum ensuring their proper suspension and distribution within the product.

Technological Advancements in Food Processing: Advancements in food technology and processing continue to open new avenues for gellan gum, particularly in the creation of innovative food textures and stability solutions. These advancements not only improve the functional quality of gellan gum but also enhance its appeal in vegan and vegetarian products, aligning with the growing consumer preference for plant-based diets. The ability to replace animal-derived gelling agents with gellan gum in these applications presents a significant opportunity for market growth.

Sustainability and Clean Label Trends: Sustainability initiatives and the clean label movement are driving the demand for ingredients like gellan gum, which are perceived as natural and environmentally friendly. Manufacturers are increasingly seeking eco-friendly production methods and sourcing practices, and gellan gum fits well into this narrative. Its functionality in low pH environments and adaptability for vegan and vegetarian products accentuates its end-use scope across various sectors, making it a key player in the push towards more sustainable and transparent food production processes

Latest Trends

Shift Toward Natural and Sustainable Products

The gellan gum market is significantly influenced by the rising consumer demand for natural and sustainable products. This trend is driving manufacturers to adopt more eco-friendly production methods and sourcing practices. The increasing preference for plant-based and clean-label products is shaping the market, as gellan gum’s natural qualities make it an ideal fit for these categories. This shift is not just prevalent in the food industry but also in pharmaceuticals and personal care, where there’s a growing emphasis on sustainability.

Technological Advancements in Production

Technological innovations in the production of gellan gum are leading to more efficient manufacturing processes. Improvements in fermentation and processing technologies have enhanced the quality and functionality of gellan gum, making it more cost-effective and accessible for various applications. These advancements are crucial as they allow for the broader use of gellan gum in the food and beverage industry, including in vegan and vegetarian products, where it provides essential gelling and stabilizing properties.

Expansion in Functional Foods and Nutraceuticals

There’s a noticeable growth in the use of gellan gum within the nutraceutical sector and in the development of functional foods. Its versatility is highly valued for formulating dietary supplements and functional foods that offer health benefits beyond basic nutrition. The focus on health and wellness continues to drive innovation in this area, leveraging gellan gum for its stabilizing and texturizing properties, which are essential for enhancing the delivery of nutrients and active ingredients

Regional Analysis

North America emerges as the leading region, holding a significant 38% market share with a valuation of approximately USD 63.3 million. This dominance is fueled by robust demand from the food and beverage sector, particularly for low-calorie and clean-label products. The United States leads in this regard, capitalizing on advanced food processing technologies and a rising consumer preference for plant-based diets, which extensively utilize gellan gum as a stabilizer and thickener.

Europe follows closely, where sustainability and stringent food safety regulations drive the demand for natural and safe food additives. European manufacturers are increasingly incorporating gellan gum to comply with the clean label trend that dominates the food industry across key markets such as Germany, France, and the UK. This region is also significant for its technological advancements in food production, aiding the proliferation of functional and fortified foods.

Asia Pacific is noted for its rapid growth, propelled by expanding food and beverage industries in emerging economies like China and India. The increase in disposable incomes and urbanization contributes to the heightened demand for processed foods, where gellan gum is essential for texture and stability. This region also benefits from a growing awareness of health and wellness, boosting the use of gellan gum in functional foods and beverages.

Middle East & Africa and Latin America are emerging markets with growing potentials, driven by increasing industrial activities and the adoption of Western eating habits. These regions are experiencing a slow yet steady increase in the use of food additives like gellan gum, supporting local food manufacturing capacities and gradually adopting more sophisticated food processing standards.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Gellan Gum market is characterized by a competitive and diversified landscape, featuring a range of key players from global giants to specialized local firms. Companies like CP Kelco and DuPont de Nemours, Inc. are prominent players, known for their extensive research and development capabilities and wide range of gellan gum products suited for various applications from food and beverage to pharmaceuticals. These companies have a strong global presence and are active in innovation to meet the evolving demands of the market.

DSM Food Specialties B.V. and Cargill, Incorporated also hold significant positions in the market, leveraging their large-scale operations and international networks to distribute gellan gum globally. These players focus on sustainable practices and clean label solutions, aligning with the current consumer trends toward healthier and more natural products.

On the other hand, regional players like Inner Mongolia Rainbow Biotech Co., Ltd., Hebei Xinhe Biochemical Co., Ltd., and Zhejiang Zhongken Biotech Co., Ltd. contribute to the market with their localized expertise and customized product offerings. These companies often focus on specific market niches, such as high acyl gellan gum production or the development of specialized gellan gum applications for regional food and beverage manufacturers.

Top Key Players in the Market

- CP Kelco

- Inner Mongolia Rainbow Biotech Co., Ltd.

- Jungbunzlauer Suisse AG

- DuPont de Nemours, Inc.

- Shanghai Fortune Biotech Co., Ltd.

- DSM Food Specialties B.V.

- Zhejiang Tech-Way Biochemical Co., Ltd.

- Merck KGaA

- Cargill, Incorporated

- IHC Chempharm

- Xi’an Sheerherb Biological Technology Co., Ltd.

- Fufeng Group Company Limited

- Zhejiang Zhongken Biotech Co., Ltd.

- Hebei Xinhe Biochemical Co., Ltd.

- Deosen Biochemical (Ordos) Ltd.

- Shanghai Kaison Chemicals Co., Ltd.

- Dancheng Caixin Sugar Industry Co., Ltd.

- Tianshen (Group) Holdings Co., Ltd.

- TIC Gums, Inc.

- Silver Fern Chemical, Inc.

Recent Developments

In 2024, the gellan gum market, including contributions from companies like Inner Mongolia Rainbow Biotech, is projected to see substantial growth, with market valuations expected to increase notably.

In 2021, CP Kelco launched KELCOGEL® DFA Gellan Gum, a dual-function gellan gum solution designed specifically for formulating plant-based dairy alternative beverages.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 166.7 Mn |

| Forecast Revenue (2033) | USD 265.3 Mn |

| CAGR (2024-2033) | 5.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type(High Acyl Content, Low Acyl Content), By Application(Thickener, Stabilizer, Emulsifier, Gelling, Coating, Texturizing), By End Use(Food and Beverages, Pharmaceutical, Cosmetics and Personal Care, Others), By Distribution Channel(Online Stores, Supermarkets/Hypermarkets, Specialty Stores, Direct Sales, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | CP Kelco, Inner Mongolia Rainbow Biotech Co., Ltd., Jungbunzlauer Suisse AG, DuPont de Nemours, Inc., Shanghai Fortune Biotech Co., Ltd., DSM Food Specialties B.V., Zhejiang Tech-Way Biochemical Co., Ltd., Merck KGaA, Cargill, Incorporated, IHC Chempharm, Xi’an Sheerherb Biological Technology Co., Ltd., Fufeng Group Company Limited, Zhejiang Zhongken Biotech Co., Ltd., Hebei Xinhe Biochemical Co., Ltd., Deosen Biochemical (Ordos) Ltd., Shanghai Kaison Chemicals Co., Ltd., Dancheng Caixin Sugar Industry Co., Ltd., Tianshen (Group) Holdings Co., Ltd., TIC Gums, Inc., Silver Fern Chemical, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |