Quick Navigation

- Report Overview

- Key Takeaways

- By Stone Analysis

- By Product Type Analysis

- By Method Analysis

- By Technology Analysis

- By Grade Analysis

- By End-User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

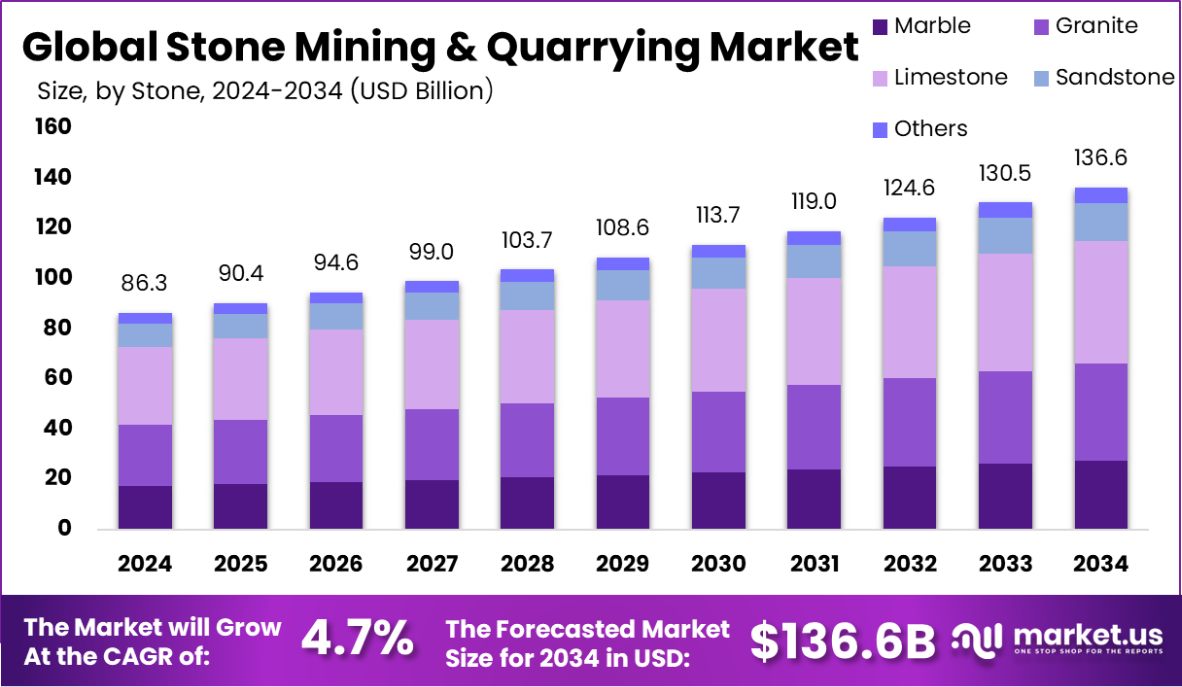

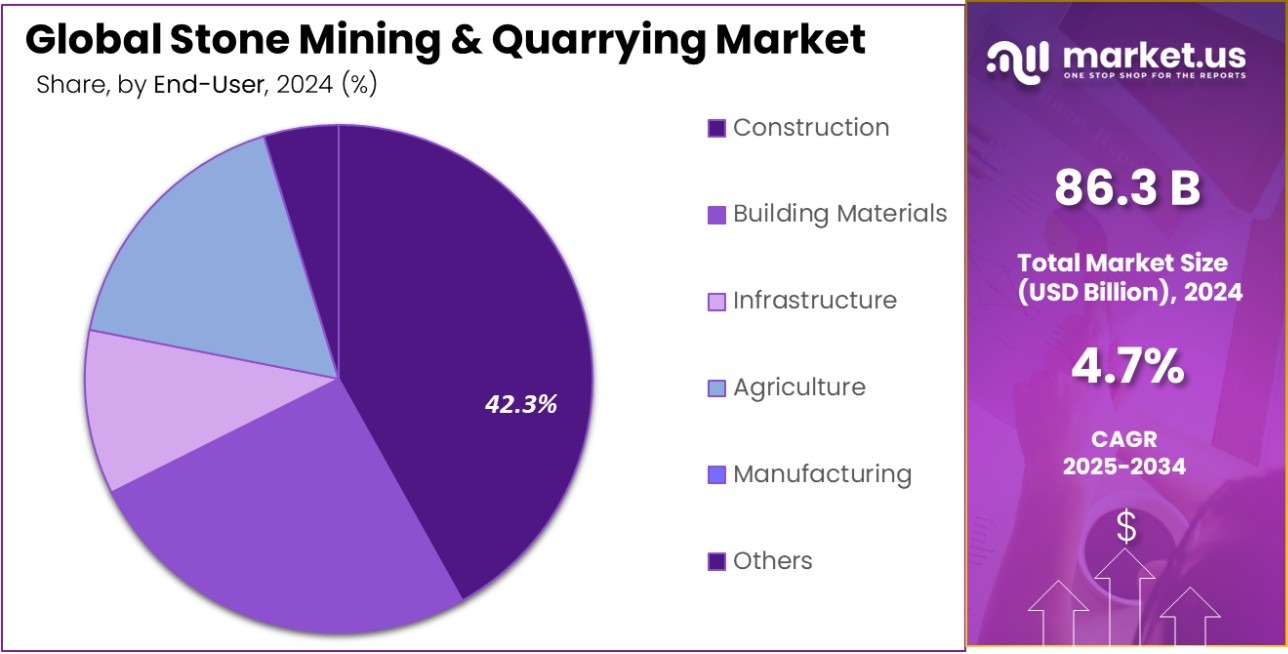

Global Stone Mining & Quarrying Market is expected to be worth around USD 136.6 Billion by 2034, up from USD 86.3 Billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034. North America Leads Stone Market with $33.2 Billion Revenue.

Stone mining and quarrying involve extracting natural stone from the Earth, which is then used in construction, architecture, and various industries. This process can include the extraction of various types of stone such as limestone, granite, marble, and sandstone. The methods of quarrying include drilling, blasting, and cutting the stone out of the natural rock bed, then processing and polishing it for specific uses.

The stone mining and quarrying market refers to the industry and economic segment involved in the extraction and preparation of stone for commercial and industrial use. This market is driven by the demand for building materials in construction projects ranging from residential to commercial infrastructure. The performance of this market is closely tied to trends in the construction sector and is influenced by urban development and infrastructure projects.

One major growth factor for the stone mining and quarrying market is the global increase in construction activities, especially in emerging economies. As urbanization progresses, the demand for new buildings, roads, and infrastructural projects drives the need for raw materials, including stone. Moreover, the restoration and maintenance of historical monuments and structures also contribute to market growth, as natural stone is often required to maintain aesthetic and structural integrity.

The demand in the stone mining and quarrying market is primarily fueled by the construction industry. The aesthetic qualities and durability of natural stone make it a popular choice for decorative exteriors, flooring, monuments, and countertops. Additionally, the development of smart cities and increased investment in infrastructure such as bridges, roads, and public buildings boost the demand for quarried stone.

The stone mining and quarrying market has significant opportunities for advancement through the adoption of environmentally sustainable practices. As environmental regulations tighten, companies have the chance to innovate with more efficient mining and processing technologies that reduce environmental impact.

The Stone Mining & Quarrying Market continues to expand, driven by major producers like Stone Group International, which, along with its affiliated companies, extracts over 250,000 tons of marble blocks annually from nine active quarries. Additionally, India’s limestone production surged to approximately 407 million metric tons in the financial year 2024, reflecting strong regional demand.

Key Takeaways

- Global Stone Mining & Quarrying Market is expected to be worth around USD 136.6 Billion by 2034, up from USD 86.3 Billion in 2024, and grow at a CAGR of 4.7% from 2025 to 2034.

- Limestone dominates the stone mining and quarrying market, holding a substantial 36.4% share by stone type.

- Crushed stone leads product types in the market with a significant 43.2% share, showcasing its widespread use.

- Surface mining is the predominant extraction method, making up 73.6% of operations in the stone quarrying industry.

- Conventional methods continue to lead with 62.2%, reflecting traditional preferences in mining technology and practices.

- High-grade stone, valued for its quality and durability, accounts for 38.4% of the market by grade.

- The construction sector remains the largest end-user of quarried stone, comprising 42.3% of the market.

- Direct sales are the most common distribution channel in this sector, representing 48.3% of stone distribution.

- North America Leads Stone Mining Market with a 36.9% Share, Valued at USD 33.2 Billion.

By Stone Analysis

Limestone dominates the stone segment with a 36.4% share in quarrying.

In 2024, Limestone held a dominant market position in the “By Stone” segment of the Mining & Quarrying Market, with a 36.4% share. This prominence can be attributed to limestone’s extensive application in the construction and manufacturing sectors.

Predominantly used for cement production and as a critical component in the fabrication of building materials such as bricks and concrete, limestone’s demand aligns closely with the construction industry’s growth patterns. The versatility of limestone, suitable for both residential and commercial construction, supports its strong market position.

Additionally, the environmental aspects of limestone, such as its capability to improve soil pH and its use in water treatment, further bolster its demand. As urban development continues to expand, particularly in emerging economies, the need for limestone for infrastructural projects is expected to remain robust.

The stability of limestone’s market share is also reinforced by ongoing investments in infrastructure, which consistently generate a high demand for this essential material. This sector’s growth is further supported by innovations in quarrying technology and sustainable practices that enhance efficiency and reduce environmental impacts.

By Product Type Analysis

Crushed stone leads product types, accounting for 43.2% of the market.

In 2024, Crushed Stone held a dominant market position in the “By Product Type” segment of the Mining & Quarrying Market, with a 43.2% share. This substantial market share underscores crushed stone’s pivotal role in various construction activities, including road building, foundation work, and aggregate in concrete and asphalt production.

The durability and cost-effectiveness of crushed stone make it a preferred choice for both large-scale infrastructure projects and smaller residential developments. The steady expansion of urban environments and ongoing public works, particularly in developing countries, drives the consistent demand for crushed stone.

Furthermore, as economies focus on infrastructure resilience and sustainability, crushed stone is increasingly utilized due to its natural abundance and recyclability, which align with environmental sustainability goals.

The robust market share is also supported by the ongoing developments in quarrying techniques and transportation efficiency, which reduce overall costs and enhance supply chain dynamics. This ensures that crushed stone remains a cornerstone of construction materials, catering to a broad spectrum of construction needs while supporting industry growth and sustainability initiatives.

By Method Analysis

Surface mining is the preferred method, making up 73.6% of operations.

In 2024, Surface Mining held a dominant market position in the “By Method” segment of the Mining & Quarrying Market, with a 73.6% share. This significant market share highlights surface mining’s efficiency and cost-effectiveness compared to other extraction methods.

Surface mining, which includes techniques such as open-pit mining, strip mining, and mountaintop removal, is favored for its ability to access large volumes of minerals and stones near the earth’s surface. This method reduces the need for tunneling and deep earth excavation, leading to lower operational costs and reduced risk for workers.

The dominance of surface mining is further reinforced by technological advancements in equipment and automation, which improve productivity and minimize environmental impact. As regulations around environmental conservation tighten, these innovations help mitigate the ecological disturbances associated with mining activities.

The method’s adaptability to different environments and its capacity for large-scale operations make it indispensable for meeting the growing global demand for building materials and minerals. This ensures that surface mining continues to play a crucial role in the development of the mining and quarrying industry, driving its growth in a competitive market landscape.

By Technology Analysis

Conventional methods are utilized by 62.2% of stone mining technologies.

In 2024, Conventional Methods held a dominant market position in the “By Technology” segment of the Mining & Quarrying Market, with a 62.2% share. This leadership underscores the ongoing reliance on traditional mining techniques that have been refined over decades.

Despite the rise of advanced technologies, conventional methods such as drilling, blasting, and manual sorting remain integral due to their proven effectiveness and straightforward implementation in various geological settings.

These methods are particularly prevalent in regions where the economic justification for high-cost, high-tech solutions is less compelling, or where the regulatory framework supports more traditional approaches.

The robust position of conventional methods is also supported by a workforce skilled in these traditional techniques, ensuring efficiency and safety in operations. Furthermore, in many cases, these conventional methods are less capital-intensive, making them accessible to a wider range of mining operations, including smaller and medium-sized enterprises that might not have the resources to invest in cutting-edge technology.

As the mining industry continues to balance cost, efficiency, and environmental impact, conventional methods are likely to remain a cornerstone of the industry, providing a stable foundation for its ongoing growth and adaptation in the global market.

By Grade Analysis

High-grade stone represents 38.4% of materials used in quarrying projects.

In 2024, High-Grade held a dominant market position in the “By Grade” segment of the Mining & Quarrying Market, with a 38.4% share. This significant share illustrates the substantial demand for high-grade materials in various industrial applications where quality and performance are critical.

High-grade materials, often associated with superior physical and chemical properties, are essential in sectors such as construction, where they ensure the longevity and safety of structures, and in manufacturing, where they contribute to the production of high-quality products.

The preference for high-grade materials is particularly pronounced in advanced economies, where stringent standards for building codes and manufacturing quality drive the need for premium raw materials. Additionally, the trend towards sustainable and green building practices further bolsters the demand for high-grade materials, as they typically offer greater efficiency and lower environmental impact over their lifecycle.

The dominant market share of high-grade materials is also a reflection of technological advancements in mining and processing that allow for more precise extraction and refinement, ensuring the availability of high-quality materials. This ability to consistently meet the high standards demanded by end-users cements the strong position of high-grade materials in the global market.

By End-User Analysis

The construction sector is the largest end-user, consuming 42.3% of output.

In 2024, Construction held a dominant market position in the “By End-User” segment of the Mining & Quarrying Market, with a 42.3% share. This commanding share underscores the critical role of mined and quarried materials such as aggregates, limestone, granite, and sandstone in the construction industry. These materials are foundational for both residential and commercial construction projects, driving demand for robust and durable resources that ensure structural integrity and aesthetic quality.

The construction sector’s reliance on high-quality, readily available raw materials for infrastructure development, including roads, bridges, and buildings, contributes significantly to this dominance. As global urbanization continues to escalate, so does the construction industry’s consumption of these essential materials, maintaining strong market demand. Moreover, advancements in construction technology and increasing investments in infrastructure projects worldwide support sustained growth and demand within this segment.

The strategic importance of the construction industry in the mining and quarrying market is further emphasized by the ongoing development of eco-friendly and sustainable construction practices, which require high-quality materials that adhere to stricter environmental standards.

By Distribution Channel Analysis

Direct sales are the main distribution channel, comprising 48.3% of the market.

In 2024, Direct Sales held a dominant market position in the “By Distribution Channel” segment of the Mining & Quarrying Market, with a 48.3% share. This substantial market share highlights the efficiency and effectiveness of direct sales channels in delivering raw materials directly from quarries and mines to end-users and major construction projects.

The direct sales model is particularly favored for its ability to streamline supply chains, reduce overhead costs, and provide better price control, which is crucial in the highly competitive construction and manufacturing industries.

The preference for direct sales is driven by the need for bulk material purchases, which are common in sectors requiring vast quantities of stone and minerals, such as construction and infrastructure development. By dealing directly with the producers, large-scale buyers can secure more favorable terms and ensure a consistent supply of high-quality materials, which is critical for timely project completion.

Additionally, the direct sales approach allows for stronger relationships between miners and their primary customers, fostering better communication, customized service, and quicker response times to demand fluctuations. This method not only supports operational efficiencies but also enhances customer satisfaction and loyalty, which are key to maintaining a competitive edge in the market.

Key Market Segments

By Stone

- Marble

- Granite

- Limestone

- Sandstone

- Others

By Product Type

- Crushed Stone

- Dimension Stone

- Limestone

- Marble

- Granite

- Sandstone

- Others

By Method

- Surface Mining

- Underground Mining

- Others

By Technology

- Conventional Methods

- Advanced Mining Techniques

- Laser Technologies

- Remote Sensing Technology

By Grade

- High-Grade

- Medium-Grade

- Low-Grade

By End-User

- Construction

- Building Materials

- Infrastructure

- Agriculture

- Manufacturing

- Others

By Distribution Channel

- Direct Sales

- Distribution Centers

- Online Platforms

- Retailers

- Others

Driving Factors

Increased Infrastructure Development Drives Demand

One of the top driving factors for the Stone Mining & Quarrying Market is the global increase in infrastructure development. As countries around the world invest in building new infrastructure and upgrading existing ones, the demand for raw materials like stone escalates significantly.

Stone, being a fundamental component in construction, is extensively used in projects ranging from highways and bridges to residential and commercial buildings. The push for more sustainable and resilient urban development further amplifies the need for high-quality stone products.

As governments and private sectors continue to focus on expanding and enhancing their infrastructural capabilities, the stone mining and quarrying industry experiences robust growth, driven by the foundational needs of these large-scale projects. This demand ensures a steady market for quarry operators and contributes to the overall growth of the mining sector.

Restraining Factors

Environmental Regulations Restrict Quarry Operations

A significant restraining factor for the Stone Mining & Quarrying Market is the stringent environmental regulations that govern quarry operations. As the impact of mining activities on the environment becomes more apparent, governments worldwide are implementing tougher regulations to minimize ecological damage. These regulations can include restrictions on the locations where quarries can operate, the methods used for extraction, and the handling of waste materials.

Compliance with these regulations often requires significant investment in technology and processes that reduce pollution and landscape disruption, which can increase operational costs for mining companies. This regulatory environment can slow down project approvals, limit expansion activities, and increase the cost of quarrying operations, posing challenges to the growth and profitability of the stone mining sector.

Growth Opportunity

Technological Innovations Enhance Quarry Efficiency and Sustainability

A key growth opportunity in the Stone Mining & Quarrying Market lies in the adoption of technological innovations that enhance operational efficiency and sustainability. As technology advances, quarry operators have the opportunity to implement more sophisticated machinery and automation processes that can significantly increase the speed and volume of stone extraction while reducing labor costs and improving safety.

Furthermore, technologies such as drones for site surveying, and software for resource management and logistics optimization, can streamline operations and reduce environmental impact.

This integration of technology not only helps in meeting the regulatory demands for more sustainable practices but also positions businesses to capitalize on the increasing demand for building materials driven by global construction booms, thus presenting a lucrative growth avenue within the industry.

Latest Trends

Green Quarrying Methods Gain Prominence in the Market

One of the latest trends in the Stone Mining & Quarrying Market is the shift towards green quarrying methods. As environmental awareness increases, both consumers and regulatory bodies are demanding more sustainable practices in all industries, including mining.

Green quarrying involves the use of eco-friendly techniques and technologies that reduce the environmental impact of operations. This includes water recycling, using renewable energy sources, dust suppression techniques, and reclaiming mined land for ecological purposes.

Adopting these practices not only helps companies comply with stringent environmental regulations but also improves their public image and market competitiveness. This trend is reshaping the industry as companies innovate to find the balance between operational efficiency and environmental stewardship, creating a sustainable path for future development.

Regional Analysis

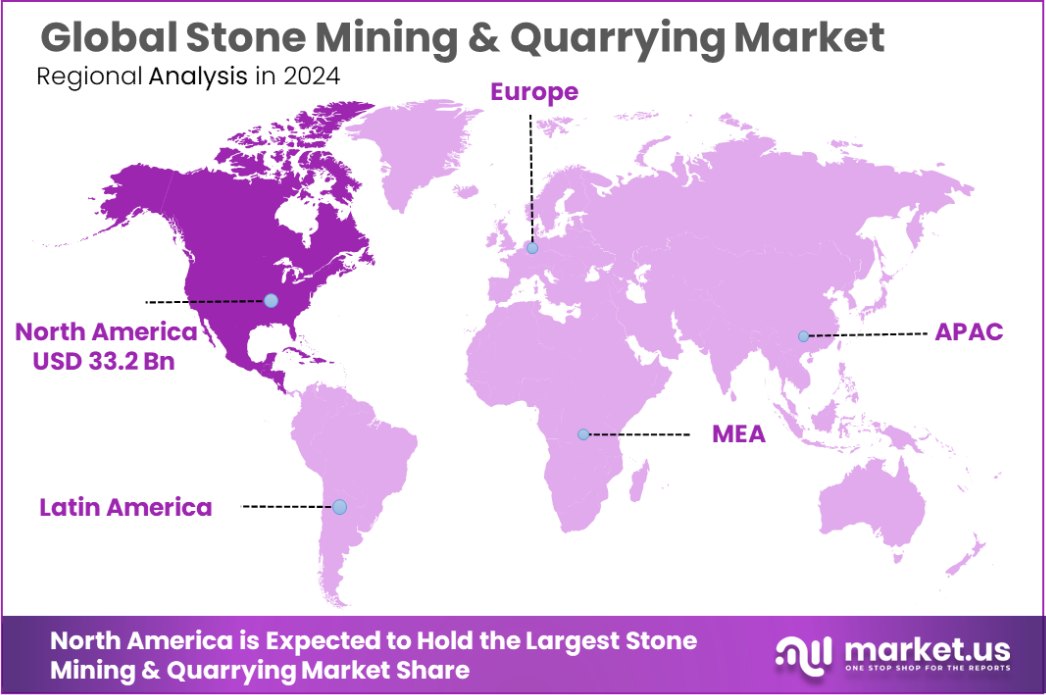

North America Leads Stone Mining Market with a 36.9% Share, Valued at USD 33.2 Billion

In the Stone Mining & Quarrying Market, regional segmentation reveals varied growth dynamics and market sizes across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America emerges as the dominating region, commanding a substantial 36.9% market share, valued at USD 33.2 billion. This significant dominance is driven by robust infrastructure development and stringent regulations that push for sustainable quarry practices.

Europe, with its advanced environmental regulations, focuses on sustainable mining technologies, contributing steadily to the global market. The Asia Pacific region is experiencing rapid growth due to extensive urbanization and industrialization, particularly in countries like China and India, which demand vast quantities of stone for construction and infrastructural projects.

The Middle East & Africa, though smaller in comparison, is seeing increased investments in construction, particularly with developments like smart cities and infrastructure modernization. Latin America, with its rich natural stone reserves, continues to grow moderately, supported by both local and export demands. Overall, North America’s leadership in the market reflects its advanced, efficient quarrying operations and high demand from the construction sector.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Stone Mining & Quarrying Market was significantly influenced by the operations and strategic movements of key players. Among these, Vulcan Materials Company stood out as a leading contributor, capitalizing on its extensive network and operational efficiency to dominate supply chains in various regions.

Similarly, Martin Marietta and CRH Americas maintained strong market positions through strategic acquisitions and expansions, aiming to enhance their geographic footprint and product offerings.

Florida Rock Industries and Lehigh Hanson continued to focus on sustainability practices, integrating more environmentally friendly quarrying methods that resonate well with the current regulatory and environmental trends. This approach not only improved their compliance with global standards but also positioned them as preferred suppliers in the green building materials sector.

Adbri Limited and Carmeuse showed significant agility in adapting to market demands, particularly in the Asia-Pacific and European regions, by scaling operations to meet the high demand for infrastructure and residential construction materials. Cemex, Tarmac, and Oldcastle invested heavily in technology to improve the efficiency of their extraction and processing operations, which proved crucial for maintaining profitability in a competitive market.

Smaller, yet impactful players like Rogers Group Inc., Luck Stone Corp, Polycor, and National Lime & Stone Company focused on niche markets, offering specialized products that cater to unique customer needs, such as high-grade limestone for chemical processing or unique stone for architectural applications.

Mulzer Crushed Stone, Inc. and CRH Company leveraged their local market insights to enhance distribution efficiencies, ensuring quick and reliable supply chains in their respective regional markets. These efforts collectively underline a strategic focus on innovation, sustainability, and customer-centric approaches, driving forward the global Stone Mining & Quarrying Market in 2024.

Top Key Players in the Market

- Vulcan Materials Company

- Florida Rock Industries

- Martin Marietta

- CRH Americas

- Lehigh Hanson

- Adbri Limited

- Carmeuse

- Cemex

- Tarmac

- Oldcastle

- Rogers Group Inc.

- Luck Stone Corp

- Polycor

- National Lime & Stone Company

- Mulzer Crushed Stone, Inc.

- CRH Company

Recent Developments

- In April 2024, Martin Marietta Materials Completed the acquisition of 20 active aggregates operations in Alabama, South Carolina, South Florida, Tennessee, and Virginia from Blue Water Industries LLC for $2.05 billion.

- In February 2024, CRH Americas Completed the acquisition of Martin Marietta Materials’ Texas cement and ready-mixed concrete assets for $2.1 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 86.3 Billion |

| Forecast Revenue (2034) | USD 136.6 Billion |

| CAGR (2025-2034) | 4.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Stone (Marble, Granite, Limestone, Sandstone, Others), By Product Type (Crushed Stone, Dimension Stone, Limestone, Marble, Granite, Sandstone, Others), By Method (Surface Mining, Underground Mining, Others), By Technology (Conventional Methods, Advanced Mining Techniques, Laser Technologies, Remote Sensing Technology), By Grade (High-Grade, Medium-Grade, Low-Grade), By End-User (Construction, Building Materials, Infrastructure, Agriculture, Manufacturing, Others), By Distribution Channel (Direct Sales, Distribution Centers, Online Platforms, Retailers, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Vulcan Materials Company, Florida Rock Industries, Martin Marietta, CRH Americas, Lehigh Hanson, Adbri Limited, Carmeuse, Cemex, Tarmac, Oldcastle, Rogers Group Inc., Luck Stone Corp, Polycor, National Lime & Stone Company, Mulzer Crushed Stone, Inc., CRH Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |