Quick Navigation

Report Overview

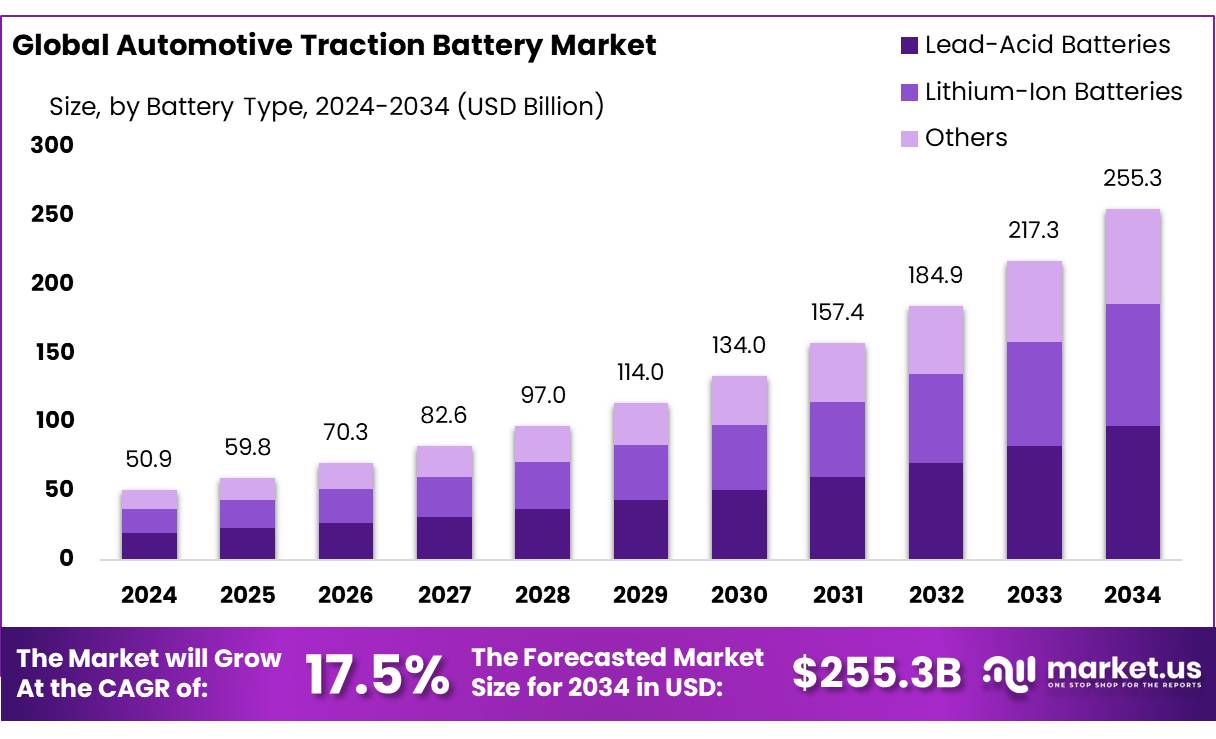

The Global Automotive Traction Battery Market size is expected to be worth around USD 255.3 Bn by 2034, from USD 50.9 Bn in 2024, growing at a CAGR of 17.5% during the forecast period from 2025 to 2034.

The global automotive traction battery market is experiencing rapid growth, primarily driven by the increasing adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs). Traction batteries are essential components in these vehicles, providing the energy needed to power electric motors. Typically lithium-ion-based, these batteries are crucial in determining the performance, driving range, and efficiency of electric and hybrid vehicles. As the automotive industry shifts toward cleaner and more sustainable solutions, the demand for high-performance traction batteries is expected to surge significantly in the coming years.

The growth of the automotive traction battery market reflects a broader shift in consumer preferences and government regulations favoring zero-emission transportation. Major automotive manufacturers such as Tesla, General Motors, Volkswagen, and BYD are heavily investing in electric vehicle production, which has created substantial demand for traction batteries. In parallel, governments around the world are offering incentives and subsidies to support the adoption of EVs and their components, further accelerating market growth.

Several key driving factors are propelling the growth of the automotive traction battery market. Rising concerns over environmental pollution, stringent emission regulations, and the global shift toward sustainable transportation are all contributing to increased demand for electric vehicles. As the automotive industry embraces EV technology, it is helping to reduce carbon emissions compared to traditional gasoline-powered vehicles, making electric mobility a key solution in the fight against climate change.

According to the International Energy Agency (IEA), the number of electric cars on the road surpassed 10 million globally in 2023, with expectations for exponential growth over the next decade. This dramatic increase is driving the demand for traction batteries, as they are essential for the widespread adoption of electric vehicles. With electric vehicles becoming more popular, the need for high-performance batteries continues to grow, positioning traction batteries as a key enabler in the transition to zero-emission mobility.

Advancements in battery technologies are significantly enhancing the performance and efficiency of traction batteries, making electric vehicles more attractive to consumers. Innovations such as solid-state batteries, lithium-sulfur batteries, and other next-generation technologies are poised to revolutionize the automotive traction battery market. These advancements promise higher energy densities, faster charging times, and lower production costs, all of which will contribute to the broader adoption of electric vehicles.

Key Takeaways

- Automotive Traction Battery Market size is expected to be worth around USD 255.3 Bn by 2034, from USD 50.9 Bn in 2024, growing at a CAGR of 17.5%.

- Lead-Acid Batteries held a dominant market position, capturing more than a 38.3% share.

- Prismatic batteries held a dominant market position, capturing more than a 54.3% share.

- 50-100 kWh capacity segment held a dominant market position, capturing more than a 44.3% share.

- Battery Electric Vehicles (BEVs) held a dominant market position, capturing more than a 68.4% share.

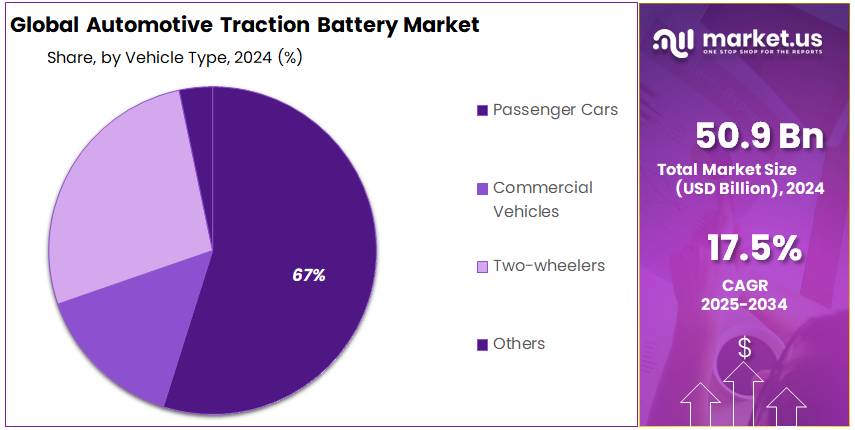

- Passenger Cars held a dominant market position, capturing more than a 67.3% share.

- OEMs (Original Equipment Manufacturers) held a dominant market position in the automotive traction battery sector, capturing more than a 76.4% share.

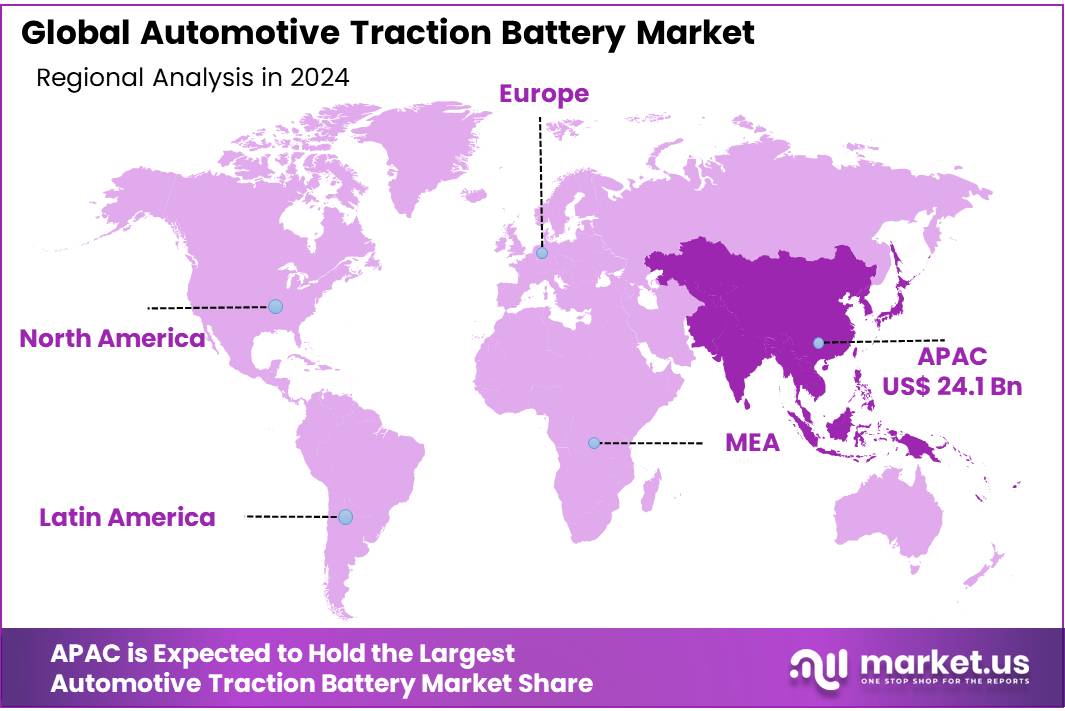

- Asia Pacific (APAC) held the dominant position in the automotive traction battery market, capturing more than 47.5% of the total market share, valued at approximately $24.1 billion.

By Battery Type

In 2024, Lead-Acid Batteries held a dominant market position, capturing more than a 38.3% share of the automotive traction battery market. Despite the growing adoption of lithium-ion batteries, lead-acid batteries continue to maintain their significant presence, particularly in lower-cost and legacy automotive applications. Their popularity is driven by their well-established technology, cost-effectiveness, and reliability. Lead-acid batteries are widely used in traditional internal combustion engine (ICE) vehicles for starting, lighting, and ignition (SLI) applications, as well as in certain hybrid and electric vehicle (EV) configurations where cost is a crucial factor.

lithium-ion batteries are increasingly becoming the go-to option for more advanced and high-performance automotive applications, particularly in electric vehicles. Lithium-ion batteries are expected to account for a substantial share of the market, growing rapidly due to their higher energy density, longer lifespan, and more efficient performance in both passenger and commercial electric vehicles.

By Battery Form

In 2024, Prismatic batteries held a dominant market position, capturing more than a 54.3% share of the automotive traction battery market. Prismatic cells are widely preferred for their efficient use of space, making them ideal for electric vehicles (EVs) where maximizing the battery’s energy density and providing a compact yet high-performance solution are critical. The flat, rectangular design of prismatic batteries allows for easier integration into the vehicle’s chassis, making them a popular choice for both passenger cars and commercial EVs.

While prismatic batteries dominate the market, cylindrical and pouch battery types are also gaining traction. Cylindrical batteries are known for their reliability and safety features, making them suitable for specific applications such as high-performance EVs.

pouch cells offer flexibility and lighter weight, which makes them attractive in certain design-oriented EV models. However, these two segments remain smaller compared to prismatic batteries, which offer a more balanced combination of performance, energy density, and ease of manufacturing scalability. As the market grows, prismatic cells are expected to continue their lead, though innovation in cylindrical and pouch designs may slowly carve out their share.

By Capacity

In 2024, the 50-100 kWh capacity segment held a dominant market position, capturing more than a 44.3% share of the automotive traction battery market. This capacity range is highly popular for mid-range electric vehicles (EVs) that offer a balanced combination of range, performance, and affordability. EVs in this category typically cover 300 to 400 kilometers on a single charge, making them suitable for daily commuting and long-distance travel.

The 50-100 kWh segment’s dominance is further supported by the continuous advancements in battery technology, such as improvements in energy density and cost reduction, which make this range more efficient and affordable for both manufacturers and consumers. Additionally, government incentives and regulatory pressures to reduce carbon emissions are encouraging more manufacturers to produce EVs in this category, leading to an increasing number of new models entering the market. By 2025, it is expected that the 50-100 kWh segment will continue to lead, as it provides the optimal balance of range and price for the majority of the electric vehicle market.

The less than 50 kWh segment primarily serves smaller, budget-friendly EVs, while the 100-200 kWh and more than 200 kWh segments cater to premium and luxury vehicles, as well as commercial electric vehicles that require extended driving ranges. However, it is clear that the 50-100 kWh range will remain the most significant segment in the automotive traction battery market through 2025, given its versatility and broad consumer appeal.

By Propulsion Type

In 2024, Battery Electric Vehicles (BEVs) held a dominant market position, capturing more than a 68.4% share of the automotive traction battery market. This significant market share is driven by the growing consumer preference for fully electric vehicles due to their zero emissions, lower operating costs, and advancements in battery technology. BEVs offer long-range capabilities, fast charging options, and are supported by expanding charging infrastructure, which has further boosted their adoption. The increasing emphasis on sustainability, government incentives, and stricter emission regulations are key factors contributing to the rapid growth of BEVs in the automotive market.

Plug-In Hybrid Electric Vehicles (PHEVs) are also experiencing growth, though at a slower pace. PHEVs, which combine an internal combustion engine with an electric motor, are gaining traction in markets where range anxiety is still a concern, offering drivers the flexibility of both electric and gasoline-powered driving. However, the BEV segment continues to outpace PHEVs as the global automotive industry moves towards full electrification, with governments around the world setting ambitious goals for phasing out internal combustion engine vehicles in the coming decades.

By Vehicle Type

In 2024, Passenger Cars held a dominant market position, capturing more than a 67.3% share of the automotive traction battery market. This is largely driven by the increasing consumer shift towards electric vehicles (EVs) as the preferred mode of transportation. As governments around the world tighten emissions regulations and offer incentives for cleaner alternatives, the demand for battery electric passenger vehicles (BEVs) continues to surge. Key factors contributing to this growth include advancements in battery technology, such as improved energy density and reduced charging times, making BEVs more practical for everyday use.

The commercial vehicle segment is also seeing growth but at a slower pace. While electric buses and trucks are gaining traction, the higher upfront costs and the need for larger battery capacities make it more challenging for fleet operators to transition from traditional fuel sources to electric power. The two-wheeler segment, while smaller, is growing rapidly in markets like Asia-Pacific, where electric scooters and motorcycles are becoming more common as affordable, energy-efficient alternatives to gasoline-powered vehicles. However, passenger cars will continue to lead the automotive traction battery market, as they offer the broadest market appeal and the strongest growth potential in the coming years.

By End-User

In 2024, OEMs (Original Equipment Manufacturers) held a dominant market position in the automotive traction battery sector, capturing more than a 76.4% share. This is primarily due to the rapid growth in the electric vehicle (EV) market, with major automakers increasingly integrating electric powertrains into their new vehicle models. As global automakers scale up their production of electric vehicles, they require a significant number of high-performance traction batteries for their OEM vehicles.

The aftermarket segment, while smaller, is also showing signs of growth. As more electric and hybrid vehicles enter the market, there is an increasing need for replacement parts, including traction batteries, for vehicle maintenance and upgrades. However, the aftermarket segment remains a secondary focus compared to OEM production, as it is driven by a smaller customer base, typically consisting of fleet operators and individual vehicle owners.

Key Market Segments

By Battery Type

- Lead-Acid Batteries

- Wet Cell

- Maintenance-Free

- Absorbent Glass Mat (AGM)

- Gel Cell

- Others

- Lithium-Ion Batteries

- Lithium Cobalt Oxide (LCO)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Manganese Cobalt Oxide (NMC)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Lithium Iron Phosphate (LFP)

- Lithium Titanate Oxide (LTO)

- Others

By Battery Form

- Prismatic

- Pouch

- Cylindrical

By Capacity

- Less than 50 kWh

- 50-100 kWh

- 100-200 kWh

- More than 200 kWh

By Propulsion Type

- Battery Electric Vehicle (BEV)

- Plug-In Hybrid Electric Vehicle (PHEV)

By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV

- Others

- Commercial Vehicles

- Light Duty Vehicles

- Heavy Duty Vehicles

- Two-wheelers

- Others

By End-user

- OEMs

- Aftermarket

Drivers

Growing Demand for Electric Vehicles (EVs) Driven by Government Policies and Consumer Awareness

In 2024, the global electric vehicle market is expected to continue its strong growth trajectory, with significant adoption in both developed and emerging markets. According to the International Energy Agency (IEA), the global EV stock surpassed 16.5 million units in 2023, with the number expected to grow exponentially in the coming years as more countries aim to achieve net-zero carbon emissions targets by 2050. For example, in 2023, over 10% of all new cars sold globally were electric vehicles.

Governments are at the forefront of encouraging EV adoption through tax credits, rebates, and other financial incentives. In the United States, for instance, the federal government’s 2023 Inflation Reduction Act provides substantial tax credits for EV buyers, helping to reduce the initial purchase cost. Similar initiatives are being implemented in Europe, where countries like Norway, the Netherlands, and Germany offer attractive incentives for EV buyers, ranging from tax exemptions to subsidies for electric car purchases.

According to the European Automobile Manufacturers’ Association (ACEA), the European market saw a 25% increase in EV sales in 2023 compared to the previous year, further solidifying the role of government support in this transition.

Additionally, China, the world’s largest car market, has committed to accelerating the adoption of EVs as part of its plan to peak carbon emissions before 2030. In 2023, more than 6 million electric vehicles were sold in China, accounting for nearly 25% of global EV sales. The Chinese government has implemented strong incentives, including subsidies for EV purchases and a goal to have new energy vehicles (NEVs) account for 20% of all new car sales by 2025.

As the number of EVs on the road increases, so too does the demand for automotive traction batteries. These batteries, primarily lithium-ion (Li-ion) types, are central to EV functionality and account for a significant portion of vehicle production costs. According to a report from the U.S. Department of Energy, the cost of lithium-ion batteries has decreased by over 85% since 2010, from around $1,100 per kilowatt-hour (kWh) to below $100 per kWh by 2023. This price reduction is making electric vehicles more affordable for consumers and further fueling demand.

Restraints

High Costs of Battery Production and Raw Materials

The cost of key components, such as lithium, cobalt, and nickel, remains a major challenge for the electric vehicle (EV) industry. These materials are essential for lithium-ion batteries, the most commonly used type of traction battery in electric vehicles. As demand for EVs grows, the pressure on the supply chain for these critical materials intensifies, driving up their prices and, in turn, the cost of batteries.

In 2024, the price of lithium has been particularly volatile. According to the U.S. Geological Survey (USGS), the average price of lithium carbonate surged by more than 500% from 2020 to 2023, largely due to a global shortage of this essential material. While prices have begun to stabilize, they remain a significant burden on manufacturers, making it difficult for electric vehicle producers to lower the price of EVs. In fact, raw material costs now account for a substantial portion of the total cost of manufacturing lithium-ion batteries.

A report by the International Energy Agency (IEA) indicates that raw materials account for nearly 50-60% of the total cost of battery production, depending on the battery type and design. This high cost of raw materials is one of the biggest obstacles to making EVs affordable for the average consumer.

Similarly, cobalt, which is another critical material used in lithium-ion batteries, has seen significant price fluctuations. The Democratic Republic of Congo (DRC) is the largest producer of cobalt, and the political instability in the region, coupled with increasing global demand, has led to price hikes. This volatility has raised concerns about the security of supply and the ethical implications of sourcing cobalt from conflict-prone areas. In fact, some automakers and battery manufacturers are exploring alternatives to cobalt to reduce their reliance on this material, but these alternatives are often more expensive or less efficient.

Governments around the world are aware of the challenges posed by high battery costs and have introduced various initiatives to help address this issue. In the United States, the Biden administration has proposed significant investments in critical minerals and battery manufacturing as part of its broader plan to strengthen the domestic EV supply chain. According to a report from the U.S. Department of Energy, the administration has allocated billions of dollars to boost the mining and processing of critical minerals like lithium, cobalt, and nickel. This is part of a broader effort to reduce the dependency on foreign sources and stabilize the supply of raw materials.

Opportunity

Advancements in Battery Recycling and Second-Life Applications

One of the most promising growth opportunities for the automotive traction battery market is the continued development of battery recycling technologies and second-life applications for used batteries. As electric vehicle (EV) adoption grows globally, the demand for batteries is surging, leading to an increase in the number of end-of-life batteries that will eventually require recycling or repurposing. Efficient battery recycling is crucial not only for reducing the environmental impact of used batteries but also for minimizing the reliance on raw materials, which are often sourced from politically unstable regions and are subject to price volatility.

Rising Demand for Battery Recycling

The global push for sustainability and the reduction of carbon emissions has driven significant investments in EVs and renewable energy systems. According to the U.S. Department of Energy (DOE), the number of EVs on the road in the U.S. is expected to exceed 18 million by 2030, which will significantly increase the number of used automotive batteries in circulation. In fact, the market for recycled lithium-ion batteries is projected to reach $12 billion by 2030, growing at a compound annual growth rate (CAGR) of over 20% from 2023 levels, driven by both the expansion of EVs and renewable energy storage.

The environmental impact of mining critical raw materials like lithium, cobalt, and nickel for batteries is another reason why battery recycling has gained attention. For example, it is estimated that over 70% of the world’s cobalt comes from the Democratic Republic of Congo (DRC), a region rife with political instability and human rights issues. By focusing on recycling, the automotive industry can reduce its reliance on such sources, improving both environmental and ethical aspects of the supply chain. The European Commission has already set a target to recycle 35% of lithium-ion batteries by 2030, aiming for this number to rise to 50% by 2040. This type of regulation is encouraging automakers to invest in closed-loop recycling systems that will allow them to reuse raw materials from used batteries in the production of new ones.

Second-Life Applications for Automotive Batteries

In addition to recycling, another growth opportunity lies in the second-life applications of used automotive traction batteries. These batteries still have significant remaining capacity after their use in vehicles, but they may no longer meet the high standards required for EV propulsion. However, they can still be repurposed for less-demanding applications, such as energy storage for homes, businesses, or grid stabilization.

According to the International Energy Agency (IEA), the second-life battery storage market could grow from $0.5 billion in 2020 to over $2 billion by 2025. This market offers automakers and battery manufacturers an opportunity to generate additional revenue streams by repurposing EV batteries for renewable energy storage. Major automakers, such as BMW and Nissan, have already begun collaborating with energy companies to explore the use of used EV batteries for stationary energy storage systems. For example, BMW’s “Second Life” project in partnership with Vattenfall aims to create a large-scale energy storage solution using used EV batteries to help stabilize the electricity grid.

Furthermore, governments are also supporting second-life battery projects. The European Union, through its Horizon 2020 program, has provided funding for several initiatives focused on the development of battery recycling and second-life applications. In 2020, the EU launched a project called “Battery 2030+” that aims to accelerate innovations in battery design, recycling, and second-life usage. Such initiatives will help create a circular economy for EV batteries, where materials are reused rather than disposed of, significantly reducing the environmental impact and creating new business models for automakers and battery manufacturers.

Supportive Government Policies

Governments worldwide are recognizing the importance of battery recycling and second-life applications in the overall push towards sustainability. In addition to EU regulations, the U.S. government has introduced policies aimed at advancing battery recycling infrastructure. The U.S. Department of Energy (DOE) has committed $15 million in funding for research into advanced battery recycling technologies. The DOE’s “Lithium-Ion Battery Recycling Prize,” which offers financial rewards to companies that develop innovative recycling solutions, is one example of how public-private partnerships can drive industry growth.

In China, the government has also prioritized the development of battery recycling capabilities, with the country expected to be the largest recycler of lithium-ion batteries by 2030, according to a report from the Chinese Battery Industry Association. As the world’s largest EV market, China is heavily investing in building infrastructure to recycle batteries at scale. This includes collaborations between automakers and tech companies to set up battery recycling plants, ensuring a steady supply of reusable materials for new batteries.

Trends

The Rise of Solid-State Batteries in the Automotive Traction Market

One of the most exciting and transformative trends in the automotive traction battery market is the rapid development and potential integration of solid-state batteries (SSBs). Solid-state batteries, which replace the traditional liquid electrolyte found in lithium-ion batteries with a solid electrolyte, are expected to revolutionize electric vehicle (EV) technology. These batteries offer numerous advantages, including higher energy density, greater safety, and faster charging times, all of which address some of the primary concerns of EV users and manufacturers.

The Shift to Solid-State Batteries

In 2024, there has been significant progress in the research and development of solid-state battery technologies, driven by the increasing demand for longer-range, quicker-charging electric vehicles. Traditional lithium-ion batteries, while efficient, are limited by their relatively low energy density and vulnerability to overheating or catching fire due to the flammable liquid electrolytes they contain. Solid-state batteries, on the other hand, are expected to offer up to 2-3 times the energy density of conventional lithium-ion batteries. This could result in EVs that can travel farther on a single charge, addressing one of the most significant barriers to EV adoption: range anxiety.

Growing Industry Interest and Investments

Global automakers and battery manufacturers are investing heavily in solid-state battery research. Toyota, a leader in the automotive industry, has made significant strides in this field, with the company projecting to launch solid-state batteries in their EV models by 2025. In 2024, Toyota increased its investment in solid-state battery technology by over $100 million, highlighting the company’s commitment to this transformative technology. Similarly, companies like Volkswagen, BMW, and QuantumScape are accelerating their efforts to commercialize solid-state batteries. QuantumScape, a pioneer in solid-state technology, has reported that it is on track to achieve solid-state battery production by 2025, with a potential to drastically reduce charging times and extend the driving range of electric vehicles.

Key Benefits of Solid-State Batteries

The energy density of solid-state batteries means that they can store more energy in the same amount of space, which is crucial for EVs that need high-capacity batteries to achieve long driving ranges. For instance, current lithium-ion batteries typically offer energy densities of around 150-250 Wh/kg, while solid-state batteries have the potential to reach 500 Wh/kg or more. This increase in energy density could allow EVs to travel up to 800-1,000 kilometers on a single charge, significantly extending the range compared to most current models, which average between 300-400 kilometers.

Additionally, solid-state batteries offer enhanced safety. Because they use solid electrolytes, they are less prone to leakage, combustion, or thermal runaway, which are known issues with liquid-based lithium-ion batteries. This makes them safer for use in vehicles, reducing the risks of fires that can occur under certain conditions with traditional batteries.

Impact of Government Initiatives

Governments around the world are recognizing the importance of advancing battery technology and are providing financial support to further the development of solid-state batteries. In the United States, the Department of Energy (DOE) has invested over $200 million in battery research, including solid-state battery technology. The Advanced Research Projects Agency-Energy (ARPA-E), a division of the DOE, funds multiple projects aimed at developing more efficient and safer battery technologies for use in transportation. In Europe, the European Battery Alliance (EBA), led by the European Commission, is focused on building a sustainable and competitive battery industry, with a significant portion of its funds directed toward innovative solutions such as solid-state batteries.

Moreover, China, which is already a leader in EV production and sales, is investing heavily in battery research. The country’s Made in China 2025 initiative includes a focus on the development of advanced battery technologies, including solid-state batteries. By 2025, China aims to become a global leader in solid-state battery production, with substantial investments in both research and manufacturing infrastructure. This commitment by leading countries and organizations further drives the growth of solid-state batteries in the automotive traction market.

Regional Analysis

In 2024, Asia Pacific (APAC) held the dominant position in the automotive traction battery market, capturing more than 47.5% of the total market share, valued at approximately $24.1 billion. The region’s leadership is largely driven by the rapid growth of electric vehicle (EV) production, especially in countries like China, Japan, and South Korea. China, being the largest market for EVs globally, accounts for a significant portion of the demand for automotive traction batteries. The Chinese government’s strong push towards electrification, supported by favorable policies and incentives, has accelerated the adoption of EVs and, in turn, the demand for high-performance traction batteries.

North America follows as a key market, with a market share of approximately 22.1%. The United States, in particular, is witnessing a surge in electric vehicle sales, driven by initiatives such as the Biden Administration’s EV Incentives Program and the Infrastructure Investment and Jobs Act, which includes significant funding for EV infrastructure. The demand for automotive traction batteries is expected to continue growing as automakers ramp up their production of electric vehicles, with companies like Tesla and General Motors at the forefront of this transformation.

Europe is also a significant player, holding a market share of around 18.9%. The European Union’s stringent emission regulations and substantial investments in green technologies have led to a surge in EV adoption, particularly in countries like Germany, France, and Norway. As European automakers such as Volkswagen, BMW, and Renault increase their EV offerings, the demand for traction batteries is expected to rise sharply.

The Middle East & Africa (MEA) and Latin America have relatively smaller market shares but are expected to see growth in the coming years as electric mobility starts to gain traction in these regions. Governments are increasingly focusing on reducing emissions and promoting sustainable transportation solutions, which will drive the demand for automotive traction batteries in these regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global automotive traction battery market is highly competitive, with several key players leading the industry. GS Yuasa International Ltd., Contemporary Amperex Technology Co., Ltd. (CATL), and BYD Company Ltd. are some of the dominant companies in the market. CATL, based in China, is a major supplier of lithium-ion batteries, serving both electric vehicle manufacturers and renewable energy storage systems. BYD is another significant player, focusing on manufacturing electric vehicles and batteries, with a strong presence in China. GS Yuasa, a Japanese company, is known for its advanced battery technology used in various industries, including automotive, and continues to innovate in the traction battery sector.

LG Energy Solution, Panasonic Corp., and SK Innovation Co., Ltd., each contributing significantly to the market through their high-performance battery solutions. LG Energy Solution and Samsung SDI are leaders in the global supply of lithium-ion batteries for EVs, with major partnerships with top automakers like General Motors and BMW. Panasonic, in collaboration with Tesla, has been pivotal in advancing battery technologies, particularly in the electric vehicle sector. SK Innovation, based in South Korea, is expanding its footprint globally, focusing on increasing its capacity to supply batteries for the rapidly growing EV market.

Toshiba Corporation, Exide Group, EnerSys, and East Penn Manufacturing. Toshiba is known for its next-generation lithium-ion technologies, while Exide and EnerSys are key suppliers of batteries for industrial and automotive applications. Companies like Mitsubishi Corp., Leoch International Technology Ltd., and CALB Group Co Ltd also play significant roles in the market, with continued investments in battery research and production capabilities. Collectively, these companies are shaping the future of the automotive traction battery market through technological advancements, strategic partnerships, and global expansions.

Top Key Players

- GS Yuasa International Ltd.

- Contemporary Amperex Technology Co., Ltd. (CATL)

- BYD Company Ltd.

- LG Energy Solution

- Panasonic Corp.

- SK Innovation Co., Ltd.

- Toshiba Corporation

- Exide Group

- EnerSys

- Samsung SDI

- Hitachi, Ltd.

- Mitsubishi Corp.

- East Penn Manufacturing

- CALB Group Co Ltd

- Leoch International Technology Ltd

- Other Key Players

Recent Developments

In 2024 GS Yuasa International Ltd, is expected to generate over ¥500 billion in revenue, with a strong focus on the automotive and industrial sectors. They have been investing heavily in expanding their lithium-ion battery production, aiming to increase production capacity by 25% in the coming years.

In 2024 BYD Company Ltd., is projected to report revenues exceeding ¥400 billion, with a significant portion coming from its battery and electric vehicle sectors. BYD has been rapidly expanding its battery production capacity, with a goal to increase output by 30% by the end of 2024, further solidifying its leadership in the global EV and battery markets.

In 2024, LG Energy Solution is expected to generate approximately $25 billion in revenue, with a significant portion coming from its automotive battery division.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 50.9 Bn |

| Forecast Revenue (2034) | USD 255.3 Bn |

| CAGR (2025-2034) | 17.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery Type (Lead-Acid Batteries, Lithium-Ion Batteries), By Battery Form (Prismatic, Pouch, Cylindrical), By Capacity (Less than 50 kWh, 50-100 kWh, 100-200 kWh, More than 200 kWh), By Propulsion Type (Battery Electric Vehicle (BEV), Plug-In Hybrid Electric Vehicle (PHEV)), By Vehicle Type (Passenger Cars, Commercial Vehicles), By End-user (OEMs, Aftermarket) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | GS Yuasa International Ltd, Contemporary Amperex Technology Co., Ltd. (CATL), BYD Company Ltd., LG Energy Solution, Panasonic Corp., SK Innovation Co., Ltd., Toshiba Corporation, Exide Group, EnerSys, Samsung SDI, Hitachi, Ltd., Mitsubishi Corp., East Penn Manufacturing, CALB Group Co Ltd, Leoch International Technology Ltd, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |