Quick Navigation

Report Overview

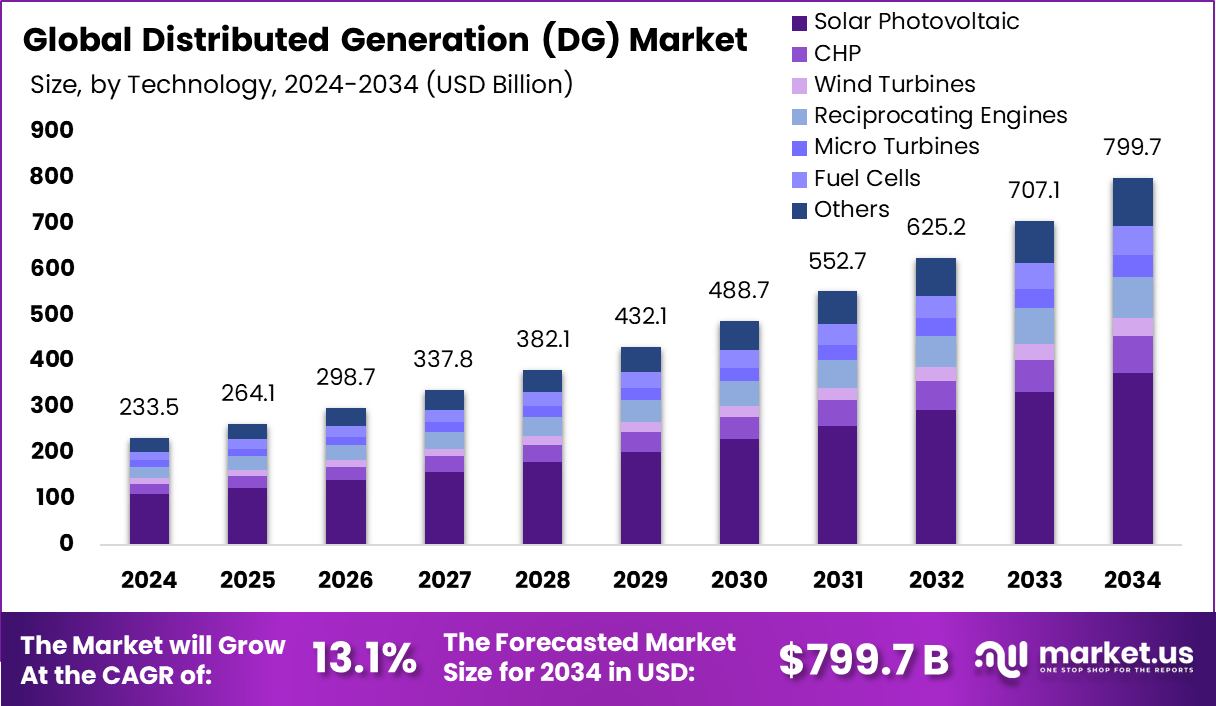

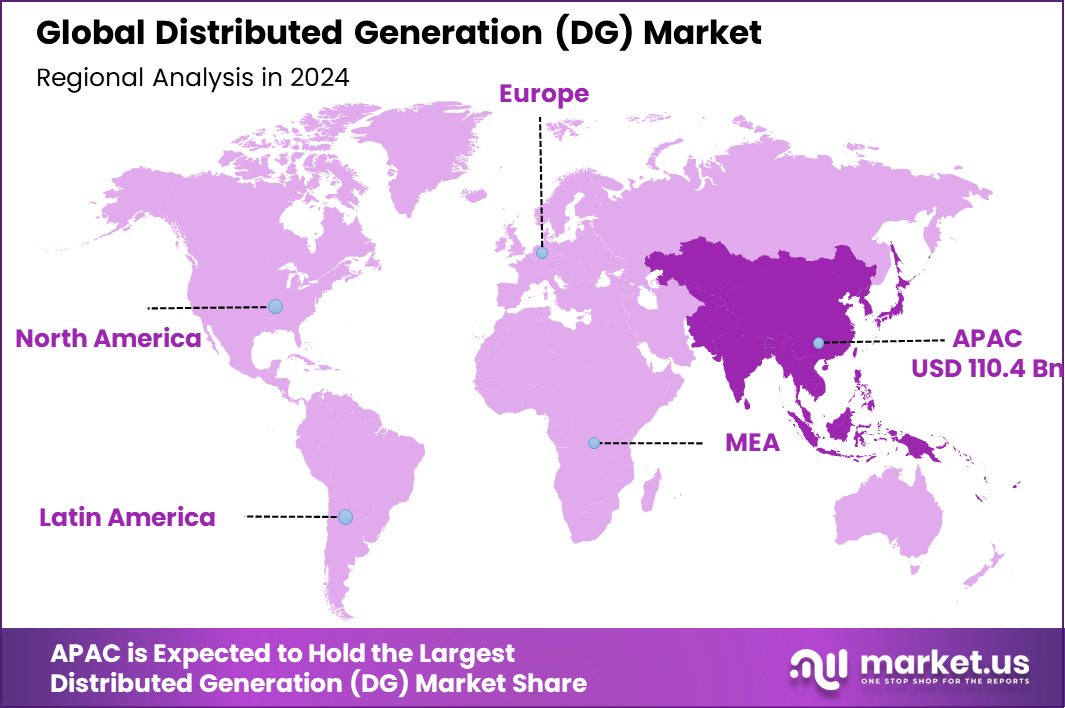

Global Distributed Generation (DG) Market is expected to be worth around USD 799.7 billion by 2034, up from USD 233.5 billion in 2024, and grow at a CAGR of 13.1% from 2025 to 2034. Asia-Pacific dominates the DG Market, holding a 47.30% share, valued at USD 110.4 billion

Distributed Generation (DG) refers to a variety of technologies that generate electricity at or near where it will be used, such as solar panels, wind turbines, and combined heat and power systems. These systems are often smaller than traditional power plants and provide an alternative to or an enhancement of the traditional electric power system. They offer benefits such as increased energy efficiency, reduced transmission losses, and enhanced reliability.

The Distributed Generation (DG) market is expanding as more individuals and businesses look to reduce energy costs and improve energy security. This market encompasses the sales, installation, and maintenance of small-scale generation units that operate independently or in conjunction with the local utility grid.

One significant growth factor for the DG market is the increasing cost of traditional energy sources, which drives the demand for more cost-effective and sustainable alternatives. Small-scale renewable installations, particularly solar and wind, are becoming more affordable and accessible, encouraging adoption among residential and commercial users.

Rising awareness about environmental issues and the push for green energy solutions also boost demand in the DG market. As people and policymakers alike seek to reduce carbon footprints and mitigate climate change, the integration of renewable energy sources into the grid continues to gain traction.

Opportunities in the DG market are vast due to technological advancements and regulatory incentives. Innovations in energy storage, smart grid technology, and energy management systems are making DG installations more efficient and reliable. Additionally, many governments worldwide are offering financial incentives for renewable energy adoption, further stimulating market growth.

Key Takeaways

- Global Distributed Generation (DG) Market is expected to be worth around USD 799.7 billion by 2034, up from USD 233.5 billion in 2024, and grow at a CAGR of 13.1% from 2025 to 2034.

- Solar Photovoltaic technology holds a significant 47.30% share in the Distributed Generation (DG) market.

- In power ratings, the 5 kW – 250 kW range accounts for 37.30% of the DG market.

- The on-grid application dominates the DG market, with a substantial 74.30% market share.

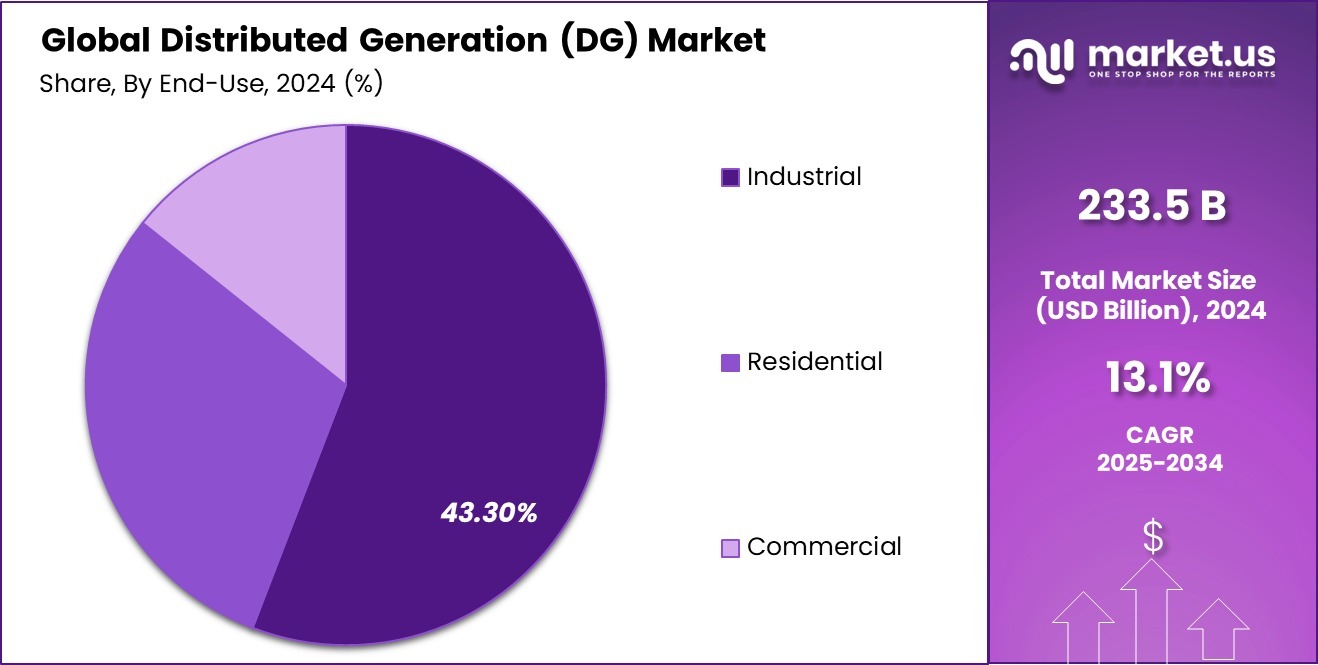

- Industrial end-users represent 43.30% of the DG market, highlighting its importance in this sector.

- Robust growth in Asia-Pacific’s 47.30% DG sector is driven by strong renewable energy adoption and policies.

By Technology Analysis

Solar photovoltaic technology dominates the DG market with a 47.30% share.

In 2024, Solar Photovoltaic held a dominant market position in the By Technology segment of the Distributed Generation (DG) Market, capturing a 47.30% share. This significant market share reflects the growing preference for solar energy solutions in both residential and commercial sectors due to their cost-effectiveness and sustainability. The appeal of solar photovoltaic systems has been enhanced by their decreasing installation costs and the availability of supportive regulatory frameworks across various regions.

As businesses and homeowners increasingly prioritize energy independence and lower utility costs, solar technology continues to advance, offering more efficient and reliable systems. This trend is supported by governmental incentives such as tax rebates and grants, which further reduce the financial burden on end-users and promote the adoption of solar energy.

The robust growth of the solar PV sector within the DG market is indicative of a broader shift towards renewable energy sources, driven by heightened environmental awareness and the global push towards carbon neutrality. As the technology evolves and the cost of solar components continues to decrease, the market share is expected to see continued growth, further cementing solar PV’s role as a cornerstone of distributed generation solutions.

By Power Rating Analysis

The 5 kW to 250 kW power rating segment holds a 37.30% market share.

In 2024, the 5 kW – 250 kW range held a dominant market position in the By Power Rating segment of the Distributed Generation (DG) Market, with a 37.30% share. This segment’s leadership underscores its versatility and wide appeal across various applications, including residential, commercial, and small industrial sites. The power range is particularly suited for those seeking to meet moderate energy needs while gaining independence from traditional grid systems.

The preference for 5 kW to 250 kW systems can be attributed to their ideal balance between affordability and capability. These systems are large enough to significantly offset energy costs and provide reliable power during outages, yet small enough to be accessible and practical for average consumers. Additionally, they fit well within the spatial limitations of small businesses and homes, making them a pragmatic choice for urban and suburban settings.

This segment benefits from the broader trend towards sustainability, where even moderate investments in renewable energy can contribute to reduced carbon emissions and enhanced energy security. The continued growth of this market segment is likely driven by improved technologies that increase the output and efficiency of smaller-scale units, coupled with supportive policies that encourage renewable energy adoption across diverse sectors.

By Application Analysis

On-grid applications lead in the DG market, capturing 74.30% of it.

In 2024, On-grid systems held a dominant market position in the By Application segment of the Distributed Generation (DG) Market, securing a 74.30% share. This predominance in the market illustrates the significant reliance on and integration with the existing utility grid, as on-grid systems provide a seamless blend of traditional and distributed power sources. These systems are particularly favored for their ability to balance power loads during peak times and reduce the overall strain on the grid.

The high adoption rate of on-grid DG systems can be attributed to their economic benefits, such as the potential for selling surplus energy back to the grid through net metering policies. This not only provides financial returns for system owners but also encourages broader participation in renewable energy generation. Moreover, on-grid systems often receive more substantial government incentives compared to off-grid solutions, which further stimulates market growth and adoption.

On-grid DG systems also benefit from advancements in smart grid technology, which optimizes energy distribution and enhances grid stability. This technology allows for more efficient management of energy resources, fostering a more resilient energy infrastructure. The dominance of on-grid applications is likely to persist as these systems continue to offer reliable, efficient, and economically advantageous solutions for integrating distributed generation into the existing energy landscape.

By End-user Analysis

Industrial end-users constitute 43.30% of the DG market’s customer base.

In 2024, the Industrial sector held a dominant market position in the By End-user segment of the Distributed Generation (DG) Market, with a 43.30% share. This leading position highlights the critical role distributed generation systems play in supporting industrial operations, where reliable and continuous power is essential for maintaining productivity and reducing operational interruptions.

The substantial market share of the Industrial segment can be attributed to the increasing adoption of DG systems by manufacturing facilities, processing plants, and other industrial entities aiming to enhance energy efficiency and reduce dependency on the traditional power grid.

Industries often face significant energy demands and cost concerns, making them ideal candidates for adopting DG technologies such as cogeneration systems, which not only provide power but also heat, thereby maximizing energy utilization and minimizing waste.

Additionally, industrial users are increasingly driven by sustainability goals and the need to comply with stringent environmental regulations, which promote the use of renewable energy sources. DG systems, particularly those based on renewable technologies like solar and wind, align well with these objectives by reducing carbon emissions and promoting a more sustainable energy profile.

Key Market Segments

By Technology

- Solar Photovoltaic

- CHP

- Wind Turbines

- Reciprocating Engines

- Micro Turbines

- Fuel Cells

- Others

By Power Rating

- Below 5 kW

- 5 kW – 250 kW

- 250 kW – 1 MW

- Above 1 MW

By Application

- On-grid

- Off-grid

By End-user

- Industrial

- Residential

- Commercial

Driving Factors

Rising Energy Costs Drive DG Adoption

The primary driving factor for the Distributed Generation (DG) Market is the escalating cost of traditional energy. As utility bills continue to rise, both individual consumers and businesses are seeking more cost-effective alternatives to meet their energy needs.

Distributed generation offers a viable solution by enabling users to produce their electricity locally, using sources like solar panels, wind turbines, or biomass systems. This shift not only helps in reducing dependency on the grid but also significantly cuts down energy expenses.

Furthermore, the ability to generate power onsite reduces transmission losses and enhances energy efficiency. As economic pressures mount and renewable technology becomes more accessible, the motivation to switch to distributed generation systems grows stronger, driving the market forward robustly.

Restraining Factors

High Initial Investment Limits DG Market Growth

One of the main restraining factors for the Distributed Generation (DG) Market is the high initial investment required to install these systems. Despite the long-term savings on energy costs, the upfront expenses associated with purchasing and installing DG technologies like solar panels, wind turbines, and other renewable energy systems can be prohibitively high for many potential users.

This financial barrier is particularly challenging for small businesses and residential customers who may not have access to the necessary capital or financing options. While government incentives and decreasing technology costs are helping to mitigate some of these expenses, the initial investment remains a significant hurdle that slows the broader adoption and expansion of distributed generation solutions in various markets.

Growth Opportunity

Technological Advances Open New DG Market Opportunities

A key growth opportunity in the Distributed Generation (DG) Market lies in the ongoing technological advancements in energy systems. Innovations in renewable energy technologies, such as more efficient solar panels, smarter wind turbines, and advanced energy storage solutions, are continuously improving the effectiveness and reducing the cost of DG systems.

These technological improvements not only enhance the performance of existing installations but also make DG more appealing and accessible to a broader range of end-users. As technology progresses, the potential for integrating DG with smart grids and IoT (Internet of Things) devices also expands, offering more sophisticated energy management and distribution capabilities.

Latest Trends

Integration of DG with Smart Grid Technology

A significant trend in the Distributed Generation (DG) Market is the integration of DG systems with smart grid technology. This trend is revolutionizing how energy is distributed and managed across various sectors. Smart grids enable real-time monitoring and control of energy flows from multiple sources, including small-scale, localized DG units. This integration enhances the efficiency and reliability of power supply, facilitating better load balancing and reducing outages.

Moreover, smart grids allow for more dynamic interaction between energy providers and consumers, supporting features like demand response and net metering, where excess power generated by DG systems can be easily fed back into the grid. This synergy between DG and smart technology is setting the stage for a more resilient and adaptive energy infrastructure, driving further adoption of DG solutions.

Regional Analysis

Increased investments and technological advancements propel Asia-Pacific’s USD 110.4 billion DG market forward.

The Distributed Generation (DG) Market demonstrates significant regional diversity, with Asia-Pacific leading as the dominating region. In 2024, Asia-Pacific accounted for 47.30% of the global market, valued at USD 110.4 billion, driven by rapid industrialization and expanding renewable energy initiatives across countries like China, India, and Japan. This region benefits from government policies favoring sustainable energy solutions and increasing investments in renewable energy technologies, positioning it at the forefront of the DG market growth.

In contrast, North America and Europe also show robust market activity, spurred by evolving regulatory landscapes and high consumer awareness about green technologies. North America, with its advanced infrastructure and high technology adoption rates, focuses on modernizing power systems and integrating smart grid solutions. Europe, meanwhile, emphasizes reducing carbon footprints through renewable energy directives and incentives.

Meanwhile, regions like Latin America and the Middle East & Africa, though smaller in market size compared to Asia-Pacific, are experiencing growth due to increasing energy demands and infrastructural developments. These regions are exploring renewable DG options to improve energy access and security, leveraging solar, wind, and biomass technologies to foster sustainable growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Distributed Generation (DG) Market has seen significant contributions from key companies like Alstom S.A., Ballard Power Systems, Bloom Energy, and Capstone Turbine Corporation. Each of these players brings unique strengths and strategies to the market, driving innovation and competition.

Alstom S.A. has continued to enhance its portfolio with efficient and scalable solutions that cater to the growing need for sustainable energy production. Known for its robust engineering and integration capabilities, Alstom has successfully expanded its reach in both developed and emerging markets, focusing on reliable and eco-friendly power generation technologies.

Ballard Power Systems remains a pivotal player in the DG sector, specializing in proton exchange membrane fuel cell technology. Ballard’s commitment to zero-emission energy solutions has positioned it well within the renewable energy market, appealing particularly to sectors looking for clean energy alternatives for transportation and stationary power.

Bloom Energy has made a significant impact with its solid oxide fuel cell technology, which converts natural gas into electricity through an electrochemical process without combustion. The efficiency and relatively lower carbon footprint of Bloom Energy’s systems offer a compelling case for businesses aiming to reduce their reliance on conventional power grids and decrease their environmental impact.

Capstone Turbine Corporation continues to lead with its microturbine technology, providing a versatile and reliable power solution for a variety of industrial, commercial, and residential applications. Capstone’s systems are prized for their low emissions and ability to operate on multiple fuel sources, making them adaptable to diverse energy needs worldwide.

Top Key Players in the Market

- Alstom S.A.

- Ballard Power Systems

- Bloom Energy

- Capstone Turbine Corporation

- Caterpillar

- Destinus Energy

- Doosan Fuel Cell Co. Ltd.

- E.ON SE

- ENERCON Global GmbH

- FuelCell Energy, Inc.

- General Electric

- Mitsubishi Power Americas, Inc.

- Rolls-Royce plc

- Schneider

- Sharp Corporation

- Siemens AG

- Toyota Turbine and Systems Inc.

Recent Developments

- In 2024, Alstom S.A. made significant strides in the Distributed Generation (DG) sector, focusing on expanding its range of high-speed and battery-electric trains, and enhancing its maintenance and signaling technologies. The company achieved a robust order intake of €18.9 billion and sales totaling €17.6 billion, reflecting a solid year-on-year growth and a strong backlog that ensures future sales stability.

- In 2024, Ballard Power Systems experienced a series of ups and downs within the Distributed Generation (DG) sector. Despite facing challenges such as a tough hydrogen and fuel cell market environment and policy uncertainties, Ballard demonstrated resilience by achieving substantial commercial milestones.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 233.5 Billion |

| Forecast Revenue (2034) | USD 799.7 Billion |

| CAGR (2025-2034) | 13.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Solar Photovoltaic, CHP, Wind Turbines, Reciprocating Engines, Micro Turbines, Fuel Cells, Others), By Power Rating (Below 5 kW, 5 kW – 250 kW, 250 kW – 1 MW, Above 1 MW), By Application (On-grid, Off-grid), By End-user (Industrial, Residential, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Alstom S.A., Ballard Power Systems, Bloom Energy, Capstone Turbine Corporation, Caterpillar, Destinus Energy, Doosan Fuel Cell Co. Ltd., E.ON SE, ENERCON Global GmbH, FuelCell Energy, Inc., General Electric, Mitsubishi Power Americas, Inc., Rolls-Royce plc, Schneider, Sharp Corporation, Siemens AG, Toyota Turbine and Systems Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")