Quick Navigation

Report Overview

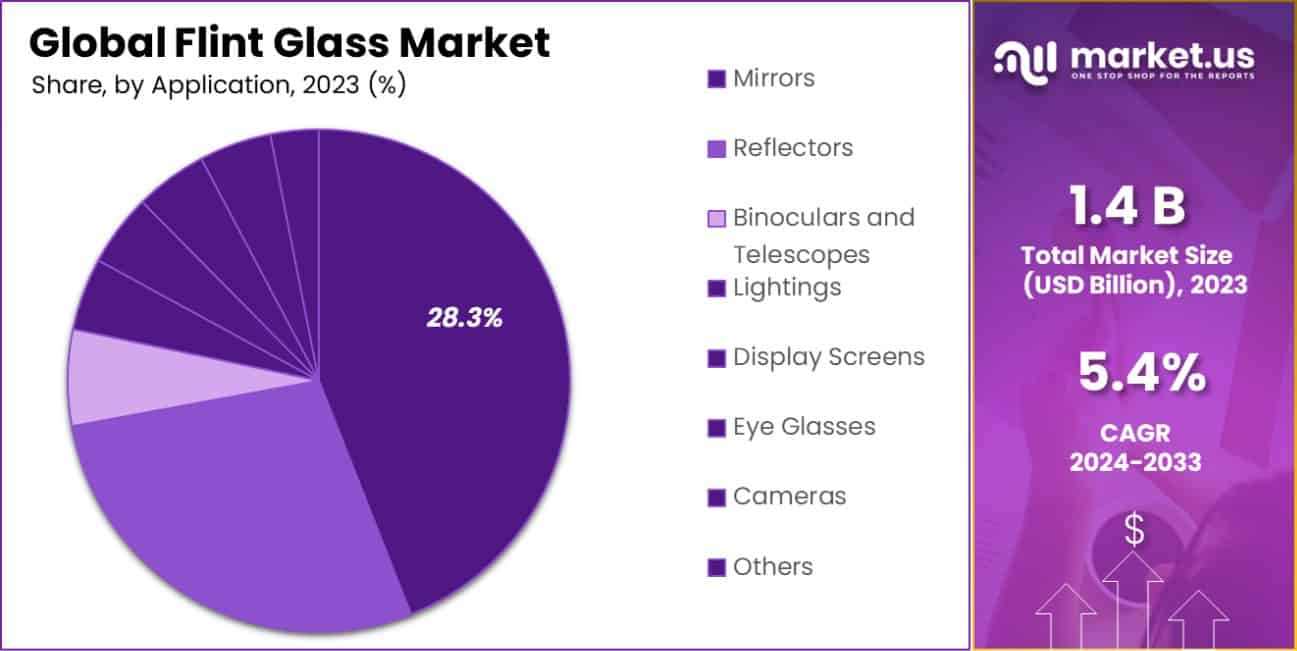

The Global Flint Glass Market size is expected to be worth around USD 2.4 Bn by 2033, from USD 1.4 Bn in 2023, growing at a CAGR of 5.4% during the forecast period from 2024 to 2033.

Flint glass is a type of optical glass characterized by its high refractive index and its ability to disperse light, which results in significant chromatic aberration. Traditionally made from an admixture of lead oxide, silica, and potash, flint glass is noted for its clarity and brilliance, making it popular for use in lenses, prisms, and decorative glassware.

The flint glass market caters primarily to sectors requiring high-quality optical components such as the automotive, photography, and scientific industries. This market is driven by the increasing demand for high-performance optical instruments and the growing use of decorative glass in architecture and interior design.

The growth of the flint glass market is propelled by advancements in optical technology and increasing applications in high-precision instruments. The automotive industry’s shift towards more sophisticated lighting and camera systems also significantly fuels market expansion.

The flint glass market is positioned for significant growth, driven by its indispensable role in high-quality optical applications across various industries. This market benefits notably from the evolution of optical technologies and the surging demand for sophisticated automotive and consumer electronics imaging systems.

The recent allocation of a $170 million federal funding package aimed at supporting communities around Flint, previously affected by lead contamination, underscores a broader commitment to revitalizing the area’s economic and industrial base, potentially benefiting local glass manufacturers.

Additionally, the infusion of $160 million by Flint Capital into early-stage startups signals a robust investment climate and a strategic push toward fostering innovation within key sectors such as technology and healthcare. These sectors rely heavily on advanced optical components, suggesting a direct impact on the demand for flint glass.

This convergence of favorable investment dynamics and technological advancements presents a ripe opportunity for market players to innovate and expand their footprint in the global market. Companies positioned to leverage these trends with sustainable production practices and advancements in glass composition are likely to capture significant market share and achieve substantial growth.

Demand in the flint glass market is bolstered by the needs of the consumer electronics sector, especially in cameras and optical devices, where superior light dispersion is crucial. Additionally, the luxury goods market contributes to sustained demand, particularly for decorative items and premium glassware.

Opportunities within the Flint glass market are abundant in the development of eco-friendly glass production techniques and in emerging markets where the adoption of advanced optical technologies is beginning to rise. Further, innovations in fiber optics and telecommunications present new avenues for application, broadening the market scope.

Key Takeaways

- The Global Flint Glass Market size is expected to be worth around USD 2.4 Bn by 2033, from USD 1.4 Bn in 2023, growing at a CAGR of 5.4% during the forecast period from 2024 to 2033.

- Clear Flint Glass dominates the market with a 56.4% share by product type.

- Machine-blown flint glass accounts for 44.5% of the market by manufacturing process.

- Mirrors are a significant application of flint glass, holding a 28.3% market share.

- In the end-use industry segment, Electronics & Electrical lead with a 34.4% share.

By Product Type Analysis

Clear flint glass dominates with a 56.4% market share.

In 2023, Clear Flint Glass held a dominant market position in the “By Product Type” segment of the Flint Glass Market, with a 56.4% share. This substantial market share underscores its widespread preference across various industries, particularly in the manufacturing of containers and beverage bottles, due to its purity and clarity.

Following Clear Flint Glass, Colored Flint Glass captured a 30.2% share, favored for its aesthetic appeal and functionality in decorative applications. Patterned Flint Glass accounted for the remaining 13.4% of the market, utilized primarily in architectural and interior design applications for its textured features that enhance visual interest and privacy.

The dominance of Clear Flint Glass can be attributed to its extensive application in both consumer goods and industrial products, where high visibility and chemical resistance are paramount. Meanwhile, the demand for Colored Flint Glass is driven by trends in personalized and premium packaging solutions, especially in cosmetics and luxury beverages, which leverage color to differentiate products on shelves.

Patterned Flint Glass, although a smaller segment, is experiencing growth due to increasing architectural trends that incorporate textured glass for aesthetic and functional benefits. This segment is expected to witness gradual growth as urbanization and interior refurbishment projects continue to rise.

By Manufacturing Process Analysis

Machine-blown flint glass holds 44.5% of the manufacturing market share.

In 2023, Machine-Blown held a dominant market position in the “By Manufacturing Process” segment of the Flint Glass Market, with a 44.5% share. This segment outpaced others due to its efficiency in mass production and consistency in product quality. Hand-blown glass followed with a 25.3% market share, appreciated for its artisanal quality and custom designs.

Press-molded glass accounts for 20.2% of the market, widely used for its ability to produce complex shapes at lower costs. Lastly, Centrifugal Casting made up 10% of the market, primarily used in specialized applications requiring large, circular flat glass pieces.

The preference for Machine-Blown Flint Glass is primarily driven by the large-scale industrial applications that demand high-volume, uniform glass products, such as bottles and jars for the food and beverage industry. The automation associated with machine-blown techniques significantly reduces production time and labor costs, making it a cost-effective option for manufacturers.

Meanwhile, the Hand-Blown segment continues to hold a substantial market share, supported by the luxury goods market where bespoke and aesthetically distinct products are highly valued. Press-Molded and Centrifugal Casting techniques remain integral for specific industrial and decorative applications, where their unique manufacturing advantages are essential.

By Application Analysis

Mirrors are a significant application, constituting 28.3% of the market.

In 2023, Mirrors held a dominant market position in the “By Application” segment of the Flint Glass Market, with a 28.3% share. Reflectors followed with a 22.1% share, while Binoculars and Telescopes captured 14.5%. Lightings accounted for 12.6%, Display Screens garnered 10.2%, Eyeglasses achieved 7.8%, and Cameras rounded out the segment with a 4.5% share.

The strong position of Mirrors in the market can be attributed to their critical role in various applications, from automotive to decorative and architectural uses. The high reflectivity and clarity of flint glass make it ideal for producing high-quality mirrors.

Reflectors also command a significant market portion, especially in automotive and lighting applications, where precise light direction is necessary. The usage of flint glass in Binoculars and Telescopes is driven by its optical properties, which enhance clarity and magnification.

As urbanization and technology integration advance, the demand for flint glass in Lighting and Display Screens continues to grow, driven by both aesthetic qualities and functionality. Eye Glasses and Cameras represent smaller but vital niches that leverage the superior optical characteristics of flint glass to improve visual accuracy in eyewear and photography.

This diversified application range underscores flint glass’s versatility and enduring demand across multiple sectors.

By End-Use Industry Analysis

Electronics & electrical industries utilize 34.4% of flint glass produced.

In 2023, Electronics & Electrical held a dominant market position in the “By End-Use Industry” segment of the Flint Glass Market, with a 34.4% share. Medical & Healthcare followed with a 24.6% share, while Solar Power captured 18.5%. Automotive and Consumer Goods rounded out the market with 12.7% and 9.8% shares, respectively.

The preeminence of the Electronics & Electrical sector is primarily due to the extensive use of flint glass in a variety of applications, including display panels, optical components, and insulators, where high optical clarity and thermal stability are paramount. The sector’s dominance is bolstered by rapid advancements in technology and increasing demand for high-performance materials in consumer electronics.

Medical & Healthcare is another significant segment, utilizing flint glass for its superior chemical resistance and durability, essential for laboratory equipment, medical devices, and pharmaceutical containers. The Solar Power industry’s reliance on flint glass, particularly for photovoltaic panels, underscores its critical role in enhancing energy efficiency and durability against environmental factors.

Automotive and Consumer Goods industries also leverage flint glass for its aesthetic and functional properties, using it in vehicle lighting systems, mirrors, and various household items. This widespread application across diverse industries highlights flint glass’s versatile properties and its integral role in modern manufacturing and technology sectors.

Key Market Segments

By Product Type

- Clear Flint Glass

- Colored Flint Glass

- Patterned Flint Glass

By Manufacturing Process

- Hand-Blown

- Machine-Blown

- Press-Molded

- Centrifugal Casting

By Application

- Mirrors

- Reflectors

- Binoculars and Telescopes

- Lightings

- Display Screens

- Eye Glasses

- Cameras

- Others

By End-Use Industry

- Electronics & Electronics

- Medical & Healthcare

- Solar Power

- Automotive

- Consumer Goods

- Others

Driving Factors

Increasing Demand in Automotive and Architectural Industries

The Flint Glass Market is significantly driven by its expanding use in the automotive and architectural sectors. Automotive manufacturers utilize flint glass for vehicle mirrors and lighting systems due to its clarity and durability.

In architecture, flint glass is prized for decorative elements and structural components, enhancing both the aesthetics and functionality of buildings. This increasing demand from both sectors supports the market’s growth as they continue to innovate and expand.

Technological Advancements in Glass Manufacturing

Technological improvements in glass manufacturing processes have notably propelled the Flint Glass Market. Modern techniques enable the production of higher-quality flint glass with enhanced properties such as increased strength and improved optical clarity.

These advancements reduce production costs and time, making flint glass more appealing for manufacturers and consumers alike, thereby boosting market growth.

Rising Popularity of High-Performance Optics

The demand for high-performance optical components in sectors such as electronics, telecommunications, and healthcare is another key driver for the Flint Glass Market.

Flint glass’s superior optical properties, including high refractive index and low dispersion, make it ideal for applications requiring precise light transmission and clarity. This is increasingly important in products like cameras, microscopes, and various scientific instruments.

Restraining Factors

High Production Costs Limit Market Expansion

Flint glass manufacturing is associated with high production costs, primarily due to the intricate processes and quality materials required. These elevated costs can be a significant barrier, particularly for smaller manufacturers and in markets where cost efficiency is a priority.

The expense involved in producing high-quality flint glass can restrict its use to high-margin applications, potentially limiting broader market penetration and growth.

Environmental Regulations Impact Production Processes

Strict environmental regulations related to glass manufacturing impact the Flint Glass Market by imposing limits on emissions and waste. Compliance with these regulations can lead to increased operational costs and necessitate investment in cleaner, but often more expensive, technologies.

This factor can restrain market growth as manufacturers may face challenges in maintaining profitability while adhering to environmental standards.

Availability of Substitute Materials

The availability of alternative materials such as polycarbonate and acrylic, which can offer similar transparency and durability at a lower cost, poses a significant challenge to the Flint Glass Market.

These materials are increasingly preferred in various applications due to their lighter weight and greater shatter resistance. The competition from these substitutes can restrain the demand for flint glass, particularly in cost-sensitive and high-volume markets.

Growth Opportunity

Expansion into Emerging Markets Boosts Flint Glass Sales

Emerging markets present significant growth opportunities for the Flint Glass Market, driven by rapid industrialization and increasing investments in infrastructure. As these regions develop, there is a growing demand for high-quality glass in the automotive, construction, and consumer goods industries.

Capitalizing on this demand by expanding into these markets could substantially increase sales volumes and market presence for flint glass manufacturers, tapping into new customer bases that seek advanced materials for development and modernization projects.

Advancements in Energy-Efficient and Sustainable Glass Products

As global focus shifts towards sustainability, there is a rising opportunity for the Flint Glass Market to innovate with energy-efficient and environmentally friendly glass products. Developing flint glass that offers better insulation properties or is produced through greener processes can attract consumers and industries looking to reduce environmental impact.

This shift not only aligns with regulatory trends but also opens up new market segments focused on green building materials and sustainable manufacturing practices.

Integration with High-Tech Industries for Specialty Applications

The high optical quality of flint glass makes it ideal for specialty applications in high-tech industries such as aerospace, electronics, and scientific research. There is a growing opportunity to collaborate with these industries to develop customized glass solutions that meet specific technical requirements.

By enhancing product offerings and forming strategic partnerships, flint glass manufacturers can tap into high-value markets where precision and performance are critically important, potentially leading to higher profit margins and strengthened market position.

Latest Trends

Growing Use of Flint Glass in Luxury Packaging

The Flint Glass Market is witnessing a trend towards increased use of luxury packaging solutions. As brands strive to differentiate their products, high-quality flint glass is becoming a preferred material for packaging premium beverages, perfumes, and cosmetics.

This glass enhances aesthetic appeal and conveys a sense of quality and luxury to consumers. Companies are leveraging this trend to boost brand image and customer attraction, driving a significant uptick in demand for flint glass in the luxury segment.

Rise of Eco-Friendly Glass Production Techniques

There is a noticeable trend towards adopting eco-friendly production methods in the Flint Glass Market. Manufacturers are increasingly prioritizing sustainability in their production processes by reducing waste, recycling materials, and lowering energy consumption.

This shift not only helps companies comply with stringent environmental regulations but also appeals to a growing consumer base that values sustainability. The move towards greener production methods is reshaping industry standards and encouraging innovation in environmentally responsible glass manufacturing.

Integration of Flint Glass in Smart Home Devices

Integration of flint glass into smart home devices represents a prominent trend within the market. Flint glass’s optical clarity and durability make it ideal for use in smart device interfaces, including touchscreens and display panels in home automation systems.

As smart homes gain popularity, the demand for high-quality, durable glass that can withstand regular interaction while maintaining functionality is increasing. This trend offers significant growth potential as technology companies seek reliable suppliers of high-quality glass for their innovative products.

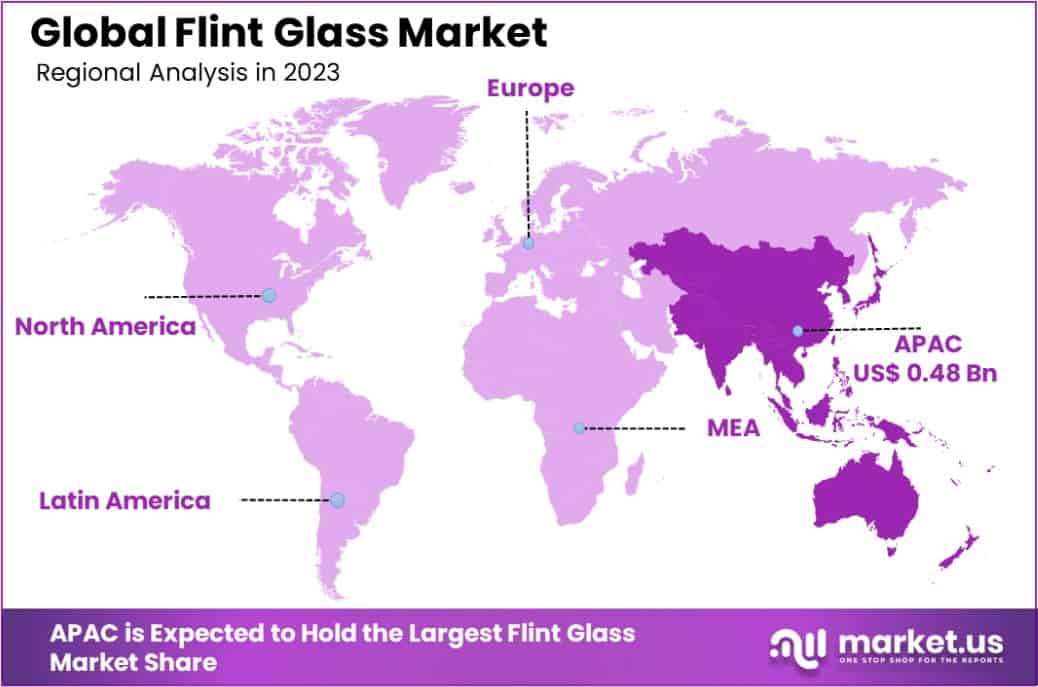

Regional Analysis

The Flint Glass Market exhibits diverse dynamics across global regions, reflecting varying levels of industrial development and consumer preferences. In 2023, Asia Pacific emerged as the dominating region, accounting for 34.6% of the global market with a value of USD 0.48 billion.

This dominance is fueled by rapid industrialization and urbanization in major economies such as China and India, coupled with extensive investments in construction and automotive sectors that demand high-quality flint glass.

North America also represents a significant share, driven by technological advancements and high consumer demand for premium glass products in both automotive and architectural applications. Europe follows closely, with a strong emphasis on sustainability and high-performance materials, leveraging advanced manufacturing techniques to produce eco-friendly flint glass.

The Middle East & Africa, though smaller in comparison, is experiencing growth due to increasing infrastructural developments and investments in luxury real estate, which utilize flint glass for aesthetic enhancements. Latin America, with its rising focus on urban modernization and renewable energy, is also witnessing a gradual increase in demand for flint glass, particularly in solar applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Flint Glass Market was notably shaped by several key players, each contributing unique strengths and innovations. Corning stood out for its technological leadership, particularly in developing high-performance glass for the tech and automotive industries. The company’s continuous investment in R&D has allowed it to maintain a competitive edge in high-quality glass solutions.

Schott AG, another significant player, has consistently expanded its market presence through strategic partnerships and global expansion. Its focus on durable and specialty glass products has made it a preferred supplier for both medical and optical applications, reflecting its robust positioning in European and global markets.

Hoya Corporation has leveraged its expertise in optical technologies to penetrate niche markets, including healthcare and photography. Its commitment to high precision and quality standards has fostered strong brand loyalty among customers, particularly in Asia Pacific, contributing significantly to the region’s dominance in the Flint Glass Market.

These companies, along with others like Nikon Corporation and Owens-Illinois, which focus on specialized and high-quality glass manufacturing, have driven the industry’s growth by meeting the increasing demands for flint glass across diverse applications, from consumer electronics to industrial and scientific use.

Top Key Players in the Market

- Ardagh Group

- CDGM glass company

- Corning

- Crytran Ltd.

- Dartington Crystal

- Edmund Optics

- Hoya Corporation

- Nikon Corporation

- Nippon Electric Glass

- OAG Werk Optik

- Ohara Corporation

- OwensIllinois

- Precision Optical Inc.

- Schott AG

- Schott Glaswerke AG

- Stuart Crystal

- Verreries de SaintGobain

Recent Developments

- In 2024, Ardagh launched its NextGen Furnace technology at its AGP-Obernkirchen facility in Germany, achieving a remarkable 64% reduction in CO2 emissions from this new hybrid electric furnace. This advancement demonstrates Ardagh’s commitment to sustainable production practices and positions the company as a leader in environmentally responsible manufacturing within the glass industry.

- In 2024, The enhancement of Nikon’s photomask substrates for FPDs. These substrates are essential for producing high-resolution displays and are made with precision polishing and deposition technologies that reflect Nikon’s commitment to quality and innovation in the Flint Glass sector

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.4 Billion |

| Forecast Revenue (2033) | USD 2.4 Billion |

| CAGR (2024-2033) | 5.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Clear Flint Glass, Colored Flint Glass, Patterned Flint Glass), By Manufacturing Process (Hand-Blown, Machine-Blown, Press-Molded, Centrifugal Casting), By Application (Mirrors, Reflectors, Binoculars and Telescopes, Lightings, Display Screens, Eye Glasses, Cameras, Others), By End-Use Industry (Electronics & Electronics, Medical & Healthcare, Solar Power, Automotive, Consumer Goods, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ardagh Group, CDGM glass company, Corning, Crytran Ltd., Dartington Crystal, Edmund Optics, Hoya Corporation, Nikon Corporation, Nippon Electric Glass, OAG Werk Optik, Ohara Corporation, OwensIllinois, Precision Optical Inc., Schott AG, Schott Glaswerke AG, Stuart Crystal, Verreries de SaintGobain |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |