Quick Navigation

Report Overview

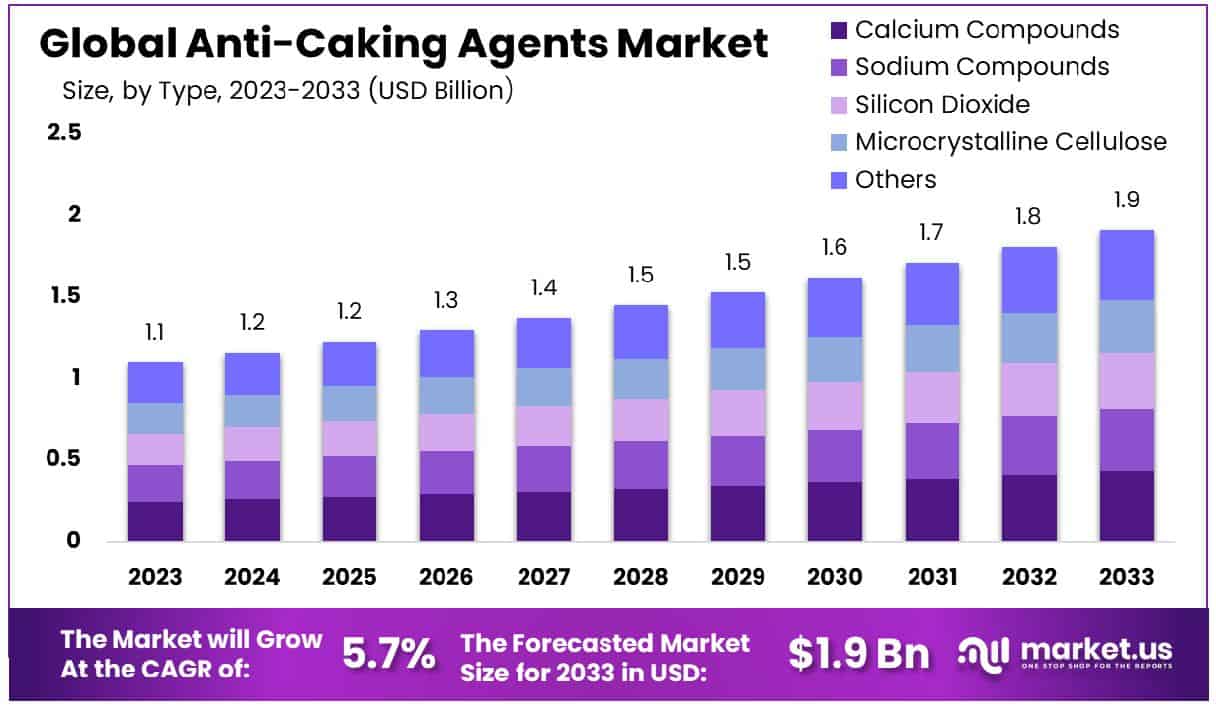

The Global Anti-Caking Agents Market size is expected to be worth around USD 1.9 Billion by 2033, From USD 1.1 Billion by 2023, growing at a CAGR of 5.7% during the forecast period from 2024 to 2033.

The anti-caking agents market comprises substances that prevent the formation of lumps in powdered or granulated materials, ensuring their free-flowing properties. These agents are critical in food processing, cosmetics, and agriculture industries. The market’s growth is driven by increasing demand for processed foods and advancements in packaging technology.

Anti-caking agents enhance the longevity and quality of end products by absorbing excess moisture and preventing clumping. Key stakeholders, including product managers, focus on this market for innovations that can improve product integrity, streamline manufacturing processes, and comply with regulatory standards.

The anti-caking agents market is poised for growth, driven by its indispensable role in enhancing the quality and longevity of various products. Employed across numerous industries including food processing, agriculture, and cosmetics, these agents ensure that powders and granules maintain their free-flowing properties by preventing the formation of clumps. Typically incorporated in minuscule amounts—less than 2% of the total product composition—anti-caking agents are pivotal in maintaining the structural integrity of a wide array of consumables.

A notable application is found in the agriculture sector, where optimized anti-caking agents are crucial for maintaining the efficacy of ammonium nitrate fertilizers. They provide 100% prevention of caking post-granulation and ensure stability over 30 days of storage, significantly enhancing product reliability and farmer satisfaction.

Furthermore, these agents act as essential flow facilitators in various dry goods, ranging from shredded cheese and dried eggs to powdered mixes and spices, as well as in the filtration processes of brewing beer. The regulatory environment, particularly in the United States, mandates a maximum inclusion rate of 2%, highlighting the critical balance between efficacy and compliance.

Key Takeaways

- The Global Anti-Caking Agents Market size is expected to be worth around USD 1.9 Billion by 2033, From USD 1.1 Billion by 2023, growing at a CAGR of 5.7% during the forecast period from 2024 to 2033.

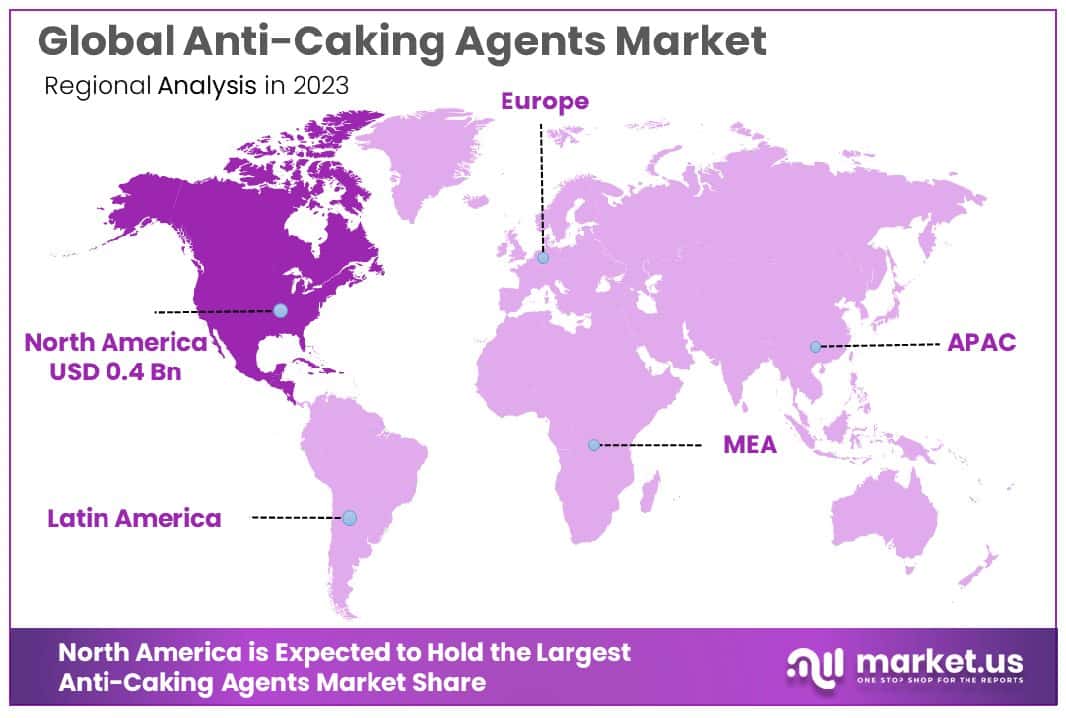

- North America holds 35.6% of the Anti-Caking Agents Market, valued at USD 0.4 billion.

- Silicon Dioxide comprises 22.6% of the Anti-Caking Agents Market.

- Natural sources dominate, constituting 56.4% of the market’s composition.

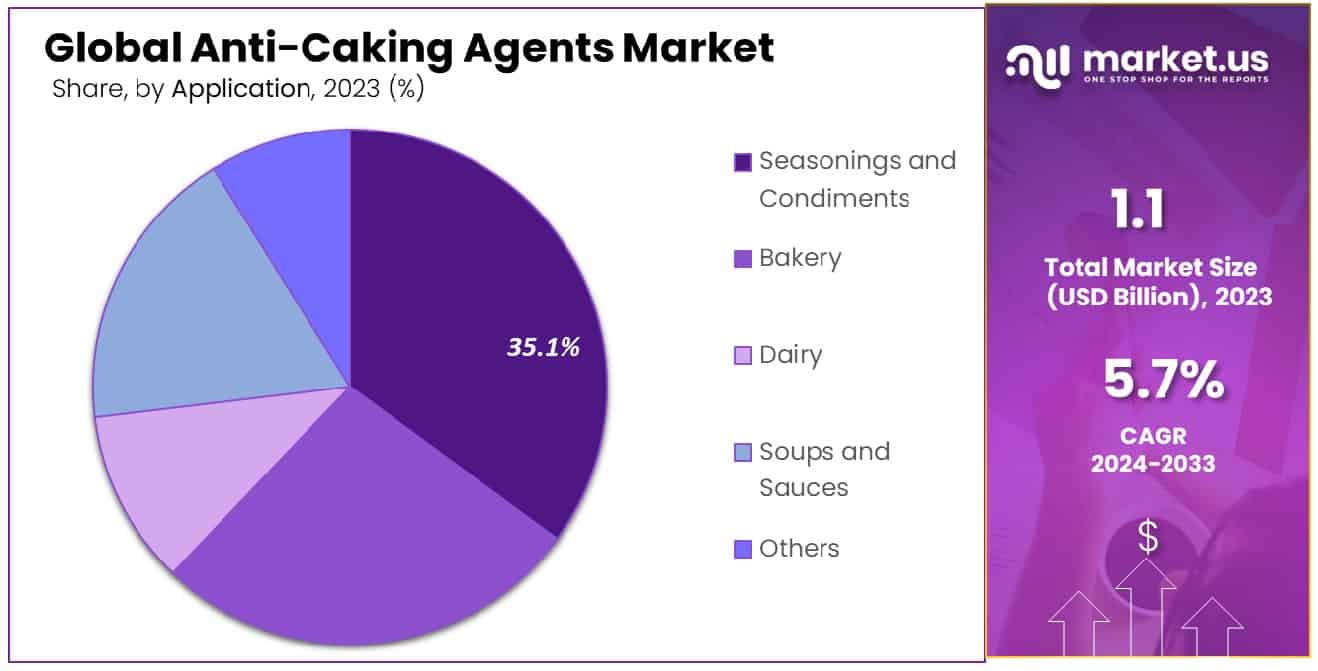

- Seasonings and condiments application leads at 35.1% market share.

Driving Factors

Increased Demand in the Food and Beverage Industry

The growth of the anti-caking agents market is primarily fueled by the escalating demand within the food and beverage industry. Anti-caking agents are critical in ensuring the free-flowing nature of numerous food products, including but not limited to baking ingredients, seasonings, and instant soups. This demand correlates with the rising global consumption of processed and convenience foods.

As urbanization continues and disposable incomes rise, the demand for packaged foods escalates, thereby boosting the need for anti-caking agents to maintain the quality and longevity of these products. Industry reports often highlight how innovations in food formulations drive the consumption of these agents, thereby propelling market growth.

Expansion of the Pharmaceutical Sector

The expansion of the pharmaceutical sector significantly contributes to the growth of the anti-caking agents market. In pharmaceuticals, these agents are indispensable in manufacturing vitamins, minerals, and other dietary supplements, preventing the agglomeration that can affect the efficacy and shelf-life of products.

With the global health consciousness on the rise, particularly post-pandemic, there is a marked increase in the consumption of nutritional supplements, driving the demand for more refined and effective anti-caking solutions in the pharmaceutical industry. This trend is expected to continue, further stimulating market growth.

Advancements in Food Packaging Technology

Advancements in food packaging technology also play a pivotal role in the adoption of anti-caking agents. Modern packaging methods aim to extend the shelf life of food products and maintain their textural and visual appeal. The integration of anti-caking technologies in packaging processes ensures that powdered and granulated products remain free-flowing and visually appealing throughout their shelf life.

This application of anti-caking agents is particularly significant in the context of global trade, where food products are transported over long distances and stored for extended periods, necessitating robust anti-caking solutions to preserve quality and consumer satisfaction.

Restraining Factors

Stringent Regulatory Standards

Stringent regulatory standards significantly restrain the growth of the anti-caking agents market. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) impose strict guidelines on the use of additives in food, which includes anti-caking agents. These regulations often require rigorous testing and verification of the safety and efficacy of these substances before they are approved for use in consumer products.

The complexity and cost of compliance can be high, especially for new entrants in the market or for the introduction of novel anti-caking technologies. This regulatory environment can delay product launches, limit the usage of certain effective but less-studied compounds, and generally slow down market growth.

Volatility in Raw Material Prices

Volatility in the prices of raw materials also poses a significant challenge to the anti-caking agents market. Many anti-caking agents are derived from natural sources such as silica or manufactured from chemical processes involving various minerals and salts.

The prices of these materials can fluctuate widely due to changes in the global commodities market, trade policies, or environmental regulations affecting mineral extraction and processing. This volatility makes it difficult for manufacturers to maintain consistent pricing and profitability, potentially leading to reduced investment in research and development or passing increased costs to consumers, which could dampen market growth.

By Type Analysis

Silicon dioxide holds a 22.6% share in the anti-caking agents market by type.

In 2023, Silicon Dioxide held a dominant market position in the “By Type” segment of the Anti-Caking Agents Market, capturing more than a 22.6% share. This prevalence is attributed to its widespread use across various industries, including food and pharmaceuticals, where it serves as an essential component in maintaining the free-flowing characteristics of powders and granulated materials. Its efficacy and safety profile, approved by regulatory bodies such as the FDA and EFSA, bolster its adoption rate.

Calcium compounds and sodium compounds also play significant roles, with each type favored for specific applications due to their distinct properties. Calcium compounds, often used in baking powders and flour, help prevent clumping under high humidity conditions. Sodium compounds are frequently utilized in salt and seasonings for their excellent moisture-absorbing capabilities.

Microcrystalline cellulose, a refined wood pulp derivative, is gaining traction, particularly in the pharmaceutical sector, where it is prized for its non-reactivity and compatibility with other drug ingredients. This material is also favored for its ability to prevent clumping without impacting the taste or nutritional value of food products.

The “Others” category includes a diverse array of materials such as magnesium stearate and talc, which are selected based on specific industry needs and application requirements. These materials are often chosen for their unique properties that address challenges not sufficiently met by more common anti-caking agents.

By Source Analysis

Natural sources dominate the market, comprising 56.4% of anti-caking agents used globally.

In 2023, Natural sources held a dominant market position in the “By Source” segment of the Anti-Caking Agents Market, capturing more than a 56.4% share. This significant market share reflects a growing consumer preference for natural and organic products, driven by increased health consciousness and a general shift towards sustainability in food production. Natural anti-caking agents, derived from organic or naturally occurring materials, are highly sought after for their minimal processing and perceived health benefits compared to their synthetic counterparts.

On the other hand, synthetic anti-caking agents, while still used extensively, account for a smaller portion of the market. These agents are primarily derived from chemical processes and are valued for their consistency, effectiveness, and cost-efficiency in large-scale industrial applications. However, their market share has seen a gradual decline due to stringent regulatory standards and a shift in consumer preferences towards cleaner labels.

The dominance of natural anti-caking agents is further bolstered by regulatory support in many regions, which are increasingly favoring naturally sourced additives in food and pharmaceutical products. Moreover, the push for clean-label ingredients, which often highlight the absence of synthetic additives, continues to drive consumer demand for natural options.

This trend is expected to persist as more consumers become aware of the contents in their food and pharmaceutical products, and as manufacturers innovate to meet these demands with naturally sourced solutions. The ongoing development and enhancement of natural anti-caking agents are likely to keep this segment in a leading position for the foreseeable future.

By Application Analysis

Seasonings and condiments are the leading applications, accounting for 35.1% of the market.

In 2023, Seasonings and Condiments held a dominant market position in the “By Application” segment of the Anti-Caking Agents Market, capturing more than a 35.1% share. This prominence is driven by the extensive use of these agents in maintaining the quality and consistency of dry mixes, spices, and seasonings, which are susceptible to moisture and clumping. The high demand in this segment is fueled by the global increase in consumption of packaged and ready-to-eat meals, which often rely heavily on seasonings for flavor.

Following behind, the Bakery segment also significantly utilizes anti-caking agents to prevent the clumping of ingredients such as flour, baking powder, and other dry mix components. This application is crucial for ensuring the quality and consistency of baked goods, which affects both texture and taste.

The Dairy segment applies anti-caking agents, particularly in powdered milk, cheese, and other processed dairy products. These agents are essential in maintaining the free-flowing nature of dairy powders and extending the shelf life of grated cheeses by preventing moisture absorption and clumping.

Soups and Sauces represent another key application area. Anti-caking agents in this segment are vital for maintaining the stability and homogeneity of dry soup mixes and sauce powders, ensuring they dissolve properly without forming lumps when reconstituted.

The “Others” category includes a diverse range of applications from pet foods to fertilizers, where anti-caking agents play a critical role in maintaining product quality and handling characteristics.

Key Market Segments

By Type

- Calcium Compounds

- Sodium Compounds

- Silicon Dioxide

- Microcrystalline Cellulose

- Others

By Source

- Natural

- Synthetic

By Application

- Seasonings and Condiments

- Bakery

- Dairy

- Soups and Sauces

- Others

Growth Opportunities

Development of Natural and Organic Anti-Caking Agents

In 2023, a significant opportunity in the global anti-caking agents market lies in the development of natural and organic anti-caking agents. As consumers increasingly demand cleaner labels and more natural products, the industry is responding by innovating and expanding offerings that align with these preferences. The shift towards natural and organic anti-caking agents not only caters to the health-conscious consumer but also complies with stricter regulatory environments that favor naturally sourced ingredients over synthetic alternatives.

This trend is particularly potent in markets like North America and Europe, where organic food sales are experiencing robust growth. Companies that innovate in this space are likely to capture new segments of the market, benefitting from premium pricing and enhanced brand loyalty among health-aware consumers.

Expansion into Emerging Markets

Another significant opportunity for the anti-caking agents market in 2023 is the expansion into emerging markets. Countries in Asia, Africa, and South America are witnessing rapid urbanization, rising incomes, and an increasing propensity for processed and packaged foods. These demographic and economic shifts represent a fertile ground for the introduction and expansion of anti-caking products in local food and pharmaceutical industries.

Moreover, as these markets develop, there is a growing sophistication in food manufacturing and packaging technologies, which further drives the demand for quality-enhancing additives like anti-caking agents. By entering these markets, companies can diversify their geographic risk and tap into new revenue streams, potentially offsetting slower growth in more developed markets.

Latest Trends

Adoption of Nano-Technology in Anti-Caking Formulations

The global anti-caking agents market is witnessing a transformative trend through the adoption of nano-technology in product formulations. This cutting-edge technology enhances the effectiveness and efficiency of anti-caking agents, allowing for smaller amounts to be used while maintaining or improving performance. Nano-scale materials can offer superior dispersion and interaction with food particles, resulting in better prevention of clumping without affecting the taste or quality of the food product.

This trend is particularly appealing to manufacturers looking to innovate in competitive markets, as it aligns with the need for cost-effective solutions that cater to high-volume production needs. The application of nano-technology also opens new avenues for developing advanced food preservation techniques, potentially leading to extended shelf life and reduced waste.

Increased Focus on Clean-Label Ingredients

In 2023, the anti-caking agents market is increasingly driven by consumer demand for clean-label ingredients. This trend reflects a broader shift towards transparency and natural compositions in food products, with consumers seeking out products that are free from synthetic additives and chemicals. The focus on clean-label ingredients compels manufacturers to reformulate existing products and develop new ones that align with this demand. As a result, there is a significant push to identify and utilize anti-caking agents derived from natural sources such as rice flour or cornstarch.

This shift not only responds to consumer preferences but also helps manufacturers differentiate their products in a crowded market, appealing to health-conscious consumers and those with dietary restrictions. The trend towards clean labels is shaping the R&D strategies of companies across the globe, leading to innovations that combine health, sustainability, and efficacy.

Regional Analysis

The North American anti-caking agents market holds a 35.6% share, valued at USD 0.4 billion.

North America dominates the anti-caking agents market, holding a 35.6% share with a market value of USD 0.4 billion. This region’s leadership is driven by advanced food processing industries and high demand for processed and packaged foods, coupled with stringent food safety regulations that necessitate the use of anti-caking agents to maintain product quality and longevity.

Europe follows closely, characterized by mature markets in Western Europe and emerging growth in Eastern Europe. The region’s market expansion is supported by a strong emphasis on clean-label ingredients and the increasing adoption of natural anti-caking agents in response to consumer demand for healthier, less processed foods.

The Asia Pacific region is experiencing the fastest growth due to rapid urbanization, rising income levels, and increasing consumer awareness about food quality. The expanding food and beverage industry, especially in countries like China and India, is propelling the demand for anti-caking agents to enhance the quality and shelf life of products.

The Middle East & Africa region, though smaller in comparison, is gradually recognizing the importance of anti-caking agents, especially in the rapidly growing packaged food sectors. Economic development and urbanization are key drivers in this region, with countries like Saudi Arabia and South Africa leading the way.

Latin America is also showing promising growth, driven by advancements in food technology and increasing local manufacturing capabilities, which support the broader adoption of anti-caking solutions in domestic and regional markets.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

Key Players Analysis

In 2023, the global Anti-Caking Agents Market features a competitive landscape dominated by several key players, each contributing unique strengths and strategies to the industry.

PPG Industries, Inc., renowned for its innovation in materials science, continues to lead with advanced formulations that enhance the efficiency of anti-caking agents in various applications. Evonik Industries AG and Solvay S.A. are pivotal in the development of specialized anti-caking solutions that cater to both the food and pharmaceutical sectors, emphasizing the integration of sustainability into their product lines.

DowDuPont Inc. leverages its vast R&D capabilities to introduce multi-functional anti-caking agents that offer additional benefits such as moisture absorption and improved product dispersibility, which are critical in processed foods and industrial applications. Similarly, BASF SE focuses on tailoring its offerings to meet stringent regulatory standards and consumer demands for cleaner labels.

Kerry Group plc and Agropur Cooperative are key players in the innovation of natural and organic anti-caking agents, responding to the growing consumer trend towards natural ingredients in food products. Univar Solutions Inc. and Innospec Inc. excel in the distribution and development of chemical solutions, ensuring wide accessibility and customization of anti-caking products across global markets.

Cargill, Incorporated and IMCD Group B.V. strengthen market dynamics through extensive supply chains and deep market penetration, which enable efficient distribution and localized customer service. Kao Corporation, Huber Engineered Materials, PQ Corporation, and Wacker Chemie AG are instrumental in driving technological advancements and scalability in the production of anti-caking agents, which are essential for maintaining the quality and longevity of a wide range of consumer products.

Market Key Players

- PPG Industries, Inc.

- Evonik Industries AG

- Solvay S.A.

- DowDuPont Inc.

- BASF SE

- Kerry Group plc

- Agropur Cooperative

- Univar Solutions Inc.

- Innospec Inc.

- Cargill, Incorporated

- IMCD Group B.V.

- Kao Corporation

- Huber Engineered Materials

- PQ Corporation

- Wacker Chemie AG

Recent Development

- In July 2023, DuPont launched a series of advanced anti-caking agents that offer improved performance in extreme conditions, catering especially to the needs of the baking and dairy industries.

- In April 2022, Solvay S.A. introduced a revolutionary anti-caking agent specifically for the Asian markets, addressing unique climate-related clumping challenges in the region. This product launch aligns with Solvay’s strategy to tailor solutions for regional market needs, bolstering its presence in high-growth areas.

- In March 2022, PPG Industries announced the launch of a new, environmentally friendly anti-caking agent designed to meet increasing regulatory demands and consumer preferences for sustainable products. This product aims to reduce clumping in both food and industrial applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.1 Billion |

| Forecast Revenue (2033) | USD 1.9 Billion |

| CAGR (2024-2033) | 5.7% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(Calcium Compounds, Sodium Compounds, Silicon Dioxide, Microcrystalline Cellulose, Others), By Source(Natural, Synthetic), By Application(Seasonings and Condiments, Bakery, Dairy, Soups and Sauces, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | PPG Industries, Inc., Evonik Industries AG, Solvay S.A., DowDuPont Inc., BASF SE, Kerry Group plc, Agropur Cooperative, Univar Solutions Inc., Innospec Inc., Cargill, Incorporated, IMCD Group B.V., Kao Corporation, Huber Engineered Materials, PQ Corporation, Wacker Chemie AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Anti-Caking Agents Market Size is USD 1.1 Billion in 2023.

The Global Anti-Caking Agents Market is expected to grow at a CAGR of 5.7% (2024-2033).

Market.US has segmented the Global Anti-Caking Agents Market by geographic (North America, Europe, APAC, South America, and Middle East and Africa). By Type(Calcium Compounds, Sodium Compounds, Silicon Dioxide, Microcrystalline Cellulose, Others), By Source(Natural, Synthetic), By Application(Seasonings and Condiments, Bakery, Dairy, Soups and Sauces, Others)

PPG Industries, Inc., Evonik Industries AG, Solvay S.A., DowDuPont Inc., BASF SE, Kerry Group plc, Agropur Cooperative, Univar Solutions Inc., Innospec Inc., Cargill, Incorporated, IMCD Group B.V., Kao Corporation, Huber Engineered Materials, PQ Corporation, Wacker Chemie AG

The US, Canada, Mexico are leading key areas of operation for Anti-Caking Agents Market.