Quick Navigation

Report Overview

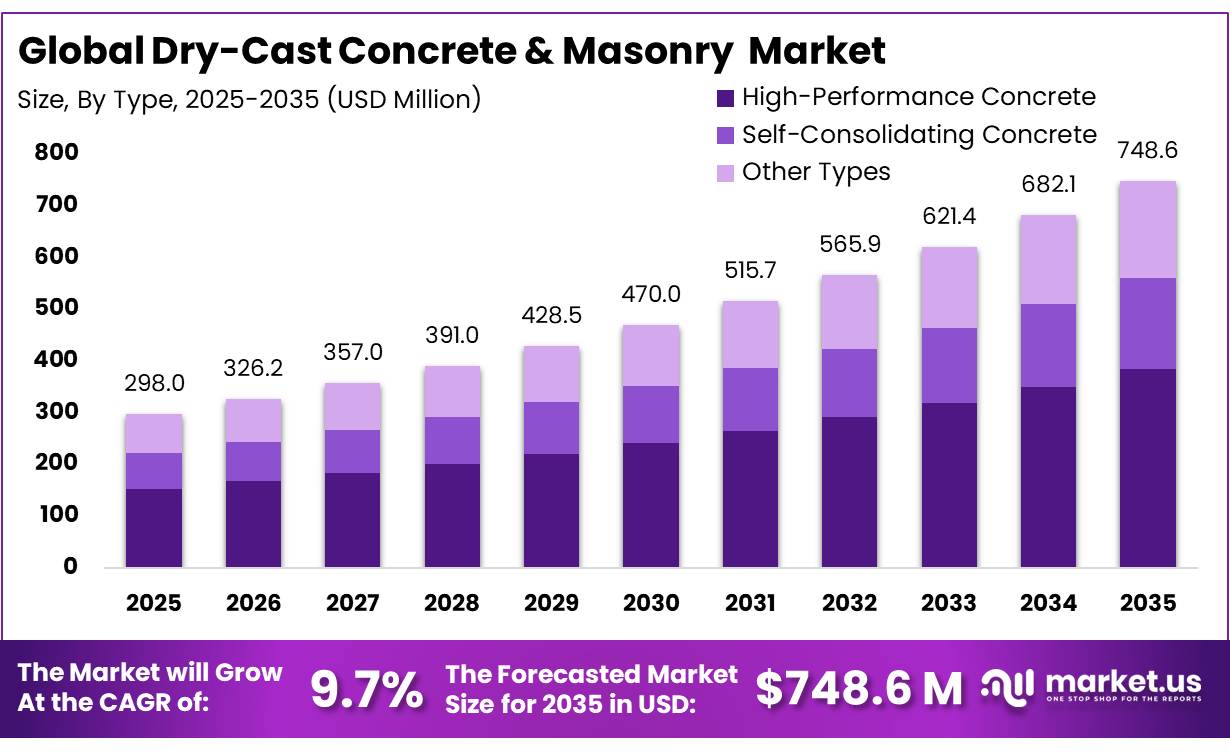

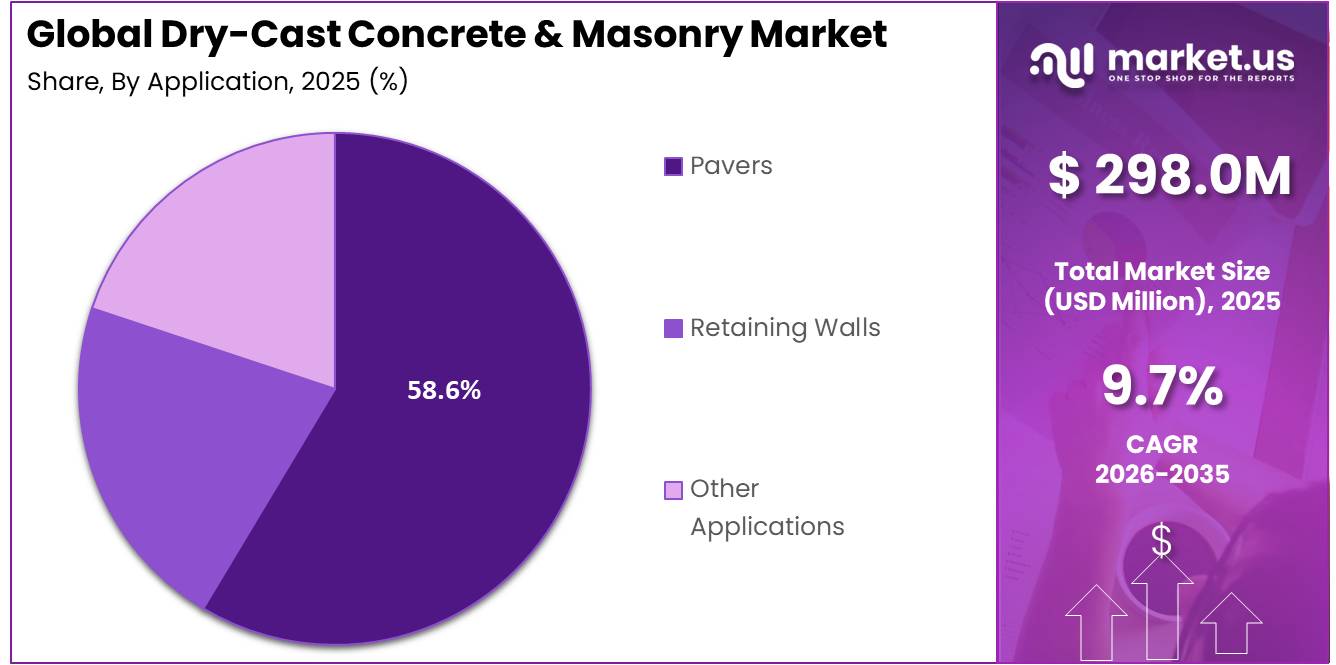

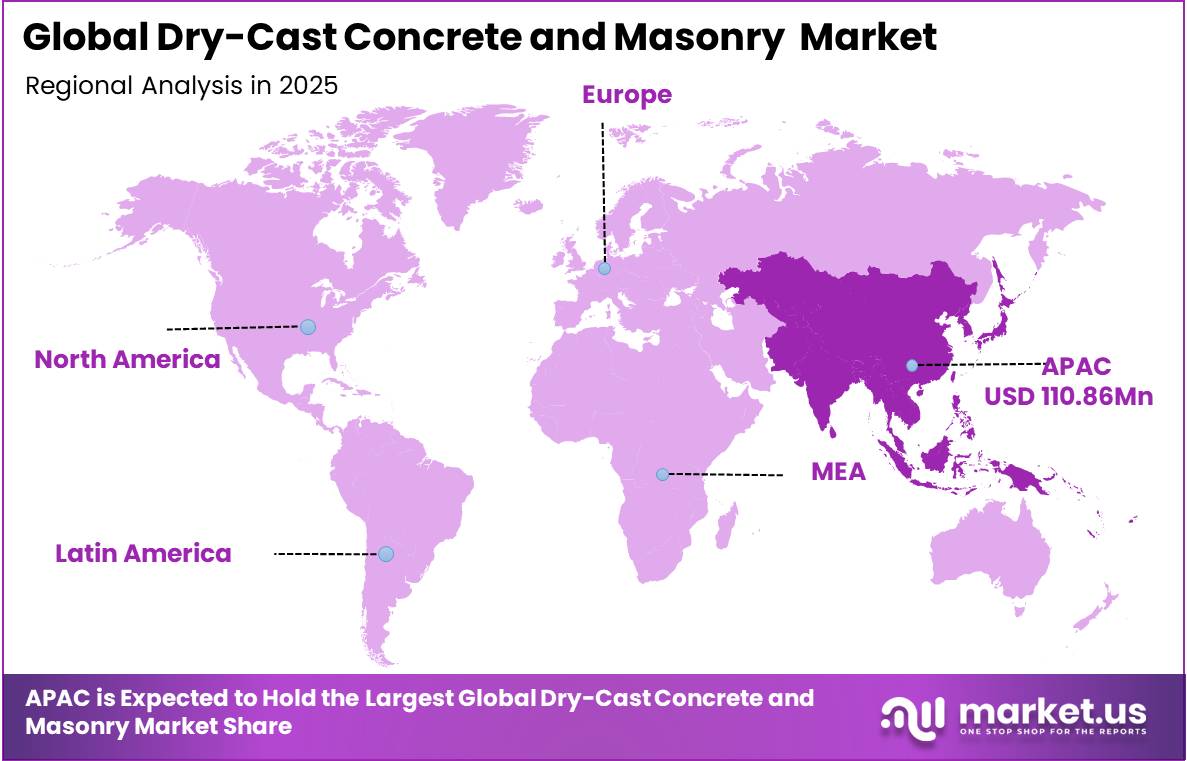

The Global Dry-Cast Concrete and Masonry Market size is expected to be worth around USD 748.6 Million by 2035, from USD 298.0 Million in 2025, growing at a CAGR of 9.7% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 37.2% share, holding USD 110.8 Million revenue.

Dry-cast concrete and masonry covers factory-made concrete masonry units, paving blocks, slabs, kerbs, pipes and segmental retaining-wall products manufactured from a stiff, zero-slump mixture.

- The industrial base is linked to housing, commercial building, transport, drainage, and public infrastructure spending. In April 2026, total U.S. construction spending reached a seasonally adjusted annual rate of USD 2.172 trillion, including USD 532.7 billion in public construction and USD 149.6 billion in highway construction. These expenditure levels support demand for blocks, pavers, pipes, and culverts because contractors require standardized units that can be installed rapidly with limited on-site forming.

Key Takeaways

- The global Dry-Cast Concrete Masonry Market was valued at US$ 298.0 million in 2025 and is projected to reach US$ 748.6 million by 2035, expanding at a CAGR of 9.7% during the forecast period.

- By type, High-Performance Concrete dominated the market with a 51.4% share in 2025.

- By application, Pavers held the largest market share of 58.6% Share.

- By end-use, Residential Buildings emerged as the leading segment, contributing 47.3% of total market revenue.

- By product type, Concrete Blocks led the market with a 38.2% share in 2025

- By construction method, Precast Dry-Cast Systems accounted for 59.4% of the market.

- Regionally, Asia-Pacific dominated the global market with a 37.2% share in 2025 and is expected to register the fastest growth through 2035.

Cement availability and pricing shape production economics. The U.S. Geological Survey estimated that the United States produced 82 million metric tons of portland and blended cement and 2.1 million metric tons of masonry cement in 2025. Cement shipments totaled about 100 million metric tons and were valued at approximately USD 17 billion, with 11% of sales directed to concrete-product manufacturers.

Infrastructure programs are a major growth driver. Under the U.S. Infrastructure Investment and Jobs Act, the National Highway Performance Program received USD 148 billion, the Bridge Formula Program USD 26.675 billion, and the National Culvert Removal, Replacement and Restoration Grant Program USD 1 billion. These allocations create opportunities for dry-cast drainage systems, precast culverts, retaining walls, and paving products used in roads, flood control, bridges, and municipal projects.

Urbanization strengthens the long-term outlook. World Bank data show that 57.56% of the global population lived in urban areas in 2024. City expansion increases the need for affordable walls, pedestrian surfaces, stormwater channels, utility structures, and durable public spaces. Dry-cast production is well positioned because it combines repeatable factory output, short cycles, local aggregate use, and modular installation.

Type analysis

High-Performance Concrete Dominates with a 51.4% Share Due to Superior Strength and Durability

In 2025, High-Performance Concrete held a dominant market position, capturing more than a 51.4% share. Its leadership was supported by its high compressive strength, improved durability, and strong resistance to harsh weather and heavy loads. The material is widely used in dry-cast concrete products, including masonry blocks, paving units, pipes, and structural components. Manufacturers prefer high-performance concrete because it supports faster production, reduces maintenance needs, and extends the service life of finished products.

Application Analysis

Pavers Dominate with a 58.6% Share Due to Strong Infrastructure and Landscaping Demand

In 2025, Pavers held a dominant market position, capturing more than a 58.6% share. The segment’s leadership was supported by the widespread use of dry-cast pavers in sidewalks, driveways, public spaces, parking areas, and commercial landscaping projects. Builders and infrastructure developers prefer pavers because they offer high load-bearing strength, simple installation, and easy replacement of damaged units. Their availability in different shapes, textures, and designs also supports their use in decorative outdoor spaces.

Product Type Analysis

Leading Role of Concrete Blocks and Strong Growth in Paving Stones

Concrete blocks dominate the global dry-cast concrete masonry market with a 38.2% share, driven by their widespread use in structural applications such as walls, foundations, and load-bearing construction across residential, commercial, and industrial projects. Their strength, durability, fire resistance, and cost efficiency make them the most preferred product type in large-scale construction activities. Alongside concrete blocks, pipes & culverts also hold a significant share of 20.0%, supported by their essential role in drainage systems, sewage networks, and water management infrastructure in rapidly urbanizing regions.

By Construction Method Analysis

Dominance of Precast Dry-Cast Systems and Shift Toward Modern Manufacturing

Precast dry-cast systems dominate the global dry-cast concrete masonry market with a 59.4% share, owing to their high efficiency, faster production cycles, and superior dimensional accuracy. These systems enable large-scale manufacturing of concrete blocks, pavers, and other masonry products with consistent quality and reduced curing time. Their ability to support automation, minimize labor dependency, and improve overall productivity makes them the preferred choice in modern construction and precast manufacturing facilities.

End Use Analysis

Strong Residential Dominance with Accelerating Growth in Housing Demand

Residential buildings dominate the global dry-cast concrete masonry market with a 47.3% share, driven by extensive usage in housing construction, including walls, foundations, and boundary structures. The segment benefits from rapid urbanization, population growth, and increasing demand for affordable housing, especially in developing economies. Dry-cast products such as concrete blocks and paving units are widely preferred in residential projects due to their cost efficiency, durability, and ease of installation, making this segment the largest contributor to overall market demand.

Key Market Segments

By Type

- High-Performance Concrete

- Self-Consolidating Concrete

- Other Types

By Application

- Pavers

- Retaining Walls

- Other Applications

By End-Use

- Residential Buildings

- Commercial Buildings

- Industrial Buildings

By Product Type

- Concrete Blocks

- Pipes & Culverts

- Paving Stones

- Retaining Wall Units

- Masonry Units & Others

By Construction Method

- Precast Dry-Cast Systems

- Conventional Masonry

- Systems

Drivers

Public infrastructure pipeline supports masonry demand

In the U.S., public transportation and water infrastructure spending reached $625.8 billion in 2023, with states and localities accounting for 79% or $494.2 billion, while ASCE’s 2025 infrastructure report card estimated $9.1 trillion of investment needs across 18 categories, sustaining a multi-year project funnel that continues into 2026 procurement cycles.

For dry-cast producers, this driver improves plant utilization, supports higher fixed-cost absorption, and shifts revenue mix toward repeat institutional contracts with better volume visibility than fragmented retail construction, justifying an estimated +2.3 percentage-point uplift to CAGR over the medium term.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public infrastructure pipeline supports masonry demand | +2.3% | North America core, India, GCC, selected EU public works | Medium term (2-4 years) |

| Resilience-led codes favor impact-resistant CMU systems | +1.8% | U.S. tornado/hurricane belts, Caribbean, Gulf, disaster-prone APAC | Short term (≤ 2 years) |

| Low-carbon procurement rewards EPD-ready masonry mixes | +1.5% | U.S. federal/state projects, Canada, EU regulatory hubs | Medium term (2-4 years) |

| Fast-cycle dry-cast automation improves unit economics | +1.7% | North America, Europe, India, Middle East industrial clusters | Short term (≤ 2 years) |

| Affordable housing and urban buildout lift block adoption | +2.0% | India, Southeast Asia, Africa urban corridors, LATAM | Medium term (2-4 years) |

| Thermal mass and fire performance boost specification | +1.2% | North America, Southern Europe, Middle East, Australia | Long term (≥ 4 years) |

Restraints

Freight and trade volatility

Freight and trade volatility constrains market expansion because dry-cast masonry margins are too thin to absorb large swings in imported cementitious inputs, pallets, machinery parts, steel reinforcement, and cross-border finished-unit movement. The 2026 Red Sea disruption has added about 8–12 days to rerouted voyages and pushed some full-container rates up 30–60%, while U.S. trade policy raised tariffs on imported steel and aluminum products and derivatives from 25% to 50% effective 4 June 2025, adding broader cost uncertainty to construction-material supply chains.

Even though masonry units are often made locally, the sector still relies on internationally exposed equipment, admixtures, molds, steel accessories, and occasionally imported cement or supplementary materials, so lead-time volatility raises spare-parts inventories, increases working capital, and can postpone plant upgrades or new line commissioning; this supports a -1.1 percentage-point CAGR deduction, particularly in import-reliant or export-oriented markets.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cement and energy inflation | -2.2% | North America core, EU, India, MENA | Short term (≤ 2 years) |

| Masonry labor scarcity | -1.8% | U.S., Canada, UK, GCC urban builds | Medium term (2-4 years) |

| Housing cycle slowdown | -1.6% | North America core, Western Europe, China spill-over | Short term (≤ 2 years) |

| Carbon compliance cost burden | -1.3% | EU core, U.S. public projects, export-to-EU suppliers | Medium term (2-4 years) |

| Freight and trade volatility | -1.1% | EU importers, MENA, APAC shipping corridors | Short term (≤ 2 years) |

| Substitute walling competition | -1.4% | India, Southeast Asia, Africa urban corridors | Long term (≥ 4 years) |

Opportunity

Carbon-labeled premium blocks

Governments and procurement alliances are now building the framework: the U.S. federal system has directed $4.15 billion toward lower embodied-carbon construction materials, Ireland’s public procurement work is explicitly pushing low-carbon concrete adoption, and the Industrial Deep Decarbonisation Initiative’s 2024 pledge architecture commits buyers to timebound procurement of low- and near-zero-emission steel, cement, and concrete using Type III EPDs and whole-project LCAs.

The commercial upside lies in repricing blocks from a pure commodity into a specification-protected line item where certified “low-carbon CMU” can win tenders, reduce bid attrition, and support 300 to 700 basis points of margin uplift while improving plant utilization through access to public and ESG-sensitive private projects; because this premium segment is still underpenetrated rather than fully reflected in baseline demand, it can add about +2.1 percentage points to CAGR through 2030 if producers move early on mix optimization, data infrastructure, and third-party verification.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Carbon-labeled premium blocks | +2.1% | U.S. public projects, Canada, EU regulatory hubs | Medium term (2-4 years) |

| Modular wall system expansion | +1.9% | North America, Europe, India, GCC | Medium term (2-4 years) |

| Resilience shelter product lines | +1.7% | U.S. storm belts, Caribbean, South Asia, Africa | Short term (≤ 2 years) |

| Energy-retrofit masonry infill | +1.4% | EU, North America, Australia | Long term (≥ 4 years) |

| Digital spec-to-site platforms | +1.3% | U.S., UK, EU, developed APAC | Short term (≤ 2 years) |

| Regional roll-up acquisitions | +1.8% | U.S., India, GCC, Southeast Asia | Long term (≥ 4 years) |

Challenges Analysis

Skilled mason attrition

The most persistent operational challenge is the erosion of skilled masonry labor, because dry-cast concrete units can be manufactured efficiently at plant level but value capture still depends on field installation quality, reinforcement detailing, mortar discipline, and wall-alignment productivity that are difficult to automate quickly. U.S. construction labor estimates for 2026 range from a need for 349,000 net new workers to roughly 499,000 additional workers depending on methodology, while workforce studies indicate that about 41% of the existing construction labor pool may retire by 2031, implying a severe experience drain rather than just a temporary hiring gap.

For masonry specifically, this creates recurring friction in crew formation, supervision ratios, rework levels, and project sequencing, often stretching wall-installation schedules by 5% to 15%, increasing subcontractor pricing by high single digits, and forcing producers to support contractors with training, layout assistance, and simplified system design; as a result, the market loses an estimated -1.3 percentage points of attainable CAGR until apprenticeship pipelines, mechanized installation aids, and labor-productivity redesign become more widespread.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled mason attrition | -1.3% | North America core, UK, GCC, Australia | Long term (≥ 4 years) |

| Logistics route instability | -1.0% | EU import corridors, MENA, APAC trade lanes | Medium term (2-4 years) |

| Carbon data readiness | -0.9% | U.S. public projects, EU hubs, Canada | Medium term (2-4 years) |

| Mix consistency pressure | -0.8% | Global cement/aggregate sourcing markets | Medium term (2-4 years) |

| Distributed plant inefficiency | -0.7% | India, U.S., Southeast Asia, Africa | Long term (≥ 4 years) |

| Specifier education gap | -0.6% | North America, EU, developed APAC | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade Disruptions and Shifting Global Supply Chains in Dry-Cast Concrete Market

Geopolitical tensions are influencing the dry-cast concrete and masonry market mainly through raw material availability, energy costs, and construction supply chains. Dry-cast products depend on cement, clinker, aggregates, steel reinforcement, chemical admixtures, fuel, and transportation networks. Any disruption in these inputs can increase production costs for concrete blocks, pavers, pipes, precast units, and masonry products.

The Russia-Ukraine war added pressure to the European construction materials sector by increasing energy costs and disrupting steel and building material supply chains. Since cement production requires energy-intensive kiln operations, higher fuel and electricity prices can directly affect the cost structure of dry-cast concrete manufacturers. Trade barriers, tariff changes, and supply chain diversification are also encouraging companies to reduce dependence on imported inputs and strengthen regional sourcing.

At the same time, several governments in the Middle East, South Asia, and other developing regions are investing in domestic infrastructure and local precast manufacturing capacity. This trend is creating new regional demand for dry-cast concrete and masonry products while reducing reliance on imported construction materials. As a result, geopolitical uncertainty is pushing the market toward more localized production, diversified sourcing, and stronger control over raw material supply chains.

Regional Analysis

Pacific Dominance with Strong Growth Across Developed Regions

In 2025, the Asia-Pacific region dominated the global dry-cast concrete masonry market with a 37.2% share, driven by rapid urbanization, large-scale infrastructure development, and strong construction activity across emerging economies. Countries in the region are witnessing significant investments in residential housing, transportation networks, and smart city projects, which is fueling strong demand for dry-cast concrete and masonry products.

Meanwhile, North America is projected to grow at a 25.0% growth rate during the forecast period, supported by a well-established and technologically advanced construction industry. Continuous investments in residential, commercial, and industrial infrastructure are sustaining steady demand for dry-cast products in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The dry-cast concrete and masonry market is fairly concentrated, with a few strong companies shaping most of the global supply. Well-known players such as Besser Company, Hess Group, CPI Concrete Products Inc., Wells Concrete, and Forterra Inc. play a major role in both equipment and precast product manufacturing. These companies stay ahead by investing in automation, better machine designs, and more efficient production systems.

In simple terms, a few big names dominate developed markets like North America and Europe, while smaller and regional manufacturers are quickly growing in Asia-Pacific due to cheaper production and rising construction demand. The competition is mainly about making stronger, cheaper, and more sustainable blocks and pavers, as infrastructure projects continue to expand worldwide.

The Major Players in The Industry

- CRH plc

- Basalite Building Products LLC

- Unilock

- Mutual Materials Co.

- Con Cast Pipe Inc.

- E.L. Paving Products

- Sika AG

- Wieser Concrete

- Rochester Cement Products, Inc.

- Solidia Technologies

- Other Key Players

Key Development

In June 2026, CRH signed an agreement to acquire 100% of Arcosa for USD 8.5 billion, including a construction-material network with 109 quarries and yards. These moves improve CRH’s access to raw materials, expand production reach, and support future masonry and concrete-product growth.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$298.0 Mn |

| Forecast Revenue (2035) | US$748.6 Mn |

| CAGR (2026-2035) | 9.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (High-Performance Concrete, Self-Consolidating Concrete, and Other Types), By Application (Pavers, Retaining Walls, and Other Applications), By End-Use (Residential Buildings, Commercial Buildings, and Industrial Buildings), By Product Type (Concrete Blocks, Pipes & Culverts, Paving Stones, Retaining Wall Units, and Masonry Units & Others), By Construction Method (Precast Dry-Cast Systems and Conventional Masonry Systems) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | CRH plc, Basalite Building Products LLC, Unilock, Mutual Materials Co., Con Cast Pipe Inc., E.L. Paving Products, Sika AG, Wieser Concrete, Rochester Cement Products, Inc., Solidia Technologies, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |